Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

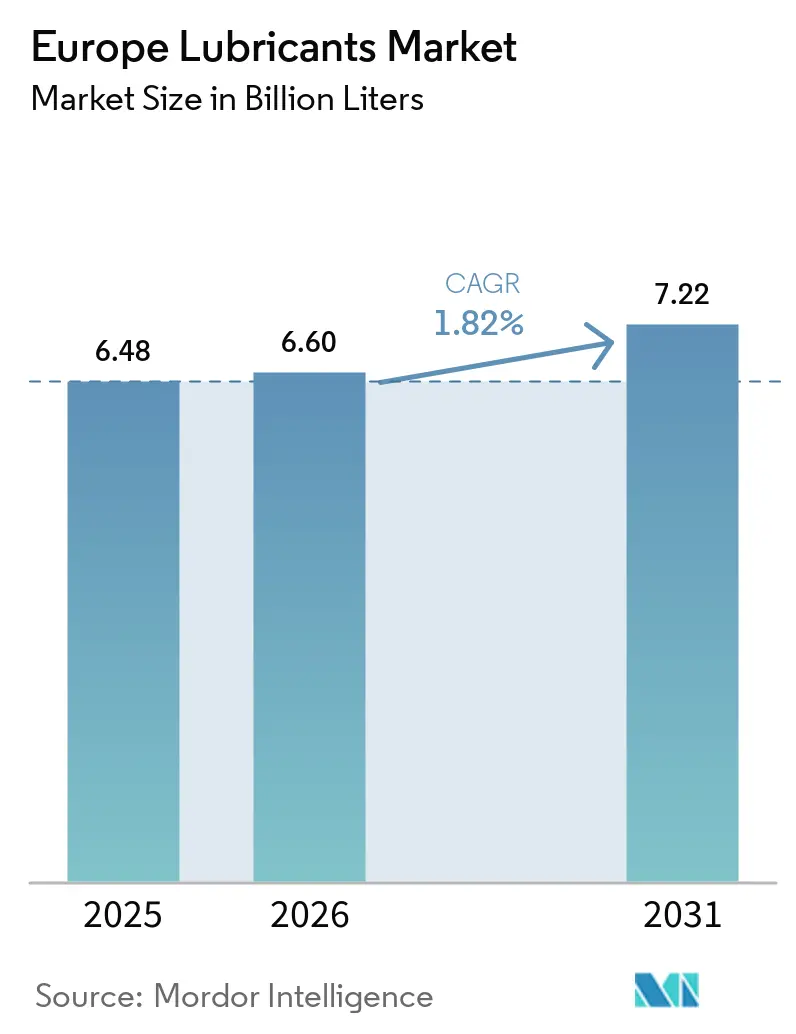

| Base Year Market Size (2025) | 6.48 Billion Liters |

| Market Volume (2026) | 6.60 Billion Liters |

| Market Volume (2031) | 7.22 Billion Liters |

| Growth Rate (2026 - 2031) | 1.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Lubricants Market Analysis by Mordor Intelligence

The Europe Lubricants Market size is expected to grow from 6.48 Billion Liters in 2025 to 6.60 Billion Liters in 2026 and is forecast to reach 7.22 Billion Liters by 2031 at 1.82% CAGR over 2026-2031. Volume growth is running ahead of value as producers shift toward high-margin specialty blends that cater to electrified drivetrains, wind-farm gearboxes, and circular-economy mandates. The automotive aftermarket continues to drive demand, as Europe’s 252-million-unit passenger car fleet averages 12.5 years, a record age that increases oil consumption per vehicle. Bio-based hydraulic and gear oils are gaining momentum in offshore wind and forestry applications, accelerating the move away from conventional mineral formulations. Integrated oil majors maintain dominance in terms of volume, while independent blenders are gaining market share in high-performance greases and re-refined base stocks that meet Group III performance standards.

Key Report Takeaways

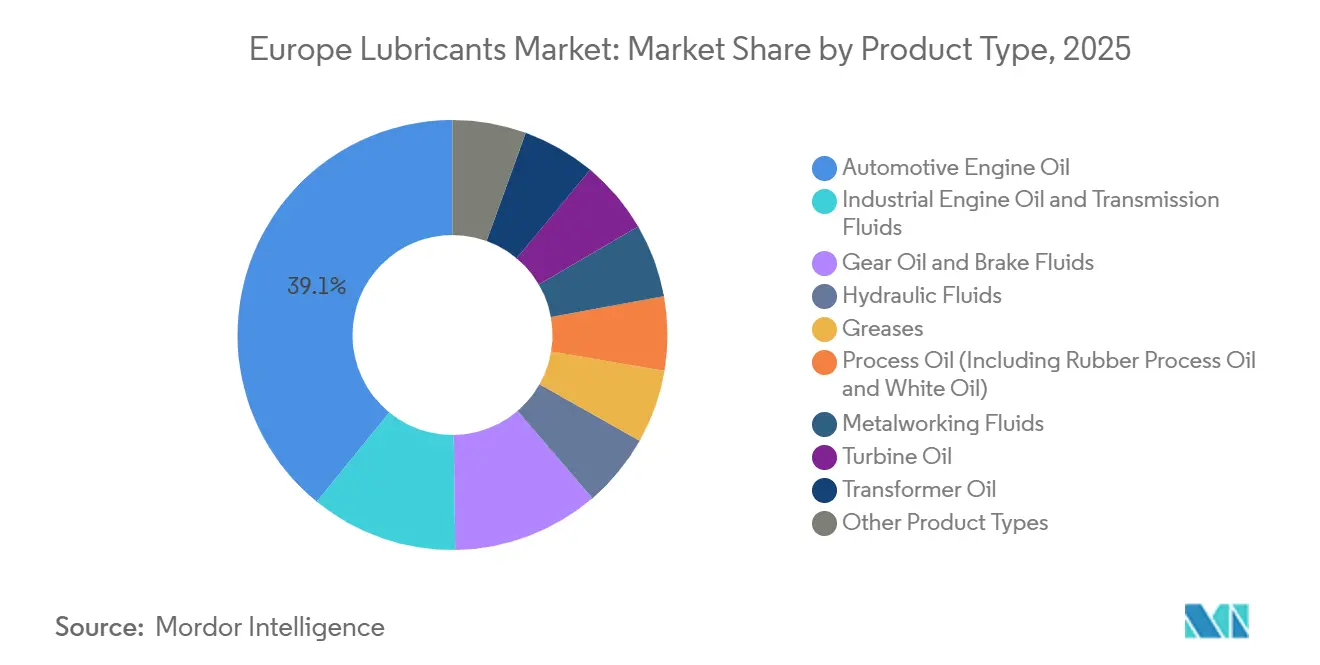

- By product type, automotive engine oil led with 39.12% of the Europe lubricants market share in 2025, while greases are forecast to post the fastest expansion at a 2.07% CAGR through 2031.

- By base stock type, mineral oil-based lubricants captured 60.11% of the Europe lubricants market share in 2025, yet bio-based lubricants are projected to grow at a 3.12% CAGR through 2031.

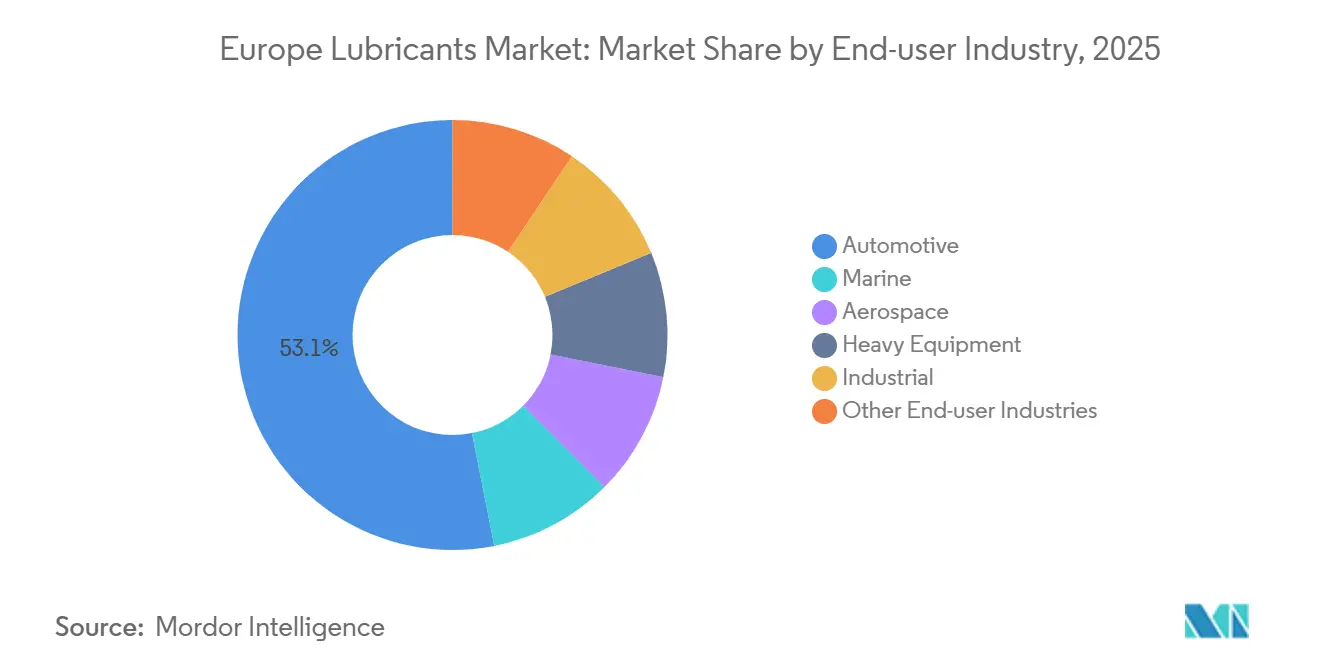

- By end-user industry, the automotive segment accounted for 53.11% of the Europe lubricants market share in 2025; the industrial segment shows the quickest trajectory, advancing at 2.33% CAGR through 2031.

- By geography, the Rest of Europe segment commanded 31.34% of the Europe lubricants market share in 2025, while Russia is expected to record the highest growth at 2.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial rebound and automation surge in CEE | +0.3% | Poland, Czech Republic, Hungary, Romania | Medium term (2-4 years) |

| Post-pandemic vehicle-parc recovery | +0.4% | Germany, France, Italy, Spain, UK | Short term (≤ 2 years) |

| Offshore-wind build-out needs gear and hydraulic lubes | +0.2% | North Sea (UK, Germany, Netherlands, Denmark) | Long term (≥ 4 years) |

| Circular-economy mandates for re-refined base oils | +0.2% | EU-wide, early adoption in Germany, France, Netherlands | Medium term (2-4 years) |

| AI-enabled predictive-maintenance boosting service fluids | +0.2% | Germany, France, UK industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Rebound And Automation Surge In CEE

Manufacturing output in Central and Eastern Europe saw robust growth in 2025, highlighted by a 4.2% rise in Poland’s industrial production index and an 8% expansion in the Czech component sector supplying German OEMs. This growth has driven demand for metalworking fluids used in precision machining of battery housings and motor laminations. Hungary secured EUR 1.8 billion (USD 1.95 billion) in battery-plant investments during 2024-2025, with each gigafactory requiring heat-transfer and hydraulic oils for automated production lines. Industry 4.0 upgrades in Romanian mills and Polish foundries have increased the need for turbine and compressor lubricants, which support sensor-driven maintenance. Buyers are increasingly demanding ISO 12925-1 cleanliness standards for hydraulic systems, embedding lubricant quality into procurement decisions. These developments collectively boost both volume and margins in the industrial fluids market.

Post-Pandemic Vehicle-Parc Recovery

Europe’s car fleet reached 252 million units in 2025, maintaining its status as the oldest globally, with an average age of 12.5 years[1]ACEA, “Passenger Car Fleet 2025,” acea.auto . Older engines continue to consume more oil, supporting aftermarket sales despite a shift in new registrations toward hybrids and battery-electric vehicles. Diesel vehicles still make up 40% of the fleet, necessitating the coexistence of high-SAPS and low-SAPS formulations for Euro 6d diesels. Battery-electric vehicles accounted for only 1.8% of the fleet in 2025, limiting their immediate impact on engine oil demand. Hybrid vehicles increasingly rely on low-viscosity grades like 0W-16 and 0W-20, which enhance fuel efficiency. Commercial fleets are extending oil drain intervals to 100,000 kilometers by using synthetic formulations, creating a volume-for-margin trade-off that benefits premium lubricant suppliers.

Offshore-Wind Build-Out Needs Gear And Hydraulic Lubes

North Sea offshore wind capacity is expected to exceed 40 gigawatts by 2030, following a wave of project approvals in 2025-2026. Each turbine requires up to 400 liters of gear oil and 100 liters of hydraulic fluid, with operators increasingly preferring synthetic PAO or PAG chemistries for their resistance to oxidation and water ingress. OEMs such as Siemens Gamesa and Vestas are specifying lifetime-fill lubricants for direct-drive models, shifting revenue streams from scheduled oil changes to premium first-fill supplies. Hydraulic fluids must adhere to ISO 15380 HEES biodegradability standards, further driving demand for ester-based products. While new installations favor high-margin synthetic lubricants, the pre-2020 turbine fleet continues to sustain demand for mineral-oil-based aftermarket products, segmenting the market by turbine age.

Circular-Economy Mandates For Re-Refined Base Oils

The EU collected 1.6 million tons of waste oil in 2024, regenerating 61% into re-refined base stocks under the Waste Framework Directive hierarchy. Group II and Group III re-refined oils now deliver performance comparable to virgin oils, meeting API SN Plus and ACEA C3 specifications while reducing lifecycle CO₂ emissions by 60%. In 2025, Germany reported that re-refined oils accounted for 18% of its domestic supply. A pending EU labeling proposal will require lubricant packaging to disclose recycled content. Although re-refined oils currently carry a 5-10% premium over virgin Group II oils, crude price volatility is narrowing the price gap, enhancing the competitiveness of bio-circular products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil and additive prices squeeze margins | -0.4% | EU-wide, acute in import-dependent markets (Italy, Spain) | Short term (≤ 2 years) |

| EU PFAS and phosphate-ester restrictions in fire-resistant fluids | -0.2% | Germany, France, Netherlands (mining, aviation sectors) | Medium term (2-4 years) |

| Lifetime-fill lubricants in wind-turbine gearboxes curb aftermarket | -0.1% | North Sea offshore wind markets (UK, Germany, Denmark) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil And Additive Prices Squeeze Margins

Brent crude oil averaged USD 82 per barrel in 2025 and remained near USD 84 in early 2026. Base-oil prices closely tracked crude trends, compressing blender margins when retail prices lagged behind cost increases. Additive package costs rose by 12% during 2024-2025 due to supply constraints for molybdenum disulfide and ZDDP concentrates, which are produced by a limited number of suppliers. Smaller blenders in Italy and Spain reported negative gross margins on certain SKUs in Q4 2025. Additionally, the strength of the US dollar inflated euro-denominated import costs, further pressuring margins for exporters targeting North Africa and the Middle-East.

EU PFAS And Phosphate-Ester Restrictions In Fire-Resistant Fluids

An ECHA proposal covering 12,000 PFAS chemicals may ban phosphate-ester hydraulic fluids, which are essential for underground mining and aviation safety[2]ECHA, “PFAS Restriction Proposal,” echa.europa.eu . Alternatives such as polyol esters do not provide equivalent extreme-pressure performance, increasing the risk of equipment failure in deep-shaft hoists operating at 350 bar. Mining hubs in Poland, Sweden, and Finland consumed approximately 15,000 tons of these fluids in 2025. Reformulation and OEM re-approval processes could cost the industry EUR 50 million (USD 54 million), posing a significant challenge for specialty blenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Greases Capture Growth Momentum

The automotive engine oil accounted for a 39.12% volume share in 2025, while greases are expected to grow at the fastest 2.07% CAGR through 2031. Lithium-complex greases dominate the segment, representing approximately 60% of the category, and are widely used in electric vehicle wheel bearings and wind turbine blade-pitch mechanisms. Calcium-sulfonate greases are gaining popularity in marine and off-highway applications due to their enhanced rust protection. Metalworking fluids are witnessing increased demand in Poland, the Czech Republic, and Hungary, driven by battery-component machining that requires low-foaming emulsions to extend tool life. Meanwhile, transmission fluid demand is moderating as hybrid dual-clutch systems require smaller oil volumes compared to traditional automatics, while brake fluid consumption remains stable, supported by an ageing vehicle fleet.

Greases also offer high margins due to their ability to withstand extreme temperatures in offshore turbines and high-speed EV bearings. Hydraulic fluid usage is expanding in Central and Eastern Europe (CEE) construction and mining sectors, with HEES-labeled ester blends mandated for forestry and offshore equipment. Turbine oils are transitioning to Group III and Group IV synthetics, enabling five-year drain intervals and reducing downtime in peaker plants and wind farms. Transformer oil upgrades are supporting grid modernization in Germany and France, where ester-based fluids enhance fire safety for urban substations. Process oil demand in tire manufacturing and pharmaceuticals is shifting toward treated distillate aromatic extracts that comply with REACH thresholds for PAH content.

By Base Stock Type: Bio-Based Lubricants Accelerate

Mineral oil-based lubricants accounted for 60.11% of the Europe lubricants market share in 2025, but bio-based lubricants are expected to grow at a 3.12% CAGR through 2031. The revised 2024 EU Ecolabel has tightened biodegradability criteria, driving demand for rapeseed, sunflower, and synthetic esters that achieve 60% degradation within 28 days under OECD 301B tests. Offshore wind operators, including Equinor and Ørsted, are increasingly specifying HEES fluids to mitigate spill risks. Synthetic PAO and PAG blends dominate premium powertrain fluids due to their oxidation stability and low-temperature performance, justifying price premiums of 30-50%. Semi-synthetic passenger car oils with 20-40% synthetic content offer a cost-effective alternative for consumers. Group III base stock production in Europe increased by 15% during 2024-2025 as refiners upgraded hydrocrackers, providing near-synthetic properties at a lower cost to support low-viscosity engine oil trends.

Mineral-based Group I blends continue to serve price-sensitive gear and metalworking oil markets, though some foundries in the Balkans and Baltics are transitioning to Group II as availability improves. Blenders are combining re-refined Group II with virgin Group III to produce ACEA C3 engine oils that meet low-SAPS requirements while promoting circularity. Premium polyalkylene glycols are gaining traction in gas-compressor lubricants for hydrogen blending trials in Germany, benefiting from water solubility and varnish-free operation.

By End-user Industry: Industrial Segment Outpaces Automotive Dominance

The automotive industry held 53.11% of the Europe lubricants market share in 2025, but the industrial segment is expected to grow at the fastest rate, with a 2.33% CAGR through 2031. Metalworking fluid demand is increasing in CEE as machining relocates to the region to support Germany’s electrified vehicle supply chain. Transformer oil usage is rising as utilities replace ageing units with ester-filled designs that enable urban deployment without fire-suppression reservoirs. Construction and mining activities in Poland and the Balkans are driving hydraulic fluid consumption, supported by EU cohesion fund investments in infrastructure.

In the automotive sector, hybrids and battery electric vehicles are shifting demand toward thermal management fluids, electric-drive oils, and high-speed greases, reducing reliance on engine oils. Marine lubricants are adapting to IMO 2020 sulfur regulations, with cylinder oil volumes declining as ships use low-sulfur fuel, although scrubber-equipped vessels still require high-base-number products. Aerospace remains a niche but profitable segment, with synthetic turbine oils meeting MIL specifications commanding premiums due to limited supplier competition. Heavy equipment operators in construction and agriculture are adopting biodegradable hydraulic fluids for forestry operations in Norway and Sweden. Power generation units are increasingly using Group III turbine oils for gas and wind assets, extending change intervals to five years or more.

Geography Analysis

The Rest of Europe accounted for 31.34% of the 2025 volume, encompassing a fragmented mix of Scandinavia, the Balkans, and smaller CEE states where local blenders thrive under diverse regulatory regimes. Russia is expected to achieve the fastest growth, with a 2.22% CAGR through 2031, as Gazpromneft and Lukoil expand blending capacity by 120,000 tons following the exit of Western majors in 2022. Germany’s automotive output declined by 6% in 2025, but demand from the chemical, machinery, and renewable energy sectors remains strong.

France benefits from TotalEnergies’ refinery-linked logistics, while the UK faces post-Brexit registration challenges that increase costs for pan-EU formulations. Italy’s average vehicle age of 13.2 years supports aftermarket engine oil sales, and its machinery hubs in Lombardy and Emilia-Romagna drive demand for specialty metalworking fluids. Spain’s market is characterized by a mix of tourism-driven coastal demand and industrial interior requirements for automotive oils and gear lubricants.

Poland, the Czech Republic, and Hungary are benefiting from battery plant investments and increased construction machinery usage. Nordic countries focus on biodegradable lubricants, with Norway and Sweden enforcing HEES hydraulics in forestry, resulting in 20-30% price premiums over mineral alternatives. The Balkans and Baltics remain price-sensitive, dominated by mineral oils from small local blenders. Turkey, positioned between Europe and the Middle-East, exports blends to North Africa while relying on Russian and Mediterranean base oil imports, exposing its supply chain to currency fluctuations and geopolitical risks.

Competitive Landscape

The Europe lubricants market is moderately concentrated, with Shell, TotalEnergies, BP, ExxonMobil, and FUCHS collectively accounting for approximately 50% of the volume in 2025. These companies leverage refinery-to-retail integration to secure feedstock and achieve economies of scale. However, specialty independents like FUCHS and Liqui Moly have established niches in high-performance greases and low-SAPS passenger car oils. Regional players such as MOL Hungary, Repsol, and Gazpromneft capitalize on proximity to local customers and flexible batch sizes to capture orders overlooked by multinationals.

Sustainability is a key focus area for strategic initiatives. TotalEnergies introduced a bio-hydraulic line for offshore wind and forestry in 2025, while Shell expanded re-refined base-oil capacity in Rheinland, Germany, to meet recycled-content proposals. FUCHS filed 12 lubricant patents over 2024-2025, targeting 0W-8 hybrid oils and calcium-sulfonate greases for EV wheel bearings. Digital condition-monitoring platforms offered by Shell and TotalEnergies bundle product supply with predictive analytics, locking clients into multi-year agreements.

Upstream material suppliers are also expanding their roles in the value chain. Croda and Emery Oleochemicals supply bio-esters that blenders use to qualify for the EU Ecolabel. Compliance under REACH and ISO standards acts as both a barrier for incumbents and an opportunity for mid-sized firms that can certify niche blends quickly. Regional distributors are countering volume pressure from lifetime-fill wind-turbine designs by adding services such as on-site filtration and oil analysis, shifting focus from liters sold to uptime delivered.

Europe Lubricants Industry Leaders

Exxon Mobil Corporation

FUCHS

Shell plc

TotalEnergies

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Chevron Phillips Chemical (CPChem) doubled its low-viscosity polyalphaolefin (PAO) production capacity in Beringen, Belgium, to 120,000 metric tons per year, becoming the largest decene-based PAO producer in Europe. The expansion met the rising demand for high-performance, sustainable lubricants in electric vehicles and industrial applications.

- August 2025: Castrol introduced its new MHP (MHP 1-30 and MHP 1-40) lubricant range in Europe in August 2025. This range is designed for four-stroke medium-speed marine engines, particularly those operating on alternative fuels such as LNG or biofuels, and provides enhanced engine cleanliness and wear protection, with field trials indicating oil drain intervals of up to 1,000 hours.

Europe Lubricants Market Report Scope

Lubricants are substances made from a combination of base oils and additives. These lubricants are used in various automotive applications such as engines, brakes, gears, and other parts. The base oil composition in the formulation of lubricants is primarily between 75-90%. Lubricants are used to reduce friction between surfaces in contact to minimize energy loss generated from friction.

The Europe lubricants market is segmented by product type, base stock type, end-user industry, and geography. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. The report also covers the market size and forecasts for lubricants in 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

By Geography

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

| By Geography | France | |

| Germany | ||

| Italy | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the volume of the Europe lubricants market?

The Europe lubricants market stands at 6.60 billion liters in 2026 and is projected to reach 7.22 billion liters by 2031, implying a 1.82% CAGR over 2026-2031.

Which product type is growing fastest through 2031?

Greases lead growth at a 2.07% CAGR through 2031 thanks to demand from electric-vehicle bearings and offshore-wind turbines.

How significant are bio-based lubricants in the region?

Bio-based lubricants are expected to expand at a 3.12% CAGR through 2031, outpacing mineral and synthetic lubricants as EU Ecolabel rules tighten.

Which country is expected to grow fastest through 2031?

Russia is set to post the fastest growth at 2.22% CAGR through 2031, driven by domestic refinery upgrades and import substitution.

Page last updated on: