Australia Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

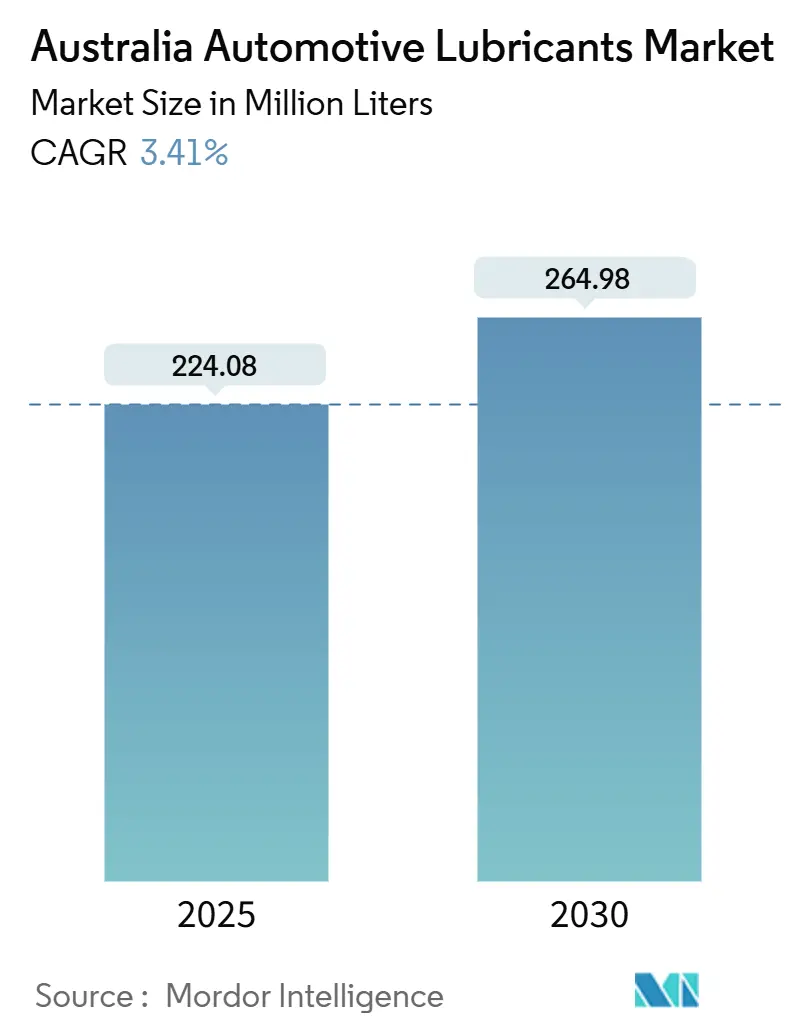

| Market Volume (2025) | 224.08 Million liters |

| Market Volume (2030) | 264.98 Million liters |

| Growth Rate (2025 - 2030) | 3.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Automotive Lubricants Market Analysis by Mordor Intelligence

The Australian Automotive Lubricants Market size is estimated at 224.08 million liters in 2025, and is expected to reach 264.98 million liters by 2030, at a CAGR of 3.41% during the forecast period (2025-2030). Demand growth reflects a delicate balance between an aging vehicle parc that averages 11 years, an expanding fleet, and rising electric-vehicle (EV) penetration. The early adoption of low-viscosity, fuel-efficient lubricants, required under Australia’s New Vehicle Efficiency Standard (NVES) and Euro 6d emissions rules, supports premium-grade volumes. Meanwhile, commercial and mining fleets drive the uptake of synthetic blends engineered for harsh operating conditions. Margin pressure persists as domestic crude output declines and base-oil imports become more volatile despite forecasts that Brent prices will ease, compelling suppliers to optimize sourcing and distribution. Ongoing investment in remote oil-condition monitoring and predictive maintenance platforms reinforces value-added service demand, offsetting the long-term volume threat posed by rapid EV uptake.

Key Report Takeaways

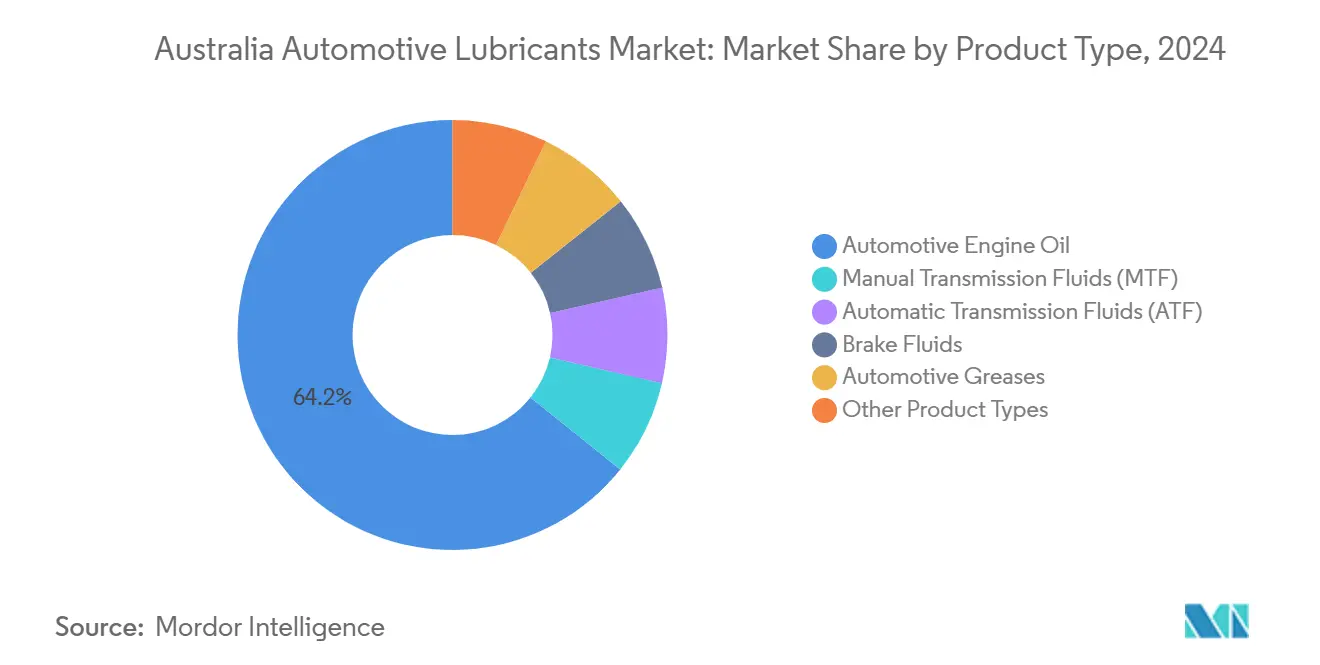

- By product type, engine oils led with 64.23% revenue share in 2024, while automatic transmission fluids posted the fastest projected CAGR at 3.67% through 2030.

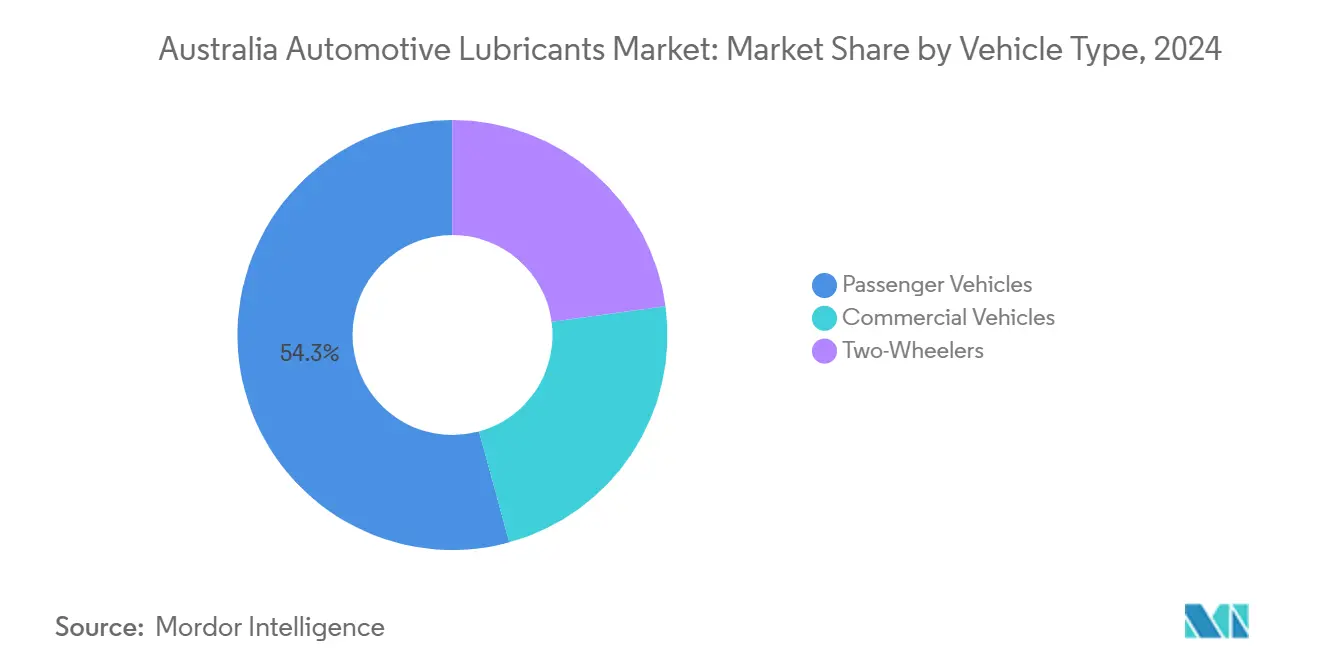

- By vehicle type, passenger vehicles accounted for 54.26% of Australia's automotive lubricants market share in 2024; however, commercial vehicles are forecasted to expand at a 3.78% CAGR through 2030.

Australia Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High OEM-genuine oil penetration sustains premium-grade demand | +0.8% | National, with concentration in major metropolitan service networks | Medium term (2-4 years) |

| Regulatory shift to low-viscosity, fuel-efficient oils | +1.2% | National, driven by NVES and Euro 6d compliance requirements | Short term (≤ 2 years) |

| Mature but aging vehicle parc maintains aftermarket volumes | +0.9% | National, with higher impact in regional areas with older fleets | Long term (≥ 4 years) |

| Growth of synthetic and bio-based blends for carbon reduction | +0.6% | National, with early adoption in fleet and mining operations | Medium term (2-4 years) |

| Remote oil-condition monitoring adoption among fleets | +0.4% | Mining regions (WA, QLD, NSW), commercial transport corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High OEM-Genuine Oil Penetration Sustains Premium-Grade Demand

Strong factory-fill alliances mean two in three manufacturers specify Castrol fluids at production, ensuring a reliable aftermarket pull for premium-grade formulations. Independent repairers now access the same data under the Motor Vehicle Information Scheme, closing the information gap with dealership networks and reinforcing nationwide quality standards[1]Australian Competition and Consumer Commission, “Motor Vehicle Information Scheme,” accc.gov.au. Digital oil-analysis services, such as Shell LubeAnalyst, help fleets verify total-cost-of-ownership savings, reinforcing their willingness to pay price premiums.

Regulatory Shift to Low-Viscosity, Fuel-Efficient Oils

The NVES, effective from January 2025, sets a 60% per-vehicle emissions reduction target for 2030, accelerating the transition toward low-SAPS lubricants that protect particulate filters in advanced powertrains. Fuel-quality reforms that cut sulfur to 10 ppm by December 2025 further enable extended drain intervals, reducing total lubricant requirements even as per-litre value rises.

Mature but Aging Vehicle Parc Maintains Aftermarket Volumes

Internal-combustion models still represent the majority of the national fleet, and as warranties expire, owners increasingly switch from OEM brands to cost-effective aftermarket alternatives. Vehicle age in remote areas exceeds metropolitan averages, encouraging more frequent oil changes and sustaining traditional volume demand.

Growth of Synthetic and Bio-Based Blends for Carbon Reduction

Fleet operators and miners are adopting synthetic and bio-based lubricants to meet ESG mandates. PETRONAS, targeting net-zero by 2050, has introduced fluid ranges that deliver comparable wear protection with lower greenhouse-gas footprints. The bio-based share remains small, but lifecycle analyses that include disposal and fuel-savings benefits are improving the value proposition.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV/hybrid uptake curbs ICE-oil volumes | -1.8% | National, with accelerated adoption in metropolitan areas and fleet operations | Short term (≤ 2 years) |

| Volatile base-oil feedstock costs pressure margins | -0.7% | National, affecting all market participants with varying impact based on supply chain integration | Medium term (2-4 years) |

| Counterfeit lubricants proliferating on e-commerce | -0.5% | National, with higher concentration in online retail channels and price-sensitive consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid EV/Hybrid Uptake Curbs ICE-Oil Volumes

EV sales rose in new registrations, with forecasts suggesting they will exceed 53% by 2030 under the most likely scenario. This trajectory limits internal-combustion-engine (ICE) lubricant growth, although specialized EV fluids for reduction gears, battery cooling, and thermal management represent a nascent but strategic niche.

Volatile Base-Oil Feedstock Costs Pressure Margins

Domestic crude production is projected to decline by 2028-29, exposing refiners and blenders to global price fluctuations even as Brent softens in the longer term. Smaller local blenders such as Penrite face higher input volatility than integrated majors that can leverage global base-oil networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Growth While Transmission Fluids Accelerate

Engine oils retained a dominant 64.23% share of Australia's automotive lubricants market in 2024. Low-SAPS synthetics that comply with Euro 6d standards command price premiums, offsetting the gradual shift toward electrified powertrains. Automatic transmission fluids are projected to experience a 3.67% CAGR through 2030, as dual-clutch and continuously variable transmissions gain popularity in both passenger and light-commercial vehicle fleets. The segment is experiencing rapid innovation in additive chemistry, targeting shear stability and long-life properties that are suited to 100,000-km drain intervals. Manual transmission fluids and power-steering fluids are facing structural decline due to the adoption of automatic gearboxes and electric steering, while high-temperature lithium complex greases are gaining market share in harsh mining environments.

The demand for automatic transmission fluid also benefits from stringent OEM warranty conditions that mandate the use of genuine or technically equivalent products, thereby creating opportunities for upselling premium synthetics. Conversely, the penetration of immersion-cooling fluids for EV battery packs, though still niche, is attracting research and development spend that could diversify supplier portfolios beyond traditional engine-oil lines. Suppliers that expand laboratory services for in-field fluid diagnostics strengthen their hold on value-added aftermarket channels.

By Vehicle Type: Commercial Fleets Outpace Passenger Cars on Volume Growth

Passenger cars accounted for 54.26% of Australia's automotive lubricants market in 2024, reflecting entrenched service networks and consistent maintenance behavior among individual owners. However, commercial vehicles (trucks, buses, and off-road mining equipment) will expand at a 3.78% CAGR through 2030. Commercial-fleet procurement favors extended-drain synthetics that reduce downtime and maintenance overhead, even at per-litre price premiums. Mining firms in Western Australia and Queensland specify Tier-1 formulations that withstand ambient temperatures above 50 °C, heavy dust loading, and continuous operations.

Fleet consolidation enables centralized purchasing, rewarding suppliers that offer integrated analytics, training, and recycling programs. The demand for two-wheeler lubricant remains steady in urban commuter corridors and enthusiast segments, although volumes are modest compared to those of four-wheel categories. Growth opportunities in the motorcycle market lie in synthetic 5W-40 and ester-based racing oils, which are marketed through performance workshops. In contrast, scooters typically use cost-sensitive mineral blends.

Geography Analysis

New South Wales and Victoria together account for a significant portion of national volumes due to dense vehicle populations, mature dealership networks, and proximity to import terminals at Port Botany and Port Melbourne. Extended urban commutes and higher disposable incomes tilt consumer preference toward premium synthetics. Western Australia, dominated by mining activity, generates higher revenue per litre due to the widespread use of heavy-duty synthetics in haul trucks and loaders operating in the Pilbara, where dust, high temperatures, and steep haul-road gradients accelerate lubricant degradation. Suppliers such as Viva Energy have invested USD 25 million in a new Karratha distribution hub to shorten lead times and secure supply for remote customers[2]Viva Energy, “Pilbara Lubricants Facility,” vivaenergy.com.au.

Queensland’s combination of agriculture, construction, and freight corridors underpins healthy demand for diesel engine oils and hydraulic fluids. Humid, tropical conditions exacerbate oxidation and sludge formation, underscoring the importance of high-TBN formulations with robust acid-neutralization capacity. South Australia and Tasmania contribute smaller but stable shares, driven by viticulture, aquaculture, and tourism fleets that require versatile lubricants for mixed operating cycles. The Northern Territory’s mining and defense assets generate pockets of high-margin demand, but long supply lines pose challenges to logistics and inventory management.

Overall, regional disparities are narrowing as e-commerce platforms expand product availability; however, the authenticity challenge hinders online volume from matching that of physical retail or workshop channels. Suppliers that pair digital storefronts with local warehouse footprints can mitigate counterfeit risks and enhance customer trust, particularly in remote areas where physical access to branded outlets is limited.

Competitive Landscape

The Australian Automotive Lubricants Market is moderately consolidated. Global majors continue to shape the strategic direction of Australia's automotive lubricants market through technical research and development, OEM endorsements, and vertically integrated supply chains. Their ability to absorb feedstock volatility and invest in next-generation EV fluids fortifies competitive positions. Local brands leverage agile formulation changes, region-specific packaging, and competitive pricing to secure share in independent queues. Retail disruptors, notably Bunnings Warehouse, are testing lubricant aisles that could erode traditional auto parts chains if a nationwide rollout occurs. Strategic deals continue to reshape the landscape. Suppliers are increasingly pitching their sustainability credentials, offering carbon-neutral product lines backed by lifecycle assessments and biodegradable packaging to align with customer ESG targets.

Australia Automotive Lubricants Industry Leaders

Shell plc

BP p.l.c.

Chevron Corporation

Exxon Mobil Corporation

Saudi Arabian oil Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. announced plans to sell its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion divestment program.

- December 2024: LIQUI MOLY launched new generalist motor oils for Australia, formulated in Germany and produced in Thailand for regional supply.

Australia Automotive Lubricants Market Report Scope

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large is the Australian automotive lubricants market in 2025?

The Australian automotive lubricants market size is 224.08 million litres in 2025 and is forecast to reach 264.98 million litres by 2030.

What CAGR is forecast for lubricant demand through 2030?

National demand is projected to grow at a 3.41% CAGR from 2025 to 2030.

Which product category leads consumption?

Engine oils hold 64.23% of total volumes thanks to Australia’s largely ICE-based vehicle fleet.

Which segment is growing fastest?

Automatic transmission fluids are expected to show the highest growth at a 3.67% CAGR due to the wider adoption of advanced transmission technologies.

How will EV growth affect lubricant suppliers?

Rising EV penetration restrains traditional engine oil volumes but opens new opportunities in specialized EV driveline and thermal management fluids.

Page last updated on: