Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

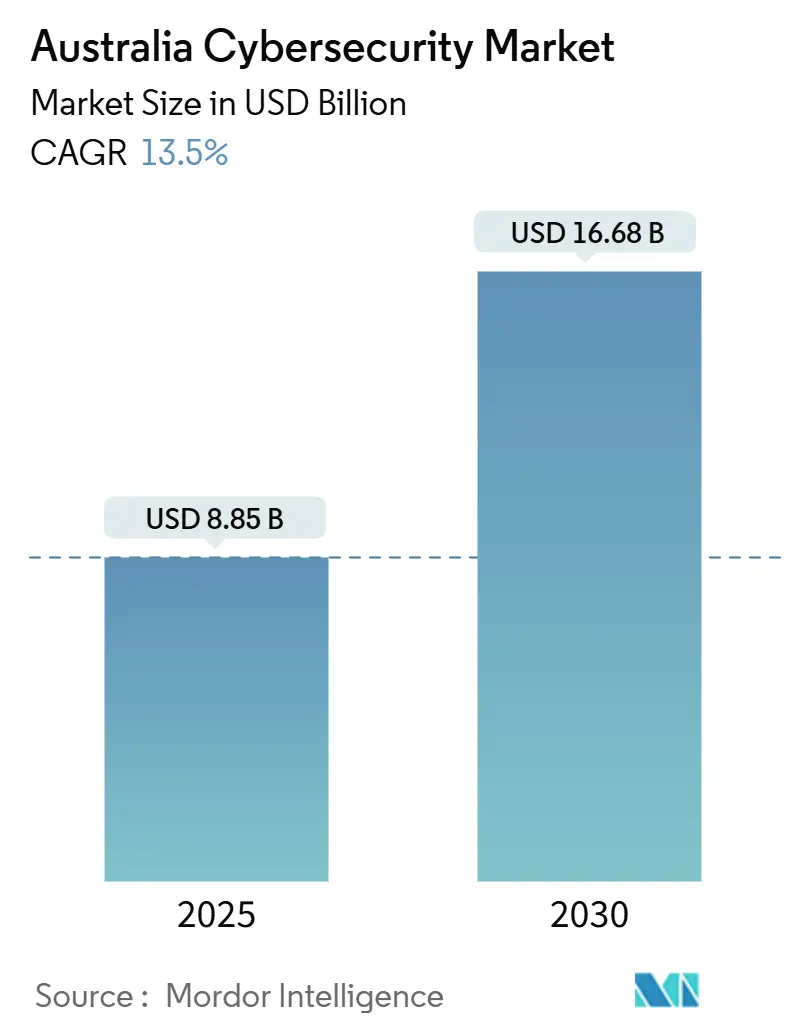

| Market Size (2025) | USD 8.85 Billion |

| Market Size (2030) | USD 16.68 Billion |

| Growth Rate (2025 - 2030) | 13.50% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Cybersecurity Market Analysis by Mordor Intelligence

The Australia Cybersecurity Market size is estimated at USD 8.85 billion in 2025, and is expected to reach USD 16.68 billion by 2030, at a CAGR of 13.5% during the forecast period (2025-2030). Escalating attack volumes, new ransomware-payment reporting laws, and sustained federal spending have turned cyber resilience into a board-level priority for organizations of every size. Large enterprises continue to consolidate security platforms to cut tool sprawl, while small and medium enterprises (SMEs) accelerate SaaS-based adoption because they cannot attract scarce talent. Public-sector investment anchored by a USD 2 billion Top Secret Cloud program has created a multiplier effect for private cloud migrations. Meanwhile, critical-infrastructure operators now face prescriptive risk-management duties covering 22 asset classes, forcing rapid modernization of operational-technology defenses. Competition is intensifying as global vendors expand local data-center footprints and domestic specialists build niche offerings for industrial and regional customers.

Key Report Takeaways

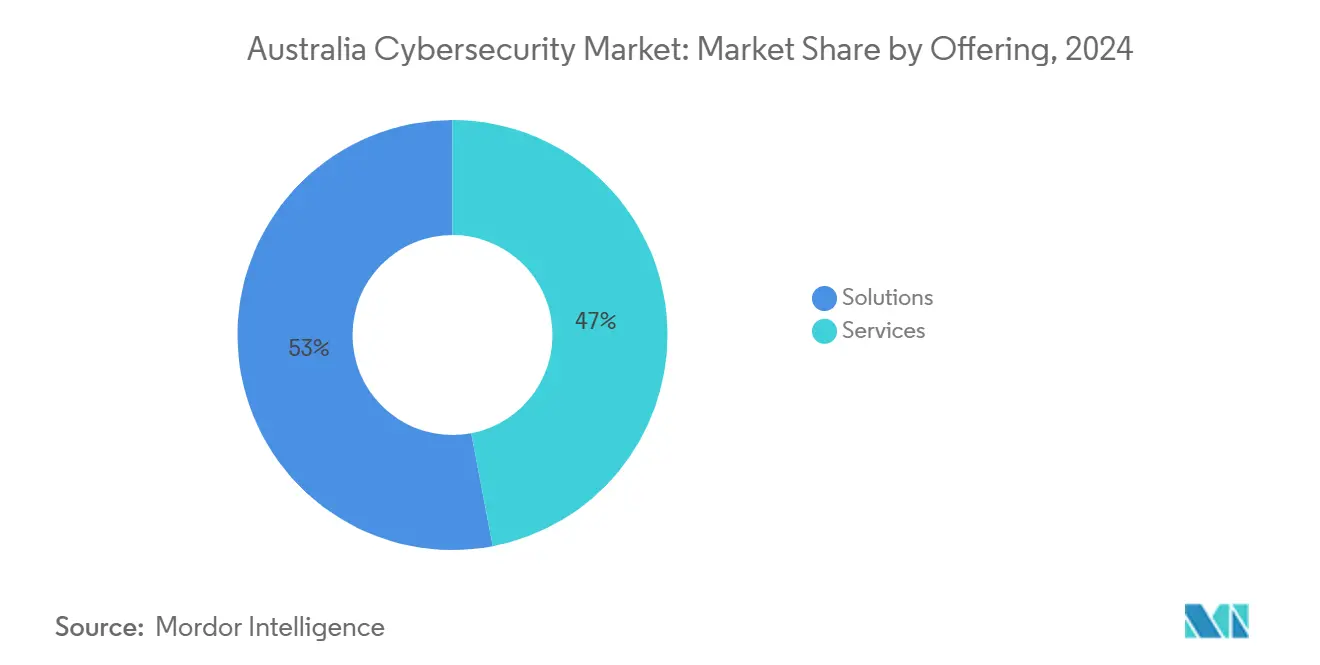

- By offering, Solutions led with 53% revenue share in 2024; services are projected to expand at a 16.7% CAGR through 2030.

- By deployment mode, cloud captured 64.8% of the Australia cybersecurity market share in 2024 and is advancing at a 19% CAGR through 2030.

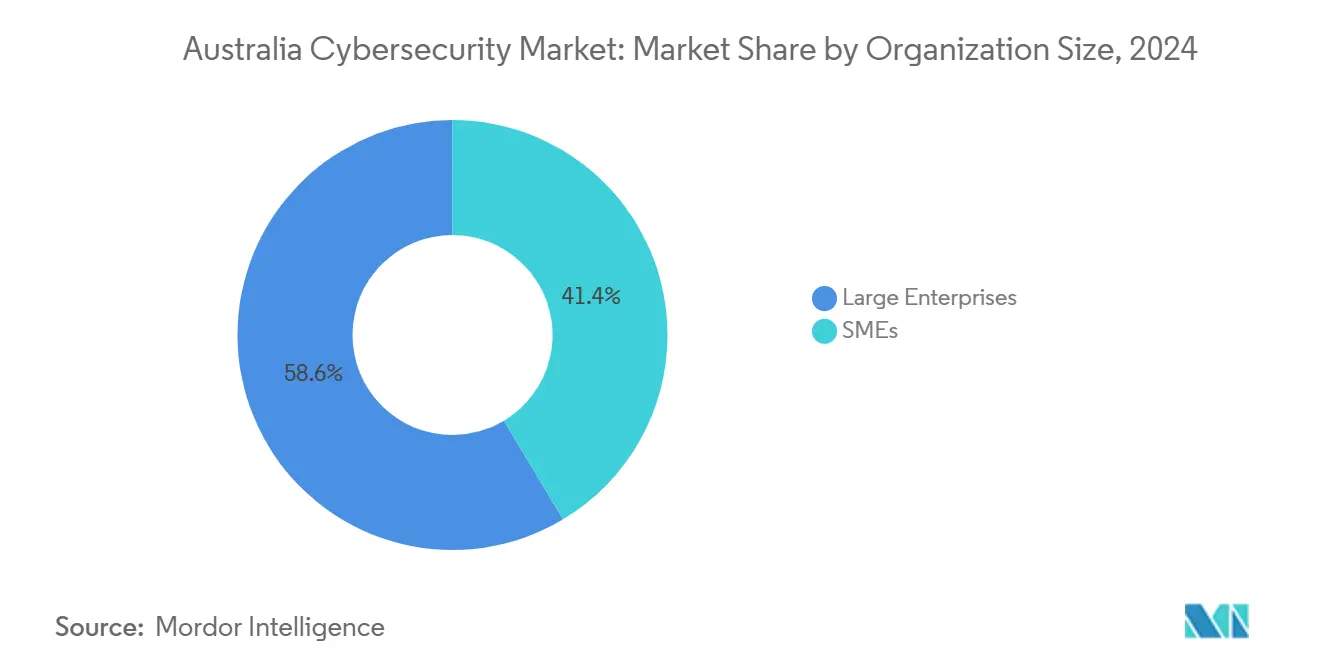

- By organization size, large enterprises held 58.6% share of the Australia cybersecurity market size in 2024, while SMEs are growing fastest at a 17.8% CAGR to 2030.

- By end user, BFSI retained 22.5% revenue share in 2024; healthcare is forecast to post the highest 15.6% CAGR to 2030.

Australia Cybersecurity Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume & sophistication of attacks | +2.8% | National, concentrated in major cities | Short term (≤ 2 years) |

| Mandatory breach-reporting & critical-infrastructure laws | +2.1% | National, sector-specific variations | Medium term (2-4 years) |

| Cloud adoption across enterprises | +3.2% | National, led by Sydney & Melbourne | Medium term (2-4 years) |

| Proliferation of IoT/OT endpoints | +1.9% | National, industrial regions | Long term (≥ 4 years) |

| Cyber-insurance premium surge | +1.4% | National, large enterprises | Short term (≤ 2 years) |

| Federal tax incentives for sovereign-security R&D | +1.1% | National, tech hubs | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Volume & Sophistication of Attacks

Australia recorded 94,000 cybercrime incidents in FY 2023, up 23% year on year.[1]Australian Government, “Annual Cyber Threat Report 2023-2024,” cyber.gov.au Ransomware hits on critical infrastructure jumped 50% in 2024, and the DP World port outage exposed economic spill-over risks. Nation-state groups now target operational-technology networks, while “hackers-for-hire” platforms lower entry barriers for criminals. Boards therefore fund AI-enabled threat-hunting tools and managed detection services at scale. These dynamics underpin double-digit growth across every layer of the Australia cybersecurity market.

Mandatory Breach-Reporting & Critical-Infrastructure Laws

The Cyber Security Act 2024 obliges firms with turnover above AUD 3 million to disclose ransomware payments within 72 hours. Security of Critical Infrastructure (SOCI) amendments extend risk-management programs to 22 asset classes, including data-storage systems. Financial institutions must also comply with APRA CPS 234 testing rules. Collectively these statutes amplify demand for compliance workflow software, incident-response retainers, and integrated security platforms accelerating revenue across the Australia cybersecurity market.

Cloud Adoption Across Enterprises

A USD 2 billion sovereign-cloud deal with AWS broke long-standing data-residency barriers for public agencies intelligence.gov.au. Amazon’s broader USD 20 billion data-center roadmap cements capacity for large-scale migrations aboutamazon.com. Regulators have issued cloud-risk frameworks that banks now treat as de-facto standards rba.gov.au. Zero-trust, container, and serverless protections are therefore commanding premium budgets, ensuring the Australia cybersecurity market keeps outpacing national IT spending.

Proliferation of IoT/OT Endpoints

Industrial IoT rollouts in mining and manufacturing widen attack surfaces that legacy firewalls cannot secure. The 2024 Cyber Security Bill requires smart-device makers to ban default passwords and push updates.[2]CMS, “Australia's Cyber Security Bill 2024: A New Era of Digital Defence,” cms-lawnow.com Waterfall Security counted 68 global OT incidents with physical impact in 2024, highlighting urgent need for segmentation and protocol whitelisting. Edge devices in remote mines further spur demand for low-latency, cloud-managed controls another tailwind for the Australia cybersecurity market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe talent shortage | -2.3% | National, most acute in major metropolitan hubs | Medium term (2-4 years) |

| High total cost of advanced solutions for SMEs | -1.8% | National, most challenging for businesses in regional areas | Short term (≤ 2 years) |

| Budget-constrained public agencies | -1.2% | National, differing by state-level funding commitments | Medium term (2-4 years) |

| Fragmented state-level data-residency requirements | -0.9% | National, driven by varying state regulations | Long term (≥ 4 years) |

Source: Mordor Intelligence

Severe Talent Shortage

Australia needs 40,000 additional cyber professionals, with cloud-security architects commanding salaries above AUD 275,000.[3]Nucamp, “Australia Cybersecurity Salaries: What Can You Expect to Earn?,” nucamp.co Google’s 6-month certificate program tackles entry-level gaps but cannot close specialist shortfalls. Enterprises therefore outsource monitoring to managed security service providers and automate routine tasks, but this dependence can create single points of failure—moderating the Australia cybersecurity market growth rate.

High TCO for Advanced Solutions in SMEs

Sixty-two percent of Australian SMEs have suffered cyber attacks, yet many still rely on consumer-grade antivirus because enterprise platforms exceed budgets. Canberra allocated USD 291 million to subsidize SME controls, but 2025 budget cuts signal fading government support. With breach costs averaging AUD 4.26 million, SMEs face existential risk, prompting demand for low-touch, subscription-based protections that can scale down for smaller footprints within the Australia cybersecurity market.

Segment Analysis

By Offering: Services Drive Market Leadership

Solutions represented 53% of the Australia cybersecurity market in 2024, equivalent to USD 3.7 billion in revenue. Managed services are forecast to grow at 16.7% annually as organizations struggle to fill internal roles. Large banks now embed service-level outcomes for threat hunting and incident response into multi-year contracts. Energy and mining firms procure on-site managed detection to safeguard remote OT assets. Professional services remain resilient because every new regulation demands fresh gap assessments and tabletop exercises. Vendor consolidation is reshaping competition illustrated by Novigi acquiring 360 Managed to expand from Canberra into Western Australia.[4]Channel Insider, “Novigi Acquires 360 Managed,” channelinsider.com Platform vendors bundle advisory hours with product subscriptions, shifting value away from standalone consultancies. As a result, the Australia cybersecurity market size tied to services is projected to surpass USD 7.8 billion by 2030.

Solutions revenue is still rising but at a slower clip as buyers favor integrated suites. Endpoint, identity, and SIEM capabilities increasingly ship as unified agents to cut overhead. Demand for application-security testing climbs because DevSecOps adoption accelerates release cycles. Cloud security posture management (CSPM) tools post the highest expansion, aligning with 19% CAGR in cloud deployments. The Cybereason–Trustwave merger highlights the pivot toward single-console threat detection across endpoints and networks. Nevertheless, niche innovators in OT firewalls and API protection still win strategic deals where generalized suites fall short.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments held 64.8% of the Australia cybersecurity market in 2024, mirroring the rapid SaaS adoption curve among enterprises and government agencies. The sovereign AWS Top Secret Cloud project validated hyperscale resilience for sensitive workloads. Financial institutions cite Reserve Bank guidelines as de facto guardrails for shared-responsibility models. As workloads shift, demand for infrastructure-as-code security and serverless-runtime protection surges. Cloud environments also simplify compliance evidence gathering, a critical benefit under CPS 234 and SOCI audits.

On-premise investments persist in utilities, ports, and defense, where air-gapping remains mandatory. Organizations deploy micro-segmentation and data-diode gateways to bridge IT and OT zones without risking bidirectional flow. Hybrid architectures blend cloud analytics with edge policy enforcement, especially in remote mining operations where connectivity is intermittent. Over time, legacy data centers will host only latency-sensitive or sovereign-sealed assets, while analytics and observability layers migrate. Even in these conservative sectors, pilot projects use cloud-based threat-intel feeds to enrich local detections, ensuring continuous revenue streams for platform vendors targeting the Australia cybersecurity market.

By Organization Size: SME Growth Outpaces Enterprise

Large enterprises produced 58.6% of 2024 revenue thanks to bigger budgets and compulsory compliance spend. Banks and telecom providers integrate identity, SIEM, and XDR under a single license to tackle tool sprawl. These firms also deploy AI-driven playbooks to offset analyst shortages, freeing senior staff for deeper threat-hunting. Enterprises negotiate volume pricing that lowers unit costs yet still raise overall outlays year over year because the threat landscape expands relentlessly.

SMEs expand fastest, with 17.8% CAGR, because attackers increasingly shift toward softer targets. Government grants cover vulnerability assessments and incident-response retainers for qualifying businesses. Google’s Cybersecurity Certificate funnels junior analysts into MSPs that predominantly serve SMEs. Vendors now tailor bundled endpoint, email, and backup subscriptions priced per employee. This consumption model enables revenue capture that traditional license tiers had missed. The Australia cybersecurity market size linked to SMEs is forecast to exceed USD 3 billion by 2030, reflecting both volume and rising average spend per seat.

By End User: Healthcare Emerges as Growth Leader

BFSI remained the largest customer base with 22.5% market share in 2024, anchored by APRA’s escalating assurance tests and high fraud exposure. Banks deploy behavioral analytics to flag anomalous payments within seconds, curbing mule-account proliferation. Insurers tighten underwriting rules, rewarding continuous-control monitoring with premium discounts, which further fuels adoption.

Healthcare posts the highest 15.6% CAGR after multi-million-record breaches at Medibank and MediSecure. Hospitals replace legacy Windows 7 machines and segment medical-device networks to meet IoT security mandates. The federal government awarded AUD 6.4 million to establish sectoral information-sharing groups, improving threat-intel flow. Manufacturing and energy operators intensify OT monitoring after a 50% spike in industrial ransomware incidents. Retailers focus on point-of-sale hardening and tokenization as e-commerce volumes rise.

Geography Analysis

The Australia cybersecurity market concentrates in New South Wales and Victoria, where Sydney and Melbourne host regional headquarters for global vendors and nearly two-thirds of enterprise customers. Federal projects such as the Australian Signals Directorate–Microsoft USD 5 billion partnership channel substantial spend into Canberra, raising average professional salaries to AUD 165,808. Queensland and Western Australia display specialized demand patterns tied to mining logistics and port security. State-specific breach-notification laws add compliance complexity, spurring uptake of adaptive policy engines.

Remote operations in Pilbara and Bowen Basin favour ruggedized edge firewalls and satellite-routed SOC connectivity. Vendor roadmaps include low-bandwidth signature updates and machine-learning models that run locally until backhaul sync resumes. South Australia benefits from AUKUS submarine programs, generating defense-grade cybersecurity subcontracts for local SMEs. Tasmania, though smaller in spend, pioneers privacy-enhancing technologies within its health-data platforms, showing that even peripheral regions contribute innovation to the Australia cybersecurity market.

Geographic threat analytics show ransomware gangs clustering attacks around high-value metros but probing regional councils with phishing to gain footholds. Nationwide adoption of remote work, now stabilised at 45% of white-collar roles, broadens the endpoint surface, leading CIOs to roll out unified endpoint management that enforces consistent policies regardless of postcode. This convergence of regional specificities and national regulatory harmonization sustains double-digit growth across every state within the Australia cybersecurity market.

Competitive Landscape

The market features moderate fragmentation. Microsoft, Palo Alto Networks, and CrowdStrike lead enterprise segments by bundling SIEM, endpoint, and identity into unified platforms. Microsoft’s Security Cloud booked USD 42.4 billion worldwide revenue in Q3 2025, with deep penetration among Australian government tenants. Palo Alto Networks posted USD 2.29 billion Q3 revenue, spotlighting AI-assisted policy tuning that resonates with talent-constrained SOC teams. Fortinet’s Secure SD-WAN and SASE portfolios secure dispersed branch offices, especially in retail and resources.

Local champions include Telstra Purple, which leverages carrier-grade telemetry to block 10 million scam calls monthly. Tesserent focuses on defense primes, while Sekuro targets APRA-regulated entities with zero-trust advisory. OT-security specialists CyberCX and Aegis9 win contracts in LNG and rail. Patent filings for blockchain-protected machine-to-machine communication indicate emerging intellectual property advantages for domestic start-ups. Acquisition activity remains brisk as MSSPs merge to achieve national coverage and 24×7 staffing, responding to client demands for guaranteed response times. These dynamics collectively shape a vibrant yet consolidating Australia cybersecurity market.

Australia Cybersecurity Industry Leaders

-

AVG Technologies

-

Check Point Software Technologies Ltd

-

Cisco Systems Inc.

-

IBM Corporation

-

Trellix Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Australia mandated 72-hour ransomware-payment reporting for businesses above AUD 3 million turnover.

- May 2025: Palo Alto Networks posted USD 2.29 billion Q3 2025 revenue, emphasizing AI and cloud-security growth.

- May 2025: Fortinet achieved USD 1.54 billion Q1 2025 revenue, driven by unified SASE demand.

- April 2025: Microsoft reported USD 70.1 billion Q3 2025 revenue, with Security Cloud at USD 42.4 billion.

Australia Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and by phishing in order to maintain data confidentiality.

Australia cybersecurity market is is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| By Offering | Solutions | Application Security | |

| Cloud Security | |||

| Data Security | |||

| Identity and Access Management | |||

| Infrastructure Protection | |||

| Integrated Risk Management | |||

| Network Security Equipment | |||

| Endpoint Security | |||

| Other Solutions | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| By Organization Size | SMEs | ||

| Large Enterprises | |||

| By End User | BFSI | ||

| Healthcare | |||

| IT and Telecom | |||

| Industrial and Defense | |||

| Retail | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Others | |||

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Organization Size

| SMEs |

| Large Enterprises |

By End User

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Australia cybersecurity market by 2030?

The market is expected to reach USD 16.68 billion by 2030, expanding at a 13.5% CAGR.

Which segment is growing fastest within the Australia cybersecurity market?

Services are forecast to grow at 16.7% annually as organizations outsource monitoring and incident response.

Why is cloud security spending rising so quickly in Australia?

Federal endorsement of a USD 2 billion sovereign cloud and broad enterprise migration have pushed cloud deployments to 64.8% share, driving strong demand for cloud-native controls.

How severe is the cybersecurity talent shortage in Australia?

The country needs 40,000 additional practitioners, and specialists such as cloud-security architects can command salaries above AUD 275,000.

Which vertical shows the highest growth potential?

Healthcare leads with a 15.6% CAGR due to recent large-scale breaches and government funding for sector-specific information-sharing networks.

What new regulation most affects Australian companies in 2025?

The Cyber Security Act 2024 mandates ransomware-payment disclosure within 72 hours for businesses exceeding AUD 3 million turnover, reshaping incident-response processes.