Market Overview

| Study Period | 2021 - 2031 |

|---|---|

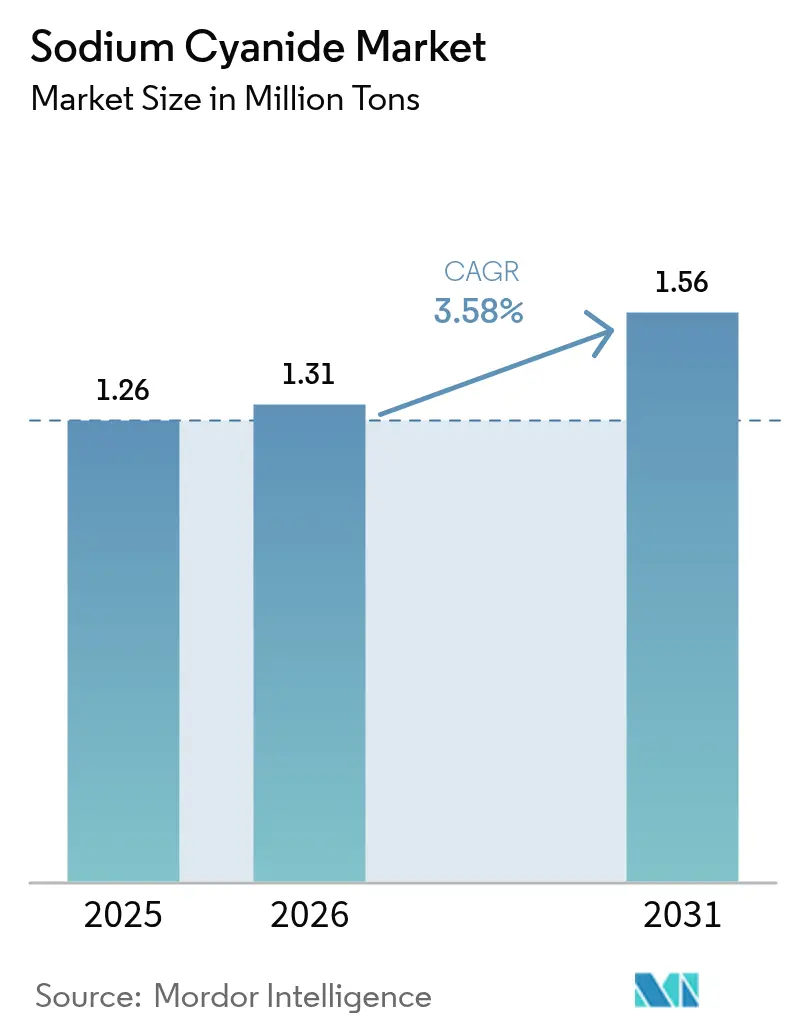

| Market Volume (2026) | 1.31 Million tons |

| Market Volume (2031) | 1.56 Million tons |

| Growth Rate (2026 - 2031) | 3.58% CAGR |

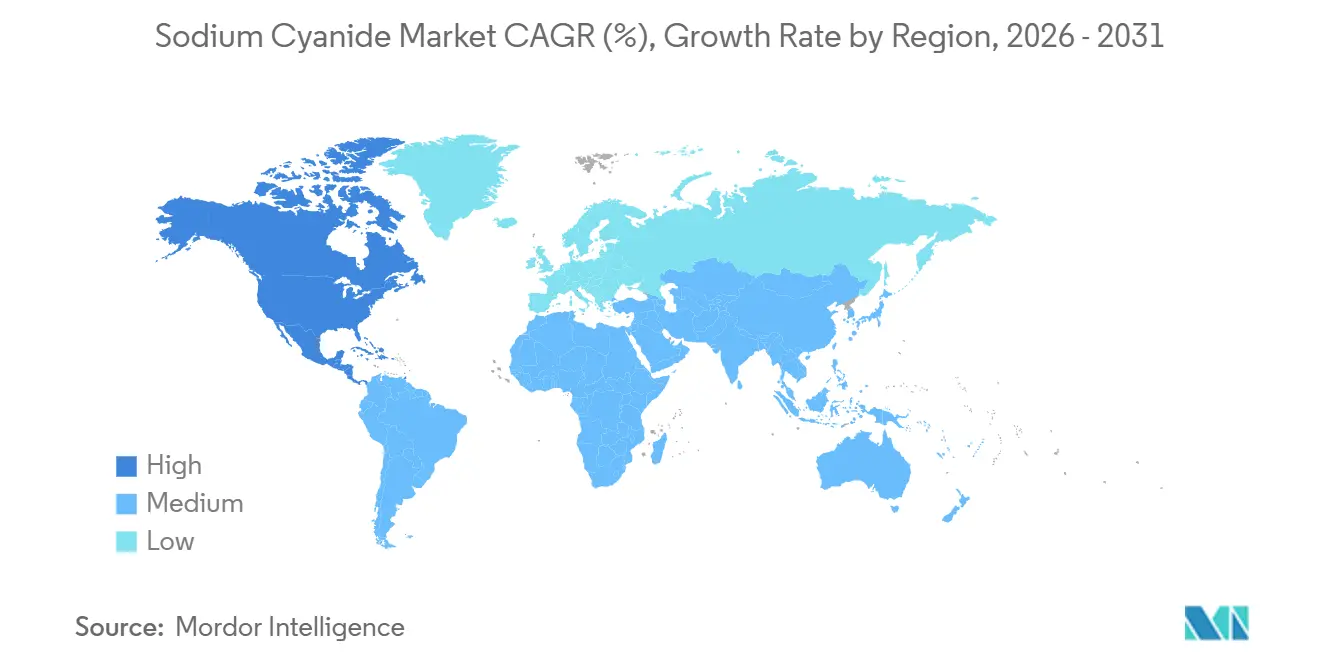

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Cyanide Market Analysis by Mordor Intelligence

The Sodium Cyanide Market size is projected to expand from 1.26 Million tons in 2025 and 1.31 Million tons in 2026 to 1.56 Million tons by 2031, registering a CAGR of 3.58% between 2026 to 2031. Steady demand stems from declining gold ore grades that require higher reagent intensity, regional expansions such as Orica’s post-acquisition capacity uplift, and the emergence of modular on-site plants that curb logistics costs. Heap-leach projects in West Africa and Central Asia continue to set the pace as their lower capital outlays attract investment, while regulatory regimes now weigh greenhouse-gas intensity alongside traditional toxicity metrics. Competitive focus is shifting toward long-term offtake agreements and bundled technical support, especially where freight disruption or winter road closures expose supply-chain risk. Producers are embedding wastewater-recycling systems that recover more than 70% of process water and incinerators that cut manufacturing emissions by nearly 30%, strengthening their audit scores under the International Cyanide Management Code.

Key Report Takeaways

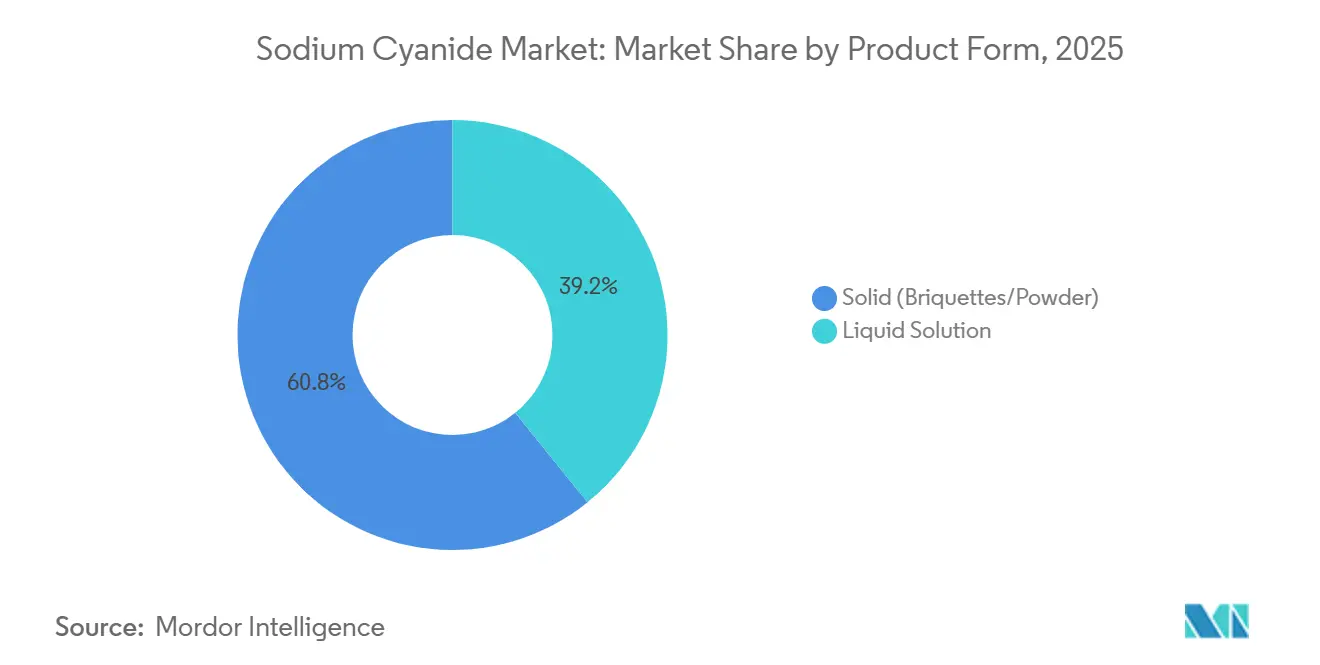

- By product form, solid (briquettes/powder) captured 60.81% of sodium cyanide market share in 2025, while liquid solution is forecast to advance at a 3.72% CAGR through 2031.

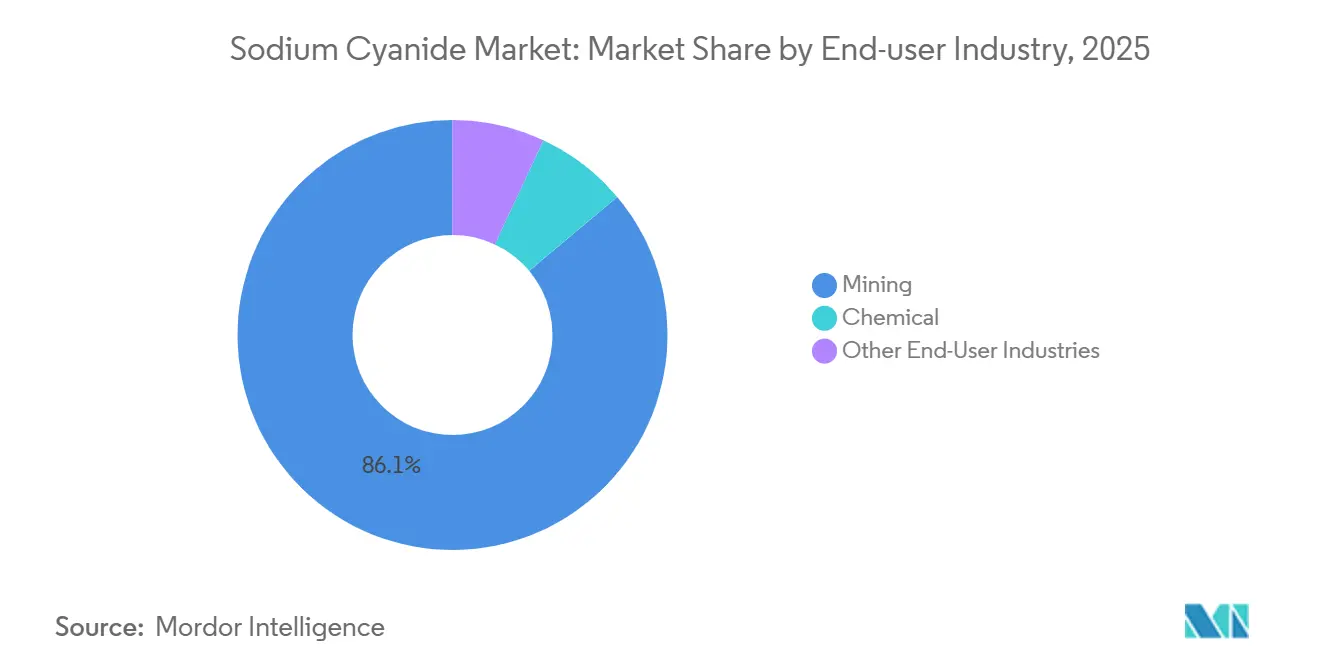

- By end-user industry, mining held 86.11% of the sodium cyanide market size in 2025, while the chemical segment is projected to post 3.95% through 2031.

- By geography, Asia-Pacific led with a 30.12% volume share in 2025, whereas North America is projected to advance at a 3.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sodium Cyanide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in low-grade gold mining requiring higher NaCN loadings | +1.2% | Global, with concentration in West Africa (Ghana, Burkina Faso), Central Asia (Kazakhstan, Kyrgyzstan), and Latin America (Peru, Argentina) | Medium term (2–4 years) |

| Rising heap-leach projects in Africa and Central Asia | +0.9% | Sub-Saharan Africa (Ghana, Sudan, Tanzania), Kazakhstan, Uzbekistan, Tajikistan | Medium term (2–4 years) |

| Growth of on-site modular NaCN plants lowering logistics cost | +0.6% | Remote mining districts in Australia (Western Australia), Canada (Yukon, Northwest Territories), and South America (Chilean Atacama, Peruvian Andes) | Long term (≥ 4 years) |

| Increasing adoption of cyanide sparging systems in Asia-Pacific mines | +0.5% | Asia-Pacific core (Australia, Indonesia, Papua New Guinea), with spill-over to Southeast Asian greenfield projects | Short term (≤ 2 years) |

| Recovery of silver-bearing tailings in Latin America | +0.4% | Peru (Cerro de Pasco, Junín), Argentina (San Juan, Catamarca), Mexico (Zacatecas, Chihuahua) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Boom in Low-Grade Gold Mining Requiring Higher NaCN Loadings

Falling head grades are driving cyanide dosages from historical 0.5–0.8 kg per tonne to 1.2–1.5 kg per tonne so that recovery stays above 85%. Each 0.1 g/t grade drop can lift per-tonne reagent demand by 10–15%, magnifying volumes even when gold output is flat. West African operators now stipulate monthly deliveries exceeding 200 tons, double those of higher-grade underground mines. Australian forecasts show domestic gold production rising to 377 tons by 2030, yet average grades have slipped below 1.8 g/t, highlighting the sodium cyanide market’s volume leverage. Miners are concurrently installing regeneration loops that recapture up to 12% of free cyanide, partially offsetting higher feed rates.

Rising Heap-Leach Projects in Africa and Central Asia

Heap leaching demands far lower capital—typically USD 50–80 million for a 3–5 Mt/a pad—than conventional mills, unlocking oxide deposits in Ghana, Sudan, and Kazakhstan. Draslovka’s USD 160 million Egyptian plant will feed nearby projects, trimming shipment times to 8–12 days via Red Sea ports. Kazakh initiatives aim at domestic reagent security as border delays hamper imports. Seasonal rainfall in West Africa dilutes solution strength by up to 20%, creating buffer-inventory requirements that favor suppliers offering consignment stock at mine-gate warehouses. Cyanide recovery aims remain above 85%, with deviations below 80% triggering step-ups in fresh reagent orders.

Growth of On-Site Modular NaCN Plants Lowering Logistics Cost

Mines located more than 500 km from ports contend with freight and insurance premiums that lift delivered cost by 15–25%. Skid-mounted units producing 10,000–30,000 t/y sodium cyanide cut working capital tied to inventory by up to 40% and remove the freeze-thaw risk of winter haulage. Australian Gold Reagents is integrating a low-emissions incinerator that slices plant-level CO₂ intensity by 28% and serves as a blueprint for mine-site modules. The trade-off is reliance on concentrated hydrogen-cyanide feedstock from a handful of suppliers, shifting risk from freight to precursor availability.

Recovery of Silver-Bearing Tailings in Latin America

Legacy dams in Peru’s Cerro de Pasco contain around 120 Mt of tailings at 50 g/t silver, now reprocessed using cyanide dosages of 1.5–2.5 kg per tonne of solids with 70–80% recovery[1]United Chemical Company, “Tailings Reprocessing Initiatives,” unitedchemical.kz, unitedchemical.kz . At silver prices of USD 28–32 per oz, internal rates of return surpass 18%. Argentina and Mexico are experimenting with lower-cost heap approaches that accept reduced recovery to minimize reagent spend. Tailings projects bypass exploration lead times, so sodium cyanide demand here is projected to grow faster than in primary ore processing through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity and tightening ICMC compliance audits | -0.8% | Global, with stringent enforcement in North America (U.S., Canada), Australia, and European Union member states; emerging rigor in West Africa (Ghana, Côte d'Ivoire) | Short term (≤ 2 years) |

| Pilot-scale switch to glycine/thiosulphate lixiviants | -0.3% | Localized trials in Australia (Western Australia), Canada (Ontario, British Columbia), and select European projects; limited commercial deployment | Long term (≥ 4 years) |

| High marine freight premiums for hazardous cargoes | -0.5% | Trade lanes from Asia-Pacific (China, Australia) to Africa and South America; intra-European shipments; trans-Pacific routes to North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Toxicity and Tightening ICMC Compliance Audits

The Code now insists on secondary containment sized for the largest tank plus piping, fixed monitors, and community outreach in local languages. Newmont’s Ghana project invested in triple-coated concrete bunds and leak-detection pumps, spending USD 3–5 million for compliance[2]WSP Group Africa, “ICMC Compliance Requirements,” wspgroup.com, africa.wsp.com. Annual audit fees top USD 80,000 and suppliers must maintain chain-wide certification, pushing smaller blenders toward consolidation. Mines that miss audits risk offtake cancellations and financing delays, steering procurement toward established, audit-ready vendors.

Pilot-Scale Switch to Glycine/Thiosulphate Lixiviants

Alternative lixiviants consume three- to five-fold more reagent and seldom exceed 80% gold recovery in sulfide-bearing ores. Process windows demand tight pH and temperature control, lifting energy cost by USD 4–6 per tonne. Cyanco’s partnership with Cycladex aims to improve kinetics, but no commercial launch has been declared. Unless carbon taxes surpass USD 80–100 per t CO₂-eq, sodium cyanide retains a decisive cost edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Solid Leads as Logistics-Friendly Choice

Solid sodium cyanide commanded 60.81% of 2025 volume, underscoring the segment’s sodium cyanide market share advantage for mines that value long shelf life and lower marine insurance costs. Briquettes resist freezing and allow operators to store several weeks of inventory without solution tanks. Powder serves smaller mills but incurs dust-control packaging expenses.

Liquid solution is projected to grow quickest as mines in remote deserts and high altitudes adopt ISO-tank deliveries that remove dissolution steps and curb hydrogen-cyanide exposure. Automated metering linked to online analyzers trims wastage by up to 8%. However, heated storage and more frequent shipments raise working capital. Suppliers offering hybrid supply contracts—briquettes for base load and solution for peak demand—expect to capture additional sodium cyanide market revenue as process-control systems become more responsive.

By End-user Industry: Mining Dominates While Chemicals Accelerate

Mining accounted for 86.11% of 2025 volume, reflecting sodium cyanide’s unrivaled economics in dissolving gold at sub-2 g/t grades. Typical reagent outlay sits at approximately USD 1.50–2.00 per gram of gold recovered, far below competing lixiviants. Heap-leach projects now elevate loadings to 1.2–1.5 kg per tonne, locking in a stable pull on the sodium cyanide market.

The chemical segment is expanding on demand from nitrile pharmaceuticals and high-purity electroplating baths. Precise dosing of liquid cyanide boosts batch yields and reduces operator exposure. Draslovka’s push into sodium-ion battery precursors could add 5,000–8,000 t/y by 2030, further diversifying the sodium cyanide industry’s client base. Niche uses in metallurgy, water treatment, and photography collectively represent less than 5% of demand but offer premium pricing for 98–99% purity grades.

Geography Analysis

Asia-Pacific controlled a 30.12% slice of the sodium cyanide market in 2025, supported by China’s export-oriented producers and Australia’s ongoing capacity build-out. Australian Gold Reagents is lifting Kwinana output by 30% to 130,000 t/y to serve a domestic gold sector forecast to reach 377 t of metal by 2030, translating into an incremental 18,000–22,000 t of sodium cyanide per year. Indonesian and Papua New Guinean mines are retrofitting sparging systems that sync cyanide dosing with clay-rich feed fluctuations, and Chinese exporters must now supply documentation proving end-use compliance with the Cyanide Code, bolstering their quality credentials.

North America is positioned for the fastest regional growth, at 3.98% CAGR through 2031. Orica’s USD 640 million purchase of Cyanco doubled regional capacity to 240,000 t/y, anchoring supply for Nevada, Ontario, and British Columbia operations that prefer domestic logistics over trans-Pacific freight. Canada’s northern mines are weighing modular plants to overcome winter road closures that limit deliveries to a few months each year. Mexico’s heap-leach expansions in Zacatecas and Sonora could add another 10,000 t/y of demand by 2029.

Europe’s consumption clusters in Russia and the CIS, where Siberian and Ural complexes tap domestic caustic soda streams for cyanide synthesis. Evonik’s CyPlus subsidiary is exploring waste-heat capture to lower plant emissions ahead of the EU’s carbon-border levies. Kazakhstan’s United Chemical Company has inked memorandums to supply 25,000 t/y from Taraz to Tajik customers, reflecting a wider pivot toward reagent self-sufficiency amidst trade frictions AZH.KZ.

South America relies on Peru, Argentina, and Brazil. Peru’s tailings-reprocessing in Cerro de Pasco applies 1.5–2.5 kg/t cyanide to unlock residual silver, delivering IRRs above 18% at today’s metal prices. Argentine projects accept lower recovery to cut reagent cost but must invest in lined storage for environmental clearance. Brazil’s Unigel dominates liquid supply domestically and exports short-sea to neighbors, leveraging lower insurance fees than trans-Pacific cargos.

Middle-East and Africa focus on Ghana, Sudan, and South Africa. Draslovka’s Egyptian plant will reduce delivery windows to under two weeks for West African mines, slicing freight cost and inventory carry. Newmont’s Ahafo North requires roughly 5,000 t/y of cyanide and has already passed a pre-operational Code audit with upgraded containment and monitoring. Deeper South African reefs and Sudan’s infrastructure gaps create openings for suppliers that combine reagent sales with turnkey handling services.

Regulatory Landscape

Sodium cyanide is regulated as a high-hazard, dual-use chemical across major regions, with compliance spanning chemical registration, occupational exposure, transport controls, and environmental release limits. In the European Union, sodium cyanide is managed under REACH via ECHA substance dossiers, while the United States overlays worker protection requirements (OSHA exposure limits) and air and water compliance frameworks for cyanide-related manufacturing and use.

Regulatory tightening also shows up through newer national production-safety standards and ongoing certification expectations in mining supply chains. China issued GB 45189-2025 (Specification for cyanide safety production management) on February 28, 2025, with implementation from September 1, 2025, formalizing requirements around production safety, storage, and emergency management. Alongside mandatory rules, the International Cyanide Management Code administered by the International Cyanide Management Institute (ICMI) remains a key procurement gate for gold mining supply chains, supported by recurring site and supply-chain audits. Canada continues to manage cyanide releases from mining through Metal and Diamond Mining Effluent Regulations (MDMER) updates effective since June 1, 2021.

Value Chain Analysis

The sodium cyanide value chain starts with upstream feedstocks and energy, then concentrates through a limited set of integrated producers and certified logistics providers before reaching mine sites and chemical users. Most industrial supply is produced via the Andrussow route, where ammonia, natural gas (methane), and air generate hydrogen cyanide over a platinum-rhodium catalyst, followed by neutralization with sodium hydroxide to make sodium cyanide in solid or solution form. This makes ammonia and caustic soda availability, as well as the reliability of utilities and catalyst systems, critical upstream nodes that can transmit disruptions quickly into delivered cyanide availability.

Midstream, the chain depends on hazardous-material packaging, ISO tank or briquette distribution, and Code-aligned handling and emergency-response readiness, often provided by producers as bundled services to mining customers (technical support, auditing, and inventory solutions). Downstream, mines increasingly add user-controlled buffering assets, such as on-site storage for briquettes and dissolution plants that convert solid to solution, to reduce dependency on single-source regional liquid supply. The November 2025 force majeure declared by Sasol in South Africa following an ammonia plant breakdown highlighted how a single upstream feedstock failure can constrain national supply and force end users to pivot to solid stockpiles and imported material where feasible.

Competitive Landscape

The sodium cyanide market is moderately concentrated: Orica, Draslovka, TAEKWANG, Australian Gold Reagents, and Anhui Shuguang collectively control roughly 60–66% of global capacity. Orica’s February 2024 acquisition of Cyanco for USD 640 million doubled its footprint to 240,000 t/y and provided North American redundancy, a core selling point during freight bottlenecks. Draslovka’s foray into sodium-ion battery chemicals diversifies revenue streams beyond mining cycles. Australian Gold Reagents is integrating a low-emissions incinerator and wastewater recycling above 70%, aligning with miners’ Scope 1 and 2 reduction goals.

Competition increasingly pivots on service packages—technical audits, regeneration circuit design, and consignment inventory—rather than spot pricing. Chinese entrants undercut incumbents by up to 12% yet struggle to secure long-term offtakes where buyers demand full ICMC certification. Modular on-site synthesis represents a white-space niche: suppliers bundling hydrogen-cyanide feedstock with turnkey plants can command premium margins in regions where haulage exceeds 500 km. Heightened regulatory scrutiny that extends liability upstream to transport partners is hastening consolidation, as smaller distributors lack the compliance infrastructure.

Sodium Cyanide Industry Leaders

Australian Gold Reagents Pty Ltd

Draslovka

Orica Limited

Anhui Shuguang Chemical Group

TAEKWANG INDUSTRIAL CO. LTD

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is emerging where buyers prioritize regional redundancy, shorter lead times, and audit-ready supply, rather than spot procurement. Multi-year contracts tied to dedicated logistics and terminal capacity illustrate this shift. In March 2026, Draslovka signed a multi-year supply agreement to provide sodium cyanide to Barrick Mining Corporation for Nevada Gold Mines, supported by handling-terminal capability in Carlin, Nevada and product supply from its Memphis facility.

Another opportunity area is regional capacity build-out and localization to reduce hazardous freight exposure and inventory carry in remote or infrastructure-constrained markets. In Australia, Australian Gold Reagents moved its Kwinana expansion from engineering into construction in November 2025 to lift total solution capacity to 130,000 tpa and solid capacity to 60,000 tpa, aligning with miners preference for secured domestic supply and improved compliance performance (including emissions and water-management upgrades referenced in producer strategies). In the Middle East and Africa, Egypt approved a USD 200 million sodium cyanide manufacturing project at the Sidi Kerir Petrochemicals complex in Alexandria led by DrasChem Specialized Chemicals, targeting 50,000 tpa in its first phase, underscoring a tangible pipeline for nearer-to-mine supply into African gold markets where freight premiums and hazardous cargo constraints remain persistent.

Recent Industry Developments

- May 2026: Orica's Houston cyanide production plant achieved its fifth certification under the International Cyanide Management Code. The re-certification strengthens Orica's audit-ready positioning with major gold miners that require Code-aligned sourcing across production and transport, helping protect long-term offtake volumes in North America.

- November 2025: Sasol, South Africa's only domestic producer of liquid cyanide, declared force majeure after a breakdown at its ammonia plant disrupted feedstock availability. The outage constrained local liquid supply and pushed mining customers to rely more heavily on solid cyanide inventories and alternative supply routes, reinforcing the value of redundancy and buffering assets in high-risk regions.

- February 2024: Orica completed its USD 640 million acquisition of Cyanco, doubling its sodium cyanide capacity footprint in North America to 240,000 t/y. The combination expanded Orica's ability to serve large gold mining corridors with domestic logistics options and reduced exposure to hazardous marine freight volatility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the sodium cyanide market covers commercially sold sodium cyanide supplied as solid or liquid solution for industrial consumption, and it is measured based on demand volumes across end users and regions.

Scope exclusions: On-site captive production that is not sold in the market, and non-sodium cyanide cyanide derivatives, are not counted in the market totals.

Segmentation Overview

- By Product Form

- Solid (Briquettes/Powder)

- Liquid Solution

- By End-user Industry

- Mining

- Chemical

- Other End-User Industries

- By Geography

- Asia-Pacific

- China

- Australia and New Zealand

- Indonesia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Russia

- CIS (ex-Russia)

- Rest of Europe

- South America

- Brazil

- Peru

- Argentina

- Rest of South America

- Middle-East and Africa

- Ghana

- Sudan

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning the product definition, trade flows, and end use linkages that explain why sodium cyanide demand moves with metals extraction and chemical output. We relied on public datasets such as UN Comtrade for trade codes, the USGS for metals and mining context, and the World Gold Council for gold demand signals that impact cyanide use intensity.

To keep assumptions realistic, we also reviewed sources such as national mining ministries, environmental and chemical safety agencies, and peer reviewed papers that discuss cyanidation practices, dosage ranges, and recovery rates. Additional context came from company annual reports, investor presentations, and reliable industry news to confirm capacity additions, plant outages, and logistics constraints. For specific company financials, patent activity, and shipment level import and export checks, our analysts also used selected paid databases under approved use cases. The sources listed here are illustrative, and many other public and proprietary references were used to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary discussions were run with producers, distributors, mining site procurement teams, and chemical buyers to validate consumption patterns and practical supply constraints, including product form choices between solid briquettes and liquid solution. We also spoke with regional experts across APAC, EMEA, and the Americas so dosage assumptions, procurement contracts, and how plants manage delivery windows could be checked against local operating realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 21% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 22% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where gold and base metal processing activity is translated into sodium cyanide consumption through typical dosage rates and process yields, which are then adjusted for regional operating practices. To avoid relying on one indicator, we checked the model using selective bottom-up approximations such as supplier capacity signals, channel feedback on contract volumes, and sampled price and volume combinations to see if totals stayed in a realistic range.

Key inputs used in the model included mined ore throughput trends at major mining regions, the share of ore treated by cyanidation, average consumption per ton of ore, the split between solid briquettes and liquid solution, and import dependence for countries with limited local supply. For forecasting, we used scenario analysis supported by simple regression checks that link cyanide demand to expected gold output and processing intensity, and then we adjusted the path based on expert views on new mine ramps, shutdown risks, and environmental compliance tightening. When bottom-up signals were incomplete for smaller markets, gaps were handled by applying region level consumption intensity ranges and validating them with trade patterns and interview feedback before finalizing totals.

Data Validation & Update Cycle

Outputs were tested using triangulation against independent signals such as trade balances, known capacity changes, and regional mining activity, and then the main variances were reviewed to understand what drove them. If a country or end use result moved too far from expected patterns, the assumptions were rechecked and, when needed, experts were recontacted to confirm whether the shift was real or model driven.

Before sign-off, the work goes through multiple analyst reviews that check math integrity, unit consistency, and conversion logic so volume and growth rates remain coherent across the report. The report is refreshed annually, and interim updates are made when material events occur, such as major plant outages, new capacity announcements, or sharp changes in mining output. Right before delivery, we do a final pass so clients receive the latest updated view based on the newest public releases and validated field feedback.

Mordor Intelligence's Sodium Cyanide Market Sizing Compared With Other Published Estimates

It is normal to see different published market sizes for sodium cyanide because groups do not always use the same unit of measurement, the same end use boundaries, or the same timing for prices and currency conversions. Differences also show up when one estimate leans more on producer capacity and another leans more on end user consumption signals.

Some external publications present the market mainly in USD value and may blend in distributor margins, freight, or a broader set of cyanide related products. The split in scope is one reason the numbers spread out, and in Mordor Intelligence's approach the total is reported in physical demand (tons) for sodium cyanide only, which avoids price cycle noise and keeps the count tied to metal processing consumption.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.26 M (2025) | |

| Industry Publisher A | USD 2.49 B (2024) | Reports market size in USD consumption value and can reflect pricing, channel markups, and mixed year price assumptions, so it is not directly comparable to a tonnage based total. |

| Global Publisher B | USD 2.67 B (2024) | Uses value sizing with a different forecast window and may include broader application and channel scope, which can lift totals if distributor pricing and adjacent chemical demand is captured. |

From the table, the biggest driver is not a small calculation choice, but the unit and scope choice that changes what gets counted. By keeping the market expressed in tons and validating it against mining activity, trade movements, and expert dosage ranges, the final result stays transparent and easier to replicate year to year.

Key Questions Answered in the Report

How fast will sodium cyanide demand grow through 2031?

Global volumes are projected to climb from 1.31 million tons in 2026 to 1.56 million tons by 2031, translating to a 3.58% CAGR.

Which region offers the highest growth potential?

North America shows the strongest outlook, advancing at approximately 3.98% CAGR as reopened deposits and heap-pad retrofits lift consumption.

Why do miners still favor sodium cyanide over alternative lixiviants?

Glycine and thiosulphate routes consume three- to five-times more reagent and rarely exceed 80% recovery, keeping cyanide the most cost-effective option.

What role do modular on-site cyanide plants play?

Skid-mounted units of 10,000–30,000 t/y slash freight premiums and cut inventory working capital by up to 40% in remote districts.

Page last updated on: