Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

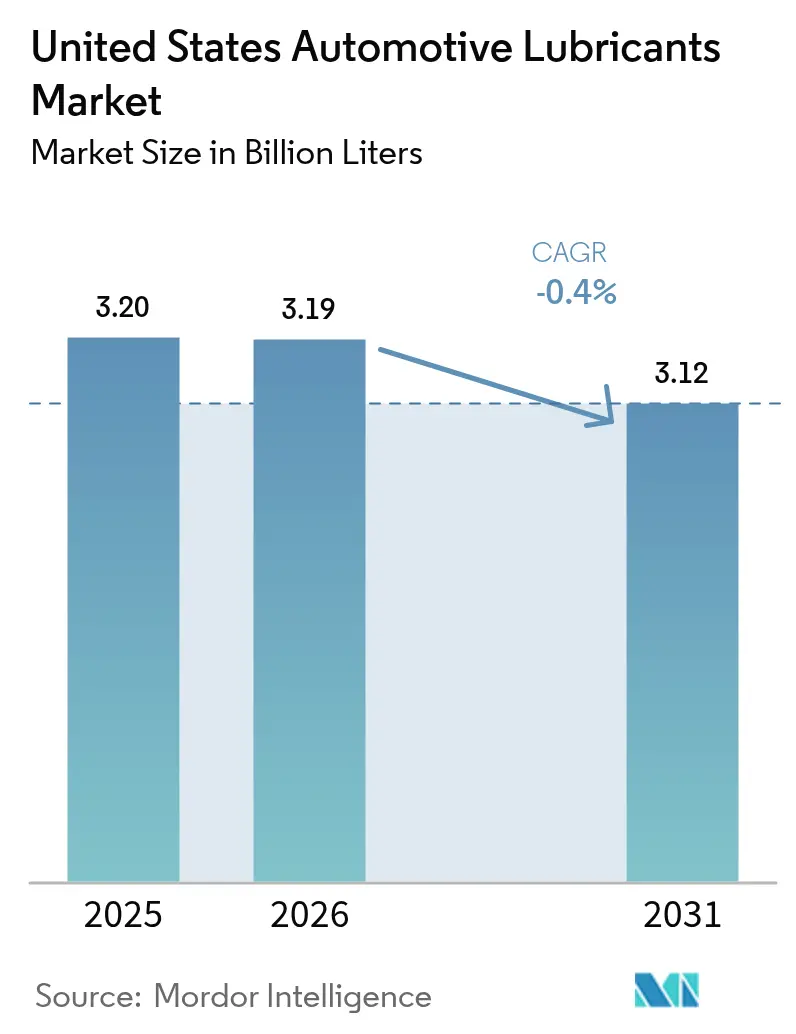

| Base Year Market Size (2025) | 3.20 Billion liters |

| Market Volume (2026) | 3.19 Billion liters |

| Market Volume (2031) | 3.12 Billion liters |

| Growth Rate (2026 - 2031) | -0.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Automotive Lubricants Market Analysis by Mordor Intelligence

The United States Automotive Lubricants Market size is projected to be 3.20 billion liters in 2025, 3.19 billion liters in 2026, and decline to 3.12 billion liters by 2031, declining at a CAGR of -0.4% from 2026 to 2031. Extended drain intervals, electrification and shared-mobility models are creating a structural headwind that outweighs incremental demand from fleet digitalization and the regulatory push toward low-viscosity synthetics. The shift to premium-grade 0W-20 and 5W-30 formulations required by new corporate average fuel-economy (CAFE) rules is raising value per liter even as overall volume shrinks. Commercial fleets are adopting predictive oil-life systems that cut oil changes by as much as 50%, yet data-subscription revenues from these platforms partly cushion the topline impact for integrated service providers. Meanwhile, California’s looming heavy-duty nitrogen-oxide rule, the American Petroleum Institute’s (API) ILSAC GF-8A specification and the forthcoming PC-12 diesel category are accelerating reformulation toward lower-viscosity, low-SAPs and bio-based chemistries.

Key Report Takeaways

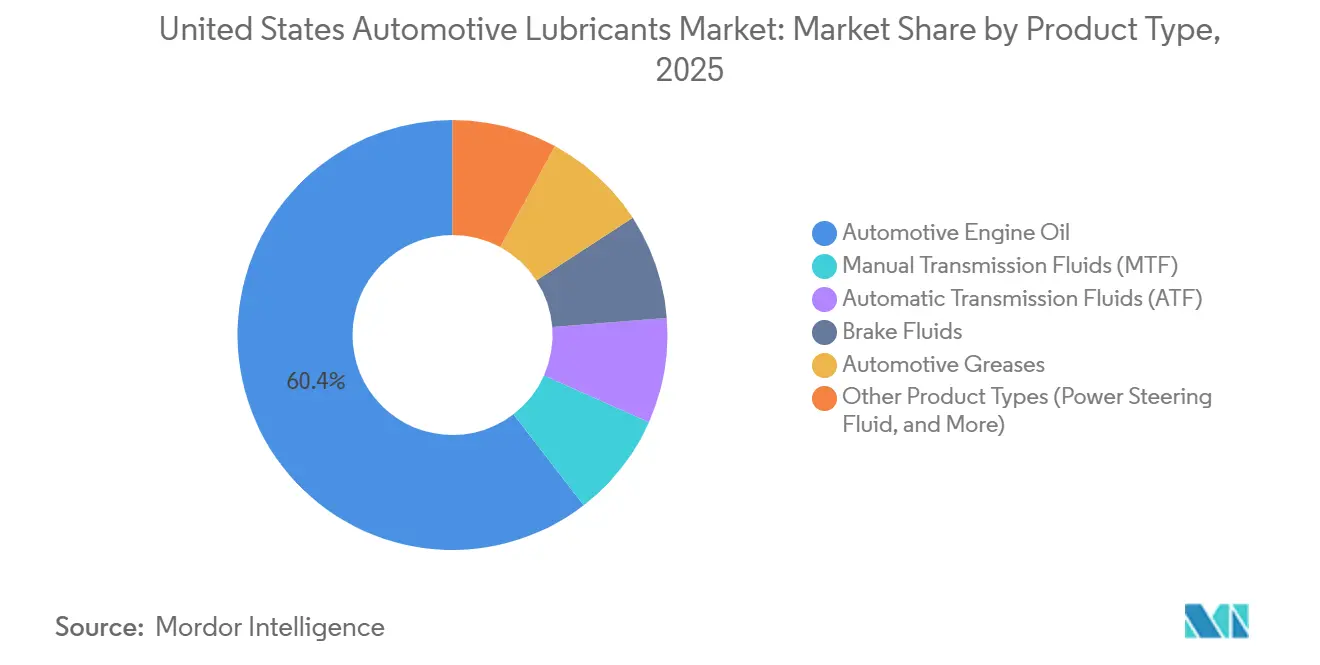

- By product type, automotive engine oil led with 60.43% revenue share in 2025, whereas automatic transmission fluid posted the least severe contraction at a -0.07% CAGR through 2031, underscoring its relative resilience in a shrinking market.

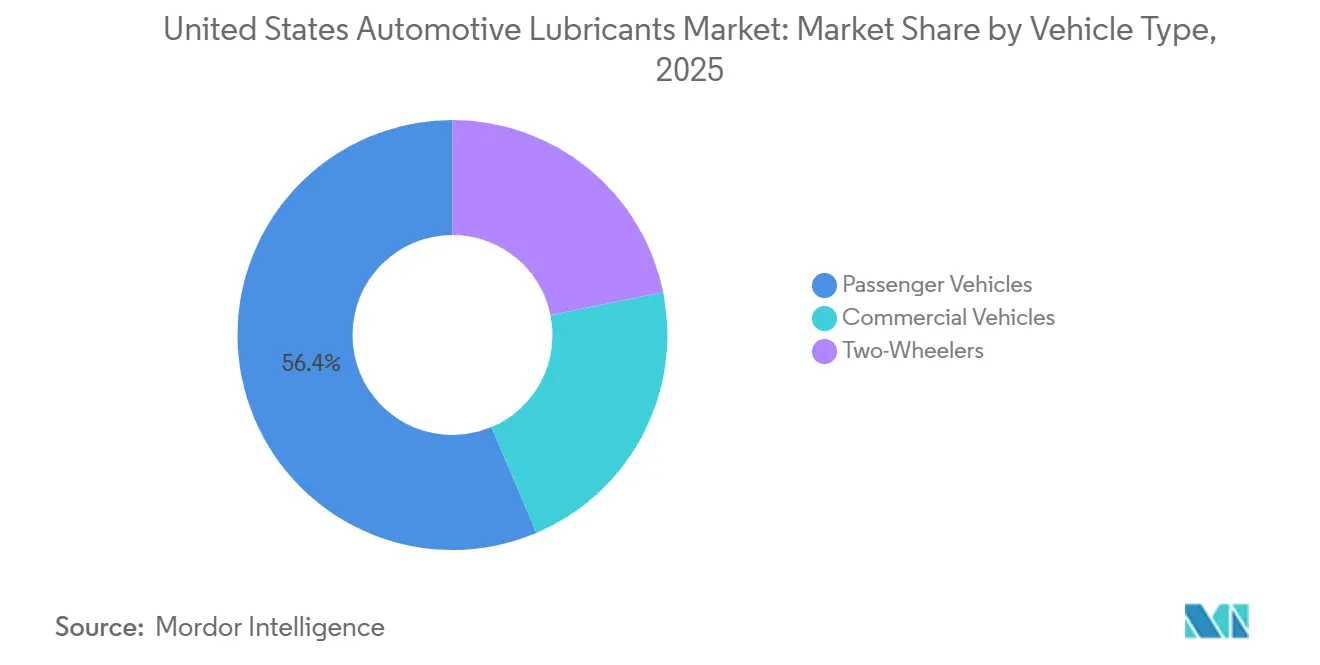

- By vehicle type, passenger vehicles accounted for 56.38% of the United States Automotive Lubricants market size in 2025, while commercial vehicles demonstrated the slowest decline with a -0.23% CAGR to 2031, buoyed by limited electrification of heavy-duty fleets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent CAFE/GHG norms accelerating shift to low-viscosity synthetics | +0.3% | National, led by California | Medium term (2-4 years) |

| OEM factory-fill specifications expanding premium-grade demand | +0.2% | Michigan, Tennessee, Alabama | Long term (≥ 4 years) |

| Fleet digitalization enabling predictive oil-life extension services | +0.1% | National logistics corridors | Short term (≤ 2 years) |

| Telematics-linked maintenance contracts boosting aftermarket volumes | +0.1% | Fleet-dense Midwest & Texas | Medium term (2-4 years) |

| California “Buy Clean” rules favoring bio-based additive packages | +0.1% | California, Pacific Northwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent CAFE/GHG Norms Accelerating Shift to Low-Viscosity Synthetics

NHTSA’s model-year 2024-2026 targets push automakers toward 49 mpg corporate averages, forcing adoption of 0W-20 and 5W-30 factory fills that slash parasitic drag[1]National Highway Traffic Safety Administration, “Final Rule for Model-Year 2024-2026 Fuel-Economy Standards,” nhtsa.gov. Ford and General Motors already specify 0W-20 across most gasoline line-ups, lifting that grade’s share of new-vehicle requirements from 8% in 2010 to 42% in 2024. AAA laboratory testing confirmed 0W-20 boosts fuel economy by 2.8% on average and cuts cold-start wear by 73% versus 5W-30, benefits that resonate in northern states. The November 2024 finalization of API’s ILSAC GF-8A locks in the trend by eliminating 5W-40 and 10W-40 passenger-car oils and demanding stricter low-speed pre-ignition protection. As a result, synthetic penetration reached 68% of the USD 8.2 billion US motor-oil market in 2024, up sharply from the prior decade.

OEM Factory-Fill Specifications Expanding Premium-Grade Demand

Automaker warranty terms now hinge on API-licensed or proprietary synthetics that can survive 10,000-mile intervals without viscosity loss. Tesla specifies Pentosin FFL-4 fluids, while Ford’s WSS-M2C961-A1 synthetic is mandatory for 2026 Explorer and F-150 models. Deviating from these grades can void powertrain coverage, effectively locking owners into premium lubricants. The new GF-8A durability test raises the bar further, forcing blenders to invest in higher-tier additive packages. Connected-vehicle data lets OEMs police compliance remotely, curbing off-spec top-offs and safeguarding engine warranties.

Fleet Digitalization Enabling Predictive Oil-Life Extension Services

Predictive-maintenance telematics moved from 27% fleet adoption in 2024 to a projected 65% by 2026, extending drain intervals and trimming unnecessary oil changes by up to 25%. Prairie States Transportation stretched intervals to 60,000 miles, reducing annual oil spend per truck by USD 441 and saving USD 847,000 across its 185-truck fleet. Castrol’s Fleet Health platform combines fluid analysis with AI algorithms that pre-empt 30% of engine faults, translating into lower downtime and parts replacement. Although volume per vehicle drops, data-subscription models at USD 25-40 per truck per month generate a new revenue stream for service providers.

Telematics-Linked Maintenance Contracts Boosting Aftermarket Volumes

Volvo Trucks’ Blue Service Contract bundles adaptive intervals, lubricant supply, and laboratory analysis, shifting fleets from fixed-mileage rules to chemistry-based triggers. Valvoline’s quick-lube network showed 5.8% same-store sales growth in fiscal Q1 2026, thanks to bundled synthetic-oil plans that lift ticket values. Take 5 Oil Change notes that synthetic users return 2.7 times per year versus 2.1 for conventional customers, validating the up-sell logic. These contracts amplify wallet share even as the absolute number of services declines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended drain intervals cutting per-vehicle lubricant consumption | -0.5% | Midwest & Texas fleets | Medium term (2-4 years) |

| Volatile base-oil feedstock prices squeezing blender margins | -0.2% | Gulf Coast refineries | Short term (≤ 2 years) |

| Shared-mobility subscriptions eroding DIY oil-change traffic | -0.2% | Urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Drain Intervals Cutting Per-Vehicle Lubricant Consumption

Modern oil-life monitors authorize up to 10,000-mile passenger-car intervals and 80,000-mile diesel-truck intervals, slashing annual changes per asset by half. Prairie States Transportation moved from 4.6 to 1.9 oil changes per truck, proving the math behind the volume decline. Even with synthetic oils priced at double conventional grades, a 2.5 times interval extension still erodes lifecycle revenue per vehicle by about 20%.

Volatile Base-Oil Feedstock Prices Squeezing Blender Margins

Group II N100 prices whipsawed between USD 1,482 and USD 1,749 per metric ton in 2025, while the N100-to-diesel crack spread fell to a 20-month low of USD 0.48 per gallon. Independent blenders cannot fully hedge these swings, forcing inventory write-downs. ExxonMobil’s 2026 investment in an 8,000 bpd Group III unit at Baytown aims to secure a captive supply and smooth margins when the plant starts in 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetic Migration Offsets Monograde Obsolescence

Automotive engine oil dominated the United States Automotive Lubricants market with a 60.43% share in 2025. Within this category, 0W-20 and other 0W-XX grades already represent most of factory-fill needs and are forecast to capture even more by 2031 as OEMs chase CAFE compliance. The automatic transmission fluids (ATF) market share is expected to drop with a CAGR of -0.07% during the forecast period (2026-2031) due to a potential rise in the demand for electric vehicles. The United States automotive lubricants market size for automatic transmission fluids contracts the least, held back by the surge in 8-10-speed gearboxes that require friction-specific Dexron-ULV and Mercon-ULV fluids. Monogrades and high-viscosity 10W-40 lines face terminal decline because GF-8A and OEM warranties no longer recognize them.

R&D is flocking to experimental 0W-16 and 0W-8 oils that cut high-temperature shear further. Meeting wear limits at these viscosities will demand roughly USD 4.5 billion in additive and base-stock innovation over the next five years. Automatic transmission fluids benefit from proprietary additive chemistry that prevents shudder across wide gear-ratio spreads. Manual-transmission and brake-fluid demand shrinks as EVs delete traditional gears and rely on regenerative braking, although Tesla’s DOT 4-only spec carves out a high-margin niche.

By Vehicle Type: Commercial Fleets Leverage Telematics to Slow Decline

Passenger vehicles captured 56.38% of the 2025 volume but face the sharpest contraction as extended drains and EV substitution bite. The United States automotive lubricants market share commanded by passenger vehicles erodes steadily despite high synthetic penetration, which only partially raises revenue per liter. Conversely, commercial trucks decline at a milder -0.23% CAGR through 2031 because API CK-4 and FA-4 oils enable longer drains without sacrificing warranty coverage.

Telematics contracts such as Volvo Trucks’ Blue Service shift fleets from mileage clocks to chemistry triggers, preserving lubricant wallet share through bundled analytics and parts. The December 2026 debut of API PC-12 (CL-4 and FB-4) is poised to add 0W-20 diesel grades, delivering up to 2% fuel-savings that more than offset the per-gallon cost premium. Two-wheelers remain volume-trivial, although enthusiasts maintain loyalty to high-viscosity gear oils outside mainstream OEM specs.

Geography Analysis

California sets the regulatory tempo for the United States Automotive Lubricants market, even though it holds only 12% of national registrations. It's 2027, heavy-duty nitrogen-oxide rule forces engine builders nationwide to certify to PC-12 oils, while its PFAS-reporting mandate accelerates movement toward bio-based additives[2]California Air Resources Board, “2027 Heavy-Duty NOx Standards,” arb.ca.gov. Pacific Northwest and Northeast states historically echo California within two years, amplifying its influence.

The Midwest logistics spine along I-80 and the Texas corridor along I-10 consume disproportionate diesel-oil volumes. Fleets in these regions adopt predictive maintenance fastest, leveraging long highway duty cycles to stretch drains to 60,000-80,000 miles. Gulf Coast refineries in Texas and Louisiana supply most base stocks; ExxonMobil’s Baytown Group III expansion will entrench the region as the only US source spanning Group I-V feedstocks by 2028.

Urban centers, New York, Los Angeles, San Francisco, and Chicago, lead EV and shared-mobility uptake, sapping DIY oil-change traffic. Northern tier states embrace 0W-20 for cold-start protection, whereas the Sunbelt still favors 5W-30 for thermal durability, though GF-8A is harmonizing preferences. Quick-lube consolidation follows population density, with Valvoline and Take 5 clustering stores in suburban belts where 70% customer loyalty underpins private-equity valuations above 10× EBITDA.

Competitive Landscape

The United States Automotive Lubricants market is moderately consolidated. White-space growth resides in bio-based friction modifiers and re-refined Group II oils. Despite a 42% lower lifecycle carbon footprint, re-refined base stocks make up less than 5% of blending feed, signaling a margin-accretive opportunity for brands able to secure waste-oil supply chains.

United States Automotive Lubricants Industry Leaders

ExxonMobil Corporation

Shell plc

BP p.l.c.

Chevron Corporation

Saudi Arabian Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: LIQUI MOLY announced the start of local motor oil production in the United States to serve American customers more quickly and with more flexibility.

- March 2025: BP p.l.c. launched a strategic review of its Castrol business, considering options such as a complete divestiture, aiming to hasten Castrol's next phase of value delivery. This could impact the company's business in the United States Automotive Lubricants market.

United States Automotive Lubricants Market Report Scope

Automotive lubricants, encompassing engine oils, gear oils, and greases, play a pivotal role in reducing friction, wear, and heat among moving parts. This not only boosts engine performance and efficiency but also extends its lifespan. These lubricants, made from a combination of base oils and additives, serve multiple functions: they clean, cool, and guard against corrosion.

The United States Automotive Lubricants market report is segmented by product type (automotive engine oil, manual transmission fluids, automatic transmission fluids, brake fluids, automotive greases, and other product types (power steering fluid and more)) and vehicle type (passenger vehicles, commercial vehicles, and two-wheelers). The market forecasts are provided in terms of volume (liters).

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid and More) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid and More) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large is the United States automotive lubricants market in 2026?

The United States automotive lubricants market size stands at 3.19 billion liters in 2026, continuing a gradual slide toward 3.12 billion liters by 2031.

Which product type holds the largest share?

Automotive engine oil leads with a 60.43% share of 2025 volume and remains the dominant segment despite volume pressure.

What is driving the move to low-viscosity grades?

Stricter CAFE rules and API’s ILSAC GF-8A specification compel OEMs to factory-fill with 0W-20 and 5W-30 synthetics that improve fuel economy by 2.5-4.5%.

How are fleets reducing lubricant consumption?

Predictive-maintenance telematics stretch drain intervals to 60,000-80,000 miles on heavy trucks, halving annual oil changes while preserving uptime.

Will bio-based additives gain traction?

California’s 2026 PFAS-reporting mandate and 2027 NOx limits create regulatory pull for bio-based friction modifiers and re-refined base oils with lower carbon footprints.

Page last updated on: