Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

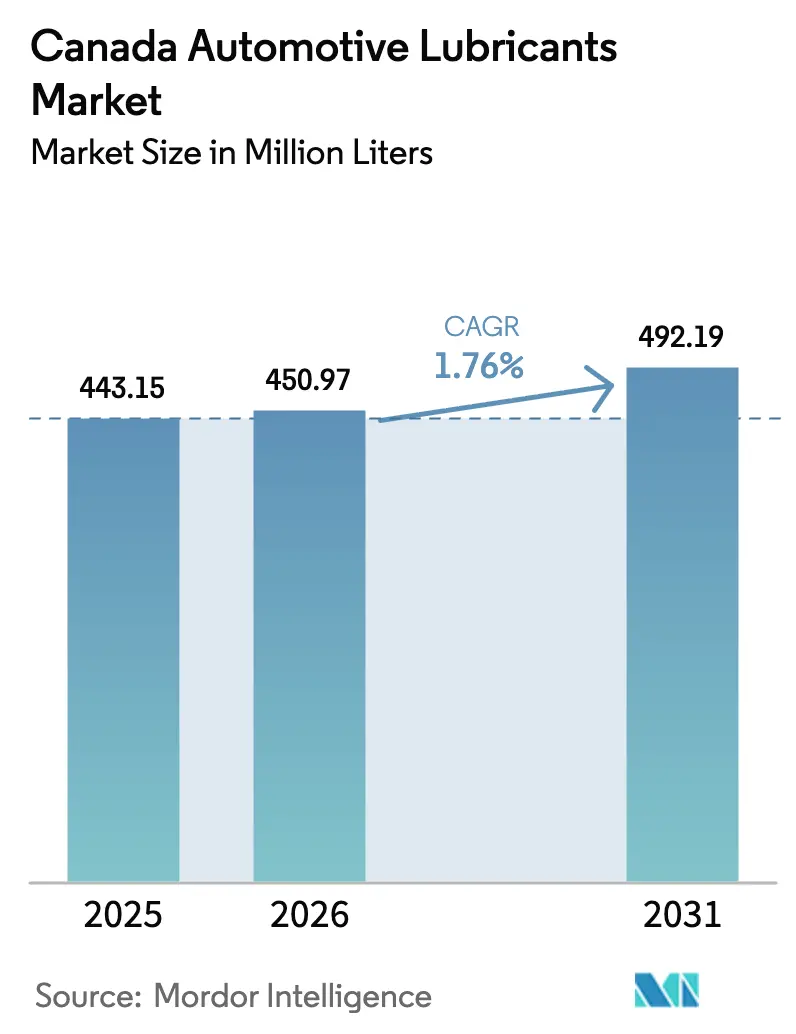

| Base Year Market Size (2025) | 443.15 Million liters |

| Market Volume (2026) | 450.97 Million liters |

| Market Volume (2031) | 492.19 Million liters |

| Growth Rate (2026 - 2031) | 1.76% CAGR |

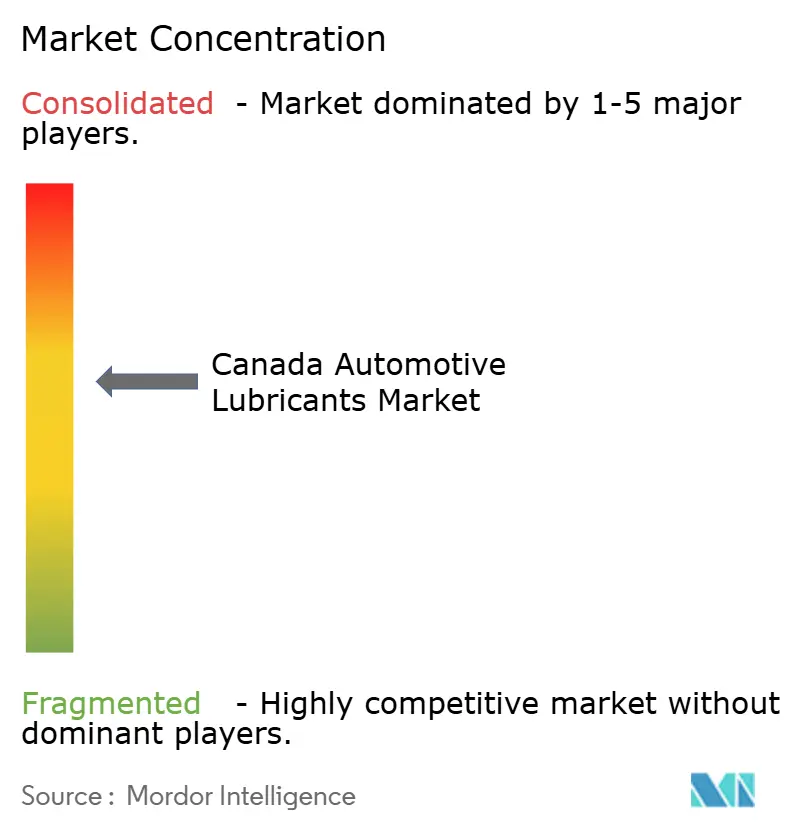

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Automotive Lubricants Market Analysis by Mordor Intelligence

The Canada Automotive Lubricants Market size is projected to be 443.15 million liters in 2025, 450.97 million liters in 2026, and reach 492.19 million liters by 2031, growing at a CAGR of 1.76% from 2026 to 2031. As light-duty electrification targets curtail internal combustion volumes, the rise of synthetic oils and high-value specialty fluids bolsters revenue streams. With the Federal Clean Fuel Regulations tightening carbon limits, fuel blenders are pivoting to additive-rich, low-viscosity formulations[1]Canadian Fuels Association, “Clean Fuel Regulations,” canadianfuels.ca . These advanced formulations are more adept at handling elevated blends of ethanol and renewable diesel. Original equipment manufacturers (OEMs) are now pushing for 0W-16 and 0W-20 grades in their turbocharged gasoline direct-injection engines, further accelerating the trend toward premiumization. E-commerce platforms are now allowing synthetic stock-keeping units (SKUs) to directly reach do-it-yourself consumers, effectively sidestepping traditional distributor mark-ups. Amidst these industry shifts, integrated refiners are leveraging Alberta's Group III base-oil supply and establishing a coast-to-coast retail presence to bolster their market share. In contrast, independent players are honing in on specialized markets, particularly in electric-drivetrain and multi-vehicle transmission fluids.

Key Report Takeaways

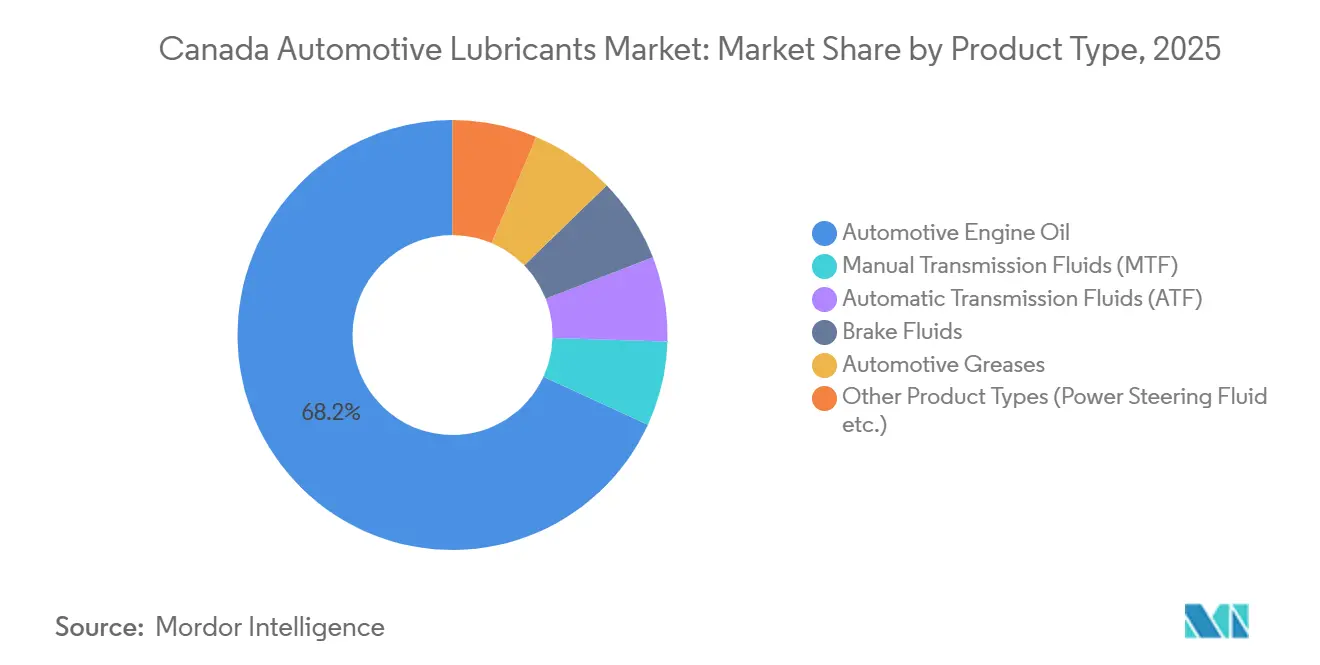

- By product type, automotive engine oil led with 68.17% of Canada automotive lubricants market share in 2025; automatic transmission fluids recorded the fastest projected CAGR at 2.10% through 2031.

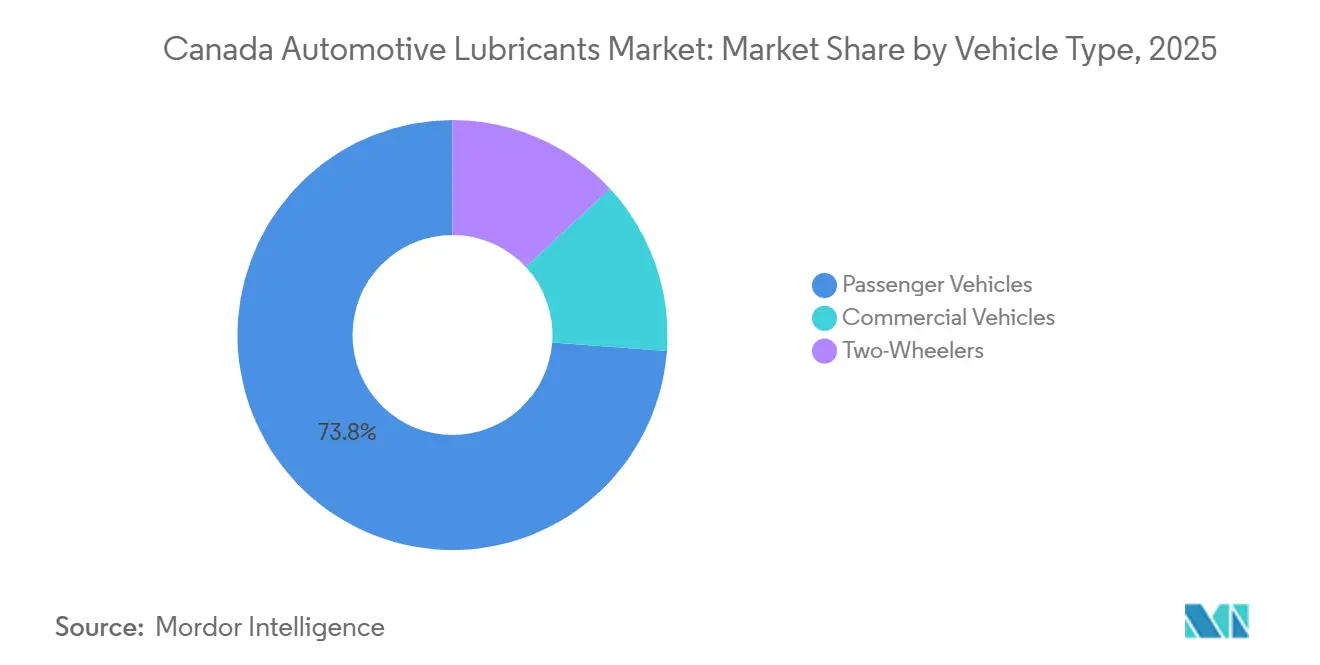

- By vehicle type, passenger vehicles accounted for 73.82% of the Canada automotive lubricants market size in 2025 and are forecast to expand at a 1.83% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM-mandated low-viscosity synthetics for fuel-economy compliance | +0.50% | National, with concentration in Ontario, Quebec, and British Columbia automotive manufacturing hubs | Medium term (2–4 years) |

| Federal Clean Fuel Regulations raising demand for high-efficiency additive packages | +0.40% | National, administered by Environment and Climate Change Canada | Long term (≥ 4 years) |

| E-commerce and omnichannel aftermarket widening access to premium SKUs | +0.30% | National, with higher penetration in urban centers (Toronto, Montreal, Vancouver) | Short term (≤ 2 years) |

| Abundant domestic Group III base-oil supply from oil-sands upgraders | +0.20% | Alberta (Strathcona, Scotford, Horizon upgraders), with distribution nationwide | Long term (≥ 4 years) |

| Cold-climate performance needs driving ultra-low-temperature formulations | +0.40% | National, with acute demand in Prairies, Northern Territories, and Quebec | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

OEM-Mandated Low-Viscosity Synthetics for Fuel-Economy Compliance

Automakers, in a bid to meet fleet-average fuel-economy regulations, are increasingly gravitating towards 0W-16 and 0W-20 grades. This shift has resulted in a waning demand for the 5W-30 and 10W-30 grades. Petro-Canada’s Supreme Synthetic 0W-16, compliant with API SN Plus and GM dexos1 Gen 3 standards, plays a pivotal role in averting low-speed pre-ignition in turbocharged gasoline direct-injection engines. The ILSAC GF-7 standard, finalized in 2025, promised extended drain intervals and bolstered anti-wear standards. This evolution has birthed a two-tier market, with premium synthetics eclipsing legacy mineral oils. Integrated suppliers, who own refineries, base-oil plants, and retail sites, can distribute nationwide and mitigate higher formulation costs. On the other hand, independent blenders, reliant on spot Group II imports, grapple with margin pressures and risk delisting if they overlook the latest OEM approvals. The surge in hybrid vehicles underscores the heightened demand for ultra-low-viscosity synthetics, essential for rapid oil circulation during frequent start-stop cycles.

Federal Clean Fuel Regulations Raising Demand for High-Efficiency Additive Packages

By 2030, the Clean Fuel Regulations aim to cut the lifecycle carbon intensity of gasoline and diesel, referencing 2016 benchmarks[2]IETA, “Canada Clean Fuel Regulation at a Glance,” ieta.org . This initiative has spurred a rise in ethanol blending and renewable-diesel co-processing. However, additive manufacturers now face challenges, such as fuel dilution and soot from bio-components, leading to a surge in demand for detergents, antioxidants, and dispersants. In response, refiners like Imperial Oil have adjusted fuel pump prices to account for these added costs. For Canada's automotive lubricants market, these escalating costs heighten the allure of synthetics. Despite their premium pricing, synthetics promise extended drain intervals. Imperial Oil’s Strathcona renewable-diesel unit, inaugurated in mid-2025, underscores the intricate link between fuel and lubricant dynamics, illustrating how upstream fuel tweaks can reshape downstream lubricant requirements due to shifts in combustion chemistry.

E-Commerce and Omnichannel Aftermarket Widening Access to Premium SKUs

Online platforms have carved out a substantial share of Canadian aftermarket parts sales, with motor oil consistently ranking in the top three. Brands like AMSOIL leverage these digital avenues to spotlight their 100% synthetic CVT fluids, bolstered by comprehensive data sheets and consumer ratings, deftly bypassing the traditional retail gatekeepers. While traditional retailers are witnessing a comeback, they are contending with hurdles like technician shortages and volatile parts pricing. This omnichannel retail strategy not only accelerates customer choices but also nudges suppliers to invest in search-optimized content, real-time inventory tracking, and prompt order fulfillment. As distributors refine their stock, products like TotalEnergies' Fluidsyn ATF/CVT, a versatile multi-vehicle ATF and universal synthetic blend, find prime shelf space due to their broad vehicle coverage.

Cold-Climate Performance Needs Driving Ultra-Low-Temperature Formulations

In regions like the Prairies and Northern Territories, where winter temperatures can plummet below -30°C, there is an urgent demand for lubricants that remain pumpable at -40°C. Synthetic oils, unlike their mineral counterparts that congeal at -15°C, retain their fluidity at lower temperatures. This advantage not only hastens oil pressure build-up but also minimizes metal-to-metal contact during frigid starts. Petro-Canada's Supreme Synthetic range, with pour points reaching -45°C, aligns perfectly with OEM's 0W-20 recommendations for frigid locales. Heavy-duty fleets are shifting from SAE 15W-40 to 10W-30 and 5W-30 grades, prioritizing fuel efficiency and smoother engine cranking. Transmission and CVT fluids, too, face the dual challenge of transmitting torque in cold conditions while resisting oxidation in heat. This premium placed on climate-adapted lubricants strengthens the Canadian automotive lubricants market, even as coastal regions witness a surge in electric vehicle (EV) adoption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet electrification eroding ICE-oil volumes | -0.60% | National, with accelerated impact in British Columbia (greater than 20% ZEV adoption) and Quebec (provincial rebates up to CAD 7,000) | Long term (≥ 4 years) |

| On-board oil-life monitoring extending drain intervals | -0.30% | National, concentrated in newer passenger vehicles and commercial fleets with telematics | Medium term (2–4 years) |

| Import-driven price competition squeezing local blenders' margins | -0.20% | National, with pressure points in Ontario and Quebec distribution hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet Electrification Eroding ICE-Oil Volumes

Federal targets set ambitious goals for light-vehicle sales, aiming for a substantial shift to zero-emission vehicles (ZEVs) by 2035 - with further increases projected by 2040. These targets, bolstered by purchase incentives and a growing network of charging stations, find a frontrunner in British Columbia, which already boasts a significant share of ZEVs. Among these, battery-electric vehicles, notably free from the need for engine oil, make up a considerable volume. While the demand for heavy-duty on-highway diesel is set to wane over the next fifteen years, the segment's value is buoyed by the rising adoption of premium synthetics, even as the overall volume in liters diminishes. On another front, off-highway mining and construction equipment are projected to rely on internal combustion engines until 2040. This reliance somewhat alleviates industry challenges, yet the total consumption of lubricant liters still trends downward.

On-Board Oil-Life Monitoring Extending Drain Intervals

Vehicles produced post-2015 are increasingly outfitted with sophisticated oil-life monitors, adjusting change intervals in real-time based on driving conditions. This innovation can significantly elongate service intervals, especially with the use of synthetic oils. Take Ford’s Intelligent Oil-Life Monitor, for instance; it alerts drivers only when the oil is nearing the end of its useful life. Commercial fleets are now adopting these advanced sensors, integrating them with telematics systems. This synergy empowers fleets to delay workshop visits until analytics deem it necessary, resulting in a notable dip in lubricant consumption per vehicle. Highlighting this market trend, Petro-Canada’s DURON HD Synthetic 668 ATF, designed for extended drains, points to a tightening volume squeeze while simultaneously showcasing an uptick in revenue per liter.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transmission Fluids Outpace Engine-Oil Growth

Automatic transmission fluids are projected to grow at a 2.10% CAGR during the forecast period of 2026-2031. This growth is driven by the increasing adoption of Continuously Variable Transmissions (CVTs) in hybrid and fuel-efficient vehicles. Additionally, the rising popularity of multi-vehicle synthetic ATFs, which simplify inventory management, plays a significant role. TotalEnergies' Fluidsyn ATF/CVT product is compatible with more than 95% of light vehicles. In engine oils, grades 0W-XX and 5W-XX are surpassing 10W-XX and 15W-XX, driven by Original Equipment Manufacturers (OEMs) pursuing fuel-economy credits. While engine oil commands a dominant 68.17% share in Canada's automotive lubricants market in 2025, its influence is gradually declining, making way for specialty fluids. These emerging fluids, such as multi-vehicle synthetics, universal CVT formulas, and those tailored for next-generation electric vehicles (EVs), are contributing to increased value creation. Brake fluids and greases, though growing steadily, are influenced by mandated maintenance intervals and components designed to be "sealed for life."

A noticeable shift toward synthetic premiumization is underway. In 2025, TotalEnergies transitioned from its mineral lines Quartz 7000 and Rubia Optima 1300 to synthetic technologies, highlighting benefits such as improved cold-flow, cleanliness, and fuel efficiency. Petro-Canada's Supreme UHP Hybrid fluid caters to hybrid engines, mitigating start-stop stresses. Chevron and AMSOIL promote CVT fluids that meet specifications from more than 20 OEMs. Manual transmission fluids, while still favored in performance circles, are losing traction to the more prevalent dual-clutch and automatic systems. Specialty greases are evolving toward polyurea and lithium-complex chemistries, offering extended relubrication intervals and reduced consumption per vehicle.

By Vehicle Type: Passenger Cars Anchor Volume Despite Production Headwinds

Passenger vehicles accounted for 73.82% of the Canadian automotive lubricants market share in 2025, with a projected growth of 1.83% CAGR during the forecast period of 2026-2031. The used-vehicle market, outpacing new sales by a three-to-one ratio, bolsters the aftermarket. Despite a predicted decline in new vehicle sales in 2026, the average age of vehicles on the road has reached 9.7 years, extending the maintenance-service revenue window. Commercial vehicles, though a smaller volume segment, yield significant value, especially through high-margin heavy-duty synthetics. For instance, Petro-Canada's DURON UHP 10W-30 claims fuel savings over the 15W-40 variant. Two-wheelers, while a niche market, remain stable and require wet-clutch-compatible formulations.

However, trade frictions pose challenges. U.S. tariffs enacted in 2025 led to a decline in Canadian vehicle production, with further reductions projected in 2026, affecting OEM first-fill volumes. Nevertheless, the delayed replacement of vehicles bolsters resilience in the passenger-car aftermarket. While the electrification of commercial fleets reduces diesel volumes, sectors such as off-highway mining, agriculture, and construction - often in remote areas with charging challenges - continue to drive strong lubricant demand. In conclusion, despite setbacks in OEM factory-fill volumes, Canada's passenger-vehicle service bays in the automotive lubricants market remain robust.

Geography Analysis

Ontario and Quebec's automotive dominance is fueled by assembly plants from Stellantis, Ford, GM, Honda, and Toyota, alongside over 700 tier-one suppliers in the "Auto Valley" corridor. While Federal Clean Fuel Regulations apply nationwide, British Columbia's Low Carbon Fuel Standard accelerates the adoption of renewable diesel and influences the demand for lubricant additives. Alberta's oil-sands upgraders provide Group III base stocks to domestic blenders, protecting them from import price swings, and sequester significant CO₂ amounts annually via the Quest CCS facility.

Cold weather shapes viscosity preferences: the Prairies and Northern Territories favor 0W-20 and 0W-30, while coastal British Columbia opts for 5W-30. Quebec's French-language and consumer-protection regulations complicate labeling, but the province's harsh winters drive a robust demand for synthetics. Despite being a smaller market, Atlantic Canada faces maritime humidity challenges that hasten lubricant degradation, resulting in a steady demand for replacements.

British Columbia's significant stake in zero-emission vehicles (ZEV) is steering the market towards EV-specific fluids. The federal Strategic Response Fund and Regional Tariff Response Initiative are heavily investing in diversifying Canadian auto manufacturing, potentially reshaping lubricant logistics hubs over the next decade. Meanwhile, mining activities in Northern Quebec, Ontario, and British Columbia are driving demand for off-highway lubricants, even as heavy equipment electrification lags.

Competitive Landscape

The Canada automotive lubricants market is moderately consolidated. Integrated refiners like Imperial Oil (Esso/Mobil), Shell (Petro-Canada Lubricants), and Chevron utilize captive crude, proprietary catalysts, and a branded service station network to maintain their combined market share. Imperial Oil promoted lube oils through its extensive nationwide network. TotalEnergies, fully transitioned to synthetic technology, launched Quartz EV-Drive R 3.1, Canada's first major-brand EV-reducer fluid, capitalizing on an early market opportunity. BP's strategic review of Castrol suggests potential divestiture scenarios, possibly altering current distribution partnerships.

Independent players are finding their footing: FUCHS is pushing its FUCHS2025 initiative, emphasizing North American blending hubs and carbon-neutral products. Chevron's Delo TorqForce MP, with Allison TES 781 approval, highlights extended off-highway transmission drain intervals for maintenance savings. AMSOIL, harnessing e-commerce and strong customer ratings, is capturing DIY market share from traditional auto-parts retailers. Catalys (LubeSource) is offering private-label programs, appealing to jobbers keen on margins in a price-sensitive landscape.

Growth prospects are evident in EV fluids, extended-drain heavy-duty synthetics, and universal ATF/CVT products. Suppliers securing OEM approvals, building a digital footprint, and validating products for cold-weather use are set to dominate the Canadian automotive lubricants arena.

Canada Automotive Lubricants Industry Leaders

Shell Plc

Imperial Oil Limited

Petro‐Canada Lubricants Inc.

BP p.l.c.

Saudi Arabian Oil Co. (Valvoline Global Operations)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Petro-Canada Lubricants introduced its EVR fluids, engineered specifically for electric drivetrain and thermal management applications. This launch is expected to strengthen the company's position in the Canada automotive lubricants market by addressing the growing demand for specialized fluids in electric vehicles.

- February 2024: TotalEnergies Lubricants has entered into a five-year distribution agreement with Boss Lubricants to strengthen its market presence in Western Canada. This partnership is expected to enhance the availability of high-quality lubricants in the region, potentially driving growth and competition within the Canada automotive lubricants market.

Canada Automotive Lubricants Market Report Scope

Automotive lubricants reduce friction between contacting surfaces, thereby minimizing energy loss. These lubricants are vital for ensuring vehicles operate smoothly and have a prolonged lifespan. Engine oil, the most prevalent lubricant, not only reduces friction among engine components but also prevents corrosion, combats rust, and aids in cleaning the engine.

The Canada automotive lubricants market is segmented by product type and vehicle type. By product type, the market is segmented into automotive engine oil, manual transmission fluids, automatic transmission fluids, brake fluids, automotive greases, and other product types. By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What volume will the Canada automotive lubricants market reach by 2031?

The Canada automotive lubricants market size stands at 450.97 million liters in 2026, and it is projected to reach 492.19 million liters by 2031 at a 1.76% CAGR.

Which product category is growing fastest in Canada?

Automatic transmission fluids are forecast to grow at a 2.10% CAGR to 2031, outperforming engine oils.

How is electrification affecting lubricant demand?

Rising zero-emission vehicle sales are trimming internal-combustion engine oil volumes, but premium synthetic grades and EV-specific fluids are offsetting some losses.

Why are low-viscosity synthetics gaining share?

OEM fuel-economy targets require 0W-16 and 0W-20 oils that cut friction and support turbocharged engines, driving consumers toward full synthetics.

What is driving regional differences in lubricant needs?

Climate extremes, provincial fuel-carbon rules, and varying EV-incentive levels create distinct viscosity, additive, and product-mix requirements across provinces.

Page last updated on: