Bangladesh Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

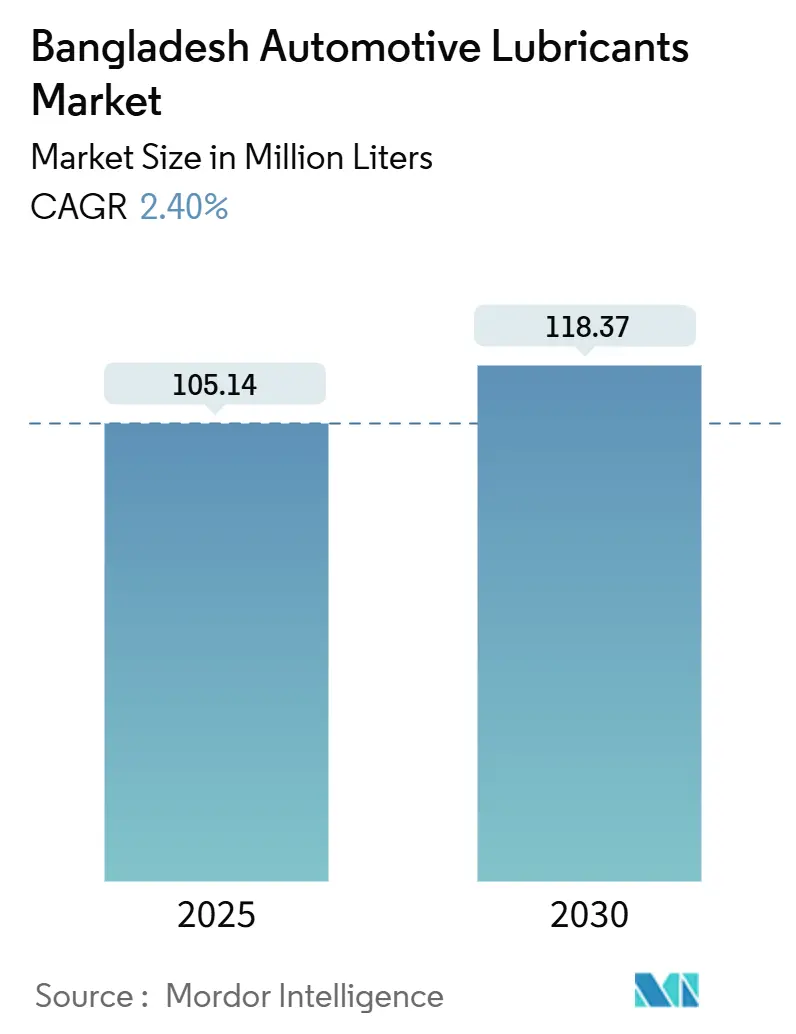

| Market Volume (2025) | 105.14 Million liters |

| Market Volume (2030) | 118.37 Million liters |

| Growth Rate (2025 - 2030) | 2.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Automotive Lubricants Market Analysis by Mordor Intelligence

The Bangladesh Automotive Lubricants Market size is estimated at 105.14 million liters in 2025, and is expected to reach 118.37 million liters by 2030, at a CAGR of 2.40% during the forecast period (2025-2030). Stable macroeconomic growth, accelerated road and bridge construction, and a growing OEM footprint anchor demand, while gradual electrification and pervasive counterfeit products temper the outlook. Engine oil volumes remain underpinned by Bangladesh’s large motorcycle parc, yet rising automatic-transmission adoption in urban passenger vehicles and modern fleet renewal in road freight introduce higher-value lubricant niches. Organized retail chains in Dhaka and Chittagong now bundle installation services and digital payments, improving product authenticity and tilting preferences toward synthetics. At the same time, import-dependent raw-material costs and weak rural enforcement sustain a dual market where premium brands and counterfeit offerings coexist. Over the forecast horizon, the Bangladesh automotive lubricants market is expected to see incremental volume growth, but a faster shift in grade mix toward low-viscosity, fuel-efficient, and OEM-approved synthetics.

Key Report Takeaways

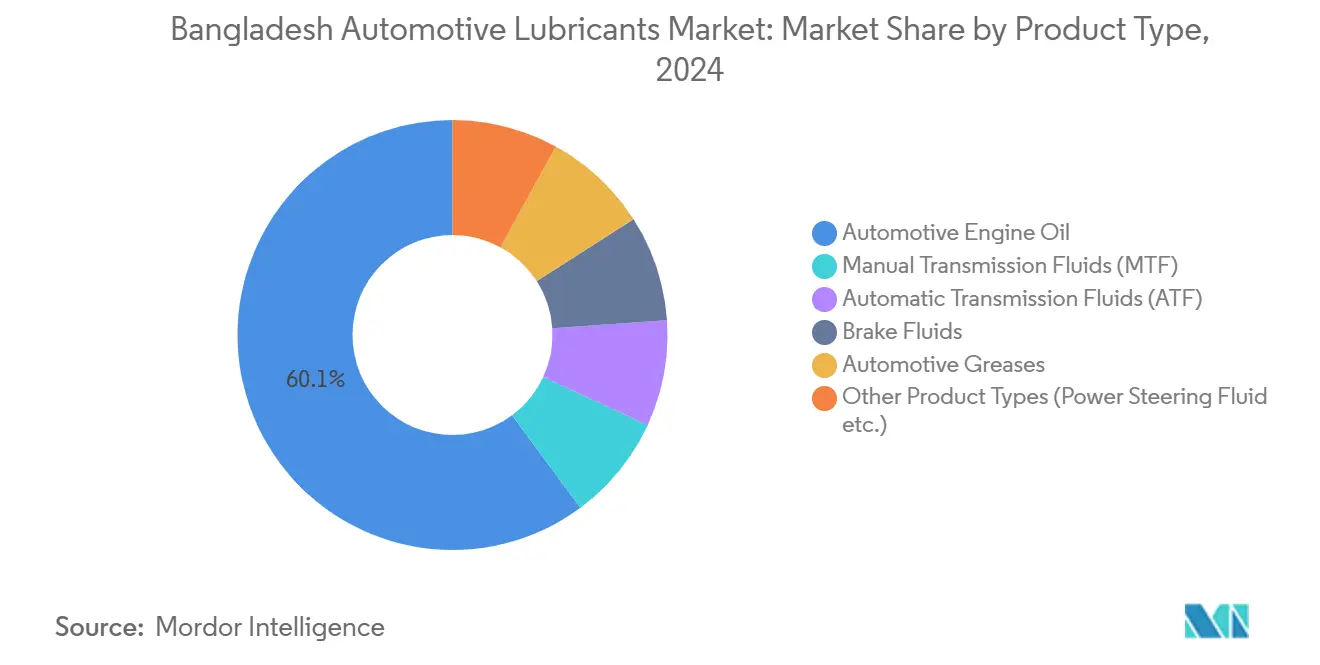

- By product type, automotive engine oil captured 60.13% of the Bangladesh automotive lubricants market share in 2024, while automatic transmission fluids are forecast to expand at a 2.56% CAGR through 2030.

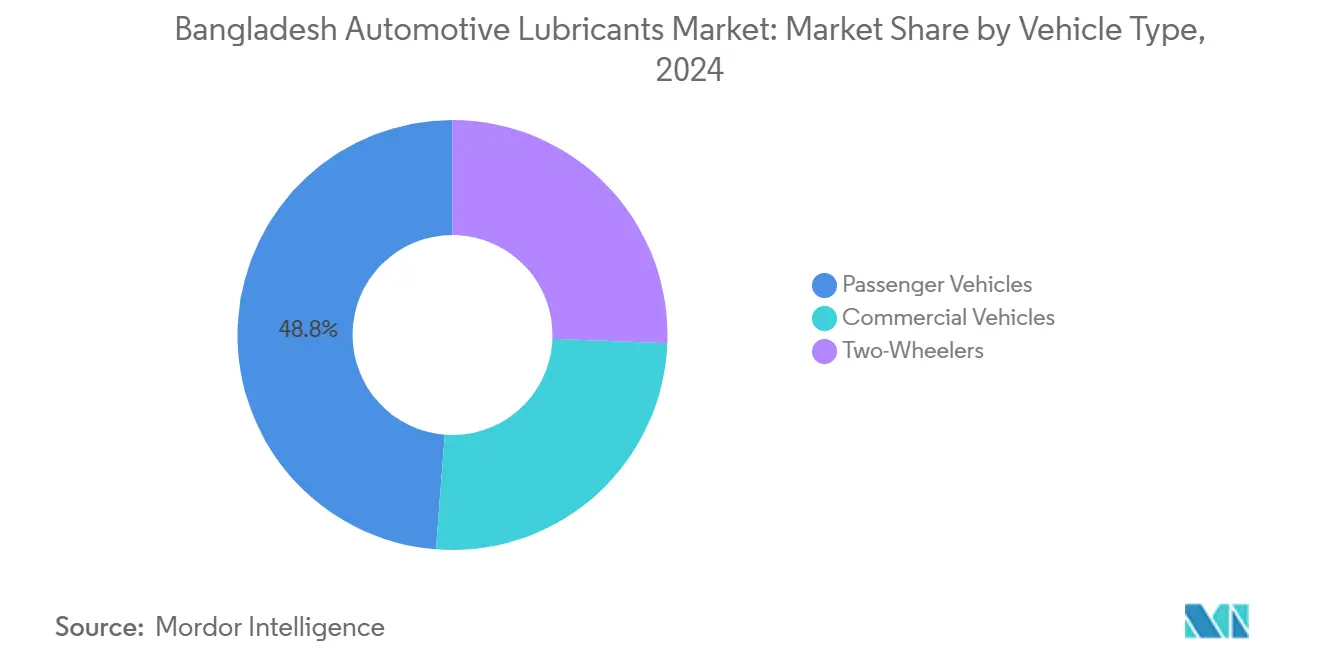

- By vehicle type, passenger vehicles accounted for 48.78% of the Bangladesh automotive lubricants market size in 2024, whereas commercial vehicles are set to post the fastest 2.67% CAGR during 2025-2030.

Bangladesh Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steady rise in two-wheeler ownership | +0.8% | Dhaka, Chittagong, Sylhet | Medium term (2-4 years) |

| Urbanisation & logistics fleet expansion | +0.6% | Tier-1 cities, emerging industrial corridors | Long term (≥ 4 years) |

| Branded retail lubricant chains | +0.4% | Metropolitan Dhaka and Chittagong | Short term (≤ 2 years) |

| OEM-backed awareness of synthetics | +0.3% | National, premium buyer segments | Medium term (2-4 years) |

| Shift toward low-viscosity grades | +0.2% | Urban OEM-service channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steady Rise in Two-Wheeler Ownership

Motorcycle registrations, buoyed by the 2023 ceiling lift to 375 cc and the launch of local Royal Enfield assembly, continue to expand the active fleet despite the FY24 sales dip. Higher-displacement bikes require specialized low-friction synthetics, while the far larger 100-150 cc pool sustains high-frequency drain intervals that favor mineral and semi-synthetic blends. Local assemblers such as Ifad Motors increasingly specify branded lubes at point of sale, deepening aftermarket brand lock-in and encouraging co-marketing between OEMs and lubricant blenders. An aging parc—average bike age exceeds seven years—magnifies maintenance demand, ensuring that the Bangladesh automotive lubricants market retains a sizable two-wheeler service segment even as new-vehicle volumes fluctuate. Rising ride-sharing and last-mile delivery platforms in Dhaka further intensify engine-oil usage cycles. Over the medium term, this demographic driver adds positive momentum to overall volume while steering lubricant grade evolution toward lighter-viscosity, higher-detergency formulations.

Urbanization & Logistics Fleet Expansion

Padma Bridge and Bangabandhu Tunnel have shortened key haulage routes, allowing higher daily truck mileage and compressing the refill interval for heavy-duty engine oils [1]Staff Correspondent, “Padma Bridge Cuts Travel Time, Boosts Logistics,” tbsnews.net. E-commerce fulfillment, pharmaceutical cold-chain growth, and the 85% trade dominance of Chattogram Port collectively raise lubricant consumption per commercial vehicle as utilization climbs. Dedicated delivery fleets now track lubricant condition to minimize downtime, stimulating the adoption of premium extended-drain synthetic lubricants. New economic zones along the Dhaka-Matarbari logistics spine draw incremental truck and van procurement, reinforcing commercial-grade demand within the Bangladesh automotive lubricants market. The adoption of telematics for preventive maintenance supports data-driven lubricant replenishment contracts, a capability currently offered by leading suppliers to fleet operators with over 100 vehicles.

Branded Retail Lubricant Chains in Dhaka/Chittagong

Organized outlets bundle quick-lube services, warranty cards, and counterfeit-proof packaging, persuading urban motorists to trade up from informal shops that historically dominated supply. Global majors partner with fuel marketers and dealer networks, converting forecourts into multiproduct auto-service hubs. POS digital payment and inventory platforms lower retailer working capital as SKUs turn faster, enabling competitive pricing on genuine synthetic oils. These improvements accelerate premium-grade penetration in metropolitan areas where motorist willingness to pay aligns with disposable income. While organized coverage remains below one-third of national demand, rapid urban expansion and franchising present a viable path to 50% channel share by 2030, reshaping distribution economics and indirectly curbing counterfeit circulation.

OEM-Backed Awareness of Synthetics

Local assemblers mandate factory-fill synthetics that meet modern emission and fuel-economy standards, reinforcing end-user perception that higher initial outlay buys measurable engine protection. BSTI’s tighter viscosity-index thresholds and volatility limits further steer workshops toward accredited suppliers. Technical education clinics organized by OEM-lube partnerships now train more than 5,000 mechanics annually, diffusing product knowledge into the independent aftermarket. The synthetic-to-mineral price ratio has narrowed to roughly 3:1 from 4:1 in 2020 as import costs stabilize, broadening the addressable consumer base in midsized cities. Over the forecast period, OEM advocacy is expected to lift synthetics’ share of the Bangladesh automotive lubricants market to double-digit percentages.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported base oils & finished lubes | -0.7% | Nationwide | Long term (≥ 4 years) |

| Counterfeit lubricant penetration | -0.5% | Rural and informal urban markets | Medium term (2-4 years) |

| Limited local blending & testing infrastructure | -0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Base Oils & Finished Lubes

Bangladesh sources nearly all Group I-III base stocks from overseas suppliers, with China and India jointly exceeding one-third of import volume[2]Asian Development Bank, “Bangladesh Petroleum Product Imports Data,” adb.org. Volatile freight rates and taka depreciation elevate landed costs, leaving local blenders exposed to currency swings and margin compression. The absence of deep-conversion refining capacity continues to throttle any near-term import substitution. While strategic storage expansion is under discussion, the current 30-day reserve level prolongs exposure to supply shocks. Over the long term, this external reliance applies downward pressure on the Bangladesh automotive lubricants market’s price competitiveness and creates planning uncertainty for investment in high-end additives.

Counterfeit Lubricant Penetration in Informal Retail

Illicit refilling and recycled-oil adulteration account for an estimated 30-40% of rural volume, eroding consumer trust and inflicting engine damage that rarely traces back to culprits. Non-registered outlets sell fake brands at up to 50% discount, exploiting motorists’ price sensitivity and limited legal recourse. BSTI mandates cover 229 petroleum derivatives, yet enforcement staff shortages and resource gaps hamper field inspections. Genuine suppliers must raise marketing spend on tamper-proof seals and holograms, raising cost of goods. Although urbanization and organized retail gradually displace informal channels, counterfeit activity will remain a medium-term drag on Bangladesh automotive lubricants market value realization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oil Dominance Faces Transmission Fluid Growth

Automotive engine oil accounted for 60.13% of the Bangladesh automotive lubricants market share in 2024, driven by the country’s climate-related three-month change intervals and a two-wheeler fleet exceeding 7 million units. The segment’s stickiness arises from universal applicability across motorcycles, passenger cars, and trucks. Yet grade composition is shifting as synthetics and lower-viscosity 0W/20 and 5W/30 blends gain OEM endorsement, raising average revenue per liter. Automatic transmission fluid exhibits the fastest 2.56% CAGR because passenger-car buyers in Dhaka and Chittagong increasingly favor AT variants. Imported mid-range sedans and crossovers now default to six-speed or CVT gearboxes, and assembled minibuses for ride-hailing services often specify ATF with a longer service life, thereby improving the value mix. Manual gear oil demand remains resilient in commercial haulage fleets but faces gradual erosion as urban last-mile operators transition to automatic vans for mitigating driver fatigue.

Across the forecast period, engine oil still anchors more than half of the Bangladesh automotive lubricants market size, yet loses single-digit percentage points of share to transmission fluids, brake fluids, and specialty greases. Brake-fluid consumption tracks vehicle-population growth, but safety-awareness campaigns sponsored by insurers promote DOT-4 upgrades, marginally extending drain intervals. Chassis and wheel-bearing greases maintain steady industrial off-take, aligned with freight-vehicle utilization. Niche products, refrigeration compressor oils and power steering fluids, benefit from cold-chain growth and vehicle sophistication, though limited volume caps their impact. The evolving product blend recommends that suppliers widen portfolios and educate retailers on correct application, differentiating through OEM approvals and performance guarantees.

By Vehicle Type: Commercial Segment Drives Premium Demand

Passenger vehicles contributed 48.78% of the Bangladesh automotive lubricants market size in 2024, primarily through low-displacement cars with modest sump capacities. However, commercial vehicles are projected to register a 2.67% CAGR to 2030, outpacing all other categories as infrastructure upgrades cut transit times and stimulate fleet renewal. Heavy-duty trucks consume up to 25 liters per drain, far exceeding the needs of light vehicles, and service intervals shorten under hot-climate, high-load operations. Fleet managers, increasingly financed by banks and micro-lenders, view synthetic 15W/40 and 10W/30 options as cost-effective over a truck’s life cycle thanks to reduced downtime. Bus operators on intercity routes add demand for long-drain coolants and gear oils, while refrigerated vans require both engine oils and compressor-specific lubricants.

Two-wheelers, although numerically dominant, collectively account for less than one-quarter of the volume due to 1-liter sump sizes and improving oil-retention technologies. Growth in ride-sharing offsets some efficiency losses, yet OEM recommendations for 5,000 km change intervals lengthen service gaps. The commercial-vehicle opportunity thus represents the primary driver of premiumization in the Bangladesh automotive lubricants market, as freight operators internalize the total cost savings from superior lubricants. Suppliers equipped to provide oil analysis, on-site training, and drum-to-bulk transition solutions stand to capture this expanding value pool.

Geography Analysis

Bangladesh's automotive lubricants market exhibits strong geographic concentration, with the Dhaka-Chittagong corridor accounting for a significant share of organized sector consumption due to industrial concentration and higher vehicle density. The capital region's dominance reflects both population concentration and economic activity, with Dhaka hosting major automotive assembly operations and serving as the primary import gateway for finished lubricants. Chittagong's significance stems from its port operations and industrial base, creating substantial commercial vehicle lubricant demand. The Padma Bridge's completion has begun redistributing logistics flows, with southern regions experiencing increased commercial activity and corresponding lubricant demand growth.

Regional market dynamics vary significantly between urban and rural areas, with organized sector’s high penetration in metropolitan centers but rel;atively lower penetration in rural districts. This disparity creates distinct market strategies, with premium brands focusing on urban retail networks while local blenders target price-sensitive rural segments. The government's infrastructure development priorities, including the Bangabandhu Tunnel and regional highway upgrades, are gradually reducing geographic disparities in market access and quality standards. Border regions face unique challenges from smuggled products and informal trade, complicating market development for legitimate suppliers.

Emerging growth corridors include the Sylhet-Chittagong industrial belt and the planned economic zones in Mongla and Payra, which are attracting manufacturing investments and creating new demand centers. The government's emphasis on decentralized industrial development aims to reduce Dhaka's congestion while creating regional economic hubs that will require expanded lubricant distribution networks. Environmental regulations under the Department of Environment framework are becoming more stringent in industrial areas, potentially favoring higher-quality lubricants that meet emission control requirements. These geographic shifts suggest opportunities for suppliers who can adapt distribution strategies to serve emerging industrial centers while maintaining strong positions in established urban markets.

Competitive Landscape

The Bangladesh automotive lubricants market is moderately fragmented, led by publicly listed MJL Bangladesh. MJL capitalizes on its Petrobangla joint venture backing and a 50,000-ton-per-year blending plant, distributing through 6,000 retail outlets. Global players operating in the market leverage fuel-station co-branding to extend penetration, while Shell focuses on industrial lubricants for the marine and power sectors. Domestic players compete on price and rural distribution reach, offering locally blended products in 1-liter pouches. Entry barriers center on BSTI certification, working-capital intensity, and brand equity, constraining new entrants to niche or private-label segments.

Bangladesh Automotive Lubricants Industry Leaders

BP p.l.c. (Castrol)

Exxon Mobil Corp. (Mobil)

Chevron Corp. (Caltex Havoline)

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: ACI Motors became the national distributor for German premium brand LIQUI MOLY, introducing high-additive motor oils tailored for tropical climates

- March 2024: TotalEnergies partnered with Asian Petroleum to integrate lubricant sales across 400 fuel stations, widening metropolitan product availability and shortening last-mile delivery cycles.

Bangladesh Automotive Lubricants Market Report Scope

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large is the Bangladesh automotive lubricants market in 2025?

The Bangladesh automotive lubricants market size stands at 105.14 million liters in 2025 and is forecast to reach 118.37 million liters by 2030.

Which lubricant segment leads by volume?

Automotive engine oil leads with 60.13% of the Bangladesh automotive lubricants market share in 2024, driven by the motorcycle and passenger-vehicle parc.

What is the fastest-growing vehicle segment for lubricants?

Commercial vehicles post the highest 2.67% CAGR between 2025 and 2030 thanks to infrastructure-led freight expansion.

How are counterfeit products affecting genuine brands?

Counterfeit oils command up to 40% of rural sales, forcing legitimate suppliers to invest in tamper-proof packaging and organized retail to protect brand equity.

Will electric-vehicle adoption curb lubricant demand?

Bangladesh targets 30% EV penetration by 2030, yet ICE vehicles will dominate through the medium term, allowing lubricant volumes to see gradual rather than abrupt change.

Which regions are emerging as new demand centers?

Economic zones in Sylhet-Chattogram, Mongla, and Payra are attracting logistics fleets that require premium heavy-duty lubricants, diversifying geographic demand beyond Dhaka.

Page last updated on: