Carbonyl Iron Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

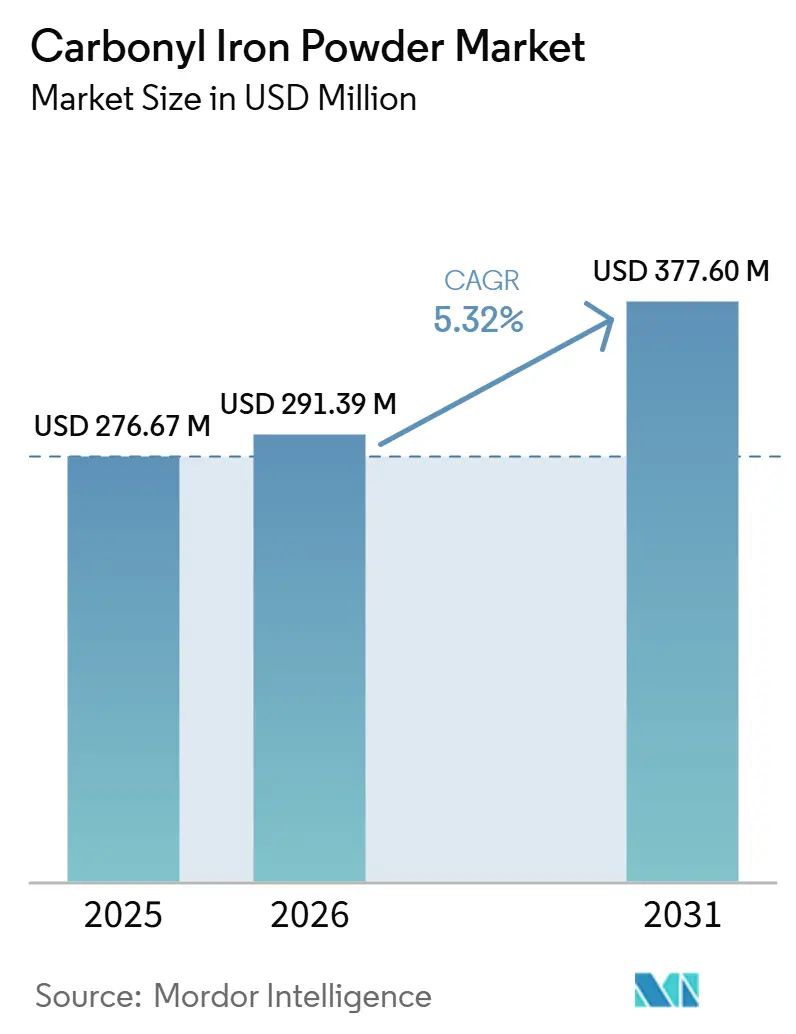

| Market Size (2026) | USD 291.39 Million |

| Market Size (2031) | USD 377.60 Million |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

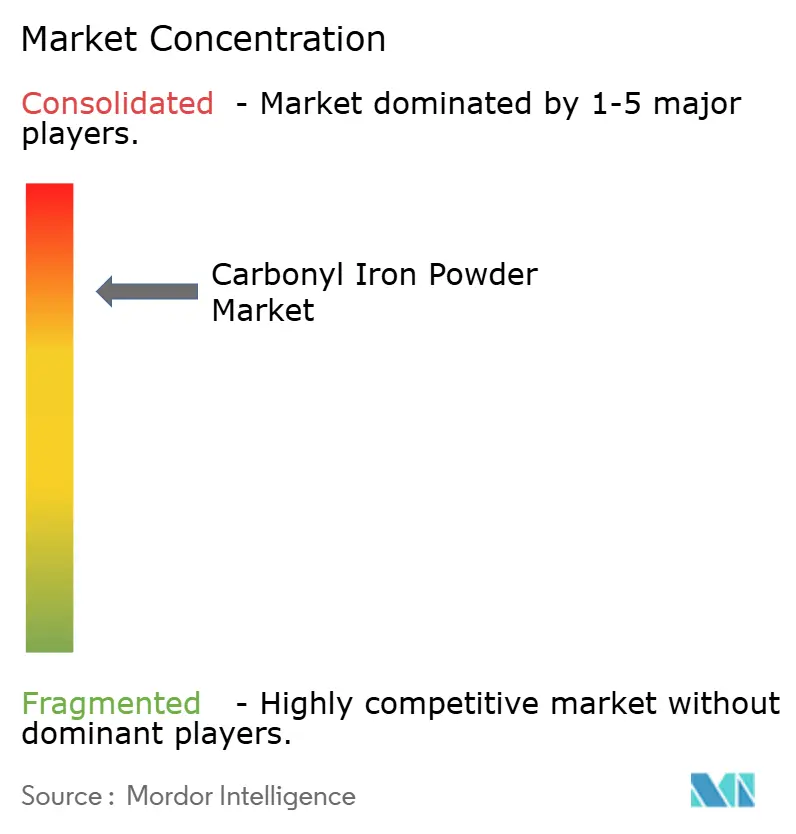

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbonyl Iron Powder Market Analysis by Mordor Intelligence

The Carbonyl Iron Powder Market size is projected to expand from USD 276.67 million in 2025 and USD 291.39 million in 2026 to USD 377.60 million by 2031, registering a CAGR of 5.32% between 2026 to 2031. As the automotive and medical sectors evolve, there's a pronounced shift in customer demand towards ultra-high-purity and surface-treated grades. These grades are pivotal for next-generation electric vehicle drivetrains and medical components produced through metal injection molding. Suppliers who can ensure oxygen levels stay below 0.2% and maintain particle-size tolerances within 0.5 microns stand to benefit significantly from these lucrative markets. Furthermore, automakers are increasingly favoring high-frequency soft magnetic composites, leading to a surge in demand for atomized variants. In the pharmaceutical realm, there's a notable shift towards micro-encapsulated carbonyl iron powder, lauded for its 2-4 times greater bioavailability compared to ferrous sulfate alternatives. On the regulatory front, Europe's Directive 2024/1785 is tightening the reins, leading to heightened compliance costs related to dust exposure and emissions. This regulatory pressure is catalyzing a wave of supplier consolidations and a strategic pivot of incremental capacity towards Asia-Pacific production hubs. In China, leading manufacturers are ramping up capacity by over 12,000 metric tons. While this surge is intensifying price competition in commodity structural parts, it hasn't yet encroached upon premium niches that demand ASTM and USP certification.

Key Report Takeaways

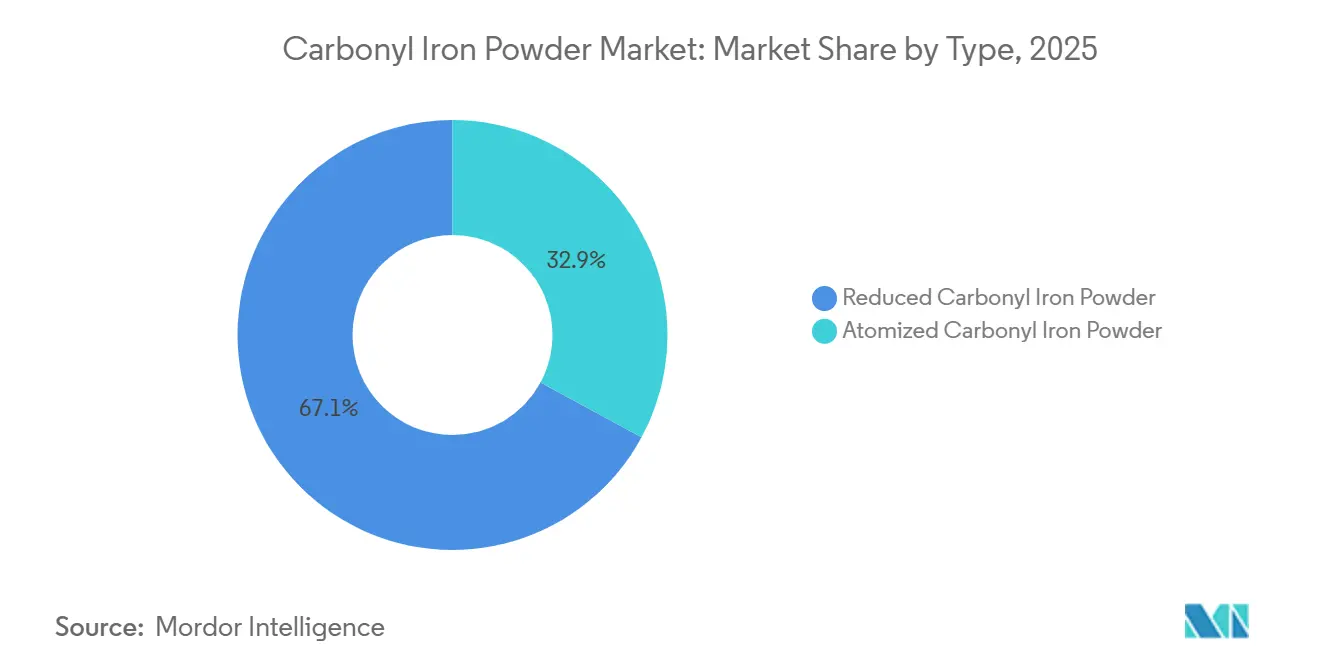

- By type, reduced grades accounted for 67.11% of the carbonyl iron powder market share in 2025. Atomized variants are projected to post the fastest 5.88% CAGR from 2026 to 2031.

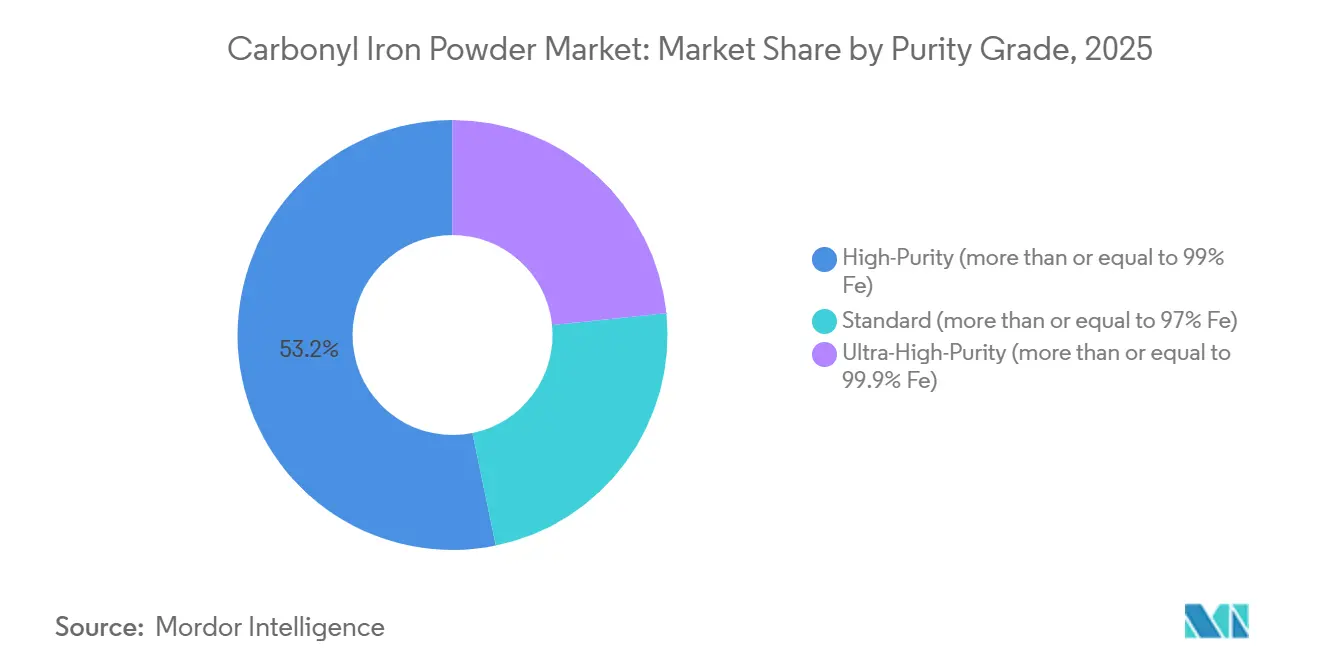

- By purity grade, high-purity material captured 53.22% share of the carbonyl iron powder market size in 2025. Ultra-high-purity grades are forecast to advance at a 5.92% CAGR from 2026 to 2031.

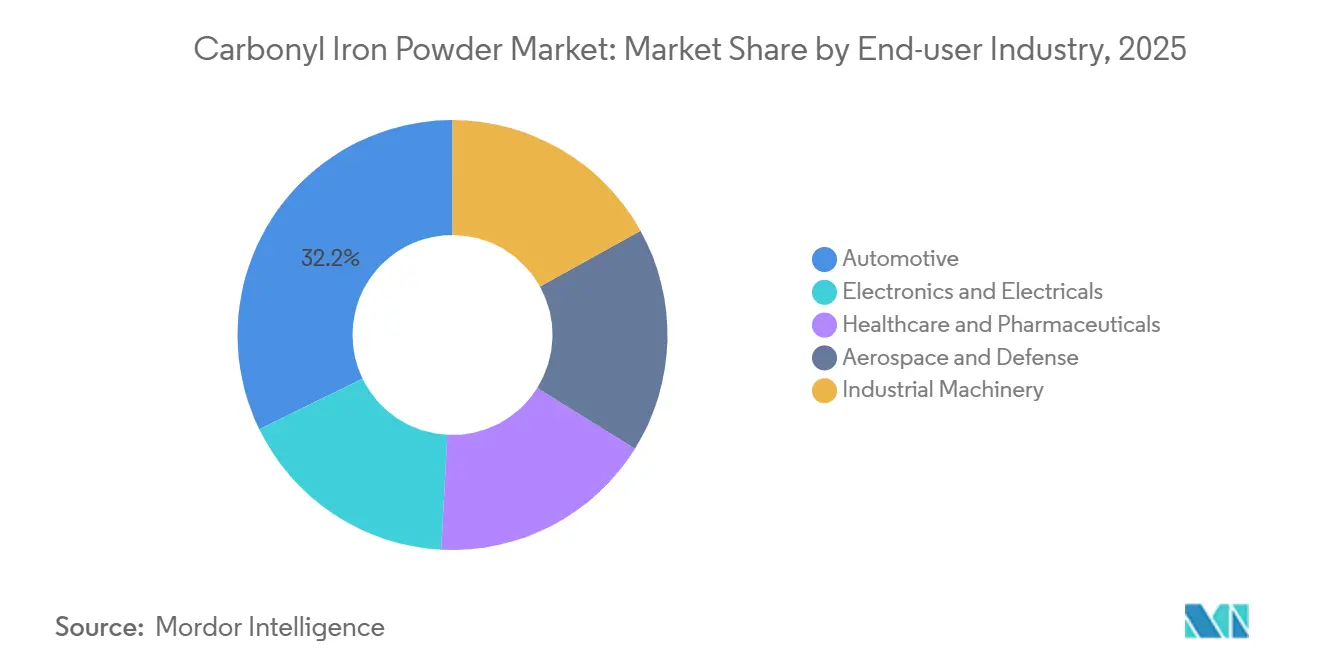

- By end-user, automotive led with 32.22% revenue share in 2025, whereas healthcare and pharmaceuticals is poised for a 6.04% CAGR from 2026 to 2031.

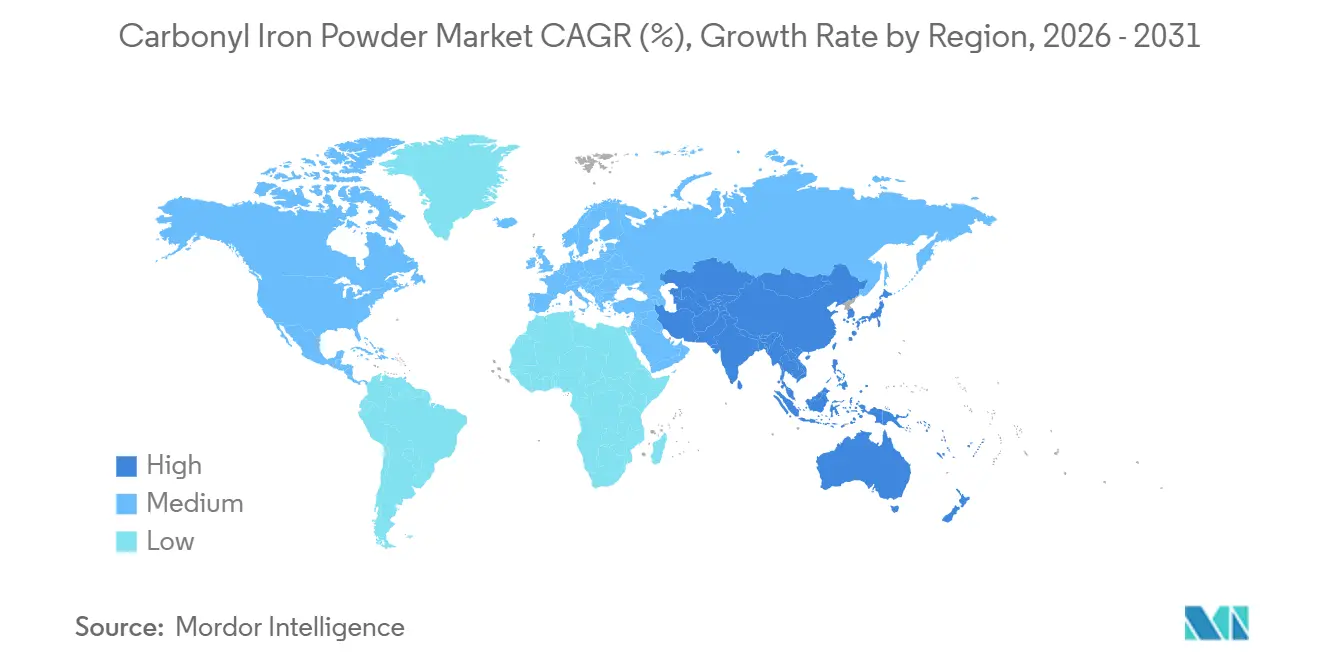

- By geography, Asia-Pacific dominated with 42.27% share in 2025 and is expected to grow at a 6.31% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carbonyl Iron Powder Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in powder-metallurgy use for lightweight electric vehicle drivetrain parts | +1.2% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Uptake of metal-injection molding (MIM) for miniaturized medical devices | +0.9% | Global, with early gains in North America, Europe, and Japan | Medium term (2-4 years) |

| Expansion of iron-fortified micro-encapsulated nutraceuticals | +0.7% | Asia-Pacific and Latin America, emerging in Africa | Long term (≥4 years) |

| Localized radar-absorbing composites for autonomous-vehicle sensors | +0.5% | North America, Europe, China | Long term (≥4 years) |

| Inductive-charging pad magnetics specification tightening | +0.4% | Global, led by Asia-Pacific automotive electronics hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surge in Powder-Metallurgy Use for Lightweight Electric Vehicle Drivetrain Parts

Electric-vehicle manufacturers are increasingly adopting powder-metallurgy components such as gears, cams, and brackets. These components help reduce drivetrain mass by 15% to 20% while maintaining fatigue strength above 500 MPa. This reduction contributes to an additional range of 15 to 20 km for every kilogram saved. A case study from Porite indicated a 20% to 30% cost reduction compared to machined steel. Similarly, Sterling Sintered Technologies reported that soft magnetic composites made with carbonyl iron powder reduced core losses by 20% and decreased motor sizes by 30%. The growing demand for lightweight and efficient components in electric vehicles is driving the adoption of powder-metallurgy solutions. Carbonyl iron powder is gaining attention in high-performance applications due to its spherical morphology and high sinterability[1]JHPIM Editorial Board, “Powder Metallurgy for EV Applications,” JHPIM, jhpim.com. Suppliers capable of customizing particle sizes within the 1 to 5 micron range and providing pre-insulated grades to minimize eddy-current losses are positioned to achieve higher pricing. On the other hand, producers without these capabilities may face pressure on margins as automakers leverage their purchasing volumes to negotiate lower prices.

Uptake of Metal-Injection Molding for Miniaturized Medical Devices

In 2024, the revenue from medical and dental metal-injection molding (MIM) ranged between USD 578 million and USD 1.88 billion, with a growth rate of nearly 9% CAGR. The preference for carbonyl iron powder is driven by its spherical particles, which enable a 60 vol% solids loading and achieve densities exceeding 95% of theoretical post-sintering. To meet USP and ASTM B883-10 standards, oxygen content is limited to 0.2%, which helps reduce porosity in body-fluid environments. Suppliers that fail to comply may face exclusion from high-margin contracts, as FDA 21 CFR 820 documentation requirements become stricter. Metal-injection molding, capable of achieving tolerances below 0.05 mm and surface finishes finer than 1.6 µm, is essential for manufacturing orthodontic brackets and implantable housings.

Expansion of Iron-Fortified Micro-Encapsulated Nutraceuticals

Encapsulated carbonyl iron powder improves iron absorption in fortified foods, achieving two to four times higher absorption rates compared to ferrous sulfate, while also addressing metallic off-flavors. A study published in Nature Food in 2024 reported that oat nanofiber hybrids achieved a 46.2% absorption rate, compared to 26.3% for ferrous sulfate. Additionally, a trial on medRxiv observed that serum-ferritin levels in participants increased over 12 weeks without causing gastrointestinal side effects. In the Asia-Pacific and Latin America regions, government-mandated fortification is driving the demand for pharmaceutical-grade material. This material complies with strict heavy-metal limits, including lead at < 3 ppm and arsenic at < 2 ppm. Suppliers leverage clean-room production and comprehensive REACH documentation to secure higher margins in the market.

Localized Radar-Absorbing Composites for Autonomous-Vehicle Sensors

Polymer compounds containing 30%–50% carbonyl iron powder achieve reflection losses below -20 dB across the 8–18 GHz spectrum. This performance complies with the CISPR 25 Class 5 electromagnetic compatibility standards. Priced between USD 8,500 and 11,000 per ton, these compounds provide a cost-efficient alternative to nickel-coated carbon fibers, which cost more than USD 15,000 per ton. BASF’s insulated grade, CIP HQ-I, with a resistivity of ≥ 1 × 10^7 Ω·m, expands the absorption bandwidth and addresses a near-term demand of 200-300 tons annually, generating over 40% in converter gross margins. As autonomous vehicles progress toward Level 3–4 production by 2027–2028, suppliers with ISO 11452-verified electromagnetic testing capabilities will meet the qualification requirements.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Occupational nanoparticle inhalation liabilities | -0.6% | Global, with stricter enforcement in Europe and North America | Medium term (2-4 years) |

| Substitution threat from cheaper water-atomized iron powders | -0.8% | Asia-Pacific and emerging markets | Short term (≤2 years) |

| European Union dust-exposure directive raising compliance costs | -0.4% | Europe, indirect impact on global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Occupational Nanoparticle Inhalation Liabilities

Regulators, despite a systematic review finding no consistent disease link, have capped workplace iron-oxide exposure at 10 mg m-3. They now require real-time dust monitoring and medical surveillance by July 2027[2]A. Lewinski, “Occupational Exposure to Nanoparticles,” PubMed Central, ncbi.nlm.nih.gov. Compliance upgrades, such as HEPA filtration, quarterly audits, and health tracking, increase costs by USD 50,000 to 150,000 annually per line. This rise in costs has prompted insurers to adjust premiums by 15% to 25%. While large integrated producers are managing these costs, smaller converters are experiencing financial pressure, which could lead to their exit from the market. This development is gradually driving the carbonyl iron powder market toward increased consolidation.

Substitution Threat from Cheaper Water-Atomized Iron Powders

Water-atomized iron powders, priced between USD 5,000 and 7,000 per ton, are approximately 30%–40% less expensive than their counterparts. This cost advantage makes them suitable for structural components requiring a 0.1 mm tolerance, where magnetic properties are less critical. These powders have an oxygen content of 0.4%–0.6%, while carbonyl grades contain ≤ 0.2%. As a result, water-atomized powders require an additional sintering heat of 50 °C–100 °C and consume 8%–12% more energy. Chinese suppliers are promoting a 70% water-atomized blend, achieving a 15%–20% cost reduction while maintaining acceptable flowability. This approach is impacting the price-sensitive markets of the Asia-Pacific. To address this, suppliers should focus on specialized niches, such as USP-compliant supplements and high-frequency inductors, where technical substitution is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Reduced Grades Anchor Volume While Atomized Variants Scale in High-Frequency Electronics

In 2025, reduced grades, pharmaceutical supplements and metal-injection-molding medical parts, requiring oxygen levels of ≤ 0.2% and particle sizes between 1–10 µm, accounted for 67.11% of the carbonyl iron powder market under the reduced grades segment. Production depends on reactors operating at ≥ 20 MPa for cycles exceeding 120 hours, achieving iron purity levels above 99.5%. These characteristics ensure adequate green strength and densification surpassing 95% of theoretical standards, meeting the needs of healthcare and nutraceutical applications with relatively stable price sensitivity.

Atomized carbonyl iron powder, produced in 8 MPa reactors over a span of 60 hours, is projected to grow at a 5.88% CAGR. This growth is driven by its tighter D50 distributions of 3–8 µm, which help reduce eddy-current losses in soft magnetic composites, particularly for 50–100 kHz inverter coils. The segment is supported by the increasing adoption of 800-V EV platforms and silicon-carbide inverters in Asia-Pacific's vehicle programs. Suppliers offering pre-insulated atomized grades are gaining traction in high-frequency inductors, where a 1% reduction in core loss results in a 0.5% decrease in charging time. Additionally, dual-line producers capable of both high-pressure reduced and mid-pressure atomized outputs are positioned to maintain margins while addressing the varied demands of the carbonyl iron powder market.

By Purity Grade: Ultra-High-Purity Captures Electronics and Aerospace Upside

Ultra-high-purity grades, targeting impurity ceilings of 0.1% oxygen and 0.05% nitrogen for applications like radar-absorbing structures and satellite inductors, are projected to grow at a 5.92% CAGR. In comparison, high-purity material (≥ 99% Fe), which currently accounts for 53.22% of shipments, may experience slower growth. BASF’s sub-1 µm product is advancing performance metrics, achieving saturation magnetization beyond 1 Tesla and relative permeability over 2,000, which are not achievable with water-atomized powders.

Standard-grade powder, priced between USD 8,500 and 11,000 per ton, continues to dominate in terms of volume for structural sintered parts. However, its value share in the carbonyl iron powder market is expected to decline. This trend is driven by increasing demand from electronics, aerospace, and medical sectors for suppliers certified to ASTM A811-15R22, offering ultra-low coercive fields. Chinese entrants provide high-purity material at a 20%–30% discount but face a 5%–10% rework rate due to batch variability. This issue reduces the apparent price advantage.

By End-User Industry: Pharmaceuticals Lead Growth While Automotive Retains Scale

In 2025, the automotive sector held a 32.22% share of the carbonyl iron powder market, supported by demand for sintered gears and soft magnetic composites. The healthcare and pharmaceutical sectors are expected to grow at a CAGR of 6.04% through 2031, driven by the increasing use of micro-encapsulated supplements, which provide absorption rates 2–4 times higher than ferrous sulfate. The electronics and electricals sector contributes to approximately 30% of the market demand, with insulated grades being utilized in high-frequency inductors and EMI shields.

The aerospace and defense sectors require ultra-high-purity powder certified to ISO 9001 and ASTM B783-24 standards, maintaining a price of USD 20,000 per ton. Industrial machinery continues to consume standard-grade powder but is facing competition from lower-cost water-atomized blends. Suppliers focusing on research and development in healthcare and electronics are likely to sustain profitability. However, those with significant exposure to commodity automotive structural parts may need to mitigate risks through forward contracts in the carbonyl iron powder market.

Geography Analysis

In 2025, Asia-Pacific represented 42.27% of the revenue, with a projected 6.31% CAGR through 2031. This growth is supported by China's significant role, holding over 45% of global capacity and a demand exceeding 8,000 tons in 2023. In the first quarter of 2025, Chinese producers announced 12,000 tons of new production lines to cater to customers in Southeast Asia and North America. India, dealing with a 20%–30% premium on landed costs, imported between 1,200 and 1,500 tons in 2025, indicating the need for regional distribution hubs.

In North America, the aerospace, defense, and pharmaceutical sectors drive demand, with a focus on ASTM and USP traceability. American Carbonyl's plant in Alabama plays a key role in the domestic supply. Additionally, Höganäs' biochar substitution initiative is expected to reduce CO₂ intensity by 15% by 2026, aligning with OEM Scope 3 targets. In Europe, BASF's site in Ludwigshafen increased capacity by 800 tons in 2023 and is now applying stricter classifications for sub-µm grades. However, Directive 2024/1785 is raising compliance costs, prompting smaller converters to consider consolidation or relocation.

South America and the Middle East & Africa remain fully dependent on imports, facing challenges with lead times of 8 to 12 weeks. Establishing bonded regional warehouses with 500 to 1,000 tons of stock and technical-service centers could enable price premiums of 10% to 15%. This approach is particularly relevant as multinational buyers implement supplier audits aligned with EU and U.S. standards.

Competitive Landscape

Top suppliers, including BASF SE, Höganäs AB, JFE Steel Corporation, CNPC Powder, and Jiangxi Yuean Advanced Materials, dominate the carbonyl iron powder market. BASF, with facilities in Germany, China, and South Korea, leads the market by offering pharmaceutical-grade, insulated, and sub-µm powders, priced up to USD 20,000 per ton. Höganäs markets low-carbon powders produced through biochar sintering, which reduces CO₂ emissions per ton by 15%. Chinese firms Jiangxi Yuean, Jiangsu Tianyi, and Jilin Zhuochuang compete on price by offering discounts of 20%-30% compared to Western benchmarks.

Competitive approaches vary among players. Established companies focus on application-specific innovations, such as pre-insulated, ultra-fine, and surface-functionalized grades, while also securing third-party certifications. In contrast, Chinese firms emphasize scaling commodity production and obtaining automotive qualification audits. Opportunities for growth include carbonyl-based soft-magnetic alloys and polymer-coated powders designed for radar absorption. Additionally, additive manufacturing specialists are working on developing gas-atomized carbonyl iron powder with sphericity exceeding 95%, which could enable its use in aerospace and medical implant applications.

Carbonyl Iron Powder Industry Leaders

BASF

CNPC Powder

Höganäs AB

JFE Steel Corporation

Jiangxi Yuean Superfine Metal Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: GKN Powder Metallurgy completed the acquisition of Dauch Family Enterprises' powder-metallurgy assets for an undisclosed sum, consolidating North American capacity for automotive structural parts and positioning the combined entity to capture incremental demand from electric-vehicle drivetrain components that require lightweight, high-strength sintered gears and cams. The transaction adds approximately 15,000 metric tons of annual pressing capacity and strengthens GKN's ability to negotiate volume discounts with carbonyl iron powder suppliers.

- April 2025: Höganäs is implementing a strategic biochar substitution project aimed at replacing 20% of the fossil coal used in its sponge iron production with renewable biochar by end of 2026.

Global Carbonyl Iron Powder Market Report Scope

Carbonyl iron powder is a highly pure, spherical microparticle powder produced via the chemical decomposition of iron pentacarbonyl. It features high reactivity and superior electromagnetic properties, making it essential for high-frequency magnetic cores, radar-absorbing materials, metal injection molding (MIM), and pharmaceutical iron supplements.

The market is segmented by type, purity grade, end-user industry, and geography. By type, the market is segmented into reduced carbonyl iron powder and atomized carbonyl iron powder. By purity grade, the market is segmented into standard (more than or equal to 97% Fe), high-purity (more than or equal to 99% Fe), and ultra-high-purity (more than or equal to 99.9% Fe). By end-user industry, the market is segmented into electronics and electricals, automotive, healthcare and pharmaceuticals, aerospace and defense, and industrial machinery. The report also covers the market size and forecasts for Carbonyl Iron Powder in 19 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Reduced Carbonyl Iron Powder |

| Atomized Carbonyl Iron Powder |

| Standard (more than or equal to 97% Fe) |

| High-Purity (more than or equal to 99% Fe) |

| Ultra-High-Purity (more than or equal to 99.9% Fe) |

| Electronics and Electricals |

| Automotive |

| Healthcare and Pharmaceuticals |

| Aerospace and Defense |

| Industrial Machinery |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Reduced Carbonyl Iron Powder | |

| Atomized Carbonyl Iron Powder | ||

| By Purity Grade | Standard (more than or equal to 97% Fe) | |

| High-Purity (more than or equal to 99% Fe) | ||

| Ultra-High-Purity (more than or equal to 99.9% Fe) | ||

| By End-user Industry | Electronics and Electricals | |

| Automotive | ||

| Healthcare and Pharmaceuticals | ||

| Aerospace and Defense | ||

| Industrial Machinery | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the carbonyl iron powder market by 2031?

The Carbonyl Iron Powder Market size was valued at USD 276.67 million in 2025 and is estimated to grow from USD 291.39 million in 2026 to reach USD 377.60 million by 2031, at a CAGR of 5.32% during the forecast period (2026-2031).

Which region will grow fastest in demand for carbonyl iron powder?

Asia-Pacific is expected to post the highest regional CAGR of 6.31% through 2031, supported by capacity expansion and rising EV and electronics output.

Which industry is set to record the strongest growth in carbonyl iron powder consumption?

Healthcare and pharmaceuticals will advance at 6.04% CAGR as micro-encapsulated supplements displace ferrous sulfate.

How are suppliers addressing environmental compliance in Europe?

Leading producers are installing HEPA filtration, emissions monitoring, and low-carbon sintering upgrades to meet Directive 2024/1785 requirements and avoid penalties up to 3% of EU turnover.

What competitive strategies are Western incumbents using against low-cost Asian entrants?

They focus on ultra-high-purity, insulated, and application-specific grades with ASTM and USP certification, plus sustainability credentials such as biochar-enabled CO₂ cuts.

Page last updated on: