Mining Explosives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.05 Billion |

| Market Size (2031) | USD 16.77 Billion |

| Growth Rate (2026 - 2031) | 3.60% CAGR |

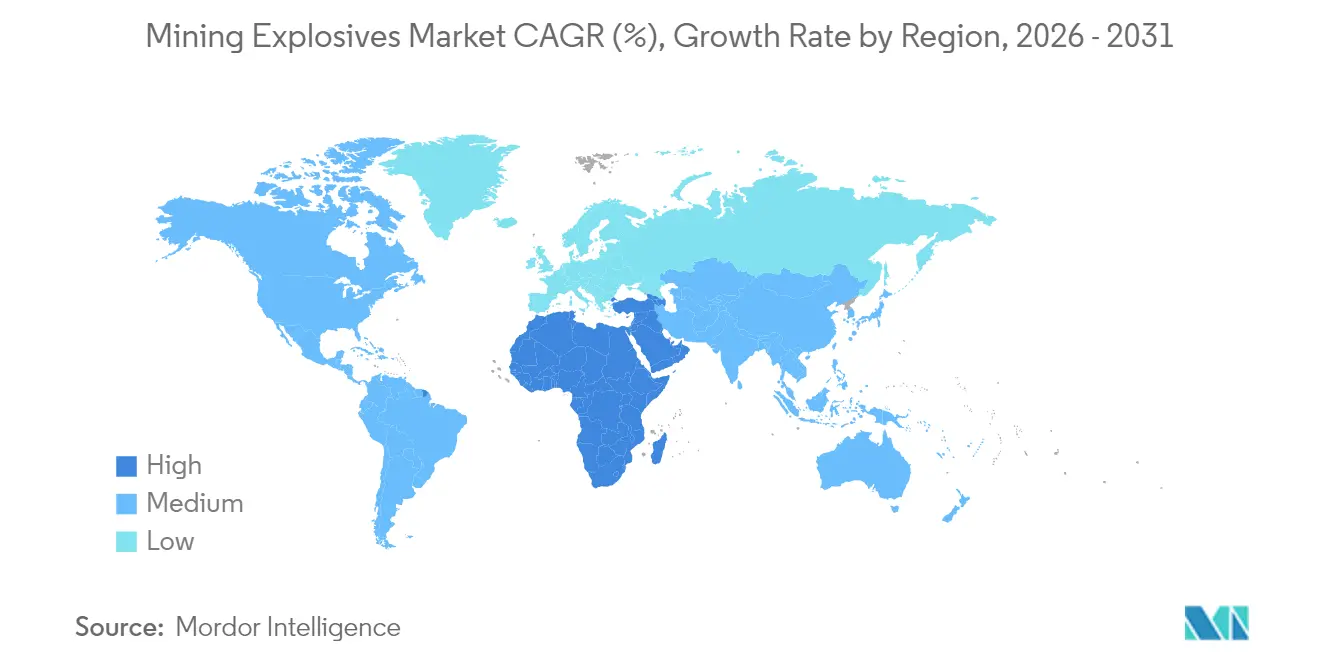

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

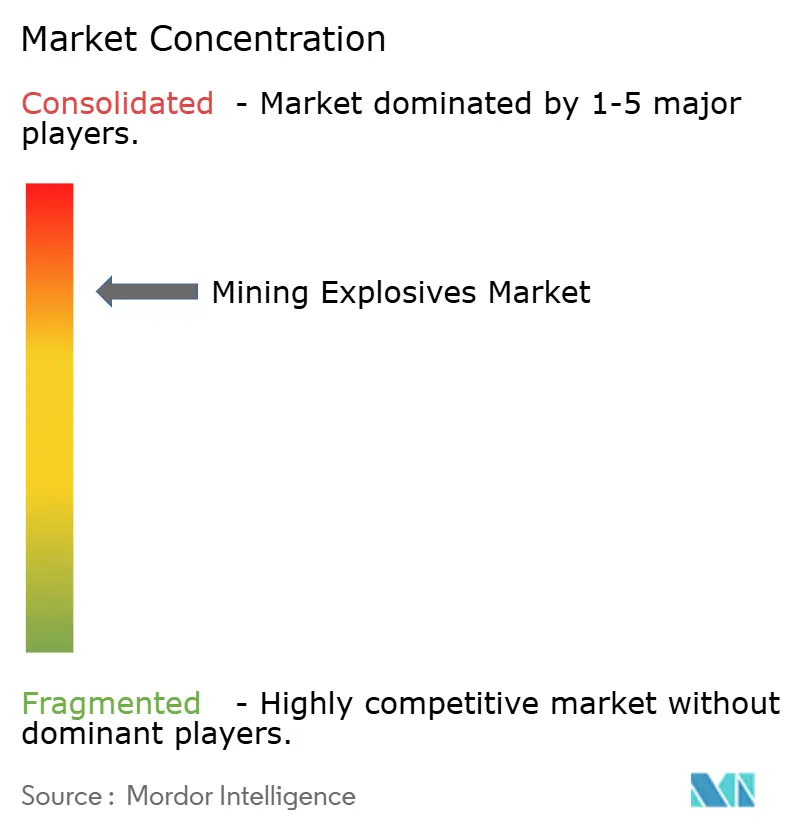

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mining Explosives Market Analysis by Mordor Intelligence

The Mining Explosives Market size was valued at USD 13.56 billion in 2025 and estimated to grow from USD 14.05 billion in 2026 to reach USD 16.77 billion by 2031, at a CAGR of 3.60% during the forecast period (2026-2031). Sustained demand for minerals that feed energy-transition technologies, infrastructure programs, and industrial manufacturing underpins the steady expansion, while operators focus on productivity gains through precision blasting and digital initiation systems. Increasing surface stripping ratios, deeper underground deposits, and stringent vibration norms are simultaneously reshaping product preferences toward bulk emulsions for volume efficiency and electronic detonators for timing accuracy. Asia-Pacific maintains dominance because of China’s coal production and India’s quarrying needs, whereas the Middle East and Africa posts the fastest acceleration, fueled by Saudi Arabia’s Vision 2030 mining push and African critical-mineral exploration. Competitive intensity centers on technology rather than price, with market leaders acquiring specialty chemical and digital capabilities to lock in customer contracts and offset regulatory cost pressures.

Key Report Takeaways

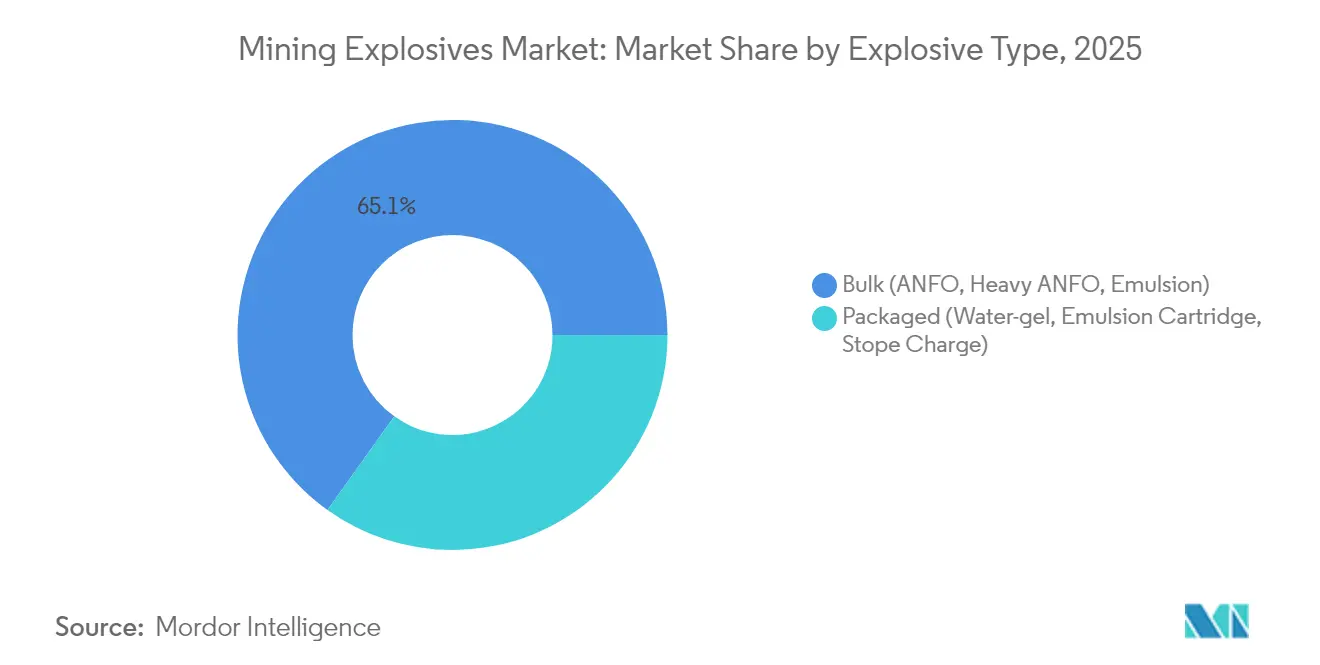

- By explosive type, bulk explosives commanded 65.12% of the mining explosives market share in 2025; while packaged explosives are forecast to advance at a 3.93% CAGR between 2026-2031.

- By initiation system, electronic detonators held 39.38% share of the initiation segment in 2025 and are projected to expand at a 4.28% CAGR through 2031.

- By application, coal mining accounted for 58.34% of the mining explosives market size in 2025, while quarry and construction aggregates are set to rise at a 4.06% CAGR to 2031.

- By geography, Asia-Pacific held 48.21% of global value in 2025, while the Middle East and Africa region is expected to grow at 3.99% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mining Explosives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Overburden-To-Ore Ratios Force Higher Blast Volumes | +0.8% | Global, particularly Australia and North America | Long term (≥ 4 years) |

| Shift From Cap-Sensitive to Electronic Detonators Cuts Misfires | +0.6% | Global, led by Europe and North America | Medium term (2-4 years) |

| Surge in Underground Metal Exploration in Africa | +0.4% | Sub-Saharan Africa, spill-over to Middle East | Medium term (2-4 years) |

| Automation of Loading Systems (Mobile Manufacturing Units) Gains Traction | +0.3% | North America and Australia | Long term (≥ 4 years) |

| Government Push for Domestic AN Production in India and Saudi Arabia | +0.2% | India and Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Overburden-To-Ore Ratios Force Higher Blast Volumes

Large surface mines are stripping more material per tonne of product than ever before. In some Australian coal pits, the ratio exceeds 15 m³ of overburden per tonne of coal versus 8-10 m³ two decades ago, driving up bulk explosive consumption and favoring ANFO and emulsions for cost-per-cubic-meter efficiency. Copper grades halved to 0.6% in key Latin American sites, compelling miners to enlarge blast patterns and deploy on-bench mobile manufacturing units to cut logistics costs. As operators extend pit perimeters, in-hole energy distribution becomes critical, encouraging adoption of bulk pumps that can meter density on demand. Digital fragmentation models further fine-tune powder factors, converting what was a volume game into a data-guided exercise that ultimately stabilizes costs even as tonnage rises.

Shift From Cap-Sensitive to Electronic Detonators Cuts Misfires

Programmable electronic detonators eliminate micro-second scatter common with pyrotechnic caps, slashing misfires, curbing fly-rock, and improving downstream mill throughput. Field trials with WebGen and DigiShot systems show crusher energy savings of 8-12% in the first year, often recouping device premiums inside 18 months[1]Dyno Nobel, “DigiShot Plus.4G Technical Bulletin,” dyno.com . Wireless initiation also removes surface lines, boosting personnel safety and allowing single-button firing from secure shelters. Regulators in the European Union prescribe vibration ceilings that electronic timing meets more predictably, accelerating conversion across quarries situated near towns. As fleets of autonomous drills proliferate, machine-readable blast files further anchor electronics as the default standard.

Surge in Underground Metal Exploration in Africa

Renewed drilling budgets in the Democratic Republic of Congo, Zambia, and South Africa are earmarked for copper, cobalt, and lithium seams essential to battery supply chains. Gulf investors committed more than USD 2 billion to joint projects in 2024, guaranteeing offtake contracts that give mines the capital to move quickly from exploration to production. Underground headings require high-brisance packaged emulsions with low fumes and rigid vibration envelopes because workings lie beneath surface communities. Precision timing with electronic detonators shortens mucking cycles, and suppliers that can combine product, detonator, and design software gain first-mover advantage in shafts now set to open before 2030.

Automation of Loading Systems (Mobile Manufacturing Units) Gains Traction

Mobile manufacturing units (MMUs) truck non-hazardous precursors, blend them into emulsions on site, and pump them directly into holes, cutting hazardous-goods trucking kilometers by as much as 60%. The safety upside persuaded Australian and Canadian regulators to streamline licensing, while insurers apply premium discounts when MMUs replace packaged stockpiles. Integration with robotic chargers such as the ABB-Boliden prototype pulls workers away from the face during loading, aligning with zero-exposure goals. Remote copper mines in the Andes and Pilbara iron ore pits record double-digit productivity lifts from coordinated drilling, on-trailer mixing, and autonomous stemming, shifting procurement criteria from price per ton to total-cycle value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ammonium-Nitrate Diversion Concerns Tighten Licensing | -0.4% | Global, particularly Australia and Europe | Short term (≤ 2 years) |

| Chronic Driver Shortages Restrict On-Bench Delivery Capacity in North America | -0.3% | North America | Medium term (2-4 years) |

| Stringent Vibration and Fly-Rock Limits Near Populated Zones in Europe | -0.2% | Europe, spreading to developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ammonium-Nitrate Diversion Concerns Tighten Licensing

Security-sensitive ammonium-nitrate rules now demand real-time tracking, staff background checks, and fortified storage, inflating compliance costs particularly for mid-tier miners. Australia’s national code and the European Union’s precursor regulation enforce transaction reporting thresholds that lengthen procurement cycles and push some buyers to swap ANFO for emulsion blends with lower porosity and reduced theft attractiveness. Smaller quarries often choose to outsource blasting altogether, accelerating consolidation toward vertically integrated service providers that can amortize compliance infrastructure across multiple sites.

Chronic Driver Shortages Restrict On-Bench Delivery Capacity in North America

North America’s aging hazmat driver pool shrank further in 2025 as retirements outpaced license renewals, leaving explosives distributors scrambling to cover remote routes. Federal Motor Carrier Safety Administration data show a vacancy ratio topping 80,000 seats for hazardous endorsements, raising delivered-cost premiums and forcing mines to stretch blast schedules or store higher inventories. Automated guided vehicles remain experimental, so suppliers are rerouting bulk loads via rail to regional hubs where scarce drivers cover shorter last-mile hauls, a workaround that still limits flexibility during production surges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Explosive Type: Bulk Dominance Faces Precision Challenge

Bulk explosive secured a 65.12% slice of 2025 revenue for bulk ANFO, heavy ANFO, and pumpable emulsions, the cornerstone products for high-tonnage coal and iron ore pits. Annual powder consumption in Indonesia’s surface operations passed 800 kt in 2025, underscoring the segment’s central role in meeting thermal-coal contractual deliveries. Emulsion trucks equipped with density-on-demand technology let engineers alter energy distribution down a single hole, optimizing cost without sacrificing heave where benches thicken.

Packaged variants captured the growth spotlight, booking a 3.93% CAGR outlook to 2031 as mines plunge deeper and environmental buffer zones narrow. Cartridge emulsions, water gels, and high-brisance stope charges command premiums because they excel in confined headings where fume toxicity, water resistance, and accurate column placement override sheer tonnage. High-energy sodium-borohydride formulations lifted brisance to 26.3 mm in lab tests, giving underground operators fresh latitude to shorten drill cycles while still keeping particulate thresholds within air-quality permits. This quality-driven dynamic redraws procurement playbooks: total-cost-of-ownership models now weigh mucking throughput, scaling, and crusher kWh per tonne, pushing packaged suppliers into consultative roles.

By Initiation System: Electronic Revolution Transforms Timing Precision

A 39.38% market share in 2025 put electronic detonators at the forefront of the initiation hierarchy and they are set to climb fastest at 4.28% CAGR. Wireless variants negate down-lines, boosting safety in block caves and open-stope headings where loose ground poses entanglement risks. Integrated diagnostic feedback flags faulty caps before firing, curbing re-entry delays and cementing the business case despite unit prices up to 9 times higher than NONEL.

NONEL tube systems remain indispensable for contract blasters operating short-term civil quarries and pipeline corridors where simplicity offsets the absence of precision. Conventional electric fuse and det-cord still thrive in small-charge secondary breakage because they are unaffected by radio-frequency interference from adjacent machinery. Yet once mines adopt asset-level digital twins, only electronics feed the data loops required to align fragmentation with haul-truck axle loads and SAG-mill energy curves, ensuring their runway to 2030 and beyond.

By Application: Coal Mining Leadership Faces Infrastructure Competition

Coal mining retained 58.34% value contribution in 2025 as thermal plants in China, India, and Southeast Asia anchored baseload grids that renewables cannot yet fully displace. Surface mines in Shanxi and Odisha alone detonated more than 90 million boreholes in 2025, cementing the segment’s pull on global ANFO capacity. Even with decarbonization pledges, metallurgical coal for steel persists, cushioning demand through 2030.

Metal mining upholds steady consumption courtesy of copper, lithium, nickel, and rare-earth ambitions. Chilean porphyry expansions, Zambian copperbelt turnarounds, and Finnish battery-chemicals hubs favor emulsion blends capable of managing variable ore hardness. Meanwhile quarry and construction aggregates climbed quickest at 4.06% CAGR as governments green-lit road, rail, and port schemes. The United States’ USD 1.2 trillion Infrastructure Investment and Jobs Act funneled funds to 56,000 asset-rehab projects, escalating quarry run-rates for crushed stone and dimension granite. Urban adjacency keeps vibration caps low, effectively steering contractors toward electronic blasts and micro-dosing water-gel cartridges.

Geography Analysis

Asia-Pacific’s 48.21% stronghold originates in China’s dig-and-load coal regime and India’s constant quarrying for highways, metros, and industrial corridors. Beijing’s five-year plan budgets emphasize domestic security of supply, stimulating placement of advanced bulk-emulsion plants close to Shanxi and Inner Mongolia pits. In India, Deepak Fertilisers’ 376 KTPA Gopalpur TAN buildout, slated for commissioning in 2026, aims to displace imports and supports local sourcing mandates that cut landed costs by up to USD 85 per tonne. Combined, these moves lock a self-reinforcing cycle where explosive demand and precursor availability rise in tandem.

North America and Europe contribute mid-teen percentages, yet they epitomize the technology vanguard. Stringent Occupational Safety and Health Administration and EU-REACH directives force suppliers to innovate low-fume emulsions and zero-plastic detonator components. Canada’s open-pit copper expansions in British Columbia apply in-house fragmentation sensors to reconcile mill feed uniformity with greenhouse-gas abatement targets. In the European Union, miners juggle supply resilience against the bloc’s Green Deal, prompting joint ventures that co-locate clean ammonium-nitrate capacity next to renewable-powered hydrogen facilities.

The Middle East and Africa stages the fastest ascent at 3.99% CAGR. Saudi Arabia’s Vision 2030 schedules USD 75 billion in mining GDP add-ons, highlighting phosphate and gold fields that will consume cartridges unsuited to conventional ANFO because of hot ground conditions. United Arab Emirates sovereign funds staked over USD 2 billion in African copper and lithium stakes during 2024, guaranteeing offtakes that funnel explosive technology transfer into jurisdictions such as the DRC and Namibia. Improved governance under the Africa Mining Vision plus highway upgrades around Dar es Salaam port unlock logistical corridors that favor bulk emulsion iso-tanks over bagged prills.

Competitive Landscape

The mining explosives market posts a high consolidation, with the top five firms controlling over 60% of 2024 revenue. Orica, MAXAM, Dyno Nobel, and Enaex leverage global manufacturing footprints and integrated digital offerings to differentiate beyond price. Orica’s USD 640 million Cyanco buyout expanded its sodium-cyanide vertical, letting the group pitch end-to-end drill-blast-leach packages that embed its WebGen detonators[2]Orica, “Acquisition of Cyanco Completed,” orica.com . MAXAM pumped USD 50 million into Chilean capacity, tripling its domestic share from 10% to 30% and illustrating how focused regional depth can upset incumbents. Dyno Nobel’s tertiary abatement retrofit promises a 30% greenhouse-gas reduction, a vital selling point in jurisdictions assigning carbon fees.

Smaller regionals such as Solar Industries India seized domestic supply opportunities, recording 38% revenue growth to INR 19.8 billion in FY 25 on the back of Coal India tenders. Similarly, Forcit’s Finnish TNT plant rebuild revives European defense munition supply, but the added cast-booster throughput cross-subsidizes its mining segment. The ecosystem’s digital arms race ushers software-hardware bundles where value pools migrate from tonnes sold to rock-mass-knowledge services.

Mining Explosives Industry Leaders

Orica Limited

Dyno Nobel

MAXAM

Enaex

Omnia Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: BME, a division of Omnia Group, introduced Innovex 300D, a bulk emulsion mining explosive for surface mining environments affected by dynamic water. The product helps mining operations address operational and environmental challenges caused by excessive water flow around blast holes.

- October 2023: Omnia group, collaborating with Hypex Bio Explosives Technology, introduced a nitrate-free emulsion mining explosive. The hydrogen peroxide-based explosive aims to reduce environmental impact compared to traditional explosives in mining operations.

Global Mining Explosives Market Report Scope

| Bulk (ANFO, Heavy ANFO, Emulsion) |

| Packaged (Water-gel, Emulsion Cartridge, Stope Charge) |

| Non-electric (NONEL) |

| Electronic Detonators |

| Electric Fuse and Det-Cord |

| Coal Mining |

| Metal Mining |

| Quarry and Construction Aggregates |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Explosive Type | Bulk (ANFO, Heavy ANFO, Emulsion) | |

| Packaged (Water-gel, Emulsion Cartridge, Stope Charge) | ||

| By Initiation System | Non-electric (NONEL) | |

| Electronic Detonators | ||

| Electric Fuse and Det-Cord | ||

| By Application | Coal Mining | |

| Metal Mining | ||

| Quarry and Construction Aggregates | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global value for Mining Explosives Market in 2031?

Forecasts peg worldwide sales at USD 16.77 billion by 2031, up from USD 14.05 billion in 2026.

Which explosive type currently accounts for the largest share of demand?

Bulk products such as ANFO and pumpable emulsions hold roughly 65.12% of 2025 spending thanks to their cost efficiency in high-volume surface operations.

Why are electronic detonators increasingly preferred over traditional caps?

Programmable timing improves fragmentation, cuts misfires, and helps mines meet tighter vibration limits, delivering payback within 18 months for many sites.

Which geographic region is set to record the fastest growth through 2031?

Middle East and Africa is projected to expand at about 3.99% CAGR, driven by Saudi Arabia’s Vision 2030 plans and growing African critical-mineral projects.

Page last updated on: