Powder Metallurgy Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

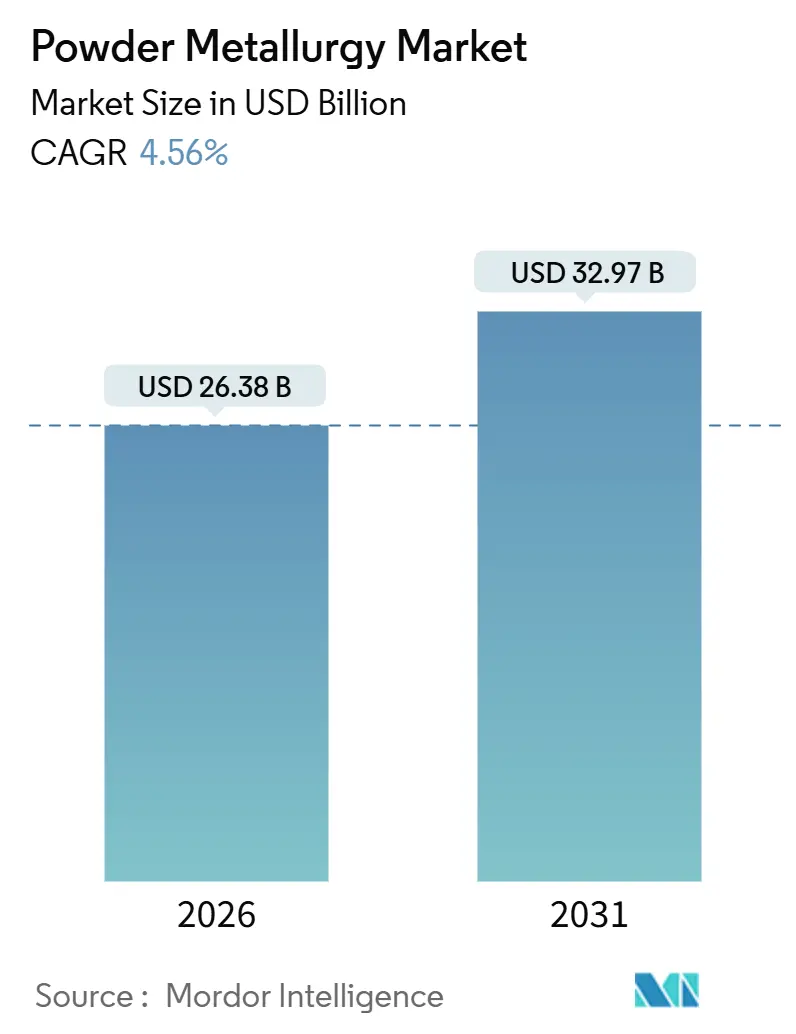

| Market Size (2026) | USD 26.38 Billion |

| Market Size (2031) | USD 32.97 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

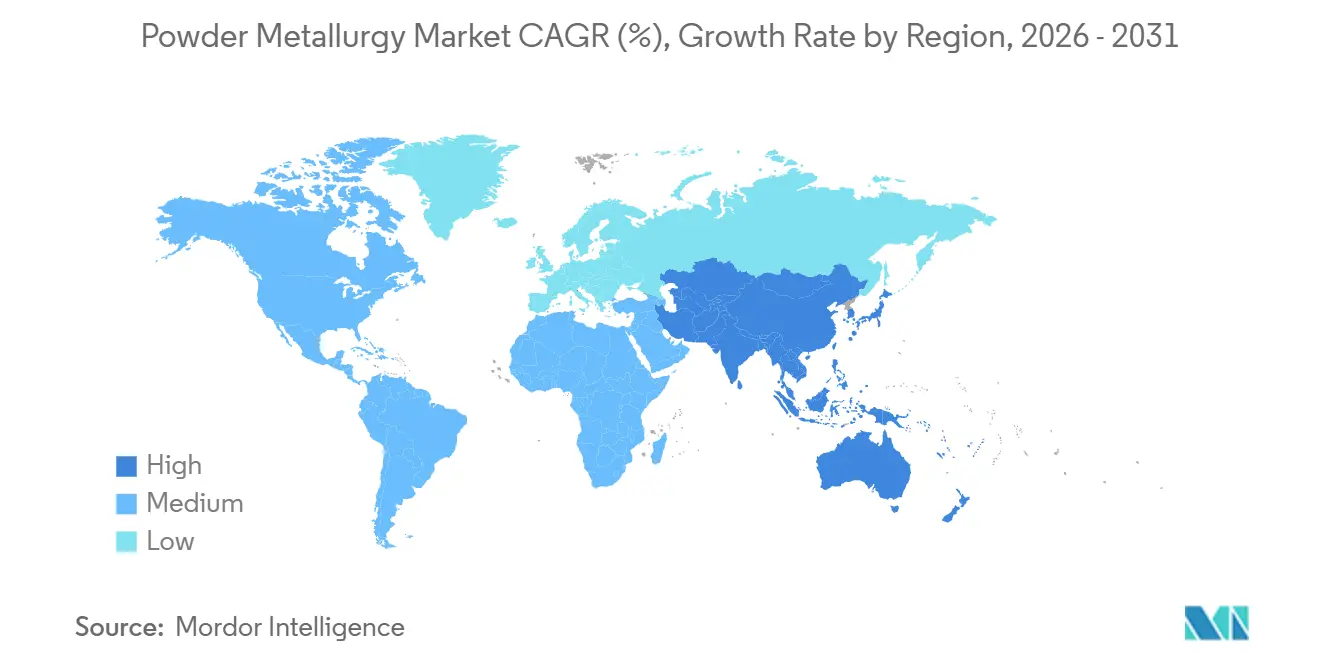

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

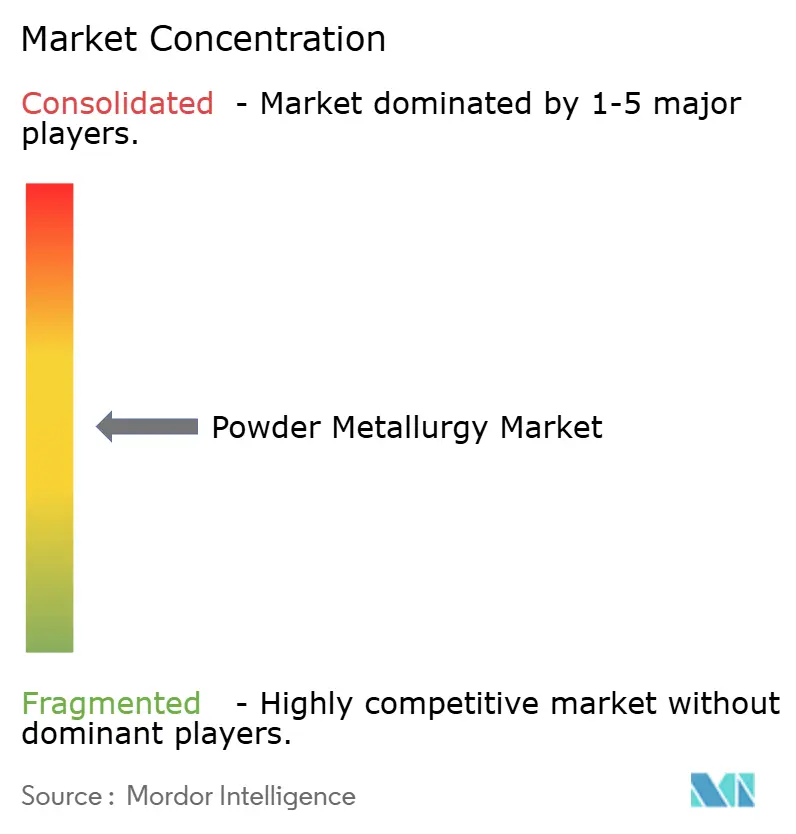

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Powder Metallurgy Market Analysis by Mordor Intelligence

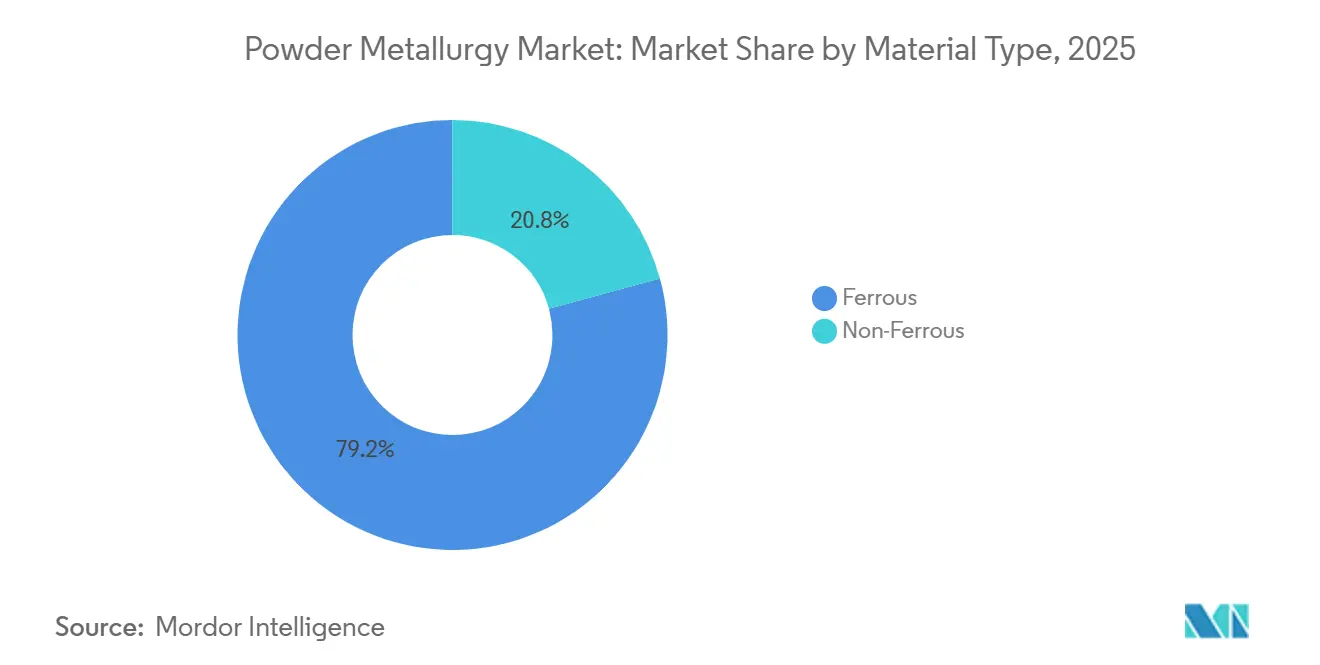

The Powder Metallurgy Market size is estimated at USD 26.38 billion in 2026, and is expected to reach USD 32.97 billion by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). Heightened electrification of drivetrains is repositioning powder metallurgy from a cost-reduction technique to a pathway for net-shape complexity, especially where ferrous soft-magnetic composites support high-frequency motors that stamping cannot match. In 2025, ferrous powders accounted for 79.24% of shipments because precision gears and bearings demanded dimensional tolerances tighter than die-cast alternatives. Additive manufacturing’s powder bed fusion is shifting from prototypes to serial aerospace brackets as primes chase 95% material utilization and lower buy-to-fly ratios. Regionally, Asia-Pacific led with 40.44% revenue in 2025, helped by China’s 1.4 million-ton powder output and Indian medical-implant localization incentives.

Key Report Takeaways

- By material type, ferrous captured 79.24% of powder metallurgy market share in 2025 and is projected to grow at a 4.66% CAGR through 2031.

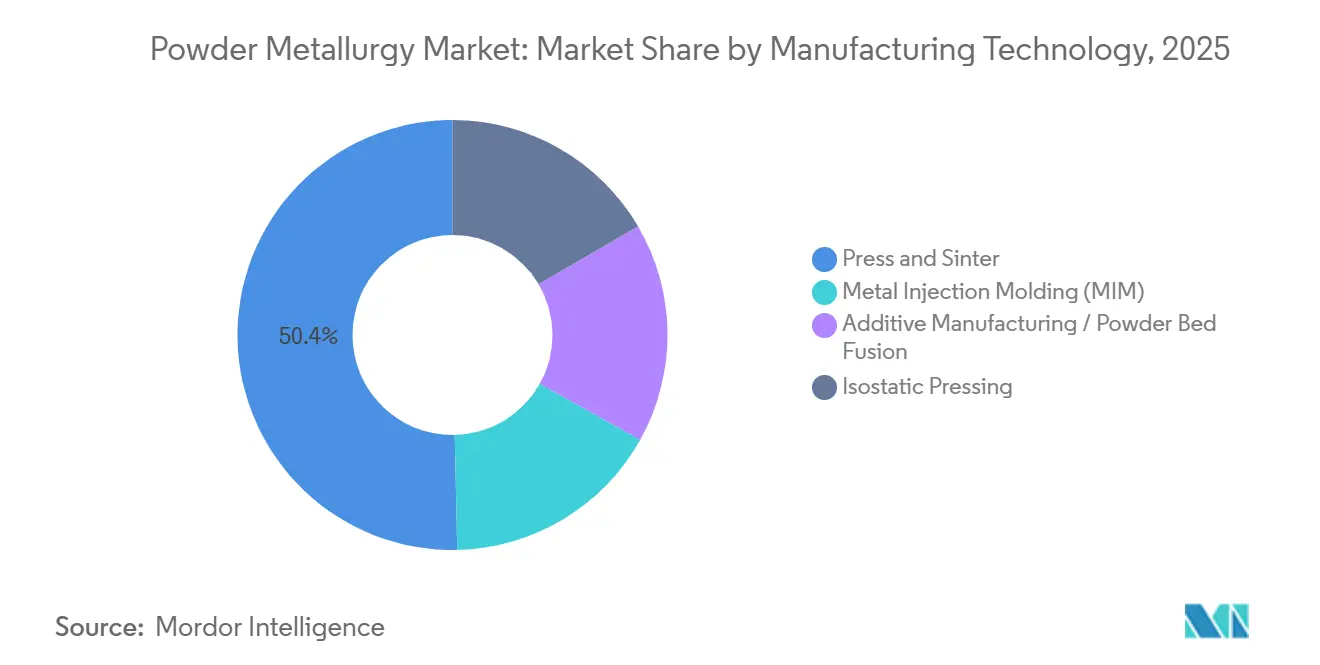

- By manufacturing technology, press and sinter held 50.35% of powder metallurgy market size in 2025, while additive manufacturing is advancing at a 4.91% CAGR to 2031.

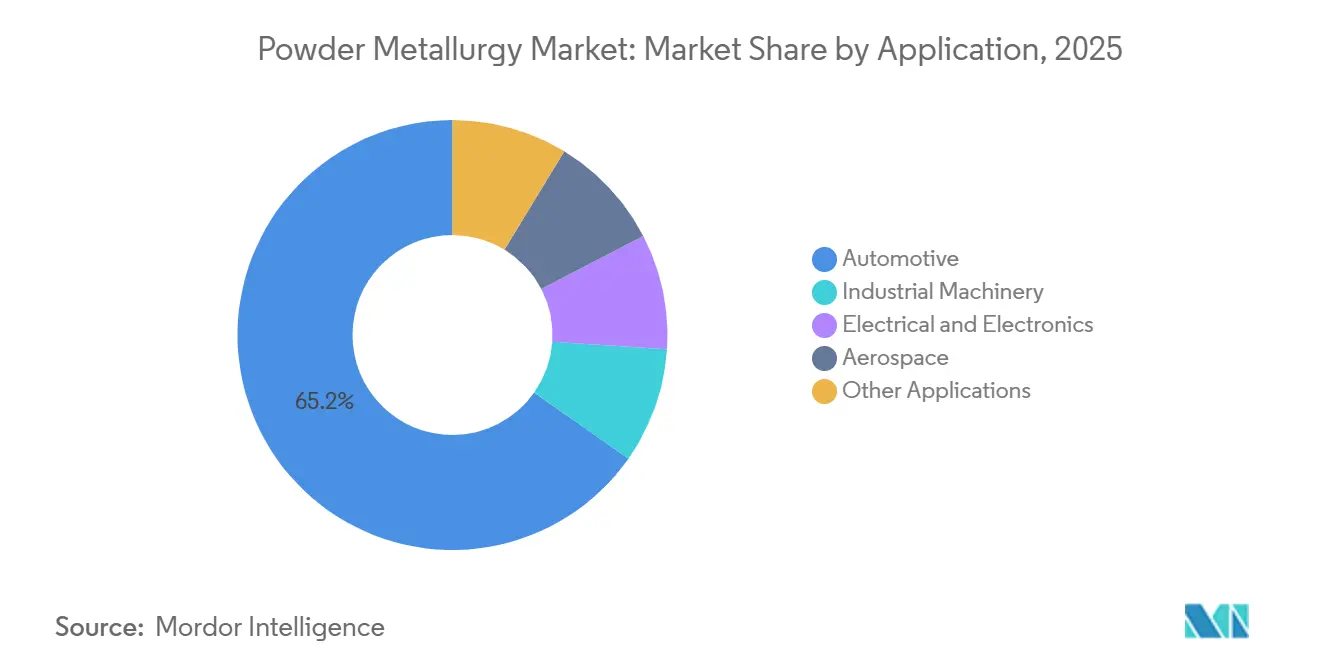

- By application, automotive led with 65.26% revenue share in 2025; industrial machinery is expanding at a 4.83% CAGR to 2031.

- By geography, Asia-Pacific commanded 40.44% of powder metallurgy market size in 2025 and the region is forecast to log the fastest 4.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Powder Metallurgy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Preference for PM in Lightweight E-Powertrain Components in North America | +0.8% | North America, with spillover to EU and China | Medium term (2-4 years) |

| Surge in Demand for Net-Shape Additive Metal Components Across Europe | +0.7% | Europe core, expanding to North America aerospace hubs | Long term (≥4 years) |

| Localization of Precision Medical-Implant Manufacturing in Asia-Pacific | +0.6% | APAC core (India, China, ASEAN), early adoption in Middle East | Medium term (2-4 years) |

| Defense Modernization Boosting Refractory Metal Powders in Middle East | +0.5% | Middle East and North Africa, U.S. defense supply chain | Long term (≥4 years) |

| Carbon-Border Adjustment Mechanism Reshaping EU Ferrous Powder Trade | +0.4% | European Union, indirect impact on Turkey and North Africa exporters | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Preference for PM in Lightweight E-Powertrain Components In North America

Electric-vehicle programs in the United States elevated powder metallurgy because soft-magnetic composites achieve relative permeabilities above 500 at 10 kHz, allowing motor-stator cores to shrink 15-20% without torque loss. General Motors and Ford locked multi-year agreements totaling 120,000 tons annually with domestic sintering suppliers for Ultium and BlueCruise platforms in 2024. These contracts favor North American atomization capacity that complies with the Inflation Reduction Act content rules[1]U.S. Department of Energy, “IRA Domestic Content Guidance,” energy.gov . Component life targets of 200,000 km require dimensional stability within ±0.02 mm at 180 °C, conditions that die-cast aluminum cannot meet.

Surge in Demand for Net-Shape Additive Metal Components Across Europe

Powder bed fusion reached serial production when Airbus integrated 14 titanium brackets per A320neo in 2025, trimming 180 kg from each airframe. Material-buy efficiency rose from 15% to 95%, saving machining scrap and cycle time. Suppliers such as Sandvik and GKN invested USD 455 million between 2024-25 to expand gas-atomization lines that deliver 15-45 µm spherical powders. EASA Part 21 and NADCAP changes cut certification loops from 48 to 28 months, accelerating design freezes.

Localization of Precision Medical-Implant Manufacturing in Asia-Pacific

India’s production-linked incentives worth INR 34 billion spurred four new metal-injection-molding lines that now output 2.8 million implant parts annually. Domestic cobalt-chrome hip stems retail at USD 320 versus USD 890 for imports, widening cost competitiveness. China’s regulator cleared 18 new porous-titanium spinal designs in 2024, each with 40-60% engineered porosity for osseointegration. Regional firms secured ISO 13485 certification, enabling export to Middle East buyers seeking competitive pricing.

Defense Modernization Boosting Refractory Metal Powders In Middle East

Middle Eastern defense budgets reached USD 186 billion in 2024, directing new funds toward domestically assembled penetrators and rocket nozzles that rely on tungsten and molybdenum powders. Saudi Arabia partnered with Plansee to build a 1,200-ton refractory-powder plant, aiming for 2027 output. The UAE awarded a USD 240 million contract to EDGE Group to localize molybdenum inserts, halving lead times. The U.S. AUKUS initiative added USD 3.3 billion for allied submarine components, amplifying demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile High-Purity Powder Prices Amid Critical-Mineral Supply Risk | -0.6% | Global, acute in non-ferrous segments (aerospace, medical) | Short term (≤2 years) |

| Limited Aerospace Part Qualification Standards | -0.4% | North America and Europe aerospace hubs | Medium term (2-4 years) |

| Competitive Threat from Advanced Casting of Complex Al Components | -0.5% | Global automotive, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile High-Purity Powder Prices Amid Critical-Mineral Supply Risk

London Metal Exchange nickel prices swung 33% between January 2024 and December 2025, raising feedstock costs that fixed-price contracts cannot absorb. Indonesia’s ore export ban compelled atomizers to pivot to higher-cost Canadian and Australian supply, adding USD 2,100–2,800 per ton to nickel powder[2]International Energy Agency, “Critical Minerals Outlook 2024,” iea.org . Cobalt remains 60% sourced from the DRC, where governance challenges complicate conflict-minerals audits for aerospace primes. Titanium sponge shortages amplified by Chinese power curbs delayed new powder qualifications by up to nine months.

Limited Aerospace Part Qualification Standards

FAA Advisory Circular 20-62E obliges powder bed fusion parts to meet 15 mechanical criteria with Cpk more than 1.67, demanding runs of at least 500 parts before approval. EASA adds traceability to melt batches and destructive witness testing, costing USD 195,000-270,000 per part number. Airbus and Boeing maintain separate qualified-powder lists, and cross-platform transfer can take 24-36 months. Suppliers therefore face duplicated quality systems across ASTM F3001, AMS 4999, and ISO/ASTM 52904 standards. These factors shave 0.4 percentage points off the medium-term growth slope.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Ferrous Dominance Anchors Volume Growth

Ferrous accounted for 79.24% of powder metallurgy market share in 2025 and is forecast to compound at a 4.66% rate to 2031, underscoring the material’s volume leverage in automotive drivetrain gears, synchronizer hubs, and bearings. Relative affordability-USD 1.80-2.40 per kg versus USD 8.50-12.00 for titanium-sustains ferrous leadership even as electrification trims total engine content. The segment is pivoting toward soft-magnetic composites that achieve 1.8 Tesla flux density at 20 kHz, a level conventional laminations cannot reach without eddy-current penalties. Suppliers such as Höganäs launched phosphorus-coated Somaloy 3P in 2024, cutting core losses 18% and earning three European EV-motor design wins for the 2027 model year.

Non-ferrous grades held 20.76% of powder metallurgy market share in 2025 as titanium, aluminum, and nickel-superalloy powders reach serial production in aerospace, medical, and energy storage programs. Recycled feedstocks soften raw-material volatility: Kymera’s RecycTi powder, approved by the FAA in 2024, offers 30% cost savings and now represents 12% of the firm’s titanium shipments. Application-specific alloying is widening the performance envelope, with ferrous suppliers adding silicon and aluminum for magnetics, while non-ferrous counterparts blend reclaimed chips to hedge commodity risk. The shift underscores a strategic divide: high-volume ferrous segments compete on cents per part, whereas low-volume titanium and nickel niches compete on certification speed.

By Manufacturing Technology: Additive Manufacturing Disrupts Qualification Timelines

Press and sinter retained 50.35% of powder metallurgy market size in 2025, thanks to 12-second cycle times and per-part costs below USD 0.85 for synchronizer hubs. Investment in servo-electric presses with closed-loop density control is keeping the process relevant for precision e-axle gears by holding sintered density within ±0.08 g/cm³. Metal injection molding is bridging geometry and volume gaps in smartphone camera modules and surgical instruments where tooling costs can amortize over millions of units.

Additive manufacturing/powder bed fusion is climbing at 4.91% CAGR as certification loops shorten. Sandvik’s Osprey division shipped 1,840 tons of titanium and nickel powder in 2025, a 28% rise fueled by 63 new NADCAP-qualified aerospace part numbers. Hot-isostatic pressing is increasingly paired with additive builds, driving residual porosity below 0.1% and meeting AMS fatigue thresholds without over-engineering wall thicknesses. The technology spectrum is now bifurcated by volume and complexity: press-and-sinter remains the cost benchmark, whereas additive routes monetize design freedom and material efficiency.

By Application: Industrial Machinery Gains as Automation Intensifies

Automotive consumed 65.26% of shipments in 2025, reflecting 18-22 kg of sintered parts per internal-combustion vehicle and 12-15 kg per battery-electric model. Despite electrification, drivetrain gears, rotors, and structural brackets keep automotive at the top of the powder metallurgy market. Yet industrial machinery is ascending with a 4.83% CAGR to 2031 as cap-ex on automation rises. Sintered bronze bushings featuring 15-25% engineered porosity enable self-lubrication and quadruple maintenance intervals in robotic joints.

Electrical and electronics is growing as data-center inductors and wireless-charging coils demand soft-magnetic composites that minimize eddy-current loss. Aerospace is growing on the back of titanium and nickel brackets produced through powder bed fusion with buy-to-fly ratios below 1.2:1. The application mix signals a gradual shift from commodity to mission-critical volumes, supporting price resilience even as automotive volumes normalize.

Geography Analysis

Asia-Pacific contributed 40.44% of global revenue in 2025, anchored by China’s 1.4 million-ton annual production capacity and India’s policy-driven medical-device localization. Chinese producer CNPC Powder operates eight water-atomization plants supplying domestic OEMs at prices 20-25% below European averages. Japan is exporting precision gears and soft-magnetic composites across Southeast Asia through Sumitomo Electric and Resonac distribution networks. India’s incentives triggered six new MIM plants between 2024-25, and ASEAN nations such as Thailand secured USD 87 million in FDI for sintered-component factories.

North America’s reshoring and e-axle investments are accelerating. GKN’s USD 1.44 billion buyout of American Axle’s facilities added 78,000 tons of capacity across Michigan and North Carolina, locking in contracts for Ultium gears. Phoenix Sintered Metals deployed a USD 42 million warm-compaction line in Tennessee in 2024 to meet domestic connecting-rod demand.

Europe is advancing as Germany, the United Kingdom, and France prioritize additive manufacturing for aerospace. Sandvik’s Neath expansion raised titanium and nickel-powder output by 40%, underpinning Airbus and Rolls-Royce programs. South America's share is driven by Brazil’s flex-fuel engines that still rely on sintered gears. The Middle East and Africa’s growth is supported by Saudi defense contracts and South African mining-equipment refurbishment.

Competitive Landscape

The top five suppliers—GKN Powder Metallurgy, Höganäs, Sumitomo Electric, ATI, and AMETEK—collectively control close to 50% of global shipments, underscoring moderate market concentration. GKN’s vertical integration through the American Axle acquisition positions the firm at the center of e-axle supply chains for Detroit-based OEMs. Höganäs differentiates on sustainability, sourcing 56% of its 500,000-ton capacity from recycled scrap and reporting carbon intensity below 1.2 tons CO₂ per ton, which qualifies for favorable EU CBAM treatment.

Technology segmentation is fragmenting competitive arenas. Press-and-sinter incumbents compete on cents-per-part efficiency, additive-manufacturing entrants on geometry freedom, and MIM specialists on high-detail features within medium volumes. Elementum and Metalysis exploit reactive-metal niches with aluminum-scandium and tantalum powders tailored for defense and energy storage, shortening FAA qualification cycles through digital-twin simulation. Sandvik filed 18 melt-pool-monitoring patents between 2024-25, aiming for closed-loop laser control that maintains porosity under 0.5% across variable chemistries.

Capacity for aerospace and medical standards expanded as ISO 13485 and NADCAP accredited plants grew from 127 in 2023 to 156 in 2025, reflecting mid-tier entrants moving beyond automotive. White-space opportunities are emerging in hybrid workflows where near-net additive preforms are finish-machined to ±0.01 mm, halving lead times for low-volume turbine components. Competitive intensity is therefore guided less by sheer tonnage and more by certification agility and sustainability credentials.

Powder Metallurgy Industry Leaders

Höganäs AB

GKN Powder Metallurgy

Sumitomo Electric Industries, Ltd.

ATI

AMETEK Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Gränges and Scandium Canada signed a Memorandum of Understanding (MoU). This partnership focused on incorporating Scandium Canada’s scandium-modified alloys into spray-formed aluminium products and aluminium powders.

- December 2024: Runaya and Eckart partnered to establish a sustainable aluminium powder production facility in India. The joint venture established a new facility in Orissa to manufacture highly sustainable spherical atomized aluminium powder.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the powder metallurgy market as the total value of ferrous and non-ferrous metal powders plus revenues from parts produced through press and sinter, metal injection molding, hot isostatic pressing, and additive manufacturing, across all end-use industries worldwide. According to Mordor Intelligence, this universe generated USD 26.34 billion in 2025.

Scope Exclusion: tooling presses, standalone metal powders sold for welding, and purely ceramic powders lie outside this assessment.

Segmentation Overview

- By Material Type

- Ferrous

- Non-Ferrous

- By Manufacturing Technology

- Press and Sinter

- Metal Injection Molding (MIM)

- Additive Manufacturing / Powder Bed Fusion

- Isostatic Pressing

- By Application

- Automotive

- Industrial Machinery

- Electrical and Electronics

- Aerospace

- Other Applications

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured discussions with powder producers, press makers, contract manufacturers, and procurement engineers across North America, Europe, China, and Japan. Interviews validated utilization rates, typical alloy price spreads, and emerging EV as well as medical part pipelines that desktop work could not fully surface.

Desk Research

We began with trade data from UN Comtrade, production indices from the US Geological Survey, and shipment statistics from the Metal Powder Industries Federation. Government automotive output dashboards (OICA), aerospace build schedules (Aviation Week), and patent counts pulled via Questel revealed demand signals. Company 10-Ks and investor decks rounded out cost and pricing benchmarks. D&B Hoovers supplied private-firm revenue splits. This list is indicative; many other public and paid sources informed the evidence base.

Market-Sizing & Forecasting

We applied a top-down and bottom-up blend. Global metal powder output and average selling prices were first modeled from customs and production statistics, then cross-checked against sampled supplier roll-ups and channel checks. Key variables like vehicle build counts, aircraft deliveries, penetration of additive manufacturing, alloy shift toward stainless and titanium, and average material yield gains drive volume or price nodes in our model. Multivariate regression links these inputs to annual market value, while scenario analysis frames upside from faster EV uptake. Data gaps in smaller geographies were bridged with regional powder-to-vehicle or powder-to-machine ratios derived from primary interviews.

Data Validation & Update Cycle

We run variance checks against historical powder-to-end-use ratios, reconcile currency conversions quarterly, and route anomalies through a two-level analyst review. Reports refresh each year, and material events trigger interim updates before client delivery.

Why Our Powder Metallurgy Baseline Commands Reliability

Published figures often diverge because firms select different process baskets, price decks, and refresh cadences.

Key gap drivers include narrower scopes that ignore legacy press and sinter parts, aggressive price deflation assumptions, or inconsistent conversions from regional currencies. Mordor's disciplined scope, annually verified input set, and live update triggers ensure a balanced baseline for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.34 bn (2025) | Mordor Intelligence | |

| USD 3.31 bn (2025) | Global Consultancy A | Focuses mainly on medical and additive segments; excludes conventional drivetrain parts and Asia's mid-tier producers |

| USD 2.84 bn (2025) | Industry Journal B | Counts only ferrous powders; relies on limited public filings, understating non-ferrous growth |

| USD 3.10 bn (2024) | Regional Consultancy C | Mixes powder value with select component revenues; inconsistent FX conversion methodology |

These comparisons show that once full process coverage, consistent pricing, and transparent refresh rules are applied, Mordor's figures provide the most dependable starting point for strategic decisions.

Key Questions Answered in the Report

How large is the powder metallurgy market in 2026?

The powder metallurgy market size reached USD 26.38 billion in 2026 and is projected to reach USD 32.97 billion through 2031.

Which region generates the most revenue?

Asia-Pacific led with 40.44% of global revenue in 2025, supported by China’s scale and India’s localization programs.

Which application is expanding fastest?

Industrial machinery is growing at a 4.83% CAGR as factory automation increases demand for self-lubricating bushings and hydraulic parts.

What manufacturing technology is gaining share fastest?

Additive manufacturing is forecast to log the quickest 4.91% CAGR as aerospace and medical users move to serial production.

Page last updated on: