Assisted Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

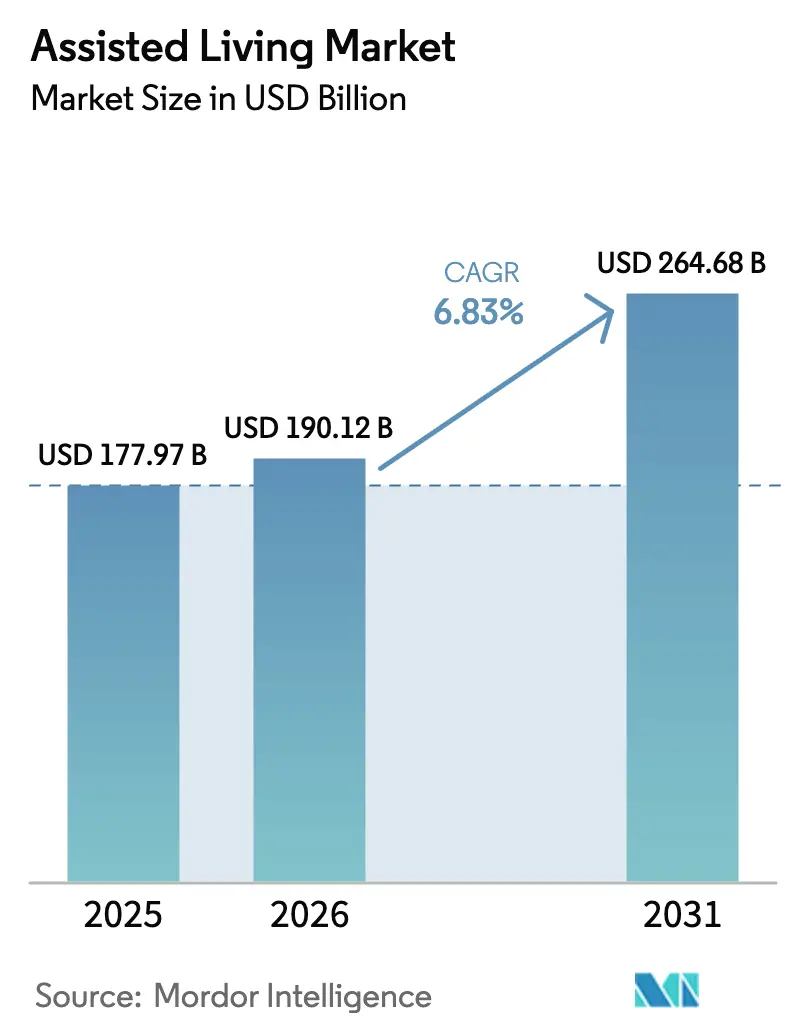

| Market Size (2026) | USD 190.12 Billion |

| Market Size (2031) | USD 264.68 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Assisted Living Market Analysis by Mordor Intelligence

The assisted living market size is expected to grow from USD 177.97 billion in 2025 to USD 190.12 billion in 2026 and is forecast to reach USD 264.68 billion by 2031 at 6.83% CAGR over 2026-2031. Demographic ageing, chronic-disease prevalence, and public-funding reforms are combining to lift demand, while operators re-engineer service models to capture higher-acuity residents and mitigate wage inflation. Expansion of Medicaid waivers, steady private-pay appetite, and rising ESG-linked capital flows are encouraging new supply, although staffing shortages and affordability gaps remain structural hurdles. North America retains the largest regional foothold, yet Asia-Pacific is gaining momentum on the back of policy initiatives such as China’s “silver economy” plan and Japan’s fee-based homes. Competitive intensity is moderate as regulatory barriers deter quick entry, but private-equity-backed consolidation accelerated during 2024–2025, reshaping ownership patterns and accelerating technology adoption.

Key Report Takeaways

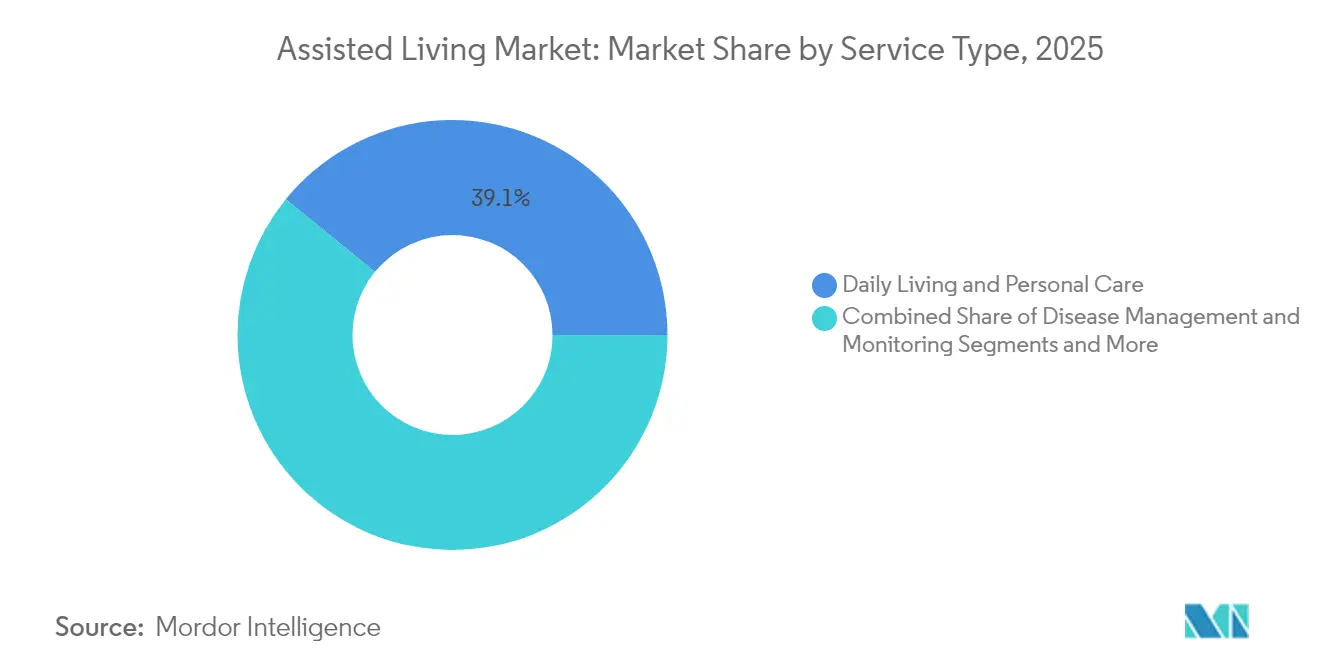

- By service type, Daily Living & Personal Care led with 39.12% revenue share of the assisted living market in 2025; Palliative & Hospice Care is projected to expand at a 10.31% CAGR through 2031.

- By facility type, Adult Family Homes commanded 49.25% of assisted living market share in 2025, while Small-Home/Green-House Models are set to grow at a 10.02% CAGR to 2031.

- By payment source, the Private Pay segment held 65.42% of the assisted living market size in 2025; Medicaid funding is the fastest-growing source, forecast at an 10.71% CAGR through 2031.

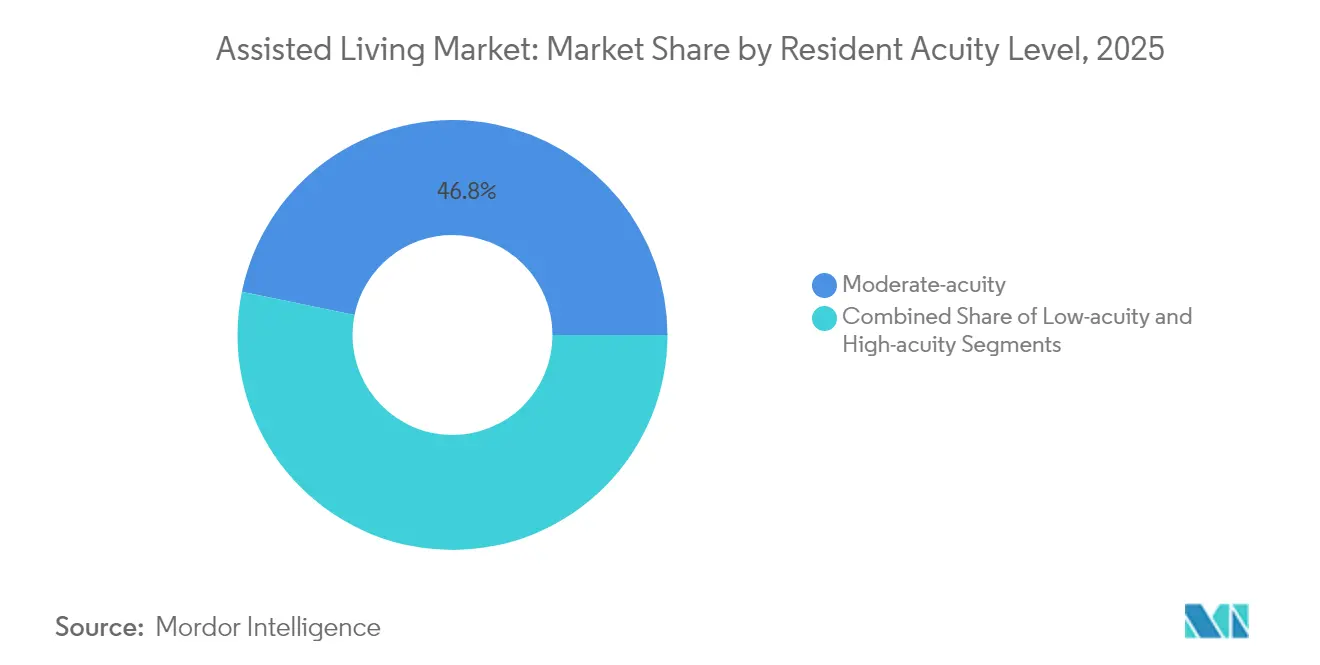

- By resident acuity, Moderate-acuity residents accounted for 46.78% of assisted living market share in 2025, whereas High-acuity/Memory-Care residents will expand at a 9.86% CAGR.

- By assisted-living model, Luxury & Lifestyle Communities covered 35.31% of assisted living market share in 2025; Tech-enabled “Smart” Communities should post an 11.36% CAGR to 2031.

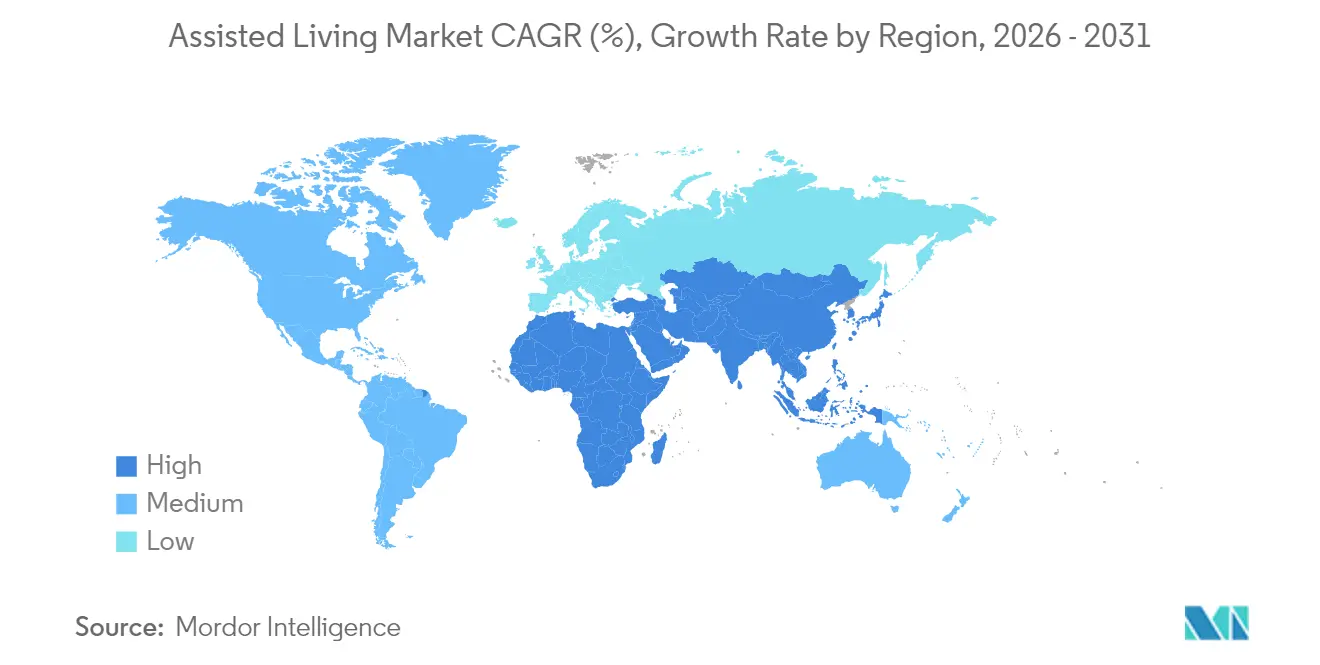

- By geography, North America captured 35.87% assisted living market share in 2025; Asia-Pacific is the fastest-growing region with a 9.21% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Assisted Living Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geriatric population worldwide | +2.8% | Global, concentration in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Medicaid waivers and government funding | +1.9% | North America, state-level variations | Medium term (2-4 years) |

| Rising prevalence of chronic diseases requiring long-term care | +1.5% | Global, higher impact in developed markets | Long term (≥ 4 years) |

| Emergence of cost-efficient “middle-market” assisted-living models | +1.2% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-driven predictive health-monitoring improving care outcomes | +0.8% | North America, Europe, global spillover | Short term (≤ 2 years) |

| ESG-linked capital inflows into senior housing assets | +0.6% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population Worldwide

The 80-plus cohort is expanding faster than any other age group, creating strong underlying demand for residential care solutions; in the United States older adults already outnumber children in 11 states, while Canada’s 85-plus population could triple by 2073.[1]U.S. Census Bureau, “Older Adults Outnumber Children in 11 States and Nearly Half of U.S. Counties,” census.gov Longevity gains lift average life expectancy to 78.9 years in 2025 and 82.3 years by 2055, extending the duration of support services required.[2]Congressional Budget Office, “The Demographic Outlook: 2025 to 2055,” cbo.gov Drivers Health-care REITs report that more than 40% of seniors can self-fund senior housing without depleting savings, signalling durable private-pay capacity. As working-age dependency ratios rise, public and private sectors are mobilising resources to expand assisted living capacity, notably through China’s “silver economy” programme that targets multi-trillion-dollar spending on elder services.

Expansion Of Medicaid Waivers & Government Funding

The 2024 Medicaid Access Rule mandates that at least 80% of certain home- and community-based payments flow directly to care-worker wages, bringing 46 states and Washington D.C. closer to reimbursement adequacy and supporting service quality.[3]Centers for Medicare & Medicaid Services, “Biden-Harris Administration Takes Historic Action to Increase Access to Quality Care, and Support to Families and Care Workers,” cms.gov Revised 2025 Supplemental Security Income resource standards set liquid-asset limits of USD 9,660 for singles and USD 14,470 for married couples, broadening eligibility for subsidised care. States such as Ohio and Virginia indexed program rates to inflation in 2025, signalling bipartisan support for long-term-care funding. These steps underpin the assisted living market by narrowing affordability gaps for middle-income seniors.

Rising Prevalence Of Chronic Diseases Requiring Long-Term Care

One-third of older Americans live with a disability that hampers independent living and 1.3 million older adults already reside in nursing homes, highlighting system-wide pressure to manage multi-morbidity outside hospitals. Medicare’s 2025 policy update formalised ten core chronic-disease categories for Medication Therapy Management programmes, strengthening clinical oversight within community settings. Alzheimer’s disease alone is projected to affect 13.8 million Americans aged 65-plus by 2050, intensifying demand for memory‐care-ready residences.

Emergence Of Cost-Efficient “Middle-Market” Assisted-Living Models

Roughly 16 million seniors will earn too much for Medicaid but too little for luxury options by 2033, opening space for monthly rents between USD 2,500 and USD 4,500. Operators are leveraging dynamic pricing engines and small-house designs to cut overheads while sustaining care standards. Public-private alliances such as Wallick Communities’ USD 5.8 million tax-credit-backed project exemplify innovation in capital sourcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of care and affordability gaps | -1.8% | Global, acute in high-cost markets | Long term (≥ 4 years) |

| Persistent workforce shortages of skilled caregivers | -1.4% | North America, Europe, widening in Asia-Pacific | Medium term (2-4 years) |

| Stricter state staffing-ratio mandates raising operating costs | -0.9% | North America, regulatory spillover potential | Short term (≤ 2 years) |

| Aging-in-place technology delaying facility move-ins | -0.7% | Developed markets with high tech adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Of Care And Affordability Gaps

Lease and service fees climbed 10% across senior-care settings in 2025, outpacing wage growth and eroding affordability even as demand rises. Median monthly assisted-living fees could reach USD 7,776 by 2040, reinforcing consumer preference for aging in place. Medicaid reimbursements cover roughly 82% of actual nursing-home costs, and 40% of facilities receive less than 80% of their expense base, forcing selective admission policies.[4]U.S. Department of Health and Human Services, “Assessing Medicaid Payment Rates and Costs of Caring for the Medicaid Population Residing in Nursing Homes,” hhs.gov Diverging rental-rate trajectories between independent living and assisted living signal growing price-sensitivity and geographic fragmentation.

Persistent Workforce Shortages Of Skilled Caregivers

New federal standards require 3.48 nurse hours per resident per day, yet 75.46% of providers presently fall short, necessitating 100,000 additional hires at an annual payroll cost of USD 6.8 billion. Survey data attribute recruitment challenges to low pay, high burnout, and pandemic-driven attrition. Meeting compliance could add USD 43 billion of labour expense over ten years, squeezing margins and raising pricing pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Palliative Care Drives Growth

Daily Living & Personal Care retained 39.12% of assisted living market share in 2025, underscoring its role as the baseline service bundle for residents who require help with bathing, dressing, meals, and medication reminders. Palliative & Hospice Care is set to grow at a 10.31% CAGR, aided by updated Medicaid hospice rates of USD 224.91 per routine-care day and USD 1,170.04 per inpatient day for compliant providers. Disease-Management and Medication-Monitoring services are benefiting from policy-mandated chronic-care protocols that reward proactive clinical oversight. Mobility Assistance remains steady as the 85-plus demographic widens.

Demand patterns show residents and families valuing a continuum that blends hospitality with clinical capacity. As acuity levels rise, management teams integrate nurse practitioners and tele-health partners to avoid hospital transfers and secure referral streams from accountable-care organisations. The assisted living market size attributed to comfort-focused services is projected to widen as payers recognise cost offsets versus acute settings, reinforcing investment in staff training and palliative certification.

By Facility Type: Small-Home Models Gain Momentum

Adult Family Homes accounted for 49.25% of assisted living market share in 2025 thanks to their six-to-eight-bed capacity, domestic ambiance, and lower build cost. Small-Home and Green-House formats are on a 10.02% CAGR trajectory, buoyed by evidence that residents experience fewer hospitalisations and greater life satisfaction relative to traditional buildings. Community-based Residential Facilities and Residential Care Apartment Complexes bridge affordability for the middle market, while Continuing-Care Retirement Communities (CCRCs) target higher-income households seeking a campus style continuum.

Operators embracing household layouts leverage modular construction and universal-worker staffing to curb per-bed capital outlays. Infection-control performance through the pandemic further validated decentralised architecture, positioning small-home models as a resilient choice. Several states now offer certificate-of-need exemptions or fast-track licensing for projects under 12 beds, accelerating pipeline growth.

By Payment Source: Medicaid Expansion Accelerates

Private Pay residents generated 65.42% of assisted living market size in 2025, with monthly fees ranging USD 2,500–7,000 depending on locale, amenities, and care bundle. Medicaid funding will grow 10.71% annually as states enlarge waiver slots and align payment floors with direct-care wage mandates. Veterans’ Affairs stipends and other public pensions provide layered funding but remain niche owing to eligibility caps.

Operators are rebalancing resident mixes to pair Medicaid beds with higher-margin private units, mitigating reimbursement deficits. Some chains pilot “Medicaid-plus” packages that allow add-on services billed separately, protecting margins while supporting access. Assisted living market share driven by public-pay sources is expected to rise but will still trail private pay in absolute dollars through 2031.

By Resident Acuity Level: Memory Care Expansion

Moderate-acuity residents held 46.78% share in 2025, typifying the traditional assisted living customer who needs daily prompts but not constant clinical oversight. High-acuity/Memory-Care residents will climb at a 9.86% CAGR, powered by Alzheimer’s incidence and longer survival with cognitive impairment. Low-acuity Independent-Plus cohorts are also forming an entry-level funnel, as active seniors choose community amenities for preventative benefits.

To serve higher acuity safely, operators retrofit wings with wander-management systems, staff dementia-trained caregivers, and enrich programming. Pricing premia of 15%–25% over standard units help cover additional labour. The assisted living market size for dedicated memory-care suites is forecast to rise proportionally faster than overall inventory as clinical protocols and design best practices proliferate.

By Assisted-Living Model: Technology Integration Leads

Luxury & Lifestyle Communities covered 35.31% assisted living market share in 2025, offering resort-style culinary, wellness, and cultural services. Tech-enabled “Smart” Communities will post an 11.36% CAGR on adoption of IoT analytics, voice-activated controls, and predictive maintenance, features prized by tech-savvy baby boomers. Value/Middle-Market schemes focus on operational efficiency and are increasingly co-locating with primary-care clinics to offer bundled packages. Small-Home/Green-House formats continue their person-centred momentum, especially in states offering construction incentives.

Technology is no longer a differentiator but a baseline expectation among prospective residents and adult-children decision makers. Operators integrate electronic health records, fall-detection wearables, and app-based family portals to improve transparency and reduce nurse call volumes. Assisted living market stakeholders view these upgrades as key to resident safety and occupancy gains.

Geography Analysis

North America contributed 35.87% of assisted living market share in 2025, anchored by the United States where the 65-plus population grew 3.1% to 61.2 million in 2024. Federal Medicaid waivers, Medicare Advantage supplemental benefits, and abundant private equity have created a sophisticated ecosystem for development and acquisition. Canada’s 85-plus cohort is on track to triple, prompting provincial investments in new long-term-care capacities. Mexico, though nascent, is witnessing pilot projects aimed at the urban middle class.

Asia-Pacific is the fastest-growing region with a 9.21% CAGR forecast. China’s “silver economy” blueprint envisages trillions in elderly-service spending, encompassing nursing homes, homecare, and digital-health platforms. Japan will have one in four citizens aged 75-plus by 2025, pushing occupancy at fee-based homes near 92% and spawning REIT interest. India’s Ashiana Housing and South Korea’s luxury developers are tailoring formats to local cultural preferences, illustrating regional segmentation.

Europe remains mature yet resilient as welfare systems cap out-of-pocket risk. New supply is concentrated in Germany, the Nordics, and Spain where demographic momentum persists and private insurers co-finance operations. Middle East and Africa offer long-run option value once cultural acceptance and regulatory scaffolding improve; GCC countries are already piloting high-end communities for expatriate retirees. Assisted living market size across emerging economies is expected to deepen as multinationals partner with local hospitals and construction firms.

Competitive Landscape

The assisted living market is moderately concentrated with the top 25 operators controlling under 30% of total capacity. Private equity intensified acquisition pace in 2024–2025, exemplified by Welltower’s USD 969 million purchase of an active-adult portfolio and Brookdale’s USD 610 million buy-back of 41 leases. Fortress Investment Group’s April 2025 takeover of The Village at Gainesville, a multi-level campus with an 80-person wait list, underscores demand for scale assets.

Strategic themes include vertical integration into hospice, home-health, and therapy to lift revenue per resident and diversify payor mix. Operators deploy smart-building technologies to cut utilities 10%–15% and monitor resident vitals remotely, enhancing marketability. Green-House and small-home entrants are capturing niche loyalty, while traditional chains renovate legacy wings into household clusters to defend share. Aging-in-place tech firms represent an external threat by enabling care at home, but several providers are co-opting these solutions to build hybrid service lines.

Capital markets remain receptive; healthcare REITs posted 8.5% returns in 2025, and institutional investors classify senior housing as a defensive inflation hedge due to annual rent escalators and consistent occupancy. The confluence of demographics and yield spreads suggests ongoing consolidation as smaller operators seek exit liquidity amidst regulatory complexity.

Assisted Living Industry Leaders

Atria Senior Living, Inc.

Brookdale Senior Living Inc.

Sunrise Senior Living

LCS (Life Care Services)

Five Star Senior Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Fortress Investment Group acquired The Village at Gainesville, a mixed-care campus with independent living, assisted living, and memory-care units.

- March 2025: Welltower agreed to buy Amica Senior Lifestyles for CAD 4.6 billion (USD 3.4 billion), marking the largest Canadian senior-housing transaction to date.

- March 2025: Spring Arbor and Allegro announced a partnership that forms a 53-property platform across multiple U.S. states.

Global Assisted Living Market Report Scope

Assisted living provides support for daily activities like bathing, dressing, and managing medications, all while enabling residents to retain a degree of independence.

The assisted living market is segmented by service type, facility type, age group, and geography. By service type, the market is segmented into medication monitoring, palliative and hospice care, disease monitoring, mobility, and others. The others segment includes disability and memory care, nutrition care, and others. By facility type, the market is segmented into adult family homes, community-based residential facilities, and residential care apartment complexes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for all the above segments.

| Medication Monitoring |

| Palliative & Hospice Care |

| Disease Management & Monitoring |

| Mobility Assistance |

| Daily Living & Personal Care |

| Adult Family Homes |

| Community-based Residential Facilities |

| Residential Care Apartment Complexes |

| Continuing-Care Retirement Communities (CCRCs) |

| Private Pay |

| Medicaid |

| Veterans’ & Public Pensions |

| Low-acuity (Independent-Plus) |

| Moderate-acuity (Traditional ALF) |

| High-acuity / Memory-Care |

| Luxury & Lifestyle Communities |

| Value / Middle-Market Communities |

| Small-Home / Green-House Models |

| Tech-enabled “Smart” Communities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Medication Monitoring | |

| Palliative & Hospice Care | ||

| Disease Management & Monitoring | ||

| Mobility Assistance | ||

| Daily Living & Personal Care | ||

| By Facility Type | Adult Family Homes | |

| Community-based Residential Facilities | ||

| Residential Care Apartment Complexes | ||

| Continuing-Care Retirement Communities (CCRCs) | ||

| By Payment Source | Private Pay | |

| Medicaid | ||

| Veterans’ & Public Pensions | ||

| By Resident Acuity Level | Low-acuity (Independent-Plus) | |

| Moderate-acuity (Traditional ALF) | ||

| High-acuity / Memory-Care | ||

| By Assisted-Living Model | Luxury & Lifestyle Communities | |

| Value / Middle-Market Communities | ||

| Small-Home / Green-House Models | ||

| Tech-enabled “Smart” Communities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the assisted living market?

The assisted living market generated USD 190.12 billion in 2026 and is on track to reach USD 264.68 billion by 2031.

Which service segment is growing the fastest?

Palliative & Hospice Care is the fastest-expanding service, forecast at a 10.31% CAGR to 2031.

How significant is Medicaid funding for assisted living operators?

Medicaid covered 33.9% of residents in 2024 and is forecast to grow at an 10.71% CAGR, reflecting expanded waiver programs and revised payment rules.

Why are small-home or Green-House models gaining popularity?

Evidence indicates they deliver higher resident satisfaction and lower hospitalisation rates while allowing intimate, household-style living.

Which region will grow the quickest through 2031?

Asia-Pacific leads with a projected 9.21% CAGR thanks to rapid ageing, policy incentives, and private-sector investment.

How is technology changing assisted living communities?

IoT sensors, AI health analytics, and app-based family portals are now standard, improving safety, enabling predictive care, and enhancing resident engagement.

Page last updated on: