Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 61.65 Billion |

| Market Size (2026) | USD 73.59 Billion |

| Market Size (2031) | USD 178.16 Billion |

| Growth Rate (2026 - 2031) | 19.36% CAGR |

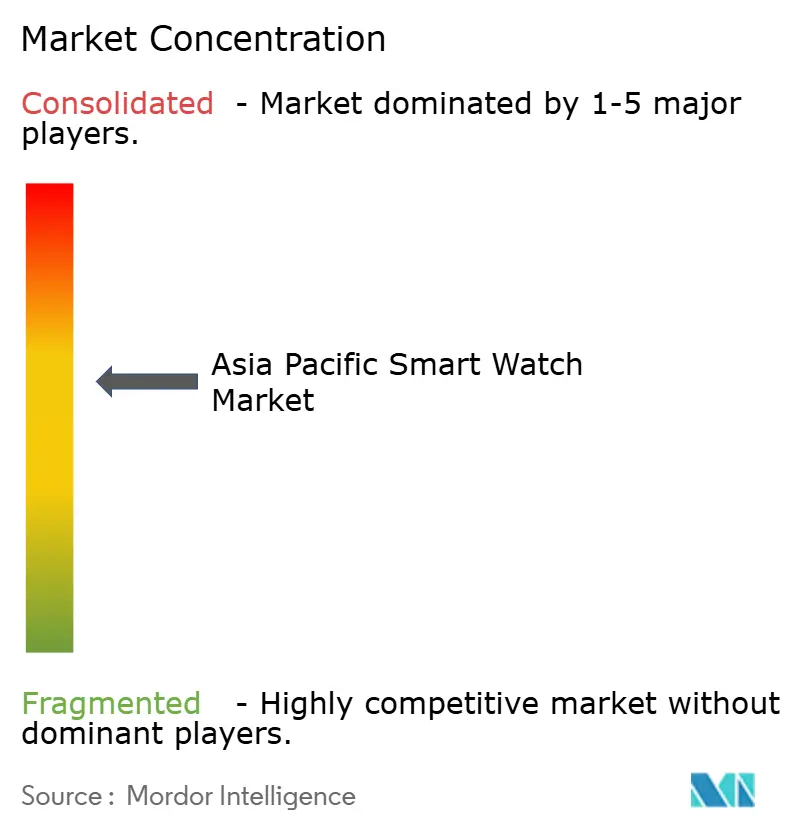

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Smart Watch Market Analysis by Mordor Intelligence

Asia Pacific Smart Watch market size in 2026 is estimated at USD 73.59 billion, growing from 2025 value of USD 61.65 billion with 2031 projections showing USD 178.16 billion, growing at 19.36% CAGR over 2026-2031. Robust consumer adoption, vertically integrated manufacturing hubs, and growing health-monitoring awareness underpin this acceleration. China leads shipments and value creation on the back of expansive supply chains, while India’s electronics-manufacturing push and aggressive insurance incentives are catalyzing the region’s fastest unit growth. Rapid 5G rollout, rising penetration of premium AMOLED displays, and ecosystem lock-in strategies by major smartphone vendors widen feature sets, deepen user engagement, and elevate replacement demand. Component tariffs, battery-life constraints, and emerging e-waste regulations temper the trajectory but have not derailed investment momentum across the Asia Pacific smart watch market.

Key Report Takeaways

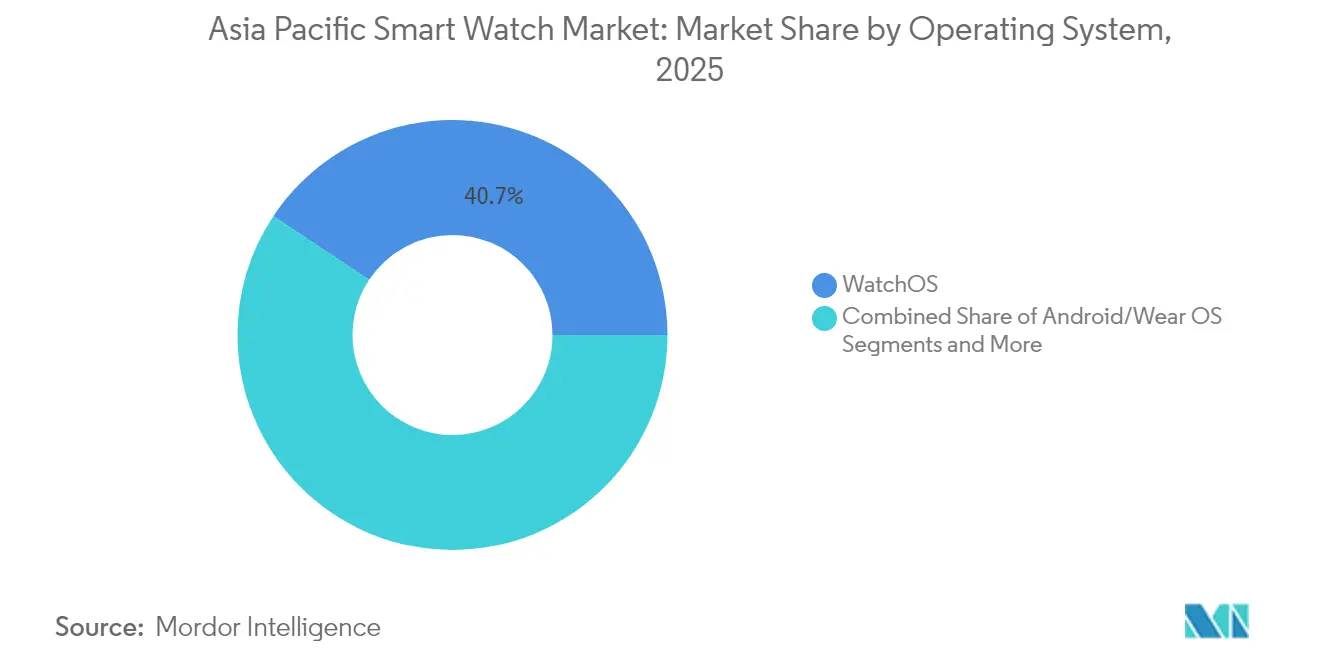

- By operating system, WatchOS retained 40.68% of the Asia Pacific smartwatch market share in 2025, while RTOS platforms are advancing at 19.65% CAGR through 2031.

- By display technology, AMOLED captured 51.97% of the Asia Pacific smartwatch market size in 2025, whereas PMOLED displays are forecast to post a 19.72% CAGR from 2026 to 2031, making them the most rapidly expanding display category.

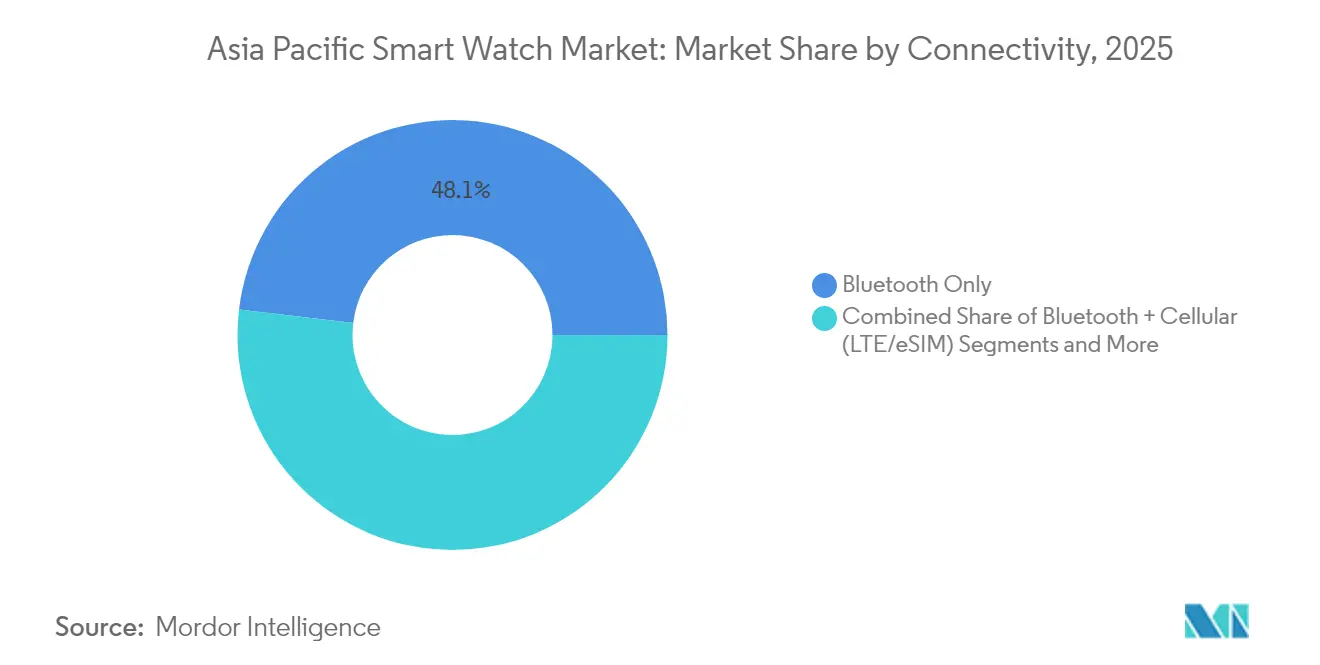

- By connectivity, Bluetooth-only models accounted for 48.10% shipments in 2025, while 5G Standalone connectivity is projected to scale at 20.52% CAGR through 2031.

- By application, sports and fitness held 36.21% revenue share in 2025; medical and health monitoring is on track for the highest 21.12% CAGR to 2031.

- By country, China commanded a 39.10% share of the Asia Pacific smart watch market in 2025, whereas India is anticipated to log a 21.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Smart Watch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of health and fitness sensors in affordable smart watches | +3.5% | China, India, Southeast Asia | Medium term (2-4 years) |

| Ecosystem lock-in strategies by smartphone OEMs | +2.1% | Global; strongest in China and Japan | Long term (≥4 years) |

| Rapid 5G rollout enabling always-connected features | +1.8% | Japan, South Korea, urban China | Short term (≤2 years) |

| Insurance-linked wellness premium discounts | +0.9% | India, Australia, emerging Southeast Asia | Medium term (2-4 years) |

| Local contract-manufacturing incentives in India and Vietnam | +0.7% | India, Vietnam, regional spillover | Long term (≥4 years) |

| Integration of eSIM and contactless payment raising daily utility | +0.4% | Japan, South Korea, urban APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Health and Fitness Sensors in Affordable Smart Watches

Sensor miniaturization has transformed entry-level units into full health dashboards that track heart rate, SpO2, and stress indicators. Huawei’s Watch GT 5 debuted at JPY 1,488 (USD 207) in China and EUR 249 (USD 279) in Europe with TruSense analytics, pushing sophisticated biometrics into mid-price tiers [1]South China Morning Post, “Huawei heats up global smartwatch market with launch of new GT 5 series,” scmp.com . China consequently recorded 18.7% year-over-year shipment growth to 11.1 million units in Q2 2024. Samsung’s Galaxy Watch8 adds AI-driven sleep and vascular-load insights to mainstream models. Blood-pressure and glucose-trend features now enter mass-market price points, expanding demand beyond fitness enthusiasts into chronic-disease management cohorts.

Ecosystem Lock-in Strategies by Smartphone OEMs

Proprietary integration heightens switching costs. Apple links iPhone hydration-tracking IP with WatchOS health data, encouraging brand loyalty within Japan, where iOS holds 59% mobile OS share. Samsung interlocks Galaxy handsets, watches, and Samsung Health for unified user journeys. Huawei’s HarmonyOS secures top global wrist-worn market share for two straight quarters. Consumers increasingly prioritize compatibility over individual hardware specs when selecting devices, reshaping the competitive contours of the Asia Pacific smart watch market.

Rapid 5G Rollout Enabling Always-Connected Features

Near-ubiquitous 5G in Japan and advanced standalone deployments in South Korea push smart watches toward full independence from smartphones. RedCap technology delivers 150 Mbps downlink with lower power draw, mitigating battery-life trade-offs [2]GSMA Intelligence, “5G RedCap: Enabling the Next Generation of IoT,” gsmaintelligence.com. NTT Docomo’s One Number service lets Galaxy Watch8 share a mobile number with an existing plan, streamlining consumer costs. Emerging enterprise use cases in healthcare and manufacturing further elevate networked-wearable value propositions across the Asia Pacific smart watch market.

Insurance-Linked Wellness Premium Discounts

Care Health Insurance offers up to 30% policy savings for Indian customers who actively log smartwatch health data, turning wearables into financially sensible purchases [3]Economic Times, “Care Health Insurance launches wellness program offering up to 30% discount on premiums,” economictimes.indiatimes.com. This model links daily activity to tangible monetary upside, encourages consistent device usage, and fuels accelerated growth in cost-conscious markets. Privacy regulations such as China’s Network Data Security Management Regulations, effective January 2025, favor well-capitalized vendors that can meet stringent localization and protection requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short replacement cycles driving e-waste regulation | -1.2% | South Korea, Japan, China, India | Medium term (2-4 years) |

| Battery-life limitations in advanced displays | -0.8% | Global; AMOLED-heavy segments | Short term (≤2 years) |

| Tightening data-privacy laws in China and India | -1.1% | China, India, Vietnam | Short term (≤2 years) |

| High tariffs on imported components | -0.6% | Australia, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short Replacement Cycles Driving E-waste Regulation

Smart watches average two- to three-year lifespans, half that of smartphones, amplifying electronic waste volumes. South Korea’s expanded RoHS and Extended Producer Responsibility requirements now encompass wearables and will fully apply by 2028. India’s E-Waste Management Rules set escalating collection targets, compelling OEMs to fund take-back logistics that erode margins. Compliance favors vendors with robust reverse-supply chains and may consolidate shares within the Asia Pacific smart watch market.

Battery-Life Limitations in Advanced Displays

AMOLED panels, while commanding a 52.67% share, consume up to 30% more power than PMOLED during active use. Feature-rich models integrating AI and 5G exacerbate drain, often pushing users toward daily charging. Micro-LED promises relief but remains cost-prohibitive for mass-market adoption. Battery degradation over multi-year ownership cycles can diminish satisfaction and extend decision times for upgrade, restraining high-end replacement momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: WatchOS Retains Pole Position while RTOS Scales Fast

WatchOS secured 40.68% of the Asia Pacific smart watch market share in 2025 on seamless iPhone integration amid Apple’s 18% Q4 shipment decline. The Asia Pacific smart watch market size tied to WatchOS is forecast to expand in lockstep with premium handset upgrades despite intensifying regional price competition. Android/Wear OS rebounds through Samsung’s Galaxy Watch8, which embeds on-device Gemini AI, while Huawei continues HarmonyOS diversification.

Real-Time Operating Systems are climbing at 19.65% CAGR as industrial, medical, and ultra-long-life use cases demand deterministic performance. RTOS solutions often forego expansive app libraries for predictable latency and extended battery profiles. Regulatory data-localization mandates in China and India further catalyze domestic OS innovation, ensuring a pluralistic software landscape inside the Asia Pacific smart watch market.

By Display Technology: AMOLED Dominates Yet Faces Efficiency Pressure

AMOLED comprised 51.97% revenue across the Asia Pacific smart watch market in 2025, driven by Samsung’s vertical integration and pixel-level illumination benefits that sustain always-on modes without excessive drain. Elevated brightness and wide color gamuts enhance medical imaging readability and outdoor fitness visibility.

PMOLED’s 19.72% CAGR underscores its resonance in entry-level tiers where affordability and low-power traits resonate. TFT LCD maintains relevance in cost-sensitive Southeast Asian markets. Micro-LED prototypes showcase AMOLED-grade visuals with lower energy usage but carry premium price tags, signaling a potential inflection point later in the decade for the Asia Pacific smart watch industry.

By Connectivity: Bluetooth Prevails but Standalone 5G Emerges

Bluetooth-only options held 48.10% shipment weighting in 2025, balancing power draw and cost by leveraging paired smartphones for connectivity. This approach sustains dominance in price-sensitive segments and battery-life-minded user cohorts.

The Asia Pacific smart watch market size attributed to 5G Standalone modules is projected to post a 20.52% CAGR, propelled by nationwide 5G coverage in Japan and South Korea, and by RedCap chipset rollouts. Operators such as NTT Docomo now bundle watch connectivity under single-number plans, lowering subscription friction and positioning cellular watches as independent safety and productivity tools.

By Application: Medical Monitoring Disrupts Fitness Primacy

Sports and fitness functions accounted for 36.21% value in 2025, reflecting enduring consumer interest in activity metrics and personalized coaching. High-end GPS, VO₂ max estimation, and athlete-grade ruggedization sustain differentiation for specialist brands.

Yet medical and health monitoring will expand at 21.12% CAGR as regulatory clearances pave the way for blood-pressure, ECG, and glucose-trend capabilities. FDA authorization of Google Pixel Watch 3’s loss-of-pulse feature exemplifies the clinical validation trend. Insurance incentives and aging demographics collectively move smart watches from lifestyle accessories to preventive-health necessities within the Asia Pacific smart watch market.

Geography Analysis

China commanded 39.10% of the Asia Pacific smart watch market share in 2025 and posted 29% year-over-year shipment growth in Q4 2024. Domestic champions Huawei and Xiaomi exploit Guangdong’s deep component clusters to accelerate design iterations and undercut imported rivals. The Network Data Security Management Regulations implemented in 2025 elevate local hosting requirements, nudging foreign brands toward joint-venture models or localized cloud infrastructure.

India, with a forecast 21.45% CAGR, benefits from Production-Linked Incentive schemes and a USD 18.2 billion semiconductor mission that stimulates component self-sufficiency. Contract manufacturers such as Dixon partner with Chinese IP holders to deliver regionally priced offerings. Insurance-linked 30% premium discounts unlock new buyer cohorts, reinforcing volume gains across the Asia Pacific smart watch market.

Japan, South Korea, Australia, and New Zealand represent saturation-stage environments where nearly universal 5G and affluent consumer bases support premium, always-connected devices. NTT Docomo’s shared-number services ease recurring-fee anxiety, spurring incremental upgrades. Conversely, Southeast Asia and the rest of the Asia Pacific see uptake linked to rising disposable income and digital-payment adoption, with eSIM features lowering cross-border roaming hassles in tourism-heavy economies.

Competitive Landscape

Market concentration is moderate as entrenched global brands confront agile regional entrants. Apple remains the global revenue leader. Huawei has secured a significant global wrist-worn share for two consecutive quarters by combining extended battery life with medical-grade sensors. Samsung differentiates through proprietary AMOLED fabrication and ecosystem breadth, embedding Gemini AI in Galaxy Watch8 to solidify high-end mindshare.

Chinese challengers Xiaomi, OPPO, and BBK subsidiaries plus Indian disruptors Noise and boAt deploy aggressive pricing and rapid feature catch-up to erode incumbents’ gaps. Masimo’s collaboration with Google and Qualcomm on Wear OS reference designs compresses ODM development cycles and could widen vendor participation. Supply-chain realignment toward India and Vietnam diversifies risk away from tariff-exposed Chinese exports, yet established players still leverage economies of scale and R&D heft to defend premium tiers inside the Asia Pacific smart watch market.

Asia Pacific Smart Watch Industry Leaders

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Apple Inc.

BBK Electronics Industry Co., Ltd.

Garmin Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Australia’s Cyber Security Standards for Smart Devices Rules 2025 came into force, obliging watch makers to implement secure boot, encryption, and coordinated vulnerability disclosure.

- July 2025: Samsung introduced Galaxy Watch8, Watch8 Classic, and Watch Ultra in Japan through NTT Docomo, bundling AI coaching and One Number plan support with JPY 6,600 launch discounts.

- February 2025: Samsung accelerated Galaxy S25 launch in Japan alongside Galaxy Fit3 and a forthcoming Galaxy Ring, with SoftBank reviving Samsung handset sales after an 11-year hiatus.

- January 2025: China’s Network Data Security Management Regulations took effect, mandating local processing for health data and approval for cross-border transfers.

Asia Pacific Smart Watch Market Report Scope

A smartwatch is a wearable electronic device with computed capabilities for specific functions and closely resembles a wristwatch. Smartwatches provide a local touchscreen interface for daily use, while a connected smartphone app enables management and telemetry, such as long-term biomonitoring. Owing to the type of application it is used for, and in addition to displaying the time, many smartwatches have wireless communication capabilities that a user can use from the watches interface to initiate and answer phone calls, read emails and messages, receive weather reports updates, dictate emails or text messages, or use it as a personal digital assistant.

Asia-Pacific smartwatches market is segmented by operating systems (watch OS, android/wear OS, other operating systems), display type (AMOLED, PMOLED, TFT LCD), application (personal assistance, medical, sports, other applications), and country (China, Japan, India, South Korea, rest of Asia-Pacific).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Operating System

| WatchOS |

| Android/Wear OS |

| Real-Time Operating Systems (RTOS) |

| Other Operating Systems |

By Display Technology

| AMOLED |

| PMOLED |

| TFT LCD |

By Connectivity

| Bluetooth Only |

| Bluetooth + Cellular (LTE/eSIM) |

| 5G Standalone |

By Application

| Personal Assistance |

| Medical and Health Monitoring |

| Sports and Fitness |

| Other Applications (Kids and Elderly Safety, etc.) |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| South East Asia |

| Rest of Asia Pacific |

| By Operating System | WatchOS |

| Android/Wear OS | |

| Real-Time Operating Systems (RTOS) | |

| Other Operating Systems | |

| By Display Technology | AMOLED |

| PMOLED | |

| TFT LCD | |

| By Connectivity | Bluetooth Only |

| Bluetooth + Cellular (LTE/eSIM) | |

| 5G Standalone | |

| By Application | Personal Assistance |

| Medical and Health Monitoring | |

| Sports and Fitness | |

| Other Applications (Kids and Elderly Safety, etc.) | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| South East Asia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific smart watch market in 2026?

The Asia Pacific smart watch market size is USD 73.59 billion in 2026.

What is the projected CAGR for smart-watch sales in Asia Pacific through 2031?

Regional revenue is forecast to rise at a 19.36% CAGR from 2026 to 2031.

Which operating-system segment is expanding the fastest across Asia Pacific?

Real-Time Operating Systems are registering the highest 19.65% CAGR.

Why is India emerging as the fastest-growing geography?

Production incentives, contract-manufacturing growth, and insurance-linked premium discounts are driving a 21.45% CAGR in India.

What connectivity trend is reshaping product design?

Standalone 5G modules are scaling at 20.52% CAGR, enabling watches to operate independently of smartphones.

How do e-waste regulations affect smartwatch vendors?

Extended Producer Responsibility rules in markets such as South Korea force brands to finance collection and recycling, adding cost and favoring companies with mature reverse-logistics networks.

Page last updated on: