Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

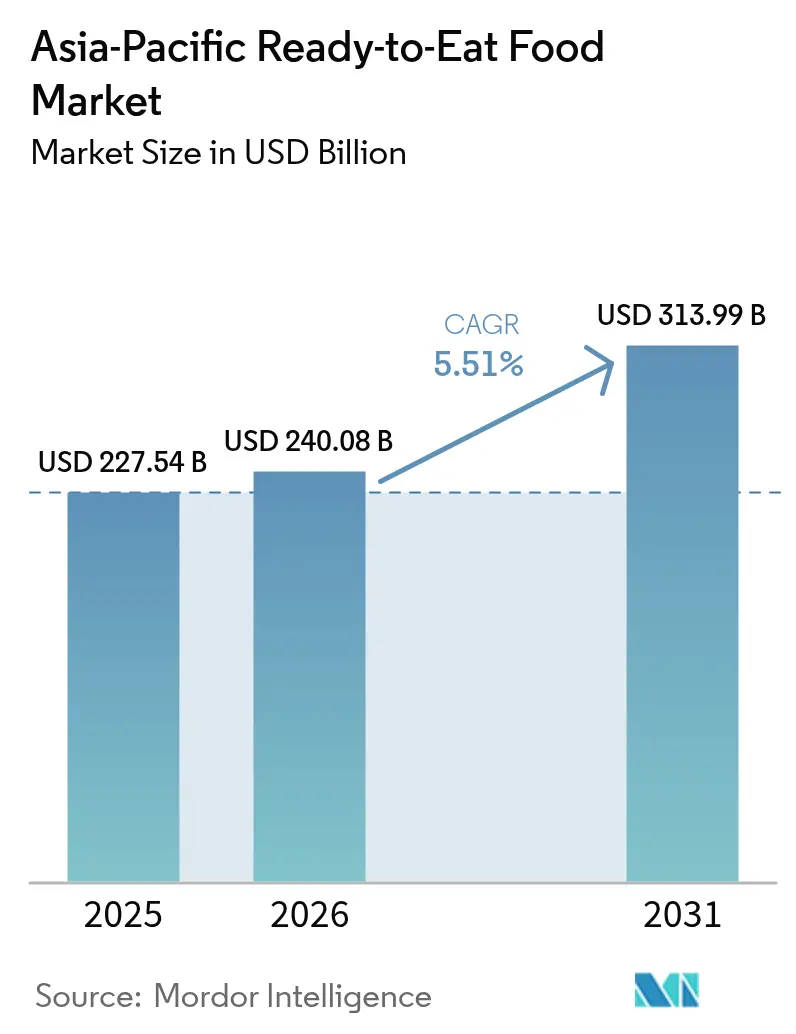

| Base Year Market Size (2025) | USD 227.54 Billion |

| Market Size (2026) | USD 240.08 Billion |

| Market Size (2031) | USD 313.99 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Ready-to-Eat Food Market Analysis by Mordor Intelligence

The Asia-Pacific ready-to-eat food market size is expected to grow from USD 227.54 billion in 2025 to USD 240.08 billion in 2026 and is forecast to reach USD 313.99 billion by 2031 at 5.51% CAGR over 2026-2031. Rapid urbanization, expanding middle-income populations, and busier lifestyles underpin this steady climb, especially in metropolitan hubs where dual-earner families rely on convenient yet nutritious meal solutions. Manufacturers are responding with products that balance flavor, shelf life, and clean-label credentials, while retailers invest in technology-enabled cold chains to maintain quality during distribution. Digital commerce is reshaping consumer access as online platforms widen product choice and shorten delivery windows. In parallel, government incentives from China’s infrastructure programs to India’s Production Linked Incentive Scheme are catalyzing capacity upgrades across processing, packaging, and logistics.

Key Report Takeaways

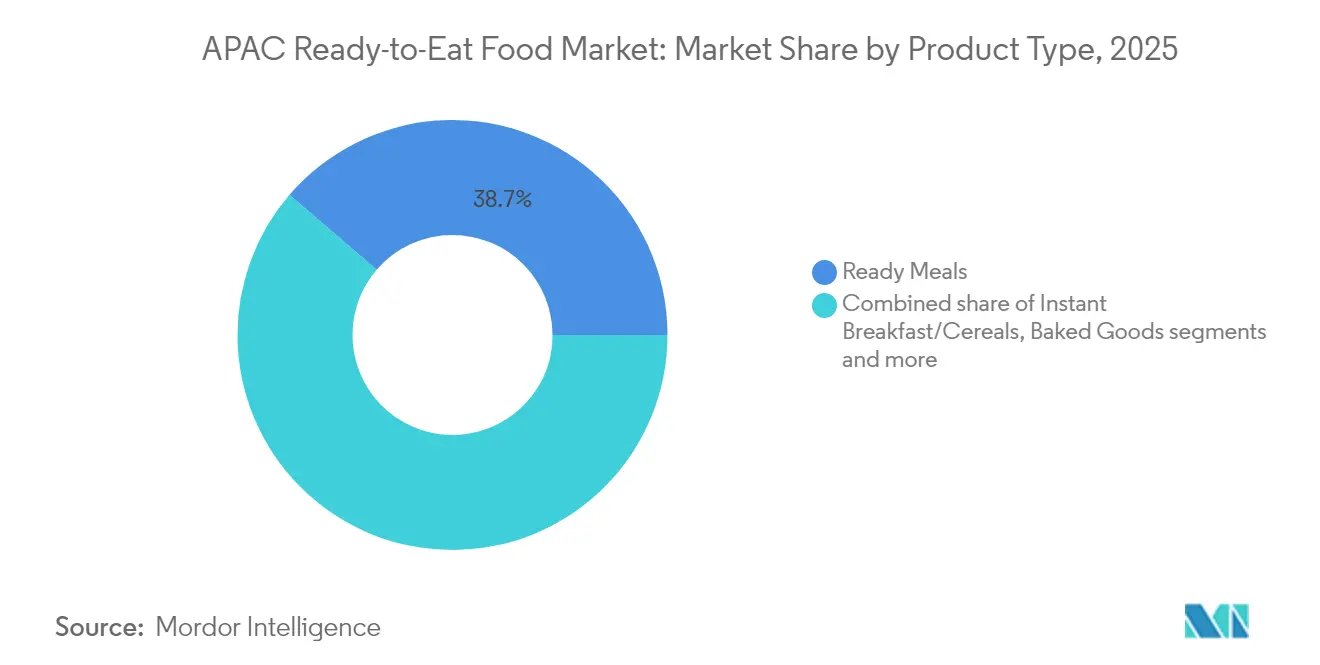

- By product category, ready meals led with 38.70% revenue share of the Asia-Pacific ready-to-eat food market in 2025, whereas instant soups and snacks are forecast to expand at an 7.72% CAGR through 2031.

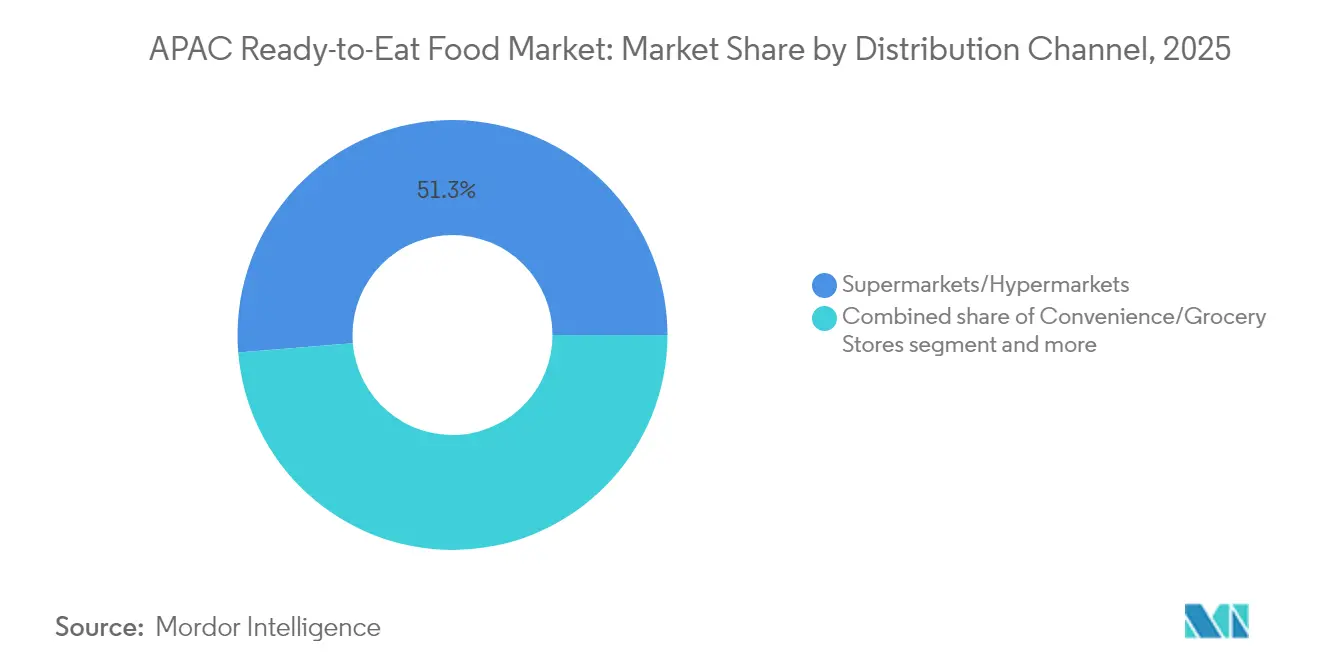

- By distribution channel, supermarkets/hypermarkets accounted for 51.30% of the Asia-Pacific ready-to-eat food market size in 2025, while online retail stores are projected to record the fastest 11.02% CAGR between 2026-2031.

- By geography, China commanded 40.60% of regional sales in 2025, whereas India is set to post the quickest 6.78% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Ready-to-Eat Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of Western diets is encouraging ready-to-eat food adoption | +1.2% | China, India, Southeast Asia | Medium term (2-4 years) |

| Growth in dual-income households is driving demand for time-saving meals | +1.5% | Japan, South Korea, Singapore, major cities | Short term (≤ 2 years) |

| Surge in organic and vegan ready-to-eat food launches boosts its demand | +0.8% | Developed markets, expanding to emerging economies | Long term (≥ 4 years) |

| Product innovation and variety are attracting a broader consumer base | +1.1% | Region-wide tech hubs | Medium term (2-4 years) |

| Busy lifestyles and long working hours are promoting convenient eating habits | +1.3% | Large urban agglomerations | Short term (≤ 2 years) |

| Growth in e-commerce platforms is fueling online ready-to-eat food purchases | +0.9% | China, India, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Popularity of Western Diets Is Encouraging Ready-to-Eat Food Adoption

Urban millennials and Gen Z are increasingly adopting Western meal formats, like single-serve entrées and breakfast bars, into their routines. Exposure to global cuisines through streaming media and travel has heightened demand for diverse flavors in the Asia-Pacific ready-to-eat (RTE) food market. Brands are localizing sauces and seasonings to suit regional tastes while ensuring convenience for time-conscious consumers. Economic growth, urbanization, and globalization in Asia have shifted diets from traditional staples to Western ones, featuring processed sauces, meats, and oils. The rise of dual-income households and longer work hours has boosted demand for quick Western-style meals like pizza and pasta. Local producers are innovating with Western and ethnic fusion RTE products to meet evolving consumer preferences.

Growth in Dual-Income Households Is Driving Demand for Time-Saving Meals

In the Asia-Pacific, the rise of dual-income households is driving demand for quick meal solutions that retain nutrition and taste. In Japan, the Ministry of Internal Affairs and Communications reported 13 million dual-income households in 2024 [1]Source: Ministry of Internal Affairs and Communications Japan, "Finances are tight for dual-income households too", www.soumu.go.jp. This trend is prominent in urban areas, where long commutes and demanding jobs limit time for traditional cooking. Changing gender roles and increased female workforce participation further fuel this demand. Companies are introducing premium ready-to-eat meals, often using locally sourced ingredients and traditional recipes, to rival home-cooked dishes. Consumers are willing to pay a premium for convenient, high-quality options, supported by rising incomes and a shift in cooking perceptions, especially among younger urban professionals.

Surge In Organic and Vegan Ready-To-Eat Food Launches Boosts Its Demand

Health-conscious and environmentally aware consumers are driving demand for organic and plant-based ready-to-eat products. The Asia-Pacific region is a hub for alternative protein innovations, with Singapore leading regulatory advancements by approving cultivated meat for commercial sale since 2020. Initiatives like the '30 by 30' food security program highlight the government's focus on local alternative protein production [2]Source: Good Food Institute Asia Pacific, "State of Play: APAC", www.gfi-apac.org. This approach is influencing countries like Japan, Australia, and South Korea to develop their frameworks for commercialization. Consumer acceptance has expanded beyond vegetarians to include flexitarians and health-conscious individuals, who value these products for their environmental benefits, taste, and convenience. Educated urbanites increasingly associate plant-based diets with a premium lifestyle and social responsibility. Companies are responding with products that replicate traditional meat textures and flavors while emphasizing sustainability and health. This growth is supported by government policies promoting sustainable food systems and significant investments in alternative protein research and development by major food manufacturers.

Product Innovation and Variety Are Attracting a Broader Consumer Base

Advancements in food processing and packaging technologies are driving product innovations, expanding the appeal of ready-to-eat foods to health-conscious individuals, gourmet enthusiasts, and diverse cultural consumers. These innovations include functional ingredients, customizable portions, and advanced packaging technologies that preserve freshness and extend shelf life without artificial preservatives. Companies are using artificial intelligence and consumer data analytics to identify flavor trends and create products that meet evolving tastes. Partnerships between food manufacturers and tech firms are accelerating innovation, such as smart packaging with real-time freshness alerts and cooking instructions. In the Asia-Pacific region, high smartphone usage and digital engagement enable companies to offer food experiences that integrate digital content, cooking tips, and community interaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing health consciousness is limiting the appeal of processed ready-to-eat food | -0.9% | Developed markets, expanding to emerging | Medium term (2-4 years) |

| Concerns over preservatives and additives are affecting consumer trust | -0.7% | Japan, Australia, New Zealand | Long term (≥ 4 years) |

| Inconsistent cold chain logistics hinder product distribution in rural areas | -0.6% | Rural and semi-urban developing markets | Short term (≤ 2 years) |

| Cultural preference for freshly cooked meals reduces ready-to-eat food adoption | -0.8% | Traditional communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Health Consciousness Is Limiting the Appeal of Processed Ready-To-Eat Food

In the Asia-Pacific region, growing health consciousness is challenging traditional ready-to-eat food products, especially those seen as overly processed or less nutritious than fresh options. This trend, driven by access to nutritional information, social media influence, and government health campaigns, emphasizes the link between diet and chronic disease prevention. Consumers now scrutinize ingredient lists, nutritional data, and processing methods, demanding transparency that many traditional products struggle to provide. Products high in sodium, sugar, or artificial ingredients conflict with evolving health standards. Companies are responding by reformulating products, reducing sodium, removing artificial preservatives, and adding functional ingredients like probiotics, fiber, and plant-based proteins. However, reformulation requires significant research and development investment and must balance health-focused branding with taste profiles critical for consumer acceptance.

Concerns Over Preservatives and Additives Are Affecting Consumer Trust

Consumers across the Asia-Pacific are increasingly skeptical of food additives and preservatives due to rising health awareness and food safety concerns amplified by social media. An ASEAN food safety report emphasizes the need for better consumer education and communication to address fears over foodborne illnesses and chemical contaminants. These trust issues challenge ready-to-eat foods, which rely on preservatives and processing aids for longevity and safety standards. Regulatory approaches vary across the region, with some countries tightening labeling requirements and others re-evaluating approved additives. This creates compliance challenges for manufacturers operating in multiple markets. Companies are investing in clean-label formulations and natural preservation methods, but these often increase production costs and may compromise product stability or shelf life. Additionally, many consumers mistakenly view natural compounds as safer than synthetic ones, despite identical chemical structures and safety assurances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready Meals Drive Market Leadership

Ready meals contributed 38.70% of the Asia-Pacific ready-to-eat food market in 2025, reflecting the broad acceptance of full-plate solutions that only require reheating. Packaging innovations, from microwave-ready trays to self-heating pouches, reinforce leadership by offering restaurant-style experiences at home. Instant soups and snacks, though smaller in absolute terms, are on track to post an 7.72% CAGR from 2026 to 2031 as consumers seek nutritious, portion-controlled options for intermittent snacking occasions. Functional enrichments, such as high-protein lentil bases or collagen-fortified broths, give these lines a health halo that resonates strongly with young professionals and fitness enthusiasts across the Asia-Pacific ready-to-eat food market.

The diversification of cereals and breakfast bars aligns with the increasing demand driven by early-morning time constraints. Premium breakfast SKUs now incorporate organic oats, reduced sugar, and probiotic infusions, enabling higher average selling prices and maintaining strong profit margins. Baked goods continue to gain traction by leveraging localized flavors, such as pandan-flavored cakes in Southeast Asia and matcha sponge rolls in Japan. In contrast, meat-based ready meals face growing environmental scrutiny, prompting processors to adopt hybrid meat-plant formulations.

By Distribution Channel: Digital Transformation Reshapes Retail

Although supermarkets and hypermarkets held 51.30% share of the Asia-Pacific ready-to-eat food market in 2025, footfall patterns continue to fragment. Shoppers still value in-store product inspection and family-sized bulk deals, yet the convenience of app-based ordering is eroding brick-and-mortar exclusivity. Online outlets are forecast to expand at an 11.02% CAGR to 2031, powered by fast-growing mobile payments and improved logistics. The Asia-Pacific ready-to-eat food industry now treats live-inventory visibility, same-day shipping, and temperature guarantees as standard features rather than add-ons.

Convenience stores flourish in bustling neighborhoods, providing late-night access, handpicked snack selections, and microwave stations for on-the-spot consumption. Specialty retailers, typically emphasizing organic or ethnic products, leverage brand storytelling and sampling events to validate their premium pricing. Newer avenues, such as smart vending machines and pantry contracts at workplaces, not only boost volume but also enhance consumer engagement, solidifying the Asia-Pacific ready-to-eat food market's foothold in daily life.

Geography Analysis

China holds a dominant 40.60% share in the Asia-Pacific ready-to-eat food market. The rapid growth of e-commerce platforms, with food categories experiencing double-digit expansion, is driving online adoption. Government initiatives, including incentives for manufacturing parks and stricter safety regulations, are enhancing supply chain reliability and boosting consumer confidence. Additionally, consumer preferences are becoming increasingly diverse.

India, anticipated to grow at a 6.78% CAGR through 2031, is leveraging PLISFPI funding of INR 10,900 crore to strengthen its ready-to-cook and ready-to-eat segments . The expanding middle-income population and increasing smartphone penetration are raising awareness of these categories. Meanwhile, hyper-local flavors, such as masala khichdi bowls and millet-based upma, ensure cultural relevance. Investments in state-level infrastructure, including road networks and cold storage facilities, are further driving the Asia-Pacific ready-to-eat food market in semi-urban areas, where modern retail formats are still developing.

Japan and South Korea represent mature markets. In South Korea, the growing number of single-person households is fueling demand for microwave-ready meals designed for individual servings. In Southeast Asia, Thailand is balancing strong domestic sales with significant export activity, creating opportunities for both local and imported products. Australia and Singapore, characterized by higher per-capita incomes and stringent labeling standards, are witnessing a shift toward premium, health-focused product offerings.

Regulatory Landscape

Food-safety compliance for ready-to-eat (RTE) foods across Asia-Pacific is increasingly framed around microbiological criteria, with country-specific limits shaping formulation, thermal processes, and cold-chain controls. Singapore Food Agency (SFA) sets microbiological limits for RTE foods, while Thailand's Ministry of Public Health Notification No. 416 lays out product-specific requirements such as non-detection of Salmonella spp. in 25 g and defined limits for organisms including Staphylococcus aureus for certain RTE categories (for example, sushi and salads). In Australia and New Zealand, Food Standards Australia New Zealand (FSANZ) updated microbiological requirements in 2025, including risk-based distinctions for Listeria monocytogenes in RTE foods based on growth potential, which raises the bar for HACCP design, environmental monitoring, and shelf-life validation for manufacturers selling across multiple markets.

Regional coordination is also becoming more visible. In June 2026, South Korea's Ministry of Food and Drug Safety (MFDS) and the Asia-Pacific Food Regulatory Authority Summit (APFRAS) advanced regulatory harmonisation through the APFRAS Seoul 2026 Declaration, pointing toward more aligned approaches on food safety controls that can reduce technical friction for cross-border RTE trade. Alongside safety standards, market access requirements such as Indonesia's halal certification mandate (with phased enforcement and an October 2026 coverage goal for non-exempt products) add another compliance layer for multi-country portfolios, affecting ingredient sourcing, co-manufacturing choices, and packaging and label governance.

Competitive Landscape

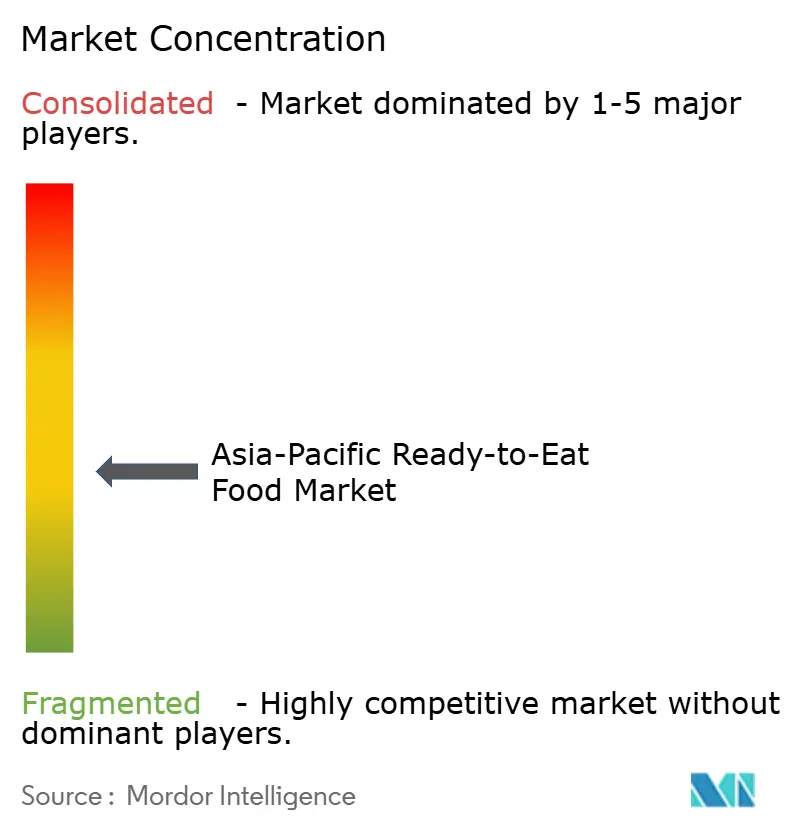

The Asia-Pacific ready-to-eat food market features a moderate fragmentation, with numerous domestic and multinational players vying for a larger share of the market. The key players are adopting strategic approaches such as mergers, acquisitions, partnerships, and expansions, as well as focusing on new product development to enhance their brand presence among consumers. The leading companies dominating the regional market include PepsiCo Inc., Nestlé SA, Kellanova, Pondok Abang, and Unilever PLC, among others. Further, the companies have been introducing new and innovative products with the inclusion of naturally derived ingredients so as to make their product unique from the existing products. Owing to the rapidly developing nature of the market, new product innovation has become the most commonly used strategy, as it helps in understanding the changing needs of the consumers in the market.

Investment in infrastructure is a decisive differentiator. Companies with integrated cold-chain assets shorten lead times and cut spoilage, critical for protein-rich ready dishes. Thailand's CP Foods, for instance, has expanded its RTE portfolio through vertically integrated supply chains across Southeast Asia, aligning with local consumption patterns while ensuring freshness. In China, domestic leaders partner with e-commerce giants to leverage real-time analytics for micro-segmented campaigns that reduce stock-outs.

Sustainability narratives shape competitive positioning. Producers race to adopt recyclable trays, mono-material pouches, and renewable-energy processing plants that align with corporate ESG commitments and tightening regulations. Technology collaborations are multiplying: food tech startups contribute AI-driven sensory mapping, while packaging suppliers offer oxygen-scavenger films that prolong shelf life without synthetic preservatives. These alliances keep the Asia-Pacific ready-to-eat food market in constant innovation mode while raising the barrier for late entrants.

Asia-Pacific Ready-to-Eat Food Industry Leaders

-

PepsiCo Inc.

-

Pondok Abang

-

Nestlé S.A.

-

Unilever PLC

-

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity build-out and capability upgrades across key Asia-Pacific markets create room for ready-to-eat portfolios that combine convenience with health-led positioning and tighter safety controls. In the Philippines, Bounty Fresh announced in June 2026 an investment of PHP 800 million in a new food manufacturing facility in Concepcion, Tarlac, aimed at increasing output for convenience food products, reinforcing local supply responsiveness for chilled and processed meal solutions. Japan has also seen manufacturing reinforcement tied to prepared foods, with CJ Foods commissioning a new mandu production plant in Chiba Prefecture (operations launched in 2025), supporting stable supply of frozen and heat-and-eat formats for modern retail and foodservice.

Portfolio expansion through corporate moves and brand scaling highlights opportunities in better-for-you, protein-forward, and quick-commerce compatible RTE items. In June 2026, Danone announced the acquisition of Australia's MADE Group to expand its health-focused offering in the region, while in Malaysia, Malayan Flour Mills introduced a protein-rich microwaveable RTE range developed at its Dindings Poultry Processing facility, reflecting investment in product formats that suit urban consumption occasions. Funding into brands designed for rapid distribution models also adds whitespace for RTE penetration in online channels: Moi Soi raised an institutional round in May 2026 to scale ready-to-eat curries through quick commerce and modern trade. These moves build on ongoing regulatory alignment efforts (for example, APFRAS activity led by MFDS in 2026) that encourage manufacturers to standardize safety systems and labeling governance across markets, supporting the feasibility of multi-country launches and cross-border e-commerce assortments.

Recent Industry Developments

- July 2026: Suntory PepsiCo Vietnam Beverage inaugurated a USD 300 million manufacturing plant in Tay Ninh Province, described as its largest facility in PepsiCo's Asian network and designed for 1.24 billion liters of annual capacity. The scale-up strengthens local and export supply for packaged convenience beverages that often sit alongside ready-to-eat food baskets in modern retail and e-commerce. The investment also reinforces high-throughput, efficient manufacturing in Southeast Asia, supporting broader cold-chain and last-mile ecosystems used by RTE players.

- May 2026: PepsiCo announced a INR 5,700 crore investment plan in India through 2030 to expand snacks and beverage manufacturing capacity via greenfield and brownfield projects in states including Madhya Pradesh, Assam, and Tamil Nadu. Expanded local production supports wider availability of packaged, on-the-go food and snack items that compete for the same convenience occasions as RTE meals and instant snacks. The commitment also signals continued channel push in modern trade and digital commerce where RTE categories are accelerating.

- July 2024: Sevenoaks Foods, an Australian startup, launched a ready-to-eat meals range for kids positioned around no artificial colors and flavors, reduced salt, and no added sugars. The launch underscores product development momentum around clean-label and child-friendly nutrition claims, which has become a key differentiation lever for RTE brands facing health-conscious scrutiny. It also broadens category participation beyond adult convenience, supporting household penetration through family-oriented formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Asia-Pacific ready-to-eat food market is defined as packaged foods that are consumed without further cooking, and that are bought through retail and online channels across Asia-Pacific countries.

Scope exclusions: Freshly prepared food sold loose through restaurants, canteens, and street stalls is excluded from this market sizing.

Segmentation Overview

-

By Product Type

- Instant Breakfast/Cereals

- Instant Soups and Snacks

- Ready Meals

- Baked Goods

- Meat Products

- Other Product Types

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Speciality Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, align country coverage, and build realistic guardrails for consumption and pricing. We referred to public statistics and reference documents such as national statistics offices in Asia-Pacific countries, UN Comtrade trade data, FAO food balance sheets, World Bank macro indicators, and OECD consumer and retail datasets (where available).

Along with that, annual reports, investor presentations, and press releases were reviewed to understand product mix shifts, channel expansion, and pricing actions that can move the market value. Where needed, we also used paid subscriptions for company financials and intelligence, plus news and financials, to cross-check timelines and reported revenue pools. The sources listed above are illustrative and not exhaustive, and many other public documents and data points were also referred to for collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of packaged foods is truly ready-to-eat in each country, and how sales split across modern trade, convenience, and online. We spoke with a mix of manufacturers, distributors, retailers, and category specialists across APAC so gaps left by public data could be filled and key assumptions could be confirmed with practical market context.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | |

| Mid tier: 49% | Functional/Unit leaders: 42% | |

| Smaller Players: 16% | Managers: 45% |

Market-Sizing & Forecasting

Sizing is built using the top-down and bottom-up combination, where packaged food consumption and retail sales signals are reconstructed at the country level, and then filtered to the ready-to-eat definition before rolling up to the Asia-Pacific total. To keep totals realistic, results are corroborated with selective bottom-up approximations like sampled average price per pack multiplied by estimated volumes for major formats, followed by channel checks from distributors and retailers.

Key inputs used in the model include packaged food retail value trends, urban population and working-age population growth, penetration of convenience retail and e-commerce, observed price movement for packaged foods, and cold chain and shelf-stable format expansion that affects availability. When country data is incomplete, nearby country patterns and conservative ranges from interviews are applied, and then tightened through review so the roll-up does not overstate smaller markets.

Forecasts are produced using scenario analysis supported by near-term indicators such as inflation, income growth, and channel expansion expectations discussed in primary calls. Once demand and pricing paths are set for each country, the regional forecast is aggregated and checked for realistic year-to-year movement.

Data Validation & Update Cycle

Outputs are checked against independent signals such as packaged food trade flows, retail sales trends, and publicly visible pricing shifts, and then any large variance is investigated before sign-off. If a country total looks out of line, assumptions are re-tested, and follow-up calls are triggered to confirm whether the issue is scope, pricing, or channel coverage.

A multi-step analyst review is used so that model formulas, country roll-ups, and currency conversion logic are consistent. The report is refreshed annually, and interim updates are made when material events occur, such as sharp inflation changes or major channel disruptions. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Asia Pacific Ready to Eat Food Market Size Measured Against Other Published Estimates

Published numbers for this market often differ because firms draw the ready-to-eat product scope differently, choose different base years, and apply different pricing and currency assumptions. Differences also come from whether the estimate is built from retail value signals, from selective category additions, or from broader convenience food definitions.

Country-level retail sales signals and pack-price tracking, followed by channel mix validation for modern trade, convenience, and online, are the evidence that links Mordor Intelligence to a packaged, no-further-cooking scope that totals USD 227.54 B in 2025. Gaps usually show up when adjacent packaged foods that still need preparation are counted, when a narrower product list is used, or when a faster price ramp is applied without reconciling it with inflation and pack-size shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 227.54 B (2025) | |

| Regional Consultancy A | USD 183.67 B (2024) | Uses a different base year and appears to apply a narrower ready-to-eat basket, which can reduce the total when rolled up across APAC countries and channels. |

| Trade Research Group B | USD 37.73 B (2024) | Shows a much tighter counted universe, likely limiting included categories and end-use pool, which materially compresses the value compared with a full packaged RTE aggregation. |

The table indicates that scope and base-year alignment are the two biggest drivers behind the spread in values. When category inclusion, channel coverage, and price assumptions are stated clearly, the final number becomes easier to reconcile and repeat across annual refreshes.

Key Questions Answered in the Report

What is the current value of the Asia-Pacific ready-to-eat food market?

The Asia-Pacific ready-to-eat food market size is USD 240.08 billion in 2026 and is projected to reach USD 313.99 billion by 2031.

Which product segment leads regional revenue?

Ready meals hold the top position, accounting for 38.70% of 2025 sales across the Asia-Pacific ready-to-eat food market.

How fast is online retail expanding in this space?

Online channels are forecast to grow at an 11.02% CAGR from 2026-2031, the fastest among all distribution modes.

Which country is the fastest-growing market?

India is expected to register a 6.78% CAGR through 2031, benefiting from government incentives and rising urban incomes.

Page last updated on: