Masterbatch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.94 Billion |

| Market Size (2031) | USD 16.18 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

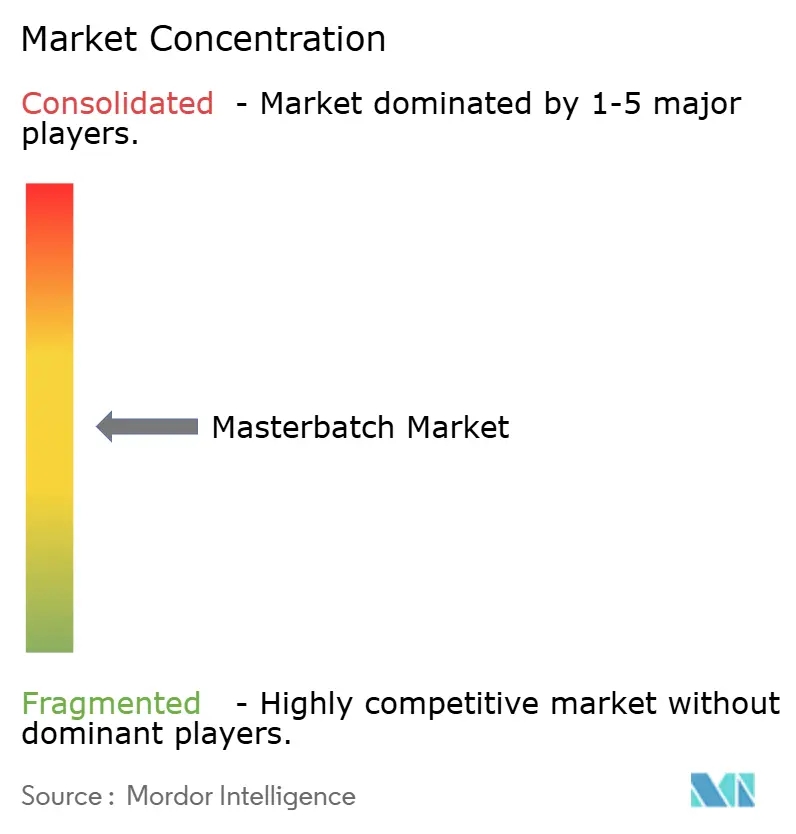

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Masterbatch Market Analysis by Mordor Intelligence

The Masterbatch Market size is projected to be USD 12.41 billion in 2025, USD 12.94 billion in 2026, and reach USD 16.18 billion by 2031, growing at a CAGR of 4.57% from 2026 to 2031. Cost volatility in titanium-dioxide feedstocks, new PFAS disclosure mandates, and the need for recyclate-compatible colorants are reshaping purchasing criteria for polymer processors. White concentrates remain the volume anchor because opacity is indispensable in flexible packaging, healthcare devices, and agricultural films. At the same time, demand for color variants is accelerating as brand owners lean on visual differentiation to defend shelf space in saturated consumer-goods categories. Processors are also prioritizing shorter lead times, which favors suppliers with local compounding assets in Asia Pacific and India.

Key Report Takeaways

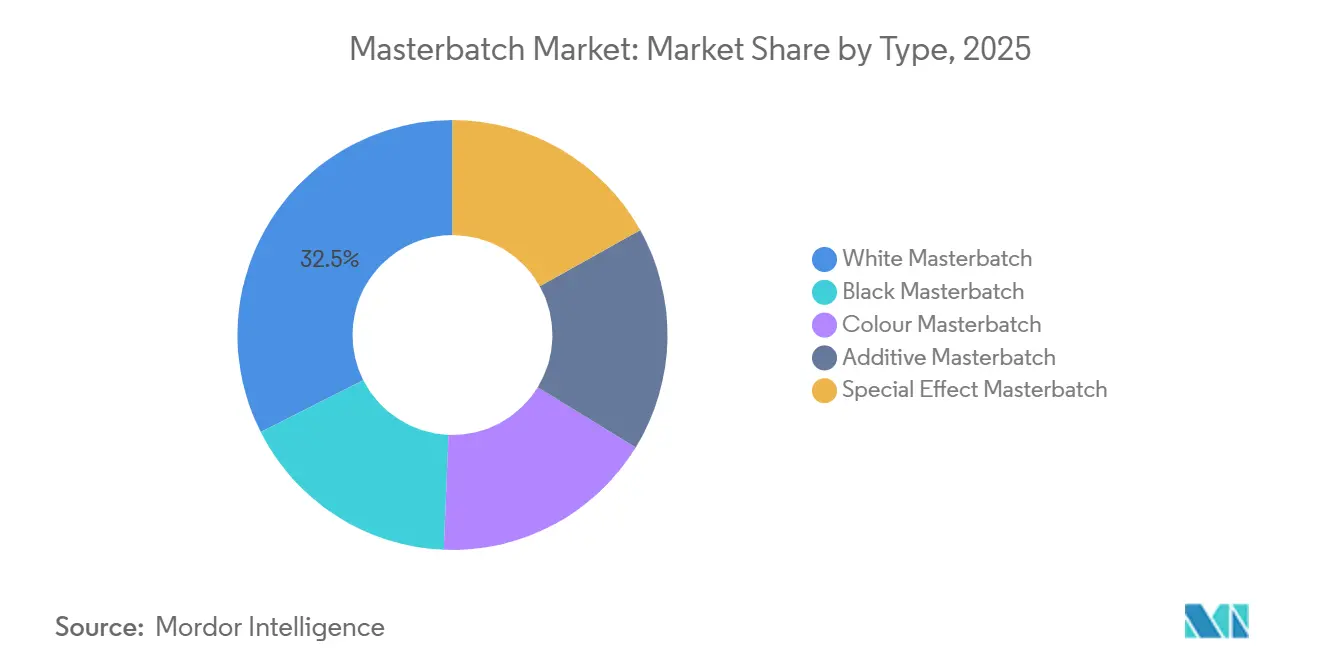

- By type, white formulations led with 32.45% of masterbatch market share in 2025; color grades are projected to accelerate at a 4.89% CAGR to 2031.

- By polymer carrier, polyethylene held 42.56% of revenue in 2025, while polypropylene is poised for the fastest 5.18% CAGR through 2031.

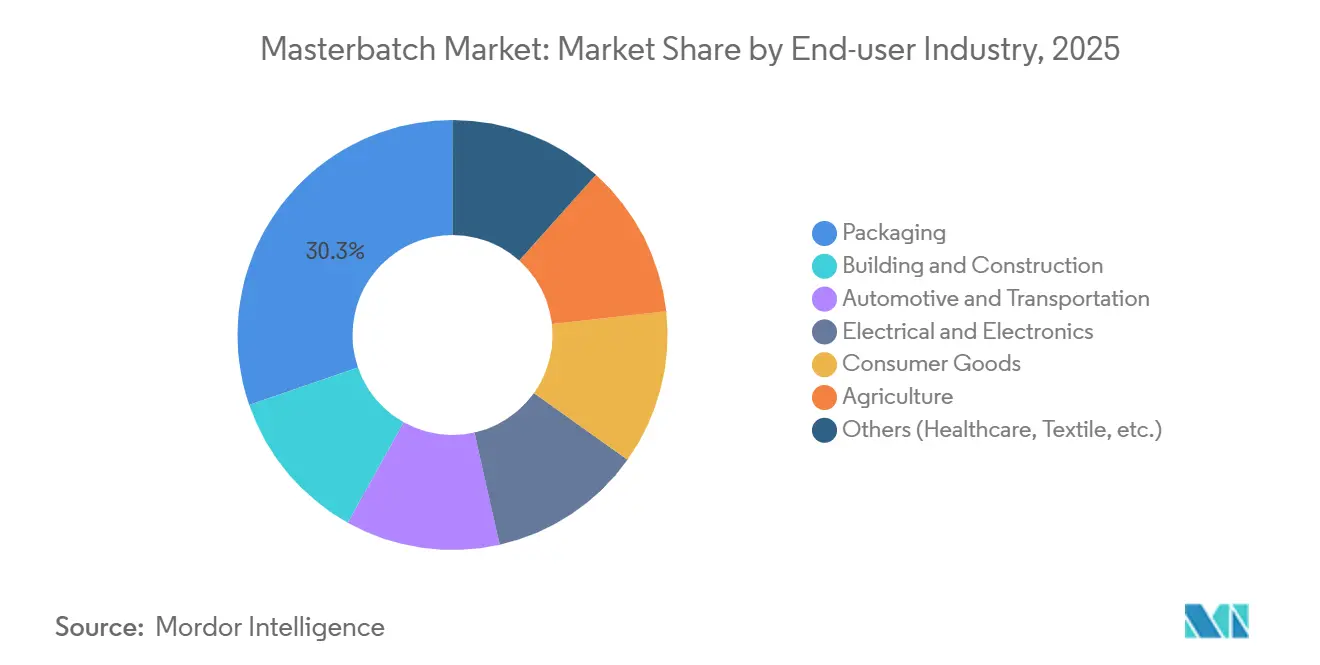

- By end-user, packaging commanded 30.28% of 2025 sales; automotive & transportation is forecast to rise at a 5.22% CAGR during the outlook period.

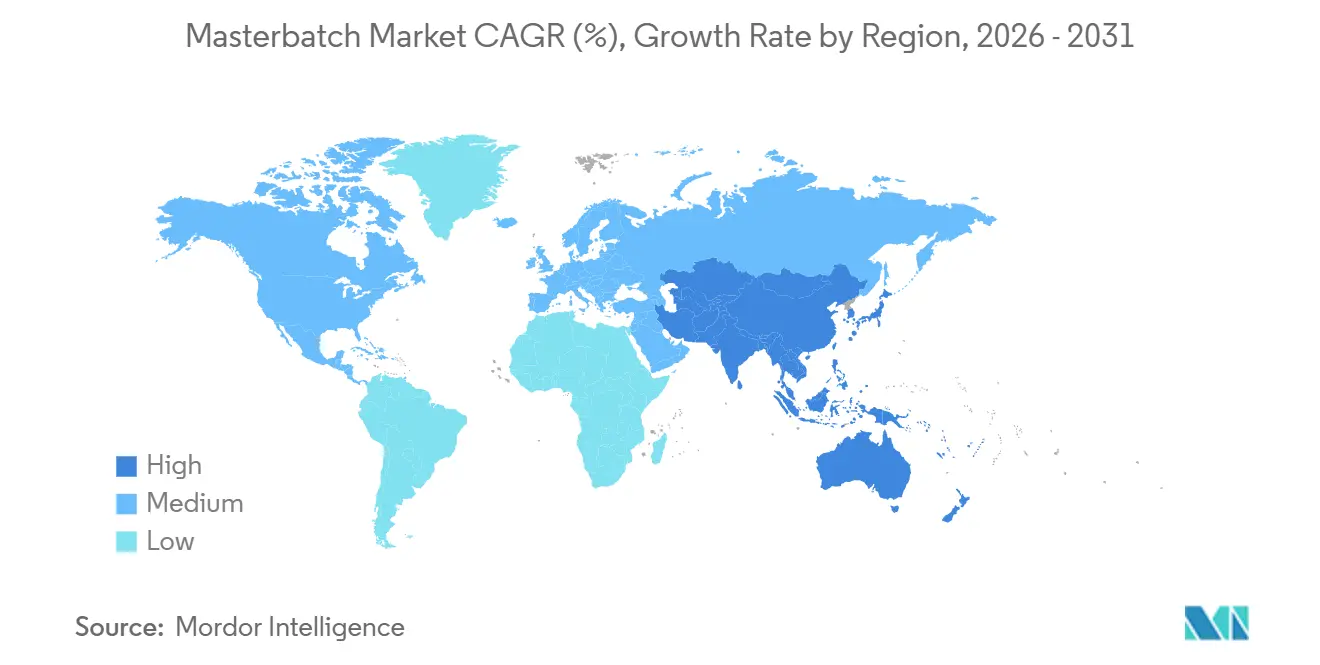

- By region, Asia Pacific captured 45.32% of the masterbatch market size in 2025 and is expanding at a 5.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Masterbatch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand in Plastic Packaging Industry | +1.2% | Global with focus on Asia Pacific and North America | Medium term (2-4 years) |

| Increasing Demand of Plastic in Automotive Industry | +1.1% | North America, Europe, China, India, South Korea | Medium term (2-4 years) |

| Shift Toward Lightweight Recyclate-Rich PP Compounds | +0.9% | Europe with spill-over to North America | Long term (≥4 years) |

| Fiber-Optic Cable Infrastructure Build-out | +0.7% | India, ASEAN, Middle East | Short term (≤2 years) |

| Increased Use in Healthcare and Hygiene Products | +0.6% | Global, early gains in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand in Plastic Packaging Industry

Global plastic packaging output touched 146 million metric tons in 2023, and flexible formats accounted for 38% of that volume. Masterbatch suppliers, supported by growth in the masterbatch market, are formulating concentrates that disperse uniformly at let-down ratios as low as 1:50, helping converters thin film gauges without sacrificing opacity. Mono-material structures now dominate new product launches because they improve recycling sortability, which lifts white-concentrate usage in polyethylene laminates. The US FDA and EU regulators still require migration testing for every colorant-resin pair, elongating commercialization timelines by up to six months. Regional penetration varies; Asia Pacific’s surge in organized retail has doubled flexible-packaging volumes since 2019 and is expanding faster than North America.

Increasing Demand of Plastic in Automotive Industry

Electric-vehicle platforms are driving polypropylene adoption in battery enclosures, door panels, and cluster housings, where every kilogram of weight removed extends driving range. General Motors’ Ultium modules use glass-fiber-reinforced polypropylene colored with heat-stabilized concentrates that survive 150°C continuous exposure. BMW’s iX seats incorporate recycled polypropylene, requiring colorants capable of masking the gray tint of post-consumer resin. Darker OEM color palettes double concentrate loading per kilogram of parts, lifting revenue per vehicle. Tier-1 suppliers in China’s Yangtze River Delta and India’s Chennai-Bangalore corridor have cut delivery windows to 24 hours, demanding local compounding. EU rules that mandate 25% recycled content in new cars by 2030 further underpin demand for advanced masterbatch, reinforcing long-term growth prospects for the masterbatch market.

Shift Toward Lightweight Recyclate-Rich PP Compounds

Europe’s updated Packaging and Packaging Waste Regulation sets a 30% recycled-content target by 2030, forcing colorant reformulation for hue stability in blends containing up to 50% post-consumer polypropylene. Borealis’ Borcycle grades illustrate technical feasibility yet carry a 15-25% premium over virgin substitutes. Avient’s ReVive compounds meet EU food-contact standards but remain supply-constrained, limiting immediate penetration. Mechanical-recycling stream variability pushes concentrate chemistries toward broader processing windows and higher thermal stability. Upcoming digital product-passport requirements will track recycled content, raising traceability costs for smaller compounders.

Fiber-Optic Cable Infrastructure Build-out

India’s fiber-optic cable revenue is forecast to climb from USD 1.28 billion in 2023 to USD 3.36 billion by 2033 at a 10.2% CAGR, stimulating demand for low-smoke-zero-halogen masterbatch that meets IEC 60332-3 standards and supporting growth in the masterbatch market. Color-coded sheathing enables rapid field identification of fiber counts while maintaining flexibility at –40°C for aerial deployment. Vietnam targets 120,000 km of new fiber by 2025, adding an estimated 18,000 metric tons of polyethylene compound requirement. Saudi Arabia’s Vision 2030 networks are spurring Gulf demand, favoring suppliers with regional plants that avoid import duties. Inorganic pigments dominate formulations because their lightfastness prevents misidentification after prolonged UV exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ & Carbon-Black Feedstock Prices | –0.8% | Asia Pacific and Europe | Short term (≤2 years) |

| Competition from Liquid Colorant Systems | –0.5% | North America and Europe | Medium term (2-4 years) |

| PFAS Disclosure Rules Forcing Reformulations | –0.4% | United States and European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ & Carbon-Black Feedstock Prices

Ilmenite mine shutdowns in Tamil Nadu triggered an 18% surge in titanium-dioxide prices during 1H 2024. Carbon black followed the opposite arc when Chinese tire output slowed in early 2026, creating unpredictable cost swings. Four global TiO₂ suppliers dominate capacity, so any force majeure spikes spot prices by up to 25% within a quarter. Backward-integrated concentrate makers preserve a 200-300 bp margin advantage versus toll compounders, but only firms above USD 500 million revenue can fund such assets. Persistent volatility encourages converters to test liquid-colorant alternatives that carry lower inventory risk.

Competition from Liquid Colorant Systems

Gravimetric dosing cuts injection-molding color-change downtime from 45 minutes to under 10 minutes, offsetting a 10-15% higher kilogram cost. Short-run molders in North America and Europe, therefore, prefer liquid systems that also trim working capital by 30-40%. Technical limitations above 280°C and in fiber-reinforced compounds keep masterbatch dominant in high-temperature or structural parts, sustaining demand across the masterbatch market. Film extrusion, blow molding, and rotomolding still favor solid concentrates because color consistency outweighs changeover speed. As liquid suppliers enhance heat stability, the performance gap narrows, intensifying competitive stress for masterbatch producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: White Masterbatch Leads, Color Variants Gain on Brand Differentiation

White grades accounted for 32.45% of the masterbatch market share in 2025 and remain irreplaceable because a single percentage point of titanium dioxide yields hiding power equal to 8–10 points of calcium carbonate. Color variants are set to log the fastest 4.89% CAGR to 2031 as retailers demand differentiated shelves. Hybrid formulations that combine inorganic and organic pigments lower exposure to titanium dioxide price spikes without compromising opacity. Black concentrates benefit from carbon black’s dual role as pigment and UV stabilizer, extending the service life of agricultural films in tropical climates from 18 months to 36 months. Additive masterbatch is gaining traction in circular-economy applications because slip agents, antioxidants, and compatibilizers can be combined in a single pellet, simplifying inventories for converters.

White grades continue to dominate thin-gauge film, blow-molded bottles, and healthcare devices, but special-effect variants are creating high-margin pockets in automotive interiors and consumer electronics, expanding value opportunities within the masterbatch market. Metallic and pearlescent effects command 20–30% premiums over solid colors, giving compounders pricing latitude despite feedstock inflation. Regulatory oversight is tight in food-contact uses where the EU positive list restricts pigment choices, lengthening approval cycles to up to three years. Suppliers with pre-cleared portfolios therefore win faster commercialization slots, consolidating share among large players in this functional niche.

By Polymer: Polyethylene Dominates, Polypropylene Accelerates on Automotive Lightweighting

Polyethylene represented 42.56% of the masterbatch market size in 2025 because of its ubiquity across film extrusion, blow molding, and rotomolding. Loading rates run 2–5%, depending on opacity and color depth. Polypropylene is projected to outpace other polymers with a 5.18% CAGR through 2031 due to electric-vehicle lightweighting and hot-fill packaging that demands higher heat-deflection temperatures. High-impact polystyrene still serves appliance housings but is ceding share to polypropylene as price gaps narrow.

PVC masterbatch remains vital for construction items such as window profiles and conduit, where lead-free stabilizers extend 50-year warranties. Yet EU sustainability policy flags PVC for potential restriction, making the long-term outlook uncertain. PET masterbatch is a specialized pocket confined to beverage bottles and thermoformed trays requiring intrinsic viscosity above 0.80 dL/g. Across polymers, ISO 1133 melt-flow testing ensures concentrate compatibility before converters commit to commercial runs.

By End-User: Packaging Leads, Automotive Surges on EV Platform Adoption

Packaging held 30.28% of 2025 revenue, spanning flexible films, rigid containers, and closures that need barrier protection and visual branding. Developers align masterbatch chemistries with mono-material designs to satisfy recycling mandates without sacrificing product integrity, supporting innovation across the masterbatch market. Electric-vehicle adoption pushes automotive demand to a 5.22% CAGR, with every kilogram of weight saved adding 0.15–0.20 km of range. Colorants compatible with recycled polypropylene hide natural discoloration in post-consumer streams, preserving interior aesthetics.

Building and construction uses weatherable concentrates in pipes, siding, and geomembranes that must survive 20–30 years of outdoor exposure. Electrical and electronics segments specify flame-retardant grades that meet UL 94 V-0 without halogens. Healthcare and hygiene applications, though smaller, command premium pricing due to ISO 10993 and ISO 13485 traceability. Agriculture gains efficiencies when black concentrates loaded at more than 2.5% extend mulch-film lifetimes across multiple crop cycles.

Geography Analysis

Asia Pacific generated 45.32% of 2025 revenue and is projected to grow at a 5.08% CAGR through 2031. China dominates on the back of vertically integrated petrochemical complexes that locate resin, pigment, and masterbatch production within a single industrial park, trimming delivered costs by up to 20%. India follows with 6.5% annual growth, lifted by automotive output, retail-ready flexible packaging, and infrastructure projects that consume colored pipes and conduit. Japan and South Korea contribute higher value per kilogram despite flat volumes because electronics OEMs specify antistatic and flame-retardant masterbatch for 5G devices. Regulatory diversity across ASEAN challenges rapid product rollout, giving an edge to suppliers with in-country labs that can localize formulas to each national list of permitted additives.

In North America, the US masterbatch market anchors demand in e-commerce packaging, automotive lightweighting, and medical-device molding, but PFAS rules inflate R&D costs for local compounders. Canada’s volume ties to auto assembly in Ontario, while Mexico’s maquiladora sector lifts consumption in appliances and electronics. FDA food-contact and UL flame-rating approvals add six to 18 months to commercialization, encouraging early supplier engagement.

Europe’s revenue, propelled by stringent circular-economy targets that make recyclate-ready colorants a must-have. Germany leads with high-performance automotive applications while the United Kingdom navigates dual compliance regimes post-Brexit. France and Italy leverage premium consumer-goods categories to grow demand for special-effect pigments. High energy prices remain a headwind, yet EU green-funding incentives partly offset input-cost pressure.

South America’s share, led by Brazil where automotive builds, agricultural films, and food packaging consume most output. Argentina’s volatile currency caps growth, but Mercosur food-contact rules still oblige local testing. In the Middle East and Africa, Saudi Arabia benefits from SABIC’s vertical integration, while GCC infrastructure initiatives boost demand for low-smoke-zero-halogen cable compounds. South Africa supplies regional export markets despite pigment import dependence and double-digit tariffs on finished concentrates.

Mordor Intelligence provides coverage of the masterbatch market across other key regional markets. Detailed country-level analysis extends to Mexico incorporating local coverage and market participation, as required.

Competitive Landscape

The masterbatch industry features moderate fragmentation. Portfolio premiumization is a common thread as suppliers launch bio-attributed and recyclate-compatible grades that fetch 15-25% premiums over virgin-based concentrates. Backward integration into pigment dispersion hedges raw-material swings and secures 200-300 bp extra margin, but the capital required limits this play to firms above USD 500 million in revenue. Mid-tier specialists gain ground by offering 48-hour color-match services and regional stock points that multinationals struggle to replicate without bloating working capital.

Masterbatch Industry Leaders

Cabot Corporation

Clariant

Ampacet Corporation

Avient Corporation

Plastika Kritis S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Ampacet Corporation broadened its ELTech portfolio, introducing high-performance color masterbatches. These masterbatches, crafted from a polybutylene terephthalate (PBT) carrier resin, are tailored for PBT jacketing in optical fiber cables. The ELTech masterbatches not only ensure superior signal transmission for optical fiber cables but also boast impressive opacity.

- May 2024: LyondellBasell Industries Holdings B.V. unveiled its latest innovation: Polybatch Effects FROST masterbatches. These masterbatches give PET packaging a chic matte frost finish, offered in two unique styles. To elevate the aesthetic further, Polybatch Effects FROST can effortlessly blend with a spectrum of colors, crafting a refined and upscale appearance.

Global Masterbatch Market Report Scope

Masterbatch (MB) is a solid plastic additive used to color polymers or give them other qualities. It is a concentrated mixture of pigments and/or additives contained in a carrier resin, and then cooled and chopped into a granular shape using a heat process.

The masterbatch market is segmented by type, polymer, end-user industry, and geography. By type, the market is segmented into white masterbatch, black masterbatch, color masterbatch, additive masterbatch, and special effect masterbatch. By polymer, the market is segmented into polypropylene, polyethylene, high-impact polystyrene, polyvinyl chloride, polyethylene terephthalate, and others. By end-user, the market is segmented into agriculture, building & construction, automotive and transportation, electric and electronics, packaging, and others. The report also covers the market size and forecasts for the masterbatch market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| White Masterbatch |

| Black Masterbatch |

| Colour Masterbatch |

| Additive Masterbatch |

| Special Effect Masterbatch |

| Polyethylene |

| Polypropylene |

| High Impact Polystyrene |

| Polyvinyl Chloride |

| Polyethylene Terephthalate |

| Packaging |

| Building and Construction |

| Automotive and Transportation |

| Electrical and Electronics |

| Consumer Goods |

| Agriculture |

| Others (Healthcare, Textile, etc.) |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | White Masterbatch | |

| Black Masterbatch | ||

| Colour Masterbatch | ||

| Additive Masterbatch | ||

| Special Effect Masterbatch | ||

| By Polymer | Polyethylene | |

| Polypropylene | ||

| High Impact Polystyrene | ||

| Polyvinyl Chloride | ||

| Polyethylene Terephthalate | ||

| By End-User | Packaging | |

| Building and Construction | ||

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Consumer Goods | ||

| Agriculture | ||

| Others (Healthcare, Textile, etc.) | ||

| By Geography | Asia Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for the masterbatch market between 2026 and 2031?

The market is forecast to grow at 4.57% CAGR over the period and reach USD 16.18 billion by 2031.

Which polymer base is expanding fastest for masterbatch usage?

Polypropylene is projected to rise at a 5.18% CAGR owing to electric-vehicle lightweighting.

Why is Asia Pacific the leading revenue contributor?

Integrated petrochemical hubs in China and rapid automotive and packaging growth in India push Asia Pacific to 45.32% revenue share.

How are PFAS regulations affecting product development?

US and EU disclosure and restriction rules are forcing costly reformulations that can delay launches by up to nine months.

Which segment shows the highest growth within end-users?

Automotive and transportation lead with a projected 5.22% CAGR as EV platforms adopt recyclate-rich polypropylene compounds.

Page last updated on: