Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

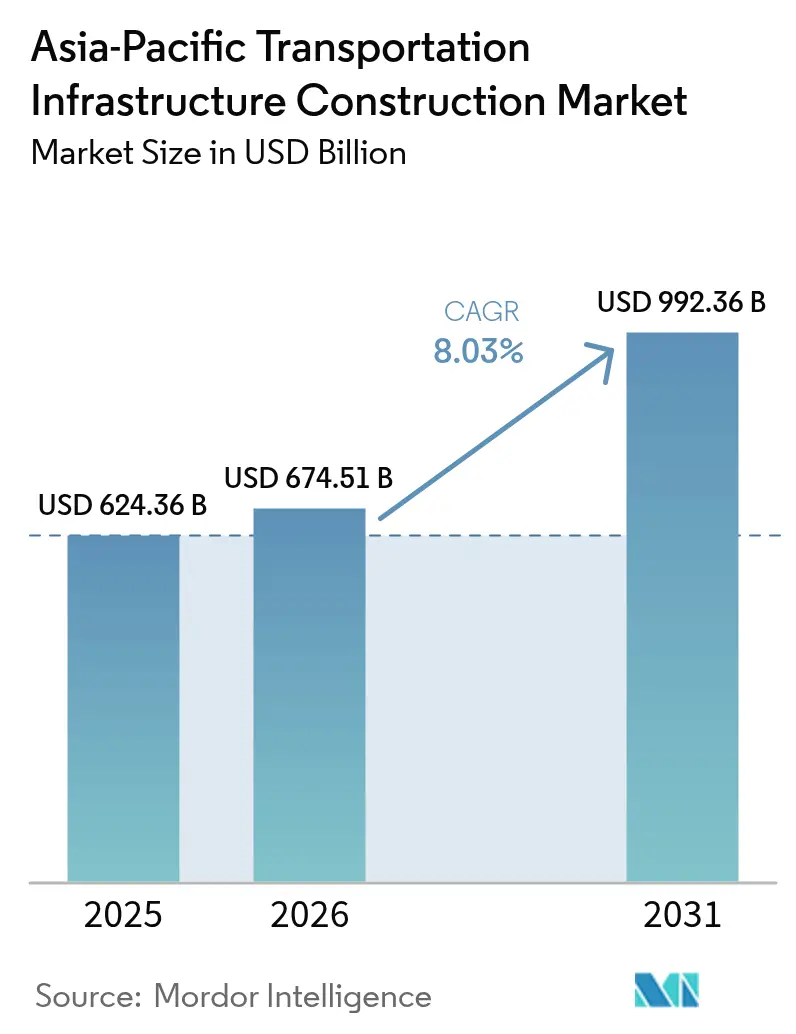

| Base Year Market Size (2025) | USD 624.36 Billion |

| Market Size (2026) | USD 674.51 Billion |

| Market Size (2031) | USD 992.36 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

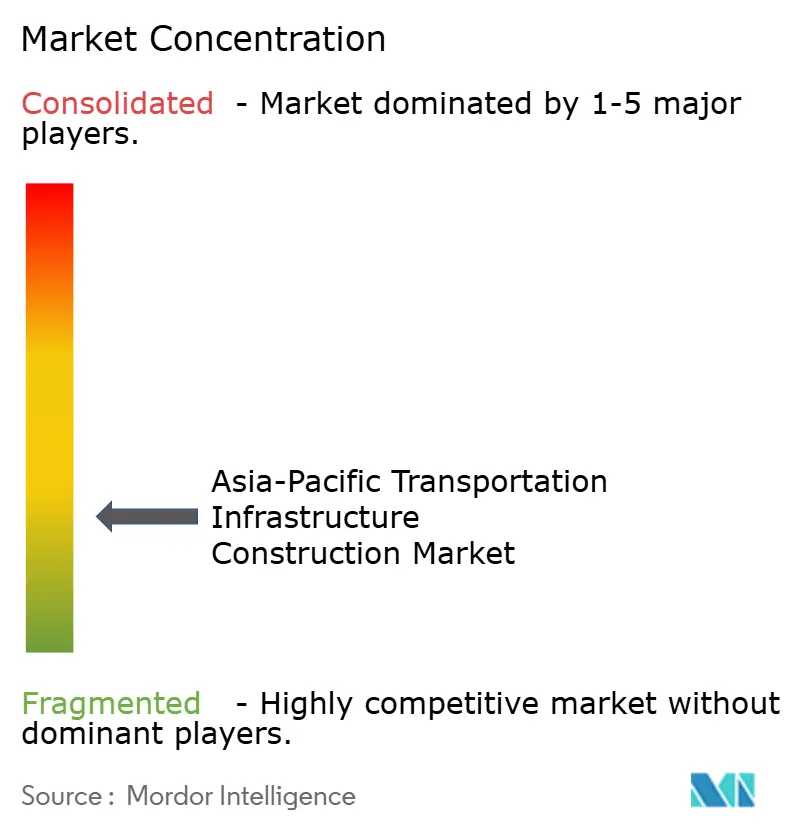

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

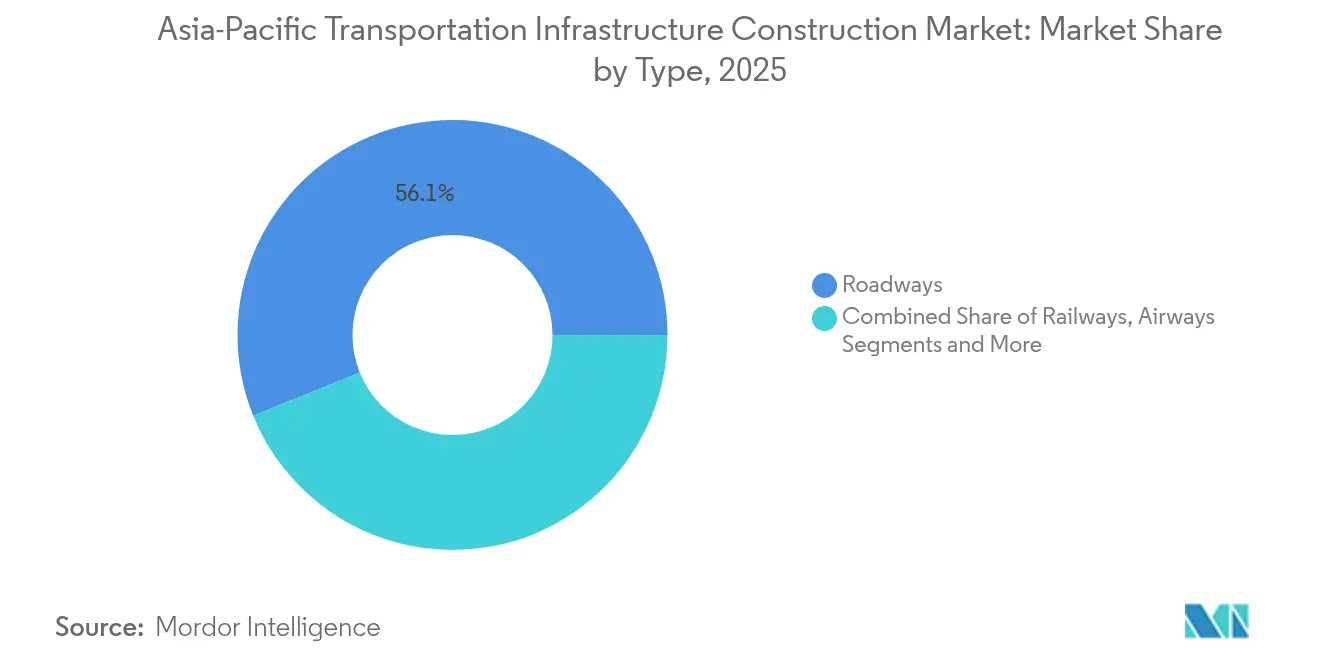

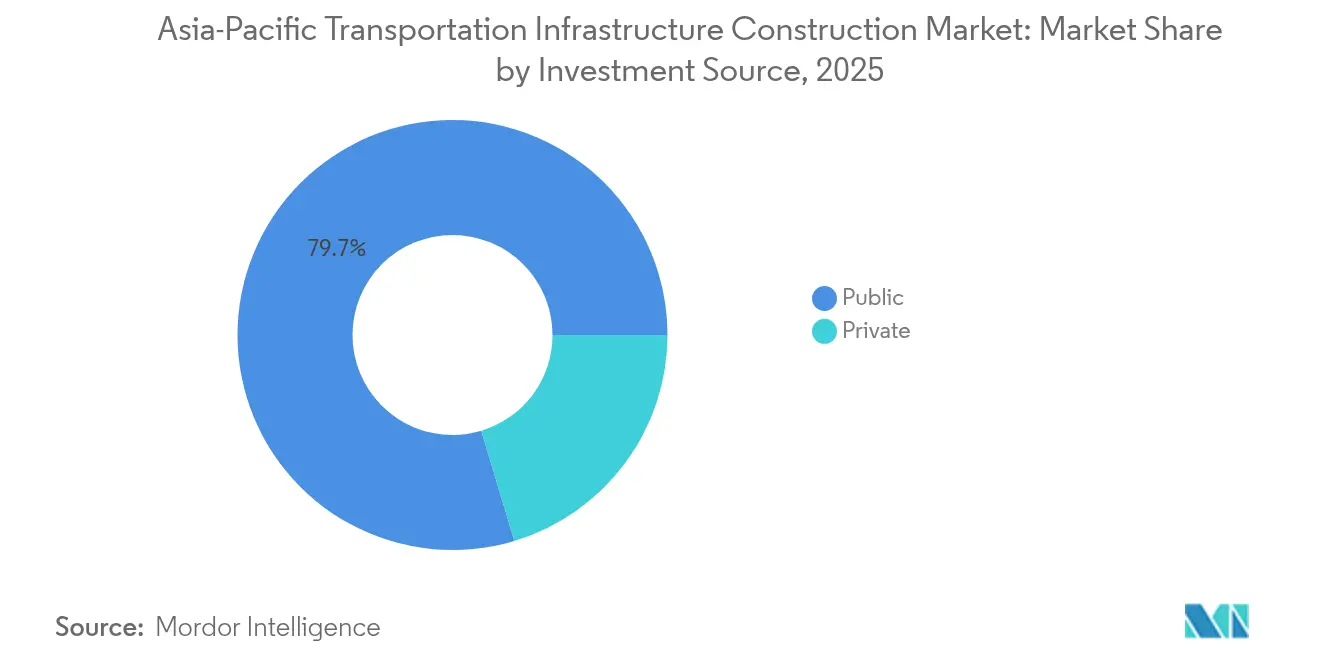

The Asia-Pacific Transportation Infrastructure Construction Market size is expected to grow from USD 624.36 billion in 2025 to USD 674.51 billion in 2026 and is forecast to reach USD 992.36 billion by 2031 at 8.03% CAGR over 2026-2031. Governments across the region view road, rail, port, and airport programs as instruments to unlock export competitiveness, secure energy-transition goals, and de-risk supply chains. Roadways retained the largest 2024 slice at 56.7% share, yet railways now lead headline growth as electrification and high-speed corridors undercut short-haul aviation economics. India’s 10.41% CAGR forecast underscores how a coordinated National Infrastructure Pipeline, metro build-outs, and new airports are transforming voter expectations and developer pipelines. Private capital is growing faster than budgetary outlays because public-private partnership templates in India, Thailand, and Australia reduce diligence time and allocate risk more predictably. Competitive intensity is rising as Chinese state-owned majors bid aggressively on cross-border megaprojects while local champions in India, Japan, and Southeast Asia protect niches that reward tunneling skill, seismic retrofits, and automation expertise,.

Key Report Takeaways

- By transport mode, roadways led with 56.12% revenue share in 2025; railways are forecast to expand at a 8.83% CAGR through 2031.

- By construction type, new builds accounted for 69.35% of the Asia Pacific transport infrastructure construction market share in 2025, while renovation is advancing at a 9.05% CAGR to 2031.

- By investment source, public funding controlled 79.65% of the Asia Pacific transport infrastructure construction market size in 2025; private capital records the highest projected CAGR at 9.52% to 2031.

- By country, China commanded 39.25% of 2025 value; India posts the fastest growth at 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and megacity growth | +2.3% | India, Indonesia, Philippines, Vietnam (Mumbai, Jakarta, Manila, Ho Chi Minh City) | Medium term (2-4 years) |

| Regional trade and logistics corridors | +1.9% | China, ASEAN core (Thailand, Vietnam, Malaysia) plus South Asia spill-over via BRI | Long term (≥ 4 years) |

| Government stimulus and PPP maturation | +2.1% | Pan-APAC with near-term traction in India, Thailand, Australia, Philippines | Short term (≤ 2 years) |

| Decarbonization and rail electrification | +1.5% | India, China, Japan, South Korea, Australia | Medium term (2-4 years) |

| Airport capacity and smart-port upgrades | +1.2% | India, Southeast Asia (Thailand, Philippines, Indonesia) plus China coastal hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization And Megacity Growth Requiring Metros, BRT And Commuter Rail

Megacity expansion is rewriting urban mobility economics. India’s Mumbai–Ahmedabad high-speed rail, now under phased construction, will cut end-to-end travel to under three hours and effectively merge two labor markets. Jakarta’s planned capital in Kalimantan embeds a 50-kilometer metro and green-field airport, demonstrating how spatial relocation sidesteps legacy congestion FT.COM. Seoul’s Great Train eXpress adds three orbital lines that promise 30-minute trips from satellite towns, spurring higher-density housing. These systems share electric or hybrid rolling stock that aligns with decarbonization pledges while lowering life-cycle costs. Collectively, they anchor the 2.3% positive swing in regional CAGR by shifting commuter preference from private cars to rail-based mass transit.

Regional Trade And Logistics Corridors To Boost Connectivity

Policy makers now treat inland rail, deep-water ports, and multi-lane highways as geopolitical hedges rather than pure freight plays. Pakistan’s USD 10 billion ML-1 upgrade links Karachi to the Afghan frontier under China’s Belt and Road Initiative and gives Central Asia a maritime alternative. Indonesia’s Patimban Port, partially opened in 2024, eases pressure on Jakarta’s Tanjung Priok by focusing on auto and electronics exports. Thailand’s Bangkok–Kunming high-speed rail underscores ASEAN’s bid to compete with ocean lanes by offering faster land delivery. Vietnam approved a USD 67 billion Hanoi–Ho Chi Minh City line that blends passenger and light-freight capacity. These corridors accommodate dual-use logistics, shaping supply-chain security and adding 1.9% to growth prospects[1]World Bank Transport Team, “Philippines Urban Transport Improvement,” World Bank, worldbank.org.

Government Stimulus And PPP Models Unlocking Multi-Year Pipelines

Fiscal stimulus continues but is now paired with structured PPP templates that balance sovereign guarantees with commercial equity. The Asian Development Bank injected USD 500 million into India’s metro and highway roster in 2024, catalyzing co-investment by domestic insurers ADB.ORG. Thailand reserved 40% of its USD 76 billion stimulus for PPP-ready schemes, signaling a definitive pivot away from pure budget procurement. Australia’s 2024 budget ties any project above USD 330 million to a private-finance screening process, accelerating deal flow. The Philippines secured an initial USD 30 million World Bank loan to fund pre-feasibility studies, smoothing the path to larger debt placements. These—and similar—actions contribute a 2.1% uplift to the regional CAGR by shortening financial close cycles.

Decarbonization: Rail Electrification, Low-Carbon Mobility And Charging Infrastructure

Environmental mandates have moved from strategy decks to contract specifications. India electrified 95% of its broad-gauge network by late 2024, trimming diesel use and operating costs by up to a quarter. Indonesia’s Jakarta–Bandung bullet train is powered by a renewables-rich Java grid, serving as a low-carbon template for Vietnam’s pending high-speed corridor. Japan’s Chuo Shinkansen maglev recovers energy during braking and aims for 30% lower emissions than the current rolling stock. Australia integrates electric-vehicle charging at Inland Rail rest stops, anticipating shared passenger–freight networks. This pervasive design shift lifts regional growth by 1.5% as projects are future-proofed for zero-emission mobility.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Funding gaps and higher interest costs | -1.4% | APAC-wide, acute in India, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Land acquisition, permits and resettlement delays | -0.9% | India, Indonesia, Philippines, Malaysia | Medium term (2-4 years) |

| Complex geology, climate risk and skilled-labor shortages | -0.7% | Southeast Asia, Japan seismic zones, Australia remote corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Funding Gaps And Higher Interest Rates Straining Capex And PPP Bankability

Tighter monetary policy erodes debt headroom and pushes required project yields above historical toll and fare trajectories. Concessions penciled at 4% interest now chase equity at yields topping 7%, stalling bids on Indian highways and Philippine metros. Indonesia’s USD 33 billion capital-move pipeline has attracted less than one-fifth of the planned private stake, forcing upfront public spend and scope deferrals. The National Infrastructure Pipeline in India similarly sees slower private lane uptake due to forex and traffic volatility. These financing gaps subtract 1.4% from regional growth until borrowing costs stabilize and tariff formulas adopt inflation indexation.

Land Acquisition, Environmental Approvals And Resettlement Delays Extending Timelines

Protracted clearances routinely add 18-24 months and inflate budgets. Gujarat farmers delayed the Mumbai–Ahmedabad bullet train despite revised compensation packages that ballooned by 30%. Indigenous groups in Indonesia’s Trans-Sumatra corridor withheld the right-of-way without community upgrades, pausing works. Malaysia’s East Coast Rail Link was rerouted after environmental lobbying, generating a USD 1 billion cost add-on. Judicial challenges against Japan’s maglev line cite groundwater risks and continue to drag on tunnel permits. These frictions reduce CAGR by 0.9% through schedule overruns and interest-during-construction accrual.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Railways Accelerate As Electrification Reshapes Modal Economics

Railways captured 8.83% forecast CAGR, the fastest within the Asia Pacific transport infrastructure construction market, even though roadways retained 56.12% share in 2025. India’s near-total rail electrification lowered fuel costs by a quarter, making rail freight the low-carbon option for bulk commodities. Indonesia’s 2024 opening of the Jakarta–Bandung line validated renewable-powered traction that Vietnam is now formatting for its north-south high-speed plan. Beyond cost, high-speed networks integrate labor markets, as evident from Japan’s continuing maglev investment. The Asia Pacific transport infrastructure construction market size for rail projects is therefore projected to compound fast enough to surpass USD 233.4 billion by 2031, should current pipelines reach financial close.

Airports and seaports follow with moderate CAGRs, powered by tourism recovery and export re-shoring. Singapore’s automated Tuas Port and Changi’s biometric terminals illustrate how turnaround speed now rivals capacity as the primary performance metric. China’s 60 automated container terminals baseline a regional shift toward 5G-connected cranes and driverless yard trucks. Upskilling requirements for air-side automation tilt contract awards toward firms with systems-integration capacity rather than pure civil capabilities. Overall, modal competition is no longer about lane kilometers or berth length alone; it revolves around energy efficiency, digital integration, and resiliency against climate disruptions.

By Construction Type: Renovation Gains As Aging Assets Require Smart Upgrades

New construction held a 69.35% share of the Asia Pacific transport infrastructure construction market in 2025, reflecting a still-wide network gap in emerging economies. Yet renovation is growing at a 9.05% CAGR, faster than greenfield builds, because Japan, South Korea, and Australia must retrofit 1970s-era expressways and bridges for seismic or climate resilience. Japan commits around USD 15 billion through 2030 to seismic upgrades, while South Korea overhauls highways with congestion-based tolling that demands sensor-rich gantries and cloud analytics. Australia’s Inland Rail blends new track and legacy upgrades to double-stack freight, revealing an integrated design logic.

Renovation projects are increasingly capital-intensive; adding smart tolling or real-time structural health monitoring can lift per-lane costs above historical new-road benchmarks. Contractors able to stage works without full closures—through prefabricated bridge segments or modular signaling—win premium margins. As these projects demand both civil and digital engineering, consortia now include software vendors, cybersecurity firms, and telecom providers. This capability mix pushes renovation toward a roughly one-third share of total spend by 2031, shifting procurement criteria from lowest price to lifecycle value.

By Investment Source: Private Capital Expands As PPP Structures Mature

Public funds still financed 79.65% of 2025 outlays, yet private investment climbs at 9.52% CAGR, the highest rate among capital sources, as clearer PPP guidelines improve bankability. The Asian Development Bank’s USD 500 million facility for Indian metros catalyzed pension-fund coinvestors, while Thailand earmarked USD 30 billion of its stimulus for concession-ready schemes. Australia insists that projects exceeding USD 330 million screen for private finance, expanding the investable universe.

A new hybrid PPP archetype blends multilateral concessional debt, sovereign guarantees, and inflation-indexed tariffs, shrinking completion-risk premiums. International sponsors such as VINCI and ACS bid not just on build contracts but lifetime concessions, including operations, digital upgrades, and commercial real-estate tie-ins. Consequently, the Asia Pacific transport infrastructure construction market size funded by private capital may crest USD 193.2 billion by 2031 if the current trajectory holds. Private investors are not replacing public money; they magnify fiscal reach by underwriting construction and operating risk over extended periods.

Geography Analysis

China’s dominance, with a 39.25% 2025 share, stems from more than 170,000 kilometers of expressways and the world’s densest high-speed rail grid, yet future growth moderates as priorities move from capacity to automation, asset health monitoring, and carbon reduction. Automated container ports in Qingdao and Tianjin trim vessel dwell times and provide a template for Southeast Asian hubs that now court transshipment volume. Belt and Road ventures such as Pakistan’s ML-1 and Thailand’s Bangkok–Vientiane link export surplus civil-works capacity to neighboring markets, sustaining revenue for Chinese SOEs even as domestic builds plateau.

India delivers the fastest 10.02% CAGR on the back of a broad policy pivot that treats infrastructure delivery as a political KPI. The Mumbai–Ahmedabad corridor, 20-million-passenger Navi Mumbai Airport, and multi-city metro build-outs display a new normal where mega-projects become campaign milestones. Domestic engineering houses like Larsen & Toubro, Dilip Buildcon and IRCON upgrade tunneling, signaling and O&M proficiency to match international benchmarks, ensuring local capture of value as project count accelerates.

Japan and South Korea keep growth moderate but high-value through Maglev, Great Train eXpress, and Incheon Airport expansions. Here, precision engineering, seismic resilience, and digital integration gain premium pricing. Australia, though smaller, embodies a strategic freight pivot: Inland Rail and Western Sydney Airport link resource basins to coastal export nodes while incorporating EV charging and hydrogen readiness. Indonesia’s Kalimantan move redistributes economic gravity within the archipelago and generates contiguous packages—such as Patimban Port extensions—that international contractors pursue with blended finance. Across Malaysia, Vietnam, the Philippines, and Thailand, ASEAN corridors knit resource provinces to export zones, helping secondary cities leapfrog infrastructure gaps through jointly funded expressways, airports, and rail spurs.

Competitive Landscape

Competitive power rests with a handful of Chinese SOEs—China State Construction Engineering, China Railway Construction, and China Communications Construction—that together controlled roughly 30%-35% of 2024 regional revenue. Their integrated engineering-procurement-construction chains and access to policy bank loans create cost advantages that are hard to match. Yet their market position is not unassailable. Indian majors like Larsen & Toubro prove competitive on complex metro tunneling after delivering the USD 3 billion Mumbai Metro Line 3 entirely underground while managing utility relocation beneath dense neighborhoods. Japanese conglomerates Obayashi, Kajima, and Shimizu secure airport and seismic-retrofit jobs where precision and quality command higher margins, a domain less sensitive to price competition.

Second-tier contenders differentiate via technology and financial structuring. Gamuda Berhad and Italian-Thai Development deploy modular viaduct construction and automation to slash on-site labor in Malaysia and Thailand. VINCI Construction Grands Projets, ACS, and Ferrovial leverage European PPP experience to structure airport and highway concessions that bundle O&M, retail, and real-estate monetization. Regional private equity funds now back mid-cap contractors that specialize in digital twin deployment and structural health monitoring, positioning them as partners for renovation-heavy pipelines.

Strategic moves illustrate the shifting landscape. China State Construction Engineering’s USD 4.5 billion Cairo monorail win extends its urban-rail turnkey offer globally. Hyundai Engineering & Construction’s USD 2.1 billion Saudi highway underscores how Asian builders chase Middle-East diversification to counter domestic slowdowns. Samsung C&T’s USD 300 million automation push into robotic rebar tying and 3D concrete printing targets productivity gains in labor-scarce markets. As renovation and smart-overlay projects rise, firms with systems-integration, cybersecurity, and data-analytics skills command premiums, tilting future rankings toward capability over sheer balance-sheet heft.

Asia-Pacific Transportation Infrastructure Construction Industry Leaders

China State Construction Engineering Corporation Ltd.

China Railway Construction Corporation

China Communications construction company Ltd.

Hyundai Engineering & Construction

OBAYASHI CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Navi Mumbai International Airport commenced operations with 20 million annual seats, deploying biometric gates and automated baggage to halve turnaround time.

- December 2024: Larsen & Toubro finished tunneling for the USD 3 billion Mumbai Metro Line 3, demonstrating advanced urban-shield tunneling under live utilities.

- November 2024: China State Construction Engineering secured a USD 4.5 billion monorail contract in Cairo that includes 15-year O&M rights.

- October 2024: Indonesia’s USD 12 billion Trans-Sumatra toll road reached 70% completion, with freight times projected to fall 40% once finalized.

Asia-Pacific Transportation Infrastructure Construction Market Report Scope

Transportation infrastructure is the system of public works that makes it easier for people to move around.Roads, railways, ports, and airports are all part of it. A complete background analysis of the Asia Pacific Transportation Infrastructure Construction Market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is covered in the report.

The Asia Pacific Transportation Infrastructure Construction Market is segmented by mode (roads, railways, airways, and waterways) and country (China, India, Vietnam, Japan, South Korea, Indonesia, Thailand, and the Rest of Asia-Pacific). The report offers market size and forecast values (in USD) for all the above segments.

By Type

| Roadways |

| Railways |

| Airways |

| Ports and Inland Waterways |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Rest of Asia-Pacific |

| By Type | Roadways |

| Railways | |

| Airways | |

| Ports and Inland Waterways | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific transport infrastructure construction market in 2026?

It is valued at USD 674.51 billion in 2026 and is forecast to hit USD 992.36 billion by 2031.

Which country will grow fastest through 2031?

India leads with a projected 10.02% CAGR, anchored by its National Infrastructure Pipeline and multiple metro and airport projects.

What is the role of private capital in upcoming projects?

Private investment grows at 9.52% CAGR because mature PPP frameworks blend multilateral debt, sovereign guarantees and indexed tariffs to reduce risk.

Why are railways gaining momentum over roadways?

Aggressive electrification, high-speed corridors and lower operating costs drive a 8.83% CAGR for rail projects, shifting freight and commuters from roads.

What are the main risks facing developers?

Higher interest rates, land-acquisition delays and skilled-labor shortages can add up to 1.4% negative impact on CAGR and extend timelines by up to two years.

Which technologies define next-generation transport assets?

Automation, 5G-enabled port cranes, biometric airport processing, modular construction and digital twins for asset monitoring are becoming standard across the region.

Page last updated on: