Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Cold Chain Logistics Market Analysis by Mordor Intelligence

The UAE Cold Chain Logistics Market size was valued at USD 1.65 billion in 2025 and is estimated to grow from USD 1.83 billion in 2026 to reach USD 2.43 billion by 2031, at a CAGR of 5.84% during the forecast period (2026-2031).

Growth is anchored in the country’s pivot to food security and pharmaceutical resilience, which is turning the logistics base into a regional platform rather than only a destination. Strategic operators in the UAE cold chain logistics market are shifting from commodity warehousing toward value-added handling to improve margins and service depth. A stronger focus on multi-temperature urban nodes supports e-grocery and healthcare flows that need fast cycle times. Infrastructure programs in ports, free zones, and integrated industrial cities are also improving multimodal options that favor compliant and time-definite cold movements.

Key Report Takeaways

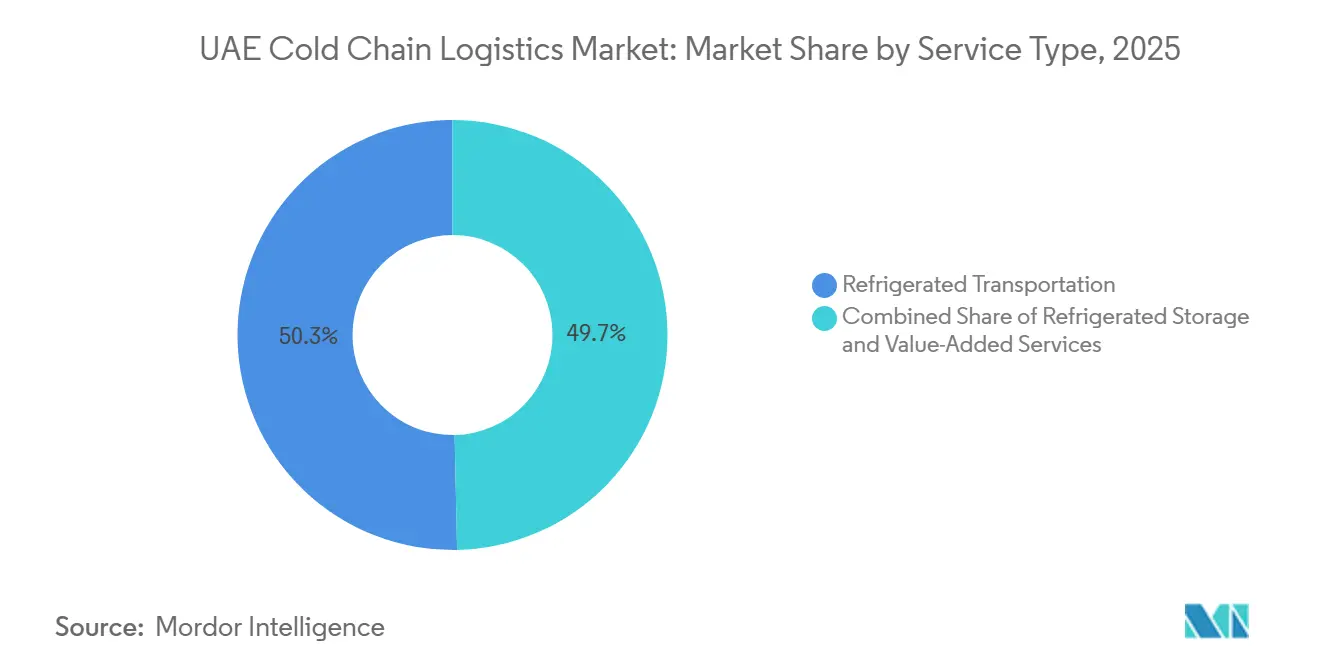

- By service type, refrigerated storage led with 50.34% of the UAE cold chain logistics market share in 2025, while value-added services are projected to expand at a 4.76% CAGR through 2026-2031.

- By temperature type, chilled cargo accounted for a 39.54% share of the UAE cold chain logistics market size in 2025, and frozen is advancing at a 5.43% CAGR through 2026-2031.

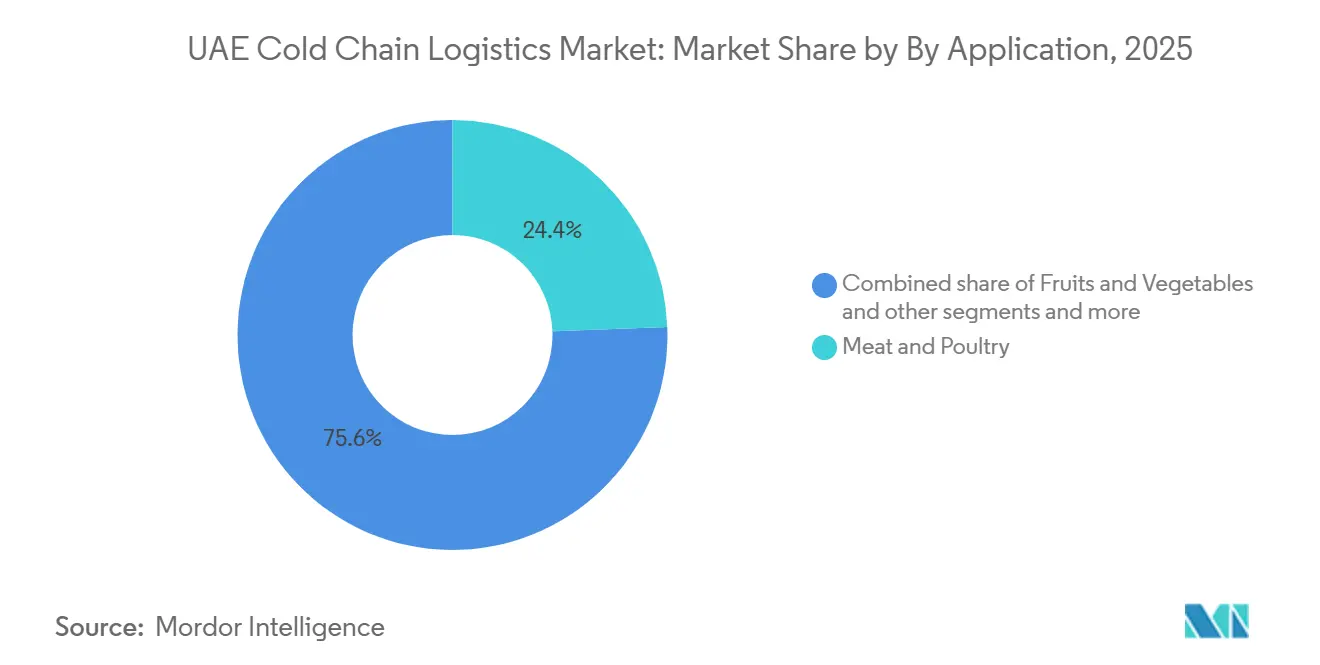

- By application, meat and poultry accounted for a 24.41% share of the UAE cold chain logistics market size in 2025, while vaccines and clinical-trial materials are set to grow at a 6.21% CAGR through 2026-2031.

- By geography, Dubai accounted for 32.60% of the UAE cold chain logistics market share in 2025 and is projected to advance at a 5.78% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth in E-Commerce Grocery and Frozen Food Delivery | + 1.2% | Dubai primary, Sharjah secondary, Abu Dhabi emerging | Medium term (2-4 years) |

| UAE Food Security Strategy Accelerating Domestic Cold Storage Capacity | + 1.5% | National, with KEZAD and Dubai South as focal points | Long term (≥ 4 years) |

| Expansion of Halal-Certified Cold Supply Chain Networks | + 0.8% | Global re-export corridors via Jebel Ali, secondary impact in Abu Dhabi | Medium term (2-4 years) |

| Growth of Vaccine and Biologics Distribution Across the GCC | + 1.1% | Abu Dhabi core (KEZAD hub), Dubai Jebel Ali air gateway | Long term (≥ 4 years) |

| Development of Agri-Tech and Hydroponic Farming Logistics | + 0.4% | Dubai Food Tech Valley, Northern Emirates expansion | Long term (≥ 4 years) |

| Investment in Solar-Powered Cold Warehousing Facilities | + 0.6% | National, with early gains in Dubai Logistics City and Al Ghuwaifat rail terminal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in E-Commerce Grocery and Frozen Food Delivery

Online grocery and quick-commerce models are compressing delivery windows and repositioning inventory closer to dense residential clusters where short-haul velocity is essential. This shift is moving network design away from large single-site warehouses toward micro-fulfillment hubs that combine chilled, frozen, and ambient zones within short drive times. Operators in the UAE cold chain logistics market are using multi-temperature cross-docks and predictive demand tools to improve slotting and reduce out-of-stocks on fast-turn SKUs. Connected fleets with real-time temperature telemetry and route optimization reduce transit excursions and improve compliance with critical control points across delivery loops. Emirate-level compliance programs that emphasize continuous temperature logging and corrective-action triggers are accelerating investments in IoT sensors and integrated cold-vehicle controls. As these capabilities expand, frozen assortment depth is becoming a hedge against last-mile delays, which supports service reliability and reduces write-offs.

UAE Food Security Strategy: Accelerating Domestic Cold Storage Capacity

The National Food Security Strategy 2051 emphasizes resilient supplies and domestic capacity, driving investments in cold warehouses and distribution nodes in industrial zones linked to ports and airports. KEZAD Group is investing AED 621 million to deliver 250,000 square meters of cold storage by 2025, supporting re-exports and inland distribution, equal to USD 169.1 million using the AED 2025 average conversion rate. Government targets, such as 90 days of reserves, highlight the strategic role of temperature-controlled reserves and accelerate site selection on inland plots near highways and rail corridors.[1]Government of the UAE, “National Food Security Strategy 2051,” Government of the UAE, u.ae Free-zone frameworks with bonded options and streamlined licensing enable the UAE cold chain logistics market to integrate import staging with GCC re-distribution, reducing dwell time and improving freshness across retail and foodservice.

Expansion of Halal-Certified Cold Supply Chain Networks

Halal logistics protocols ensure storage segregation, verified handling, and dedicated equipment to prevent cross-contamination. Operators are adding separate chambers, docks, and racking to meet audits, supporting meat and poultry flows requiring end-to-end integrity. RSA Cold Chain’s Jebel Ali Free Zone facility, launched in September 2025, adds multi-temperature bonded and non-bonded capacity with ISO 22000 and HACCP certifications, positioning Dubai as a compliant staging point for regional halal corridors. Network orchestration isolating halal lots through cross-docking and delivery improves audit outcomes and shipper confidence. The UAE cold chain logistics market benefits from this specialization, opening access to large GCC and Southeast Asian markets governed by halal standards.

Growth of Vaccine and Biologics Distribution Across the GCC

Pharmaceuticals and biologics require qualified storage, validated packaging, and controlled handling from tarmac to warehouse and into last-mile distribution. Abu Dhabi’s Department of Health launched a regional vaccine distribution hub in July 2025 at KEZAD, operated by Rafed, a PureHealth subsidiary, with design capacity and processes that accommodate more than 20 vaccine types and scale for new platforms.[2]Department of Health – Abu Dhabi, “Abu Dhabi Launches Operations at its Regional Vaccine Distribution Hub,” Department of Health – Abu Dhabi, doh.gov.ae This hub leverages air cargo networks that are certified for temperature-sensitive healthcare cargo and integrates with CEIV Pharma-compliant routes. Emirates SkyCargo enhanced this corridor by adding Liege in January 2026 with five weekly freighter flights and reported a significant 2025 uplift in pharma throughput, which signals carrier-level commitment to biologics traffic. The UAE cold chain logistics market is building depth in pharma-grade infrastructure in Abu Dhabi and Dubai, which consolidates higher value shipments and raises the compliance bar for competitors.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme Climate Conditions Increasing Refrigeration Load Costs | - 0.9% | National, acute in outdoor handling at Jebel Ali and Dubai World Central | Short term (≤ 2 years) |

| Heavy Dependence on Imported Perishable Goods | - 0.3% | National, concentrated demand in Dubai and Abu Dhabi urban centers | Long term (≥ 4 years) |

| Limited Last-Mile Cold Chain Capabilities Outside Major Emirates | - 0.5% | Ras Al Khaimah, Fujairah, rural Ajman, moderate gaps in Sharjah outskirts | Medium term (2-4 years) |

| High Maintenance Costs for Advanced Cooling Systems | - 0.7% | National, higher in industrial zones including KEZAD, Jebel Ali, and Dubai South | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extreme Climate Conditions Increasing Refrigeration Load Costs

High summer temperatures and humidity increase refrigeration loads in deep-freeze and chilled storage, which raises energy spend as a share of operating expenses. Facilities that lack modern plant controls or efficient refrigerants are more exposed to this cost pressure. Operators are responding with ammonia-based systems, better insulation, and predictive controls that modulate compressor cycles against door activity and ambient heat ingress. Sites with rooftop solar and smart demand management reduce peak tariffs and cushion volatility in energy pricing. The UAE cold chain logistics market is defining competitiveness partly through energy performance, since lower consumption per pallet processed improves margins without sacrificing service levels. This performance gap is expected to widen as regulatory frameworks on emissions and energy efficiency gain traction.

Heavy Dependence on Imported Perishable Goods

The UAE’s consumption profile relies on imports of fruits, vegetables, meat, and specialty items, which makes cold logistics sensitive to upstream disruptions and freight timing. Import dependence creates a cascading risk profile that includes currency swings, origin weather shocks, and route disruptions. Strategic stockpiles and distributed storage nodes reduce these vulnerabilities by spreading inventory and shortening last-mile routes. National policy on food security seeks to stabilize supply through a capacity that can maintain reserve levels under stress. The UAE cold chain logistics market is therefore balancing import staging with inland capacity that supports resilience objectives while improving service reliability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Dominates Yet Services Layer Gains Strategic Premium

Refrigerated storage captured 50.34% in 2025 across large-format facilities positioned in free zones and logistics districts that serve as regional nodes for importers and distributors. Value-added services are the fastest-growing at a 4.76% CAGR through 2031, reflecting a shift toward kitting, labeling, and customs-compliant break-bulk that increases contract depth and profitability. The UAE cold chain logistics market is aligning road, sea, air, and rail options to support these hubs, with road providing flexible routing across the Dubai–Abu Dhabi–Sharjah corridor, and air and sea connecting long-haul import and pharma lanes. DP World’s multi-year logistics investment program, launched in 2025, strengthens multi-temperature yard capacity and automated cross-docks that can improve reefer turns and reduce handling time. As bonded options expand in free zones, re-export flows become more efficient and reduce downstream duty burdens.

The services stack that commands premium pricing is anchored in visibility and compliance. RSA Cold Chain’s September 2025 facility at Jebel Ali Free Zone adds 40,000 pallets of multi-temperature, bonded and non-bonded capacity with ISO 22000 and HACCP certifications and smart monitoring systems that strengthen pharma and halal flows. The UAE cold chain logistics industry is monetizing telemetry and exception handling as standalone services that help shippers manage risk and improve audit readiness. These value-added features have become essential rather than optional for healthcare and high-velocity grocery accounts. As portfolio operators layer process control and bonded postponement strategies, contracts increasingly prioritize reliability metrics such as on-time performance and temperature excursion rates alongside price.

By Temperature Type: Chilled Leads in Share, Frozen Surges on E-Grocery Momentum

Chilled cargo accounted for 39.54% in 2025 as fresh produce, dairy, and ready-to-eat items moved through tight import-to-shelf windows within urban distribution loops. Frozen segments are advancing the fastest at a 5.43% CAGR through 2031 as quick-commerce and e-grocery lean on frozen meal kits and ready-to-cook categories that maintain service levels during demand spikes. Multi-temperature facilities are expanding climate zones that allow operators to balance chilled, frozen, and deep-freeze volumes under unified dock and WMS control. The UAE cold chain logistics market is adding more multi-zone facilities with continuous monitoring and automated alerting to maintain consistency across chambers. These footprints allow faster pivots in assortment planning and SKU mix as retail and foodservice categories evolve.

Ultra-low temperature rooms for biologics and vaccines are a smaller segment today, though they are building share through investments in pharma corridors and qualified storage. Kuehne+Nagel’s Emirates Drug Establishment certification in August 2025 to store raw pharmaceutical materials at Dubai South, with dedicated 2-8°C chambers and GxP-restricted areas, illustrates the buildout of regulated capacity that supports future growth in specialized healthcare products.. As sensor density rises and dashboards unify controls across temperature bands, operators improve response times to anomalies and reduce spoilage. The UAE cold chain logistics industry is also co-locating climate-controlled ambient zones for sensitive categories that do not require refrigeration but need stable environments to protect product quality.

By Application: Meat & Poultry Anchors Revenue, Vaccines Drive Premium Growth

Meat and poultry led with 24.41% in 2025 as halal protocols drive segregated storage, dedicated material handling, and robust documentation to meet certification audits. These requirements add operational complexity that strengthens barriers to entry and consolidates demand with certified operators. Vaccines and clinical-trial materials are the fastest-growing application at a 6.21% CAGR to 2031, powered by the Abu Dhabi vaccine hub launched in July 2025, which supports distribution across the Middle East, Africa, and South Asia through CEIV Pharma-compliant air corridors. Emirates SkyCargo reinforced pharma volumes and introduced new freighter routes that serve these corridors with more capacity.

Fruits and vegetables depend on chilled continuity from port to distribution center and onto retail shelves, which elevates airflow design and humidity controls in warehousing. Fish and seafood demand precise handling windows and storage bands across fresh and frozen tiers to protect quality, especially for premium and live shipments. Dairy and frozen desserts run on narrow temperature bands where airflow and fast-loading workflows reduce the risk of texture degradation. The UAE cold chain logistics market is improving performance through higher sensor density and integrated alarms that enable quicker responses. As bonded options in free zones support re-export of halal meats and other perishables, operators can manage inventory under duty-efficient structures and maintain product integrity with segregated flows.

Geography Analysis

Dubai led with 32.60% of revenue in 2025 and is projected to grow at a 5.78% CAGR through 2031, driven by integrated seaport-airport networks and free-zone ecosystems. DP World’s 2025 logistics program adds multi-temperature yards and automated cross-docks to improve reefer throughput. Emirates SkyCargo expanded pharma lanes by adding Liege in January 2026 with five weekly freighters. RSA Cold Chain’s 40,000-pallet JAFZA facility, launched in September 2025, supports halal and healthcare flows with audit-ready infrastructure. Dubai’s cold chain logistics market is also evolving toward micro-nodes for frozen and chilled inventory near high-density areas to reduce last-mile risks.

Abu Dhabi is strengthening its role as a healthcare logistics hub with qualified infrastructure. The Department of Health’s July 2025 KEZAD vaccine hub, operated by Rafed, integrates with CEIV Pharma-compliant cargo networks. KEZAD Group’s AED 621 million warehousing expansion, equal to USD 169.1 million, adds multi-user cold storage for pharma-grade handling. Abu Dhabi’s cold chain logistics market competes on certification depth and airside-to-warehouse controls to reduce risks for temperature-sensitive goods.

Sharjah and the Northern Emirates complement Dubai and Abu Dhabi with cost-competitive offerings and new bonded capacity. Gulftainer’s K-Flow facility, launched in September 2025 at Khorfakkan Commercial Terminal, provides cold storage and bonded services for regional distribution. Inland hubs linked by highway and rail offer future expansion potential, especially for food re-exports into the GCC. These emirates are also testing micro cold storage for e-grocery and foodservice, with scale-up dependent on aligning technology and demand density.

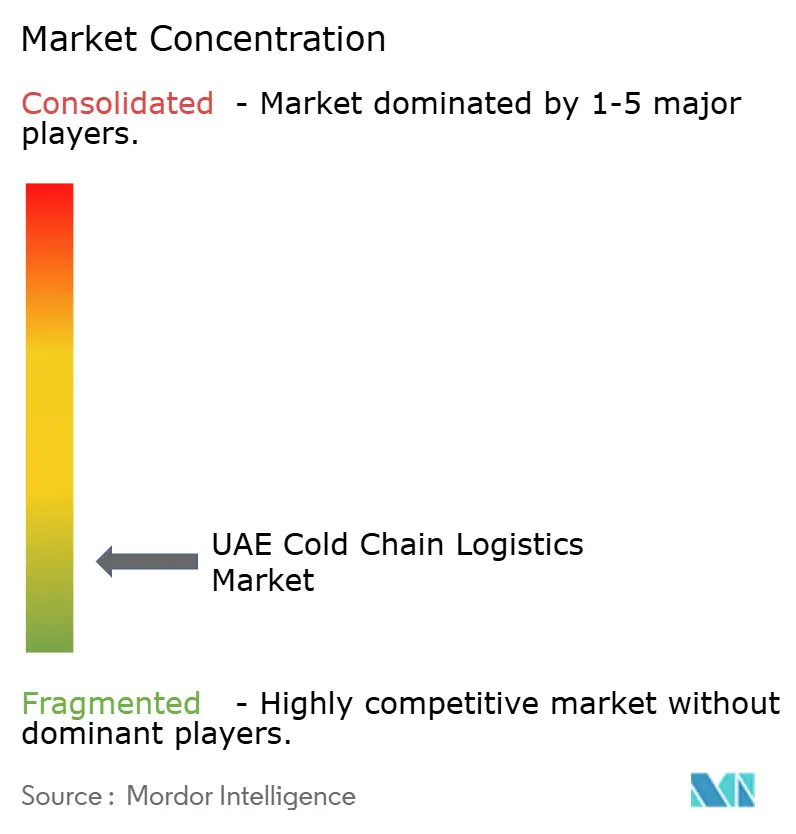

Competitive Landscape

The UAE cold chain logistics market is fragmented with multi-user facilities and specialized providers competing on certified quality, visibility, and lead-time performance. International operators are deepening footprints at strategic nodes that combine bonded options with multi-temperature flexibility. RSA Cold Chain’s large-format JAFZA site, launched in September 2025, adds certified capacity and smart monitoring that supports halal and pharma corridors and reflects confidence in the market’s long-term demand. DP World’s investment program is building more integrated flows across modes, which benefits cold shippers that require reliable handoffs and bonded efficiencies. As free-zone ecosystems add process and light manufacturing capability, standalone cold stores are pairing with processing and distribution to provide fuller solutions.

Technology and compliance are emerging as the main differentiators. Source International reports over 10,000 wireless sensors operating across seven climate zones at its main Dubai site, which enables continuous monitoring and audit-ready logs that shippers can access. In healthcare, Kuehne+Nagel’s Emirates Drug Establishment certification at Dubai South adds validated 2-8°C capacity and restricted-access GxP areas that meet higher regulatory thresholds and support raw materials handling for manufacturers.[3] Kuehne+Nagel, “Kuehne+Nagel UAE achieves Emirates Drug Establishment (EDE) Certification to store raw pharmaceutical materials,” Kuehne+Nagel, kuehne-nagel.com The UAE cold chain logistics market is also standardizing digital audit trails that capture temperatures in transit and on docks, which reduce insurance and compliance risks for sensitive cargo.

Sovereign and ecosystem capital are shaping platform scale and integration. ADQ completed a majority stake acquisition in Aramex in July 2025, integrating routes and a large warehouse footprint with other national logistics assets to build a more coordinated network. KEZAD signed a long-term land lease in June 2025 with SINGAUTO for a 100,000-square-meter intelligent refrigerated vehicle facility, equal to AED 100 million or USD 27.2 million as converted here, which links warehousing ecosystems with next-generation cold mobility. The UAE cold chain logistics market is therefore deepening integration from vehicle production to bonded warehousing and airside handling, which supports end-to-end solutions for complex temperature-sensitive flows.

UAE Cold Chain Logistics Industry Leaders

Global Shipping & Logistics LLC

Mohebi Logistics

GAC Dubai

RSA Logistics

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Emirates SkyCargo added Liege (Belgium) to its freighter network with five weekly flights, three of which connect Liege with Chicago O'Hare and Al Maktoum International Airport in Dubai, specifically for transporting critical temperature-sensitive pharmaceuticals via a seamless cool chain, boosting cargo capacity by 500 tonnes weekly.

- September 2025: RSA Cold Chain (a joint venture between UAE-based RSA Global and Americold) launched a flagship 40,000-pallet facility at Jebel Ali Free Zone featuring multi-temperature bonded and non-bonded storage, 27 loading docks, ISO 22000 and HACCP certifications, smart monitoring systems, and rooftop solar panels, more than doubling the operator's network capacity to 62,000 pallets.

- September 2025: Gulftainer launched K-Flow, a 50-hectare integrated logistics facility at Khorfakkan Commercial Terminal's bonded zone, offering customized supply chain solutions including warehousing, cold storage, distribution services, and container freight station capabilities to enhance Sharjah's trade gateway position.

- August 2025: Kuehne + Nagel UAE achieved Emirates Drug Establishment (EDE) certification to store raw pharmaceutical materials at its Dubai South facility, which spans 42,000 square meters with 25,500 square meters of temperature-controlled space featuring cold chambers at 2-8°C and GxP-compliant restricted-access chambers.

UAE Cold Chain Logistics Market Report Scope

To guarantee that the requisite low-temperature range is constantly maintained, a cold chain is a temperature-controlled distribution network that integrates refrigerated production, cold storage, and cold chain transportation facilities across air, water, and rail lines. The market for cold chains is expected to expand quickly due to rising food consumption, an expanding tourism industry, and an increase in demand for frozen and ready-to-eat foods.

The UAE Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), by Temperature Type (Chilled, Frozen, Ambient, and Deep-Frozen), by Application (Fruits and Vegetables, Meat and Poultry, Fish and Seafood, Dairy and Frozen Desserts, Bakery and Confectionery, Ready-to-Eat Meals, Pharmaceuticals & Biologics, Vaccines and Clinical Trial Materials, Chemicals and Specialty Materials, and Other Perishables), and by Geography (Dubai, Abu Dhabi, Sharjah, Ajman and Others). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5°C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen/Ultra-Low (less than -20°C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

By Emirate

| Dubai |

| Abu Dhabi |

| Sharjah |

| Ajman and Others |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen/Ultra-Low (less than -20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

| By Emirate | Dubai | |

| Abu Dhabi | ||

| Sharjah | ||

| Ajman and Others | ||

Key Questions Answered in the Report

What is the growth outlook for the UAE cold chain logistics market through 2031?

The UAE cold chain logistics market is projected to reach USD 2.43 billion by 2031 from USD 1.83 billion in 2026 at a 5.84% CAGR.

Which service type leads and which grows fastest in the UAE?

Refrigerated storage led with 50.34% in 2025, while value-added services are set to grow at 4.76% CAGR through 2031.

How are temperature bands evolving in the UAE cold chain?

Chilled held 39.54% share in 2025, and frozen is the fastest-growing at 5.43% CAGR through 2026-2031, driven by e-grocery and ready-to-cook categories.

What applications are expanding most quickly in UAE cold logistics?

Vaccines and clinical-trial materials are expanding at 6.21% CAGR through 2031, supported by Abu Dhabi’s KEZAD vaccine hub and pharma air corridors.

Which emirate leads in share for cold chain logistics?

Dubai led with 32.60% in 2025 and is projected to grow at 5.78% CAGR, supported by port-air connectivity and free-zone capacity.

What infrastructure moves are shaping future capacity in the UAE?

DP World’s multi-year logistics investment and KEZAD’s warehouse expansion with cold storage are expanding multi-temperature yards, bonded options, and inland sites tied to air and sea corridors.

Page last updated on: