Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 34.87 Billion |

| Market Size (2026) | USD 36.32 Billion |

| Market Size (2031) | USD 44.53 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Hair Care Market Analysis by Mordor Intelligence

The Asia Pacific Hair Care Market size is expected to grow from USD 34.87 billion in 2025 to USD 36.32 billion in 2026 and is forecast to reach USD 44.53 billion by 2031 at 4.16% CAGR over 2026-2031. This growth trajectory reflects the region's evolving consumer preferences toward premium formulations and multifunctional products that address scalp health alongside traditional cleansing needs. The growth outlook reflects premiumization, multifunctional product adoption, and an accelerated pivot toward scalp-health solutions. China holds the lion’s share of regional revenue, supported by rising disposable incomes and sophisticated digital commerce ecosystems. South Korea is the fastest-growing national market due to strong innovation competencies and K-beauty’s cultural influence. Category momentum is most visible in conditioners, scalp-focused treatments, and professional-grade styling lines that address humidity and pollution challenges. Distribution continues to migrate online, with social commerce and AI-driven recommendations reshaping product discovery. Regulatory pressure surrounding microplastics and packaging waste is catalyzing innovation in biodegradable ingredients and recyclable formats, even as patent activity in hair-loss cosmetics surges.

Key Report Takeaways

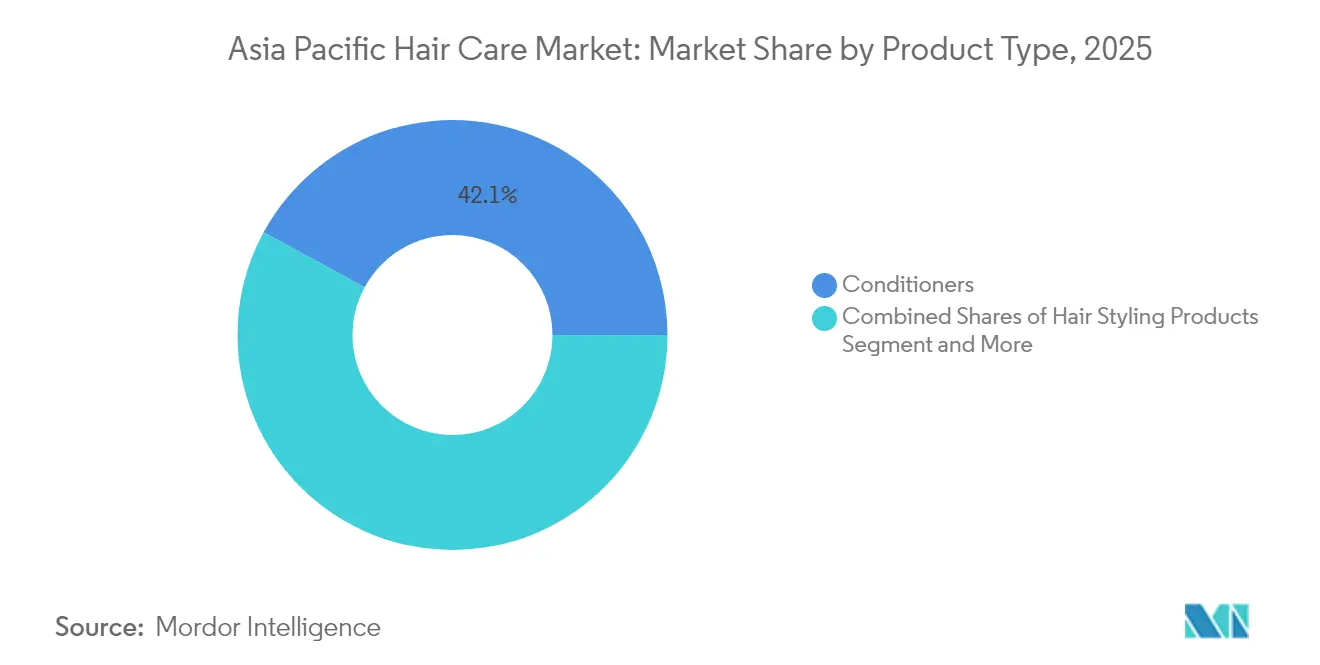

- By product type, conditioners led with 42.08% revenue share in 2025; hair styling products are projected to expand at a 5.03% CAGR through 2031.

- By category, conventional formulations commanded 78.30% of the Asia Pacific hair care market share in 2025, while natural and organic lines are advancing at a 6.33% CAGR to 2031.

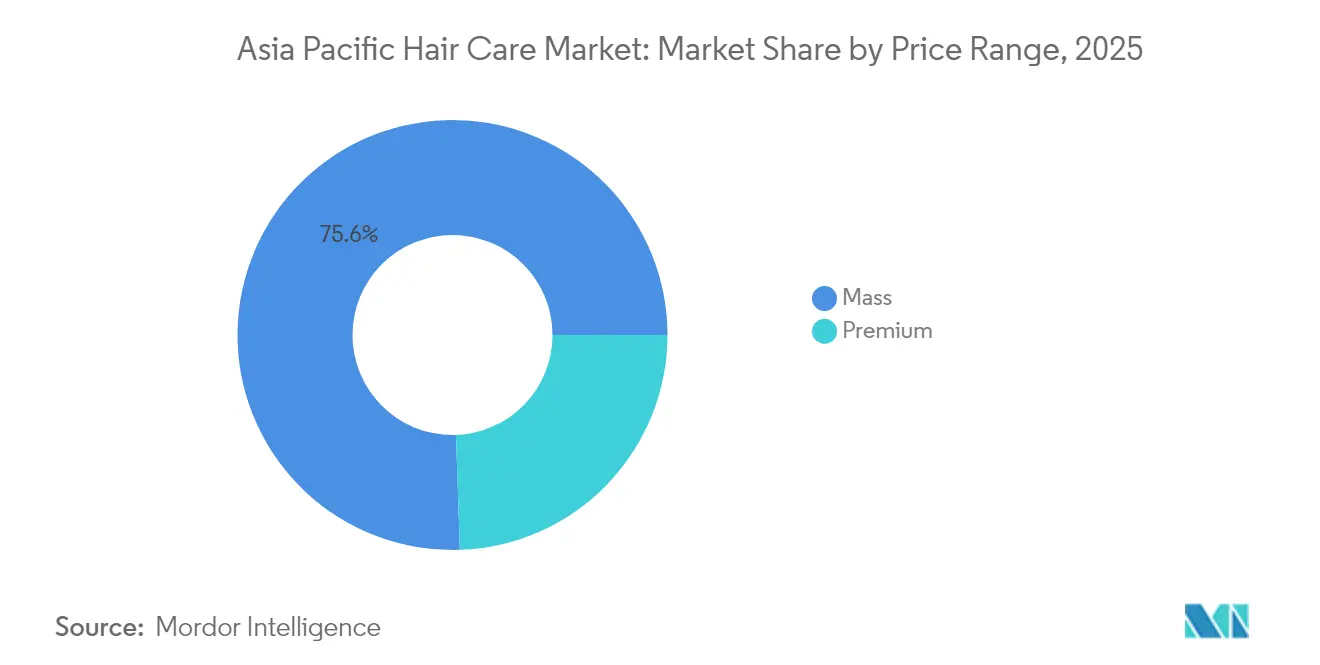

- By price range, the mass-market segment accounted for 75.55% of the Asia Pacific hair care market size in 2025; premium offerings are forecast to rise at a 5.74% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets held 33.22% share in 2025; online retail stores are set to grow at a 6.42% CAGR through 2031.

- By geography, China contributed 35.62% of regional revenue in 2025; South Korea is on track for a 5.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural and Organic Ingredient Preference | +1.2% | Global, strongest in Australia, Japan, Singapore | Medium term (2-4 years) |

| Scalp Health and Dandruff Solution Demand | +1.5% | China, India, Japan core markets | Short term (≤ 2 years) |

| Social Media and Influencer Promotion Trends | +0.8% | South Korea, Thailand, Singapore urban centers | Short term (≤ 2 years) |

| Innovative Multifunctional Hair Care Solutions | +1.1% | Japan, South Korea, urban China | Medium term (2-4 years) |

| Rising Popularity of Hair Colorants | +0.7% | Japan, South Korea, urban APAC markets | Medium term (2-4 years) |

| Premium Hair Care and Luxury Product Growth | +1.0% | China, Japan, Australia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural and Organic Ingredient Preference

Consumer demand for natural and organic hair care formulations is reshaping product development strategies across Asia Pacific. This preference stems from rising awareness of synthetic ingredient risks and cultural affinity for traditional botanical remedies, particularly in markets like India and Thailand where Ayurvedic and herbal formulations command premium pricing. Japan leads per-capita hair care spending globally at JPY 5,470 annually, with over 40% of consumers prioritizing natural ingredients in their purchasing decisions. The trend is accelerating adoption of fermented ingredients, with companies like Wella incorporating high-purity squalane from skincare applications into hair treatments to address lipid replenishment needs. Regulatory frameworks in Australia and New Zealand increasingly favor certified organic formulations, creating competitive advantages for brands that achieve COSMOS, ECOCERT, or ACO certifications while maintaining performance standards comparable to conventional alternatives.

Scalp Health and Dandruff Solution Demand

The scalp care segment is experiencing unprecedented growth as consumers adopt "scalp-as-skin" treatment philosophies, driven by rising awareness of scalp microbiome health and its impact on hair quality. China's premium scalp care market expanded 190% to over 33 billion RMB, with Unilever's CLEAR brand launching the SCALPCEUTICALS PRO RANGE featuring three patented technologies targeting cellular-level scalp repair. This shift reflects deeper consumer understanding of scalp health's role in hair loss prevention, with nearly 90% of China's population reporting hair or scalp problems according to the 2023 National Scalp Health White Paper. Innovation focuses on combining traditional anti-dandruff actives like selenium disulfide with advanced delivery systems and scalp barrier repair technologies. The trend is particularly pronounced in aging demographics, where post-COVID hair loss concerns have elevated demand for preventive scalp treatments that address telogen effluvium and stress-related hair thinning issues.

Social Media and Influencer Promotion Trends

Digital marketing transformation is fundamentally altering hair care discovery and purchase patterns, with 60% of Asia Pacific consumers using social media for product discovery and 46% engaging with livestream shopping experiences. Instagram usage among beauty shoppers reaches 80% daily in Japan, while 62% turn to influencers for new product recommendations, creating powerful amplification effects for brands that master social commerce integration. China's beauty market, projected to reach USD 78 billion by 2025, increasingly relies on Douyin and XiaohongShu platforms where livestreaming accounts for approximately 10% of e-commerce sales by 2022. The Korean beauty influence extends beyond skincare into hair care, with K-beauty market dynamics driving adoption of multi-step hair routines and ingredient transparency. Social proof through user-generated content and authentic reviews has become essential for brand credibility, particularly among Gen Z and millennial consumers who prioritize brands with social and environmental commitments.

Innovative Multifunctional Hair Care Solutions

The convergence of skincare and hair care technologies is creating new product categories that address multiple concerns in single formulations, responding to consumer demand for simplified routines and enhanced value propositions. Asia Pacific consumers increasingly favor multifunctional cosmetics, with 57% in the region viewing multi-benefit products as good value according to GlobalData's 2024 Q3 Consumer Survey. Innovation examples include L'Oréal Paris Elseve 72H Moisture Filling Shampoo in Malaysia incorporating hyaluronic acid for scalp hydration, and anti-dandruff formulations combining salicylic acid with piroctone olamine for dual-action efficacy. Korean startup Polyphenol Factory's Grabity brand exemplifies this trend with LiftMax 308 technology delivering immediate 140% hair volume increase while providing anti-hair loss benefits through polyphenol complexes. The approach extends to packaging innovations, with brands adopting solid formats and waterless formulations that combine sustainability benefits with concentrated active delivery systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Minimalist Hair Care Routines | -0.9% | Japan, South Korea, urban Australia | Short term (≤ 2 years) |

| Concerns Over Chemical Additives Rise | -0.7% | Australia, New Zealand, Singapore | Medium term (2-4 years) |

| Packaging Waste and Microplastic Environmental Concerns | -1.1% | Malaysia, Thailand, Indonesia, Philippines | Medium term (2-4 years) |

| High Brand Switching and Low Loyalty | -0.5% | China, India, emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Minimalist Hair Care Routines

The minimalist beauty movement is challenging traditional multi-step hair care routines, particularly in mature markets where consumers are simplifying their daily regimens to focus on fewer, higher-quality products. This trend reflects broader lifestyle changes toward conscious consumption and time efficiency, with Japanese consumers increasingly adopting streamlined routines despite the country's historically complex beauty traditions. The shift impacts product categories differently, with basic shampoo and conditioner combinations gaining favor over specialized treatments, serums, and styling products. Brands are responding by developing concentrated formulations that deliver multiple benefits in single applications, though this approach risks commoditization and margin pressure. The trend is particularly pronounced among younger demographics who prioritize authenticity and sustainability over-elaborate routines, creating challenges for brands that have built portfolios around step-by-step regimens. Economic pressures in some markets are amplifying this trend, as consumers seek value through product consolidation rather than premium pricing for specialized solutions.

Packaging Waste and Microplastic Environmental Concerns

Environmental regulations targeting cosmetic packaging and microplastic ingredients are creating compliance costs and reformulation pressures across Asia Pacific markets. Southeast Asian countries face severe microplastic contamination, with studies showing Malaysia, Thailand, and Philippines in 'danger' or 'extreme danger' categories for polymer hazard indices due to personal care product contributions. Vietnam's Ho Chi Minh City alone releases an estimated 1.3 billion microbeads annually from facial and body scrubs, despite growing regulatory attention to marine plastic pollution. The European Union's microplastic restrictions, phasing out plastic microbeads through 2027-2035, are influencing Asia Pacific regulatory frameworks and forcing reformulation toward biodegradable alternatives like alginate, chitosan, and PLA-based substitutes. Compliance with Extended Producer Responsibility frameworks requires significant investment in sustainable packaging development, recycling infrastructure, and supply chain transparency, creating barriers for smaller brands while favoring established players with resources to navigate complex regulatory landscapes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conditioners Drive Market While Styling Innovations Accelerate

Conditioners command 42.08% market share in 2025, reflecting their essential role in Asia Pacific hair care routines where humidity and pollution create heightened needs for protective and reparative formulations. The dominance stems from cultural preferences for smooth, manageable hair textures and growing awareness of cuticle protection benefits in tropical climates. Hair styling products emerge as the fastest-growing segment at 5.03% CAGR through 2031, driven by professional-grade formulations entering consumer markets and rising demand for humidity-resistant hold technologies. Noveon's introduction of Fixate Superhold polymer demonstrates this trend, providing superior humidity resistance specifically for Asian markets where high moisture conditions challenge traditional styling polymers.

Shampoo maintains steady market position despite commoditization pressures, with innovation focusing on specialized formulations like Unilever's CLEAR SCALPCEUTICALS PRO RANGE featuring patented selenium disulfide and piroctone olamine technologies. Hair loss treatment products benefit from aging demographics and stress-related hair concerns, particularly in markets like Korea where patent filings for hair-loss cosmetics lead globally at 42.9% of total applications. Hair colorants experience moderate growth as consumers seek salon-quality results at home, with innovations like sunlight-induced permanent dyeing using polydopamine offering eco-friendly alternatives to conventional chemical processes. Other product types including sprays, gels, serums, and masks capture growing market share through multifunctional positioning and premium ingredient integration.

By Category: Conventional Products Dominate Despite Natural Growth

The conventional/synthetic category maintains 78.30% market share in 2025, supported by established supply chains, proven efficacy profiles, and cost advantages that appeal to price-sensitive consumers across emerging Asia Pacific markets. However, natural/organic alternatives are expanding at 6.33% CAGR through 2031, driven by rising environmental consciousness and cultural preferences for traditional botanical ingredients. This growth reflects successful positioning of natural formulations as premium alternatives rather than direct substitutes, allowing brands to command higher margins while addressing sustainability concerns. Australia and Japan lead natural product adoption, with over 40% of Japanese consumers prioritizing natural ingredients despite the country's historically synthetic-focused beauty industry.

Innovation in natural formulations increasingly incorporates biotechnology applications, including fermented ingredients and plant stem cell technologies that deliver performance comparable to synthetic alternatives. The organic shampoo market specifically targets Asia Pacific as the fastest-growing region due to cultural affinity for herbal and Ayurvedic ingredients, particularly in India and Thailand where traditional medicine influences consumer preferences. Regulatory frameworks in developed markets favor certified organic formulations, creating competitive advantages for brands that achieve COSMOS, ECOCERT, or regional certifications while maintaining efficacy standards. The category evolution suggests a bifurcated market where conventional products serve mass market needs while natural alternatives capture premium segments and environmentally conscious demographics.

By Price Range: Mass Market Stability Supports Premium Expansion

Mass market products hold 75.55% market share in 2025, providing accessible hair care solutions across diverse income levels and maintaining volume growth through population expansion and urbanization trends. This segment benefits from established distribution networks, economies of scale in manufacturing, and brand recognition built over decades of market presence. Premium products accelerate at 5.74% CAGR through 2031, reflecting rising disposable incomes, aging demographics seeking advanced solutions, and premiumization trends that favor efficacy-driven formulations over basic cleansing products.

The premium segment increasingly incorporates advanced technologies like AI-powered personalization, biotechnology-derived actives, and clinical-grade formulations that justify higher price points through demonstrated efficacy. Japanese consumers lead global per-capita hair care spending at JPY 5,470 annually, creating a sophisticated market for premium innovations that combine traditional ingredients with modern delivery systems. Korean brands like Polyphenol Factory's Grabity demonstrate premium positioning through patented technologies and clinical validation, achieving secondary market prices up to USD 190 per bottle due to limited availability and proven performance. The price segmentation reflects market maturation where consumers increasingly differentiate between basic functional needs and advanced treatment solutions.

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

Supermarkets and hypermarkets maintain 33.22% market share in 2025, leveraging extensive physical presence, competitive pricing, and convenience factors that appeal to routine purchase behaviors. These channels benefit from high foot traffic, impulse buying opportunities, and the ability to showcase product ranges through in-store displays and promotions. Online retail stores emerge as the fastest-growing channel at 6.42% CAGR through 2031, driven by digital adoption, personalized recommendations, and subscription models that enhance customer retention. The shift reflects changing consumer behaviors where 46% use online shopping for better deals and 40% accept AI-powered product recommendations.

Social commerce integration transforms online retail effectiveness, with livestreaming accounting for 46% of purchase conversions and shoppable pins driving 45% of social media-influenced sales across Asia Pacific markets. Specialty stores maintain relevance through expert consultation, premium product curation, and experiential services that online channels cannot replicate, particularly for high-value treatments and professional-grade products. The channel evolution creates opportunities for brands that master omnichannel strategies, combining physical touchpoints with digital convenience and personalization capabilities. Indonesia's e-commerce regulations requiring imported products to comply with local notification and halal certification before online sale illustrate the regulatory complexity that brands must navigate in digital expansion.

Geography Analysis

China commands 35.62% market share in 2025, representing the single largest national market with projected revenue of USD 60.7 billion and accounting for nearly 70% of Asia Pacific regional growth through 2025. The market benefits from rising disposable incomes, premiumization trends, and sophisticated digital commerce infrastructure that enables livestreaming and social commerce integration. South Korea accelerates as the fastest-growing market at 5.76% CAGR through 2031, driven by innovation leadership in beauty technology, strong export performance, and cultural influence that extends K-beauty trends across the region.

Japan maintains significant market presence despite demographic headwinds, with the highest per-capita spending globally creating opportunities for premium and anti-aging formulations. India and Southeast Asian markets including Thailand, Singapore, and the Philippines represent emerging growth opportunities where urbanization, rising incomes, and increasing beauty consciousness drive market expansion. Australia and New Zealand provide developed market dynamics with emphasis on natural and organic formulations, regulatory compliance, and sustainability credentials that influence broader regional trends.

The geographic distribution reflects varying stages of market maturity, from China's sophisticated digital commerce ecosystem to emerging markets where basic infrastructure development supports volume growth. Vietnam's regulatory environment illustrates the evolving compliance landscape, with microplastic concerns driving policy development that may influence product formulation requirements across the region. The Asia-Pacific region demonstrates significant disparities in market development, with countries like Japan and South Korea showcasing advanced distribution networks and digital integration, while nations such as Indonesia and Philippines focus on expanding their basic retail infrastructure. These market variations create distinct opportunities and challenges for industry participants, requiring tailored strategies for each geographic segment.

Competitive Landscape

The Asia Pacific hair care market exhibits moderate fragmentation, creating space for both established multinationals and innovative regional players to compete through differentiated strategies. Market leaders leverage global scale advantages in R&D investment, regulatory compliance, and distribution network development, while emerging companies exploit niche opportunities through specialized formulations, direct-to-consumer models, and technology-enabled personalization.

Patent activity reveals strategic focus areas, with Korea leading global hair-loss cosmetic filings at 42.9% share, indicating substantial R&D investment in functional ingredients and biotechnology applications that challenge traditional approaches. Technology adoption is reshaping competitive dynamics, with AI-powered diagnostics, personalized formulation platforms, and social commerce integration becoming essential capabilities for market success.

Companies like Opal Cosmetics Group demonstrate this evolution through AI-enabled "Skinification" approaches that provide personalized scalp analysis and product recommendations, while Korean startups like Polyphenol Factory achieve premium positioning through patented polyphenol technologies and clinical validation. Opportunities exist in sustainable packaging solutions, microplastic-free formulations, and biotechnology-derived actives that address regulatory pressures while delivering superior performance. The competitive landscape increasingly rewards companies that combine scientific innovation with sustainability credentials and digital marketing expertise, creating barriers for traditional players that rely solely on brand heritage and distribution scale.

Asia-Pacific Hair Care Industry Leaders

L'Oréal S.A.

Kao Corporation

Procter & Gamble

Unilever

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: India's retail beauty sector witnessed a significant development with the launch of K Formula, the country's first peptide-powered molecular haircare brand. Founded by entrepreneur Anoushka Adya, the brand introduced a six-step repair ritual that claimed to deliver visible transformation within five minutes. K Formula made its market entry with a six-product line, which included a Peptide Hair Corrector (pre-shampoo), Peptide Shampoo, Peptide Conditioner, Molecular Leave-In Magic Mask, Molecular Repair Hair Oil, and a Peptide Dry Shampoo. Each product was vegan, sulphate-free, cruelty-free, and color-safe.

- July 2025: Consumer goods major CavinKare expanded its product portfolio under its popular brand Meera with the launch of 'rice kanji' shampoo as it aimed to strengthen its market leadership in the haircare category. The 'rice kanji' (starchy water) shampoo was based on a time-tested ritual from South Indian kitchens and was known for its ability to smooth hair structure, add shine, and benefit damaged and coarse hair, as per the company.

- May 2025: Unilever's premium professional anti-dandruff brand, Clear, hosted a grand launch event at TANK Shanghai, where it debuted its first-ever Scalpceuticals Pro Range. This new series emerged from over a decade of scientific research conducted by five global labs and over 200 dermatologists. The Clear Scalpceuticals Pro Range, developed with three patented technologies, was introduced with five targeted products- Hair Fall Resist Shampoo, Hair Fall Resist Conditioner, Hair Fall Resist Serum, Men Scalp Pro Anti-Hairfall Fortifying Shampoo, and Men Scalp Pro Anti-Hairfall Fortifying Serum.

- April 2025: Japanese brand Syoss launched a premium hair dye formulated with natural clay amid rising concerns regarding grey hair among older consumers. The new professional coloring products offered up to 100 days of color intensity and complete coverage of gray hair, thanks to an advanced cream-based formula. Additionally, keratin supported stronger hair, and the new deep care mask nourished freshly colored hair.

Asia-Pacific Hair Care Market Report Scope

Hair care refers to the cleanliness and cosmetology of hair that develops from the human scalp and the products employed to take care of it.

The Asia-Pacific hair care market is segmented by type, distribution channel, and geography. By type, the market is segmented into colorants, hair sprays, conditioners, styling gel, hair oil, shampoo, and other products. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, pharmacy and drug stores, and other distribution channels. The report also provides an analysis of the emerging and established geographical countries in the region, including China, Japan, India, Australia, and Rest of Asia-Pacific. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Shampoo |

| Conditioner |

| Hair loss treatment products |

| Hair Colorants |

| Hair Styling Products |

| Other Product Types |

By Category

| Natural/Organic |

| Conventional/Synthetic |

By Price Range

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| China |

| India |

| Japan |

| Australia |

| New Zealand |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Shampoo |

| Conditioner | |

| Hair loss treatment products | |

| Hair Colorants | |

| Hair Styling Products | |

| Other Product Types | |

| By Category | Natural/Organic |

| Conventional/Synthetic | |

| By Price Range | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific hair care market?

The region’s market value is USD 36.32 billion in 2026.

Which product type generates the most revenue?

Conditioners lead, accounting for 42.08% of category sales in 2025.

Which country is growing fastest in hair care sales?

South Korea is forecast to grow at a 5.76% CAGR through 2031.

How big is the premium segment relative to mass products?

Premium offerings represent 24.45% of sales and are expanding at a 5.74% CAGR, outpacing mass-market growth.

Page last updated on: