Hereditary Angioedema Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

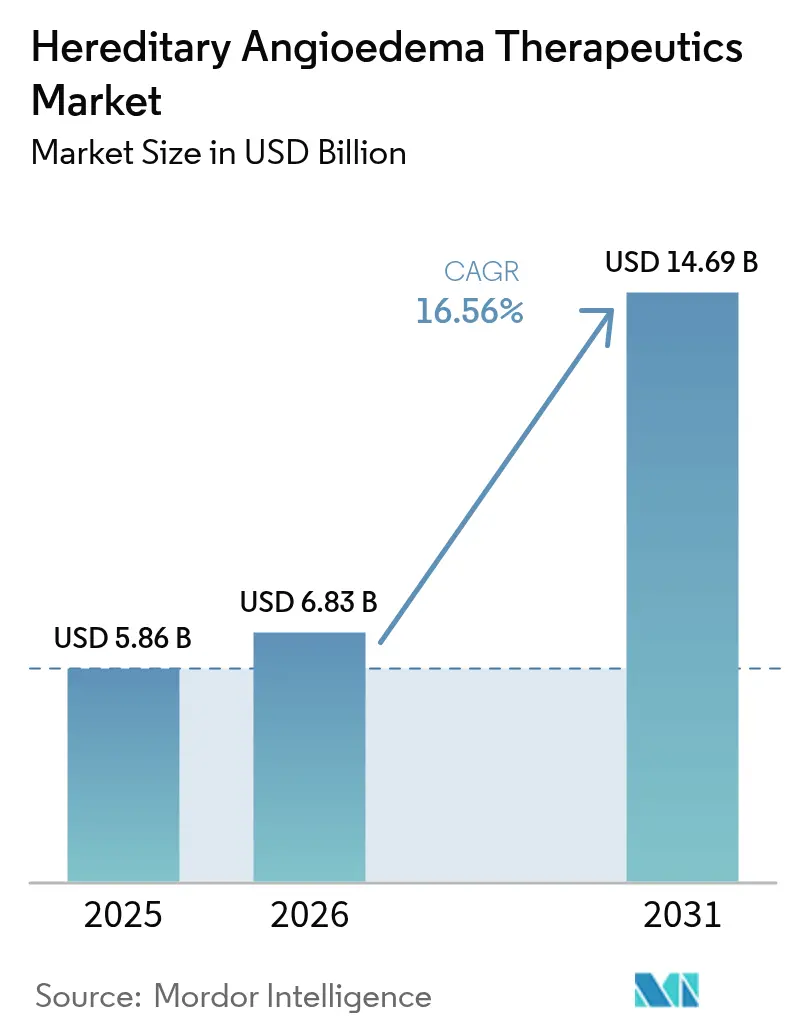

| Market Size (2026) | USD 6.83 Billion |

| Market Size (2031) | USD 14.69 Billion |

| Growth Rate (2026 - 2031) | 16.56% CAGR |

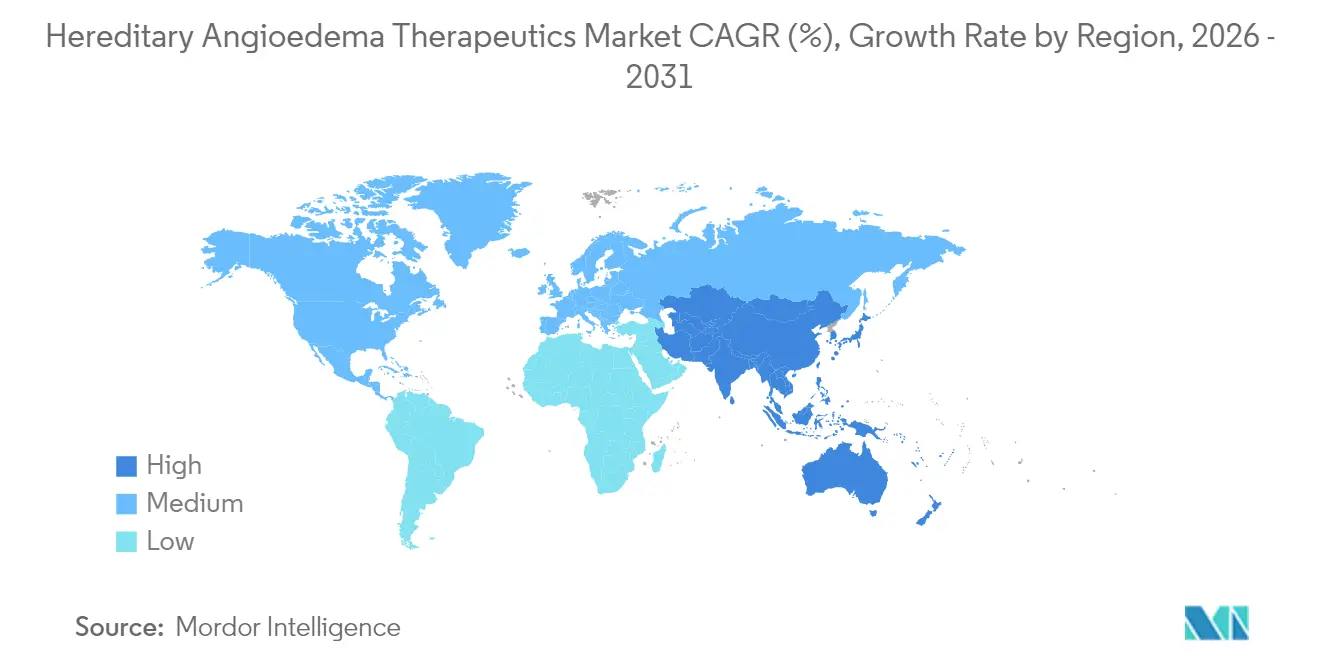

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

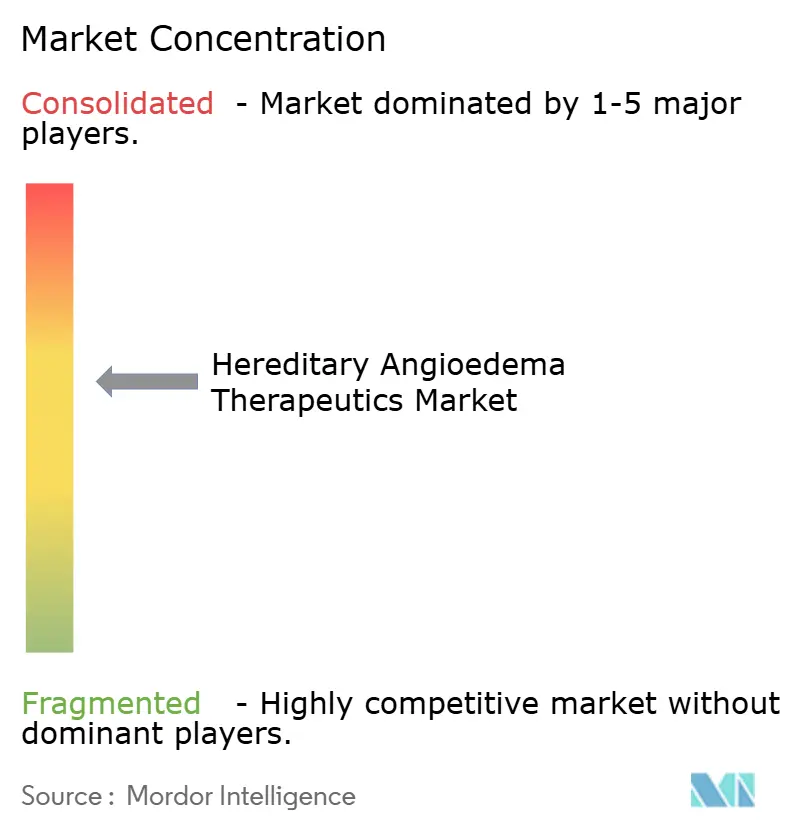

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hereditary Angioedema Therapeutics Market Analysis by Mordor Intelligence

The hereditary angioedema therapeutics market size in 2026 is estimated at USD 6.83 billion, growing from 2025 value of USD 5.86 billion with 2031 projections showing USD 14.69 billion, growing at 16.56% CAGR over 2026-2031. Breakthrough oral kallikrein inhibitors, expanding subcutaneous self-administration, and the first wave of gene-editing programs are unlocking substantial latent demand for predictable, patient-controlled prophylaxis. Rising orphan-drug pricing power and value-based reimbursement models are reinforcing investment, while specialty pharmacies and home-infusion networks remove historical adherence barriers. North America retains early-mover advantages in access and reimbursement, yet Asia-Pacific now delivers the fastest growth as regional advocacy and diagnostics improve. Competitive focus is shifting toward once-daily oral regimens, pediatric formulations, and one-time curative gene therapies, creating both opportunity and pricing pressures as payers weigh long-term budget impacts.

Key Report Takeaways

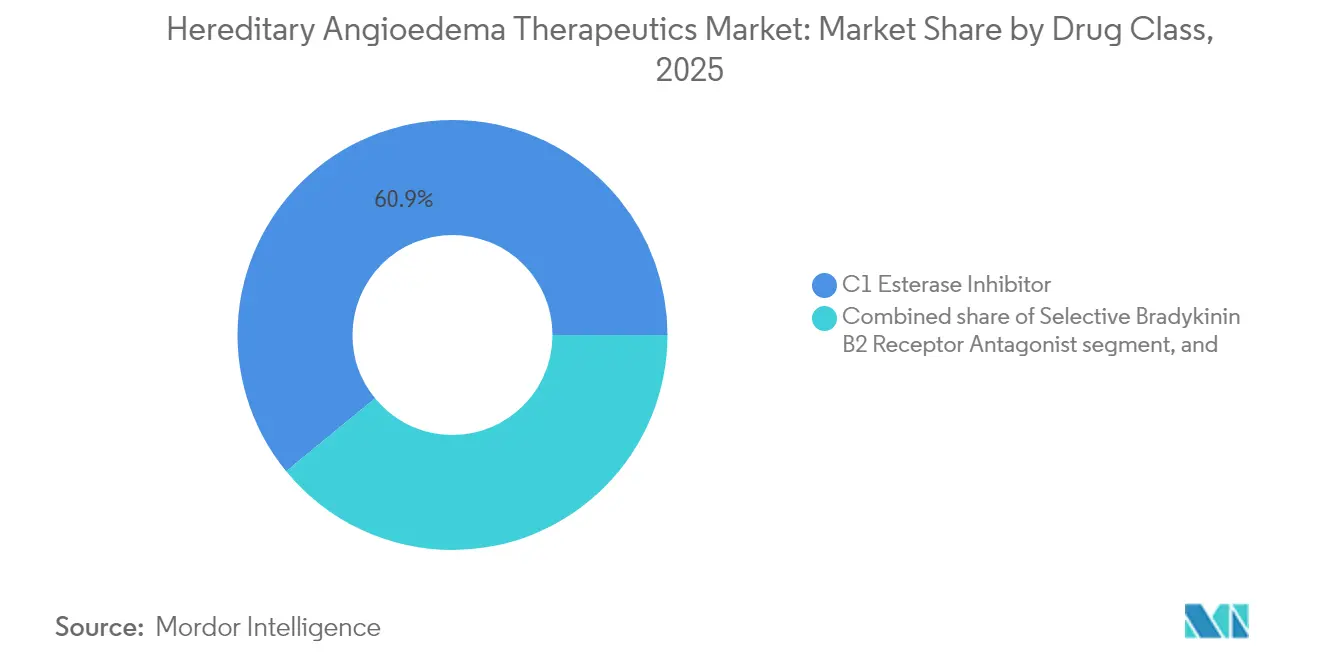

- By drug class, C1 esterase inhibitors led with 60.92% revenue share in 2025; kallikrein inhibitors are projected to grow at a 19.12% CAGR through 2031.

- By route of administration, subcutaneous delivery held 51.48% of hereditary angioedema therapeutics market share in 2025, while oral therapies are expected to register a 19.7% CAGR to 2031.

- By treatment type, long-term prophylaxis accounted for 56.85% of the hereditary angioedema therapeutics market size in 2025 and is tracking an 17.86% CAGR to 2031.

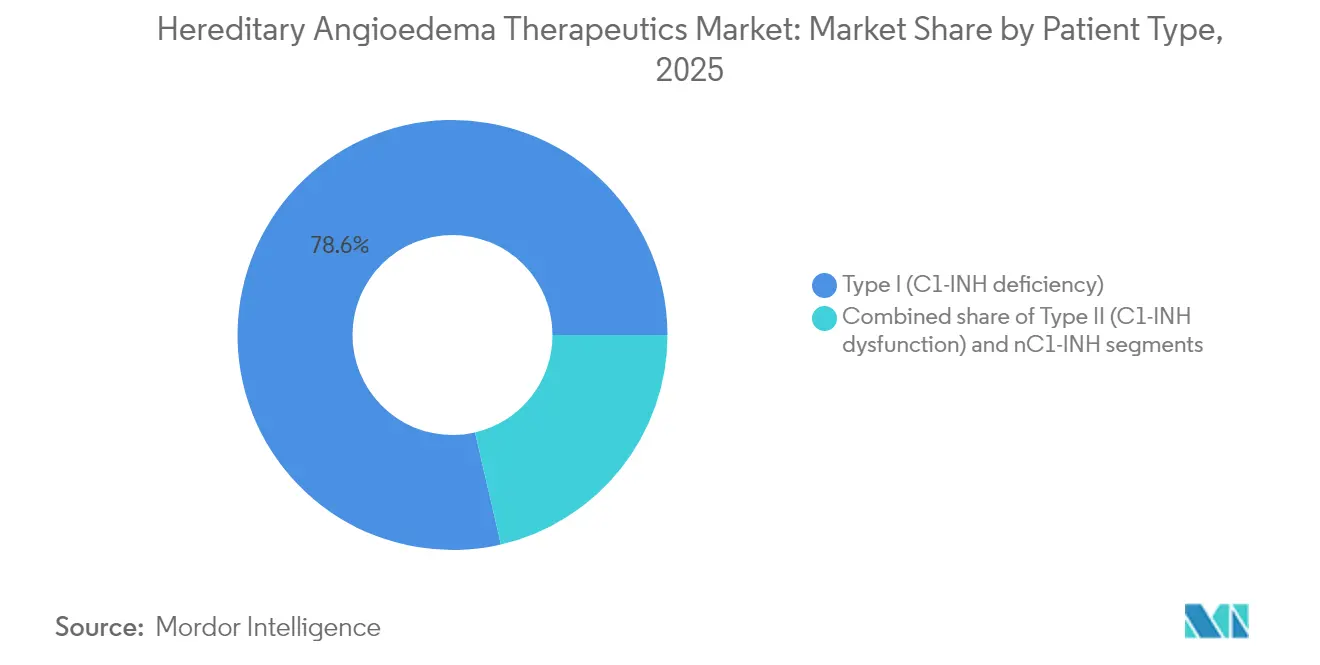

- By patient type, Type I cases captured 78.62% share of the hereditary angioedema therapeutics market size in 2025; nC1-INH patients represent the fastest-expanding cohort at 17.55% CAGR.

- By geography, North America commanded 79.55% revenue in 2025, whereas Asia-Pacific is poised for a 17.44% CAGR through 2031.

- CSL Behring, Takeda, and BioCryst collectively controlled a majority of 2024 global revenue, supported by vertically integrated plasma operations, broad portfolios, and aggressive route-innovation strategies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hereditary Angioedema Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial roll-out of first-in-class oral kallikrein inhibitors | +4.2% | Global, with earliest uptake in North America & EU | Medium term (2-4 years) |

| Escalating use of sub-cutaneous C1-INH self-administration | +3.8% | North America & EU core, extending to Asia-Pacific | Short term (≤2 years) |

| Momentum behind gene-silencing & CRISPR one-shot cures | +2.9% | North America & EU initially, global expansion planned | Long term (≥4 years) |

| Rising orphan-drug pricing power & payer acceptance | +2.1% | Global, strongest in developed markets | Medium term (2-4 years) |

| Precision-medicine push for nC1-INH HAE genotyping | +2.0% | Global, with pilot programs in the United States, EU & Japan | Medium term (2-4 years) |

| Home-infusion & tele-pharmacy infrastructure expansion | +1.8% | Global, fastest adoption in high-income countries | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Commercial Roll-Out of First-In-Class Oral Kallikrein Inhibitors

BioCryst’s berotralstat (Orladeyo) has normalized once-daily oral prophylaxis, driving USD 437 million in 2024 sales and a further 51% year-over-year uplift in Q1 2025. Young, working-age patients favor the pill format, accelerating switches from injectables; 70% of U.S. hereditary angioedema patients now choose oral prophylaxis. A pending FDA decision on KalVista’s sebetralstat could inaugurate the first oral on-demand option, with Phase 3 data showing symptom relief within 1.61 hours versus 6.72 hours for placebo[1]Eric Cromer et al., “Oral Berotralstat for Prophylactic Treatment of Hereditary Angioedema,” nejm.org. These dynamics are enlarging the hereditary angioedema therapeutics market by capturing previously undertreated segments and broadening geographic reach.

Escalating Use of Subcutaneous C1-INH Self-Administration

CSL Behring’s Haegarda cut attack frequency by 95% in pivotal trials and underpinned a global migration from intravenous replacement to patient-controlled subcutaneous dosing[2]CSL Behring, “Haegarda Clinical Overview,” cslbehring.com. Home programs reduce annual per-patient costs by 11.3% and maintain technical failure rates below 2%. Specialty pharmacies supply 24-hour helplines and nurse coaching, reinforcing adherence and freeing infusion-center capacity. Pediatric cohorts as young as eight years now achieve durable prophylaxis outside hospital settings, reinforcing quality-of-life gains.

Momentum Behind Gene-Silencing & CRISPR One-Shot Cures

Intellia’s NTLA-2002 achieved a 98% mean attack reduction over two years with no serious adverse events, suggesting a potential one-time cure. Ionis’s donidalorsen, an antisense oligonucleotide, delivered 81% attack reduction on monthly dosing. These modalities promise to compress lifetime spending from millions of dollars to a single intervention, yet long-term safety surveillance, manufacturing scale-up, and payer risk-sharing frameworks will dictate commercial timelines.

Rising Orphan-Drug Pricing Power & Payer Acceptance

Annual therapy costs above USD 500,000 are supported by documented 77.0% reductions in attack frequency and 59.5% improvements in quality-of-life metrics. Outcomes-based contracts link reimbursement to measured attack reduction, aligning incentives and sustaining innovation. Fast-track and breakthrough designations streamline FDA review, while Europe’s centralized HTA assessments increasingly recognize the rarity and severity of HAE in value determinations[3]U.S. Food and Drug Administration, “Rare Disease Development Programs,” fda.gov.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High annual therapy cost (>USD 500 k/patient) pressures budgets | –3.1% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Limited HAE expertise outside Tier-1 academic centers | –2.4% | Global, particularly rural & developing regions | Long term (≥4 years) |

| Cold-chain & plasma-supply bottlenecks for C1-INH | –1.9% | Global, pronounced in regions lacking local fractionation | Medium term (2-4 years) |

| Regulatory uncertainty for long-acting monoclonals in pediatrics | –1.6% | Global, impacting jurisdictions with stringent pediatric rules | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Annual Therapy Cost Pressures Healthcare Budgets

Despite strong clinical value, incremental cost-effectiveness ratios can breach USD 150,000 per QALY, challenging conventional thresholds[4]Journal of Managed Care & Specialty Pharmacy, “Economic Burden of Hereditary Angioedema,” jmcp.org. Real-world evidence places direct medical costs near USD 364,000 and indirect losses at USD 52,500 per patient yearly, straining public payers and limiting coverage in low-income markets. Biosimilar potential is restricted by plasma supply constraints and complex biologics manufacturing.

Limited HAE Expertise Outside Tier-1 Academic Centers

Misdiagnosis and delayed treatment persist, especially in rural areas where general practitioners rarely encounter HAE. Telehealth consultations and regional conferences—such as the 2024 HAEi meeting in Manila with delegates from 25 countries—are extending specialist knowledge but remain early-stage. Infrastructure gaps in diagnostics and cold-chain logistics impede equitable access, prolonging unmet need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: C1 Esterase Inhibitors Maintain Dominance Amid Kallikrein Innovation

C1 esterase inhibitors generated 60.92% of 2025 revenue, anchoring the hereditary angioedema therapeutics market size at USD 3.57 billion. CSL Behring’s Berinert and Haegarda safeguard this position through reliable efficacy and extensive real-world data. Yet kallikrein inhibitors are scaling faster at a 19.12% CAGR, led by BioCryst’s oral berotralstat, which delivered USD 437 million in 2024 sales. With modular oral, subcutaneous, and long-acting monoclonal formats in late-stage pipelines, kallikrein agents are positioned to capture incremental hereditary angioedema therapeutics market share over the forecast window.

Patient preference is steering capital allocation toward oral compounds and long-interval injectables, pressuring conventional plasma-derived segments. Nonetheless, plasma-free recombinant C1-INH (Ruconest) and supply-diversification strategies protect incumbents against sourcing constraints and infectious-disease risk, sustaining a two-pillar class dynamic through 2030.

By Route of Administration: Subcutaneous Gains Ground as Oral Therapies Accelerate

Subcutaneous products contributed 51.48% of hereditary angioedema therapeutics market share in 2025, equal to USD 3.02 billion, and underscore a decade-long shift toward home dosing. Training completion rates above 98% validate the model, while health-economic studies confirm 11.30% annual savings versus hospital-based intravenous care. Concurrently, oral delivery is expanding at 19.7% CAGR, on track to exceed USD 4.72 billion by 2031, driven by berotralstat and the anticipated approval of sebetralstat.

Intravenous treatments, though declining, remain critical for emergency departments and for patients requiring immediate high-dose intervention. Future pipeline assets targeting granule formulations for children aged 2-11 years will further broaden oral reach, reinforcing patient-centric care trajectories.

By Treatment Type: Long-term Prophylaxis Extends Market Momentum

Long-term prophylaxis accounted for 56.85% of 2025 revenue, anchoring the hereditary angioedema therapeutics market size at USD 3.33 billion. Physicians now favor preventive regimens because real-world studies show 77.00% fewer attacks and 52.00% lower emergency-department utilization versus on-demand approaches. Uptake accelerates as once-daily oral berotralstat and every-four-week subcutaneous lanadelumab remove logistical barriers, pushing prophylaxis prescriptions to half of all treated patients in the United States. At an 17.86% CAGR through 2031, prophylaxis will generate the largest absolute dollar expansion, while gene-editing candidates could eventually compress the segment by converting chronic dosing into one-time therapy.

By Patient Type: Type I Dominance Meets nC1-INH Precision Growth

Type I cases held 78.62% of 2025 revenue, translating to USD 4.61 billion and reflecting clear diagnostic criteria and abundant therapeutic options. The nC1-INH cohort is small but rising at 17.55% CAGR as next-generation sequencing exposes mutations in F12 and other genes previously undetected by standard assays. Off-label success with berotralstat plus emerging antisense agents signals imminent label expansions that could lift nC1-INH share above 10.00% by 2031, injecting fresh volume into the hereditary angioedema therapeutics market.

By Distribution Channel: Hospital Pharmacies Retain Control while Online Platforms Surge

Hospital pharmacies dispensed 45.32% of 2025 global sales, a USD 2.66 billion slice driven by initiation protocols and acute-care inventory requirements. Online and specialty-home platforms are the growth engine, advancing at 18.49% CAGR as secure cold-chain couriers and e-prescription portals streamline monthly refills. Digital channels bundle nurse coaching, adherence tracking, and automatic refill reminders, cutting missed doses by 30.00% and reinforcing payer support. As more patients transition to oral prophylaxis, online share is forecast to overtake hospital channels after 2028, further decentralizing the hereditary angioedema therapeutics market.

Geography Analysis

North America held 79.55% of 2025 revenue, reflecting robust reimbursement, fast-track regulatory designations, and dense specialty-pharmacy infrastructure. More than 1,200 U.S. physicians have adopted berotralstat, and payer alignment on outcomes contracts sustains high adherence. Canada leverages provincial formularies for coverage, while Mexico’s medical-tourism corridors attract regional HAE patients seeking advanced regimens.

Europe displays mature penetration, yet continued product cycling sustains value growth. EMA’s positive opinion on garadacimab and MHRA’s lanadelumab pediatric nod highlight regulatory momentum. France’s early-access program reported 65% clinically meaningful quality-of-life gains at six months, reinforcing payer confidence.

Asia-Pacific is the fastest-growing region at 17.44% CAGR, propelled by Japan’s regulatory clarity, China’s expanding rare-disease catalog, and advocacy-driven awareness. The 2024 Manila HAEi summit showcased collaborative efforts across 25 nations, though diagnostic and reimbursement heterogeneity remain hurdles. Investments in regional plasma fractionation and tele-education platforms are expected to mitigate supply and expertise gaps over time.

Competitive Landscape

Market concentration is moderate, with CSL Behring, Takeda, and BioCryst capturing the lion’s share through differentiated portfolios and integrated supply chains. CSL Behring’s plasma-to-product verticality offers cost leverage and barrier-to-entry advantages. Takeda secures positioning via the broadest global reach for lanadelumab, recently extended to pediatric populations. BioCryst capitalizes on first-in-class oral prophylaxis, with sales expected to top USD 600 million in 2025 on the back of strong U.S. and EU uptake.

Emerging disruptors focus on precision and convenience. Intellia’s CRISPR program seeks a single-dose cure, while KalVista targets oral on-demand relief. Ionis leverages antisense technology to balance efficacy and dosing convenience. Digital-health overlays for adherence monitoring and AI-enabled attack prediction are nascent differentiators, yet integration across therapy and service layers remains early.

Hereditary Angioedema Therapeutics Industry Leaders

Takeda Pharmaceutical Co. Ltd

CSL Behring

Pharming Group NV

BioCryst Pharmaceuticals

KalVista Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BioCryst reported Q1 2025 berotralstat revenue of USD 134.2 million and filed a pediatric NDA for oral granules.

- March 2025: FDA cleared fitusiran for hemophilia prophylaxis, underscoring sustained support for orphan innovations.

- February 2025: BioCryst launched berotralstat in Portugal, now reimbursed in all major Western European markets except the Netherlands.

- February 2025: CSL Behring published four-year durability data for Hemgenix, demonstrating 90% bleeding-rate reduction.

- January 2025: Grifols confirmed Q1 U.S. rollout of Yimmugo immunoglobulin with projected USD 1 billion seven-year sales.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hereditary angioedema (HAE) therapeutics market as all prescription products, plasma-derived C1-esterase inhibitors, recombinant biologics, monoclonal antibodies, oral or injectable kallikrein inhibitors, and bradykinin B2 receptor antagonists used worldwide to treat or prevent acute attacks in Type I, Type II, or nC1-INH HAE patients.

Scope Exclusions: Diagnostics, non-prescription symptom relievers, and experimental gene-editing platforms that remain outside commercial channels are excluded from this sizing.

Segmentation Overview

- By Drug Class

- C1 Esterase Inhibitor

- Selective Bradykinin B2 Receptor Antagonist

- Kallikrein Inhibitor

- Other Drug Classes

- By Route of Administration

- Intravenous

- Sub-cutaneous Injection

- Oral

- By Treatment Type

- Acute / On-Demand

- Long-term Prophylaxis

- By Patient Type

- Type I (C1-INH deficiency)

- Type II (C1-INH dysfunction)

- nC1-INH (Type III & others)

- By Distribution Channel

- Hospital Pharmacies

- Specialty & Home-infusion Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts held interviews with hospital pharmacists, clinical immunologists, and reimbursement specialists across North America, Europe, and select Asia-Pacific markets. These discussions validated treated-patient estimates, real-world dosing intensity, and emerging switch trends from injectable to oral prophylaxis, allowing us to tune model assumptions and stress-test preliminary outputs.

Desk Research

We began with structured queries across Orphanet prevalence data, the U.S. FDA Orphan Drug Database, EMA public assessment reports, and national rare-disease registries to map treated patient pools by age and mutation profile. Trade group portals such as HAEi, OECD health expenditure dashboards, and customs shipment logs for plasma products helped us benchmark therapy penetration and pricing corridors. Company 10-Ks, quarterly calls, and investor decks clarified net revenue splits between on-demand and prophylaxis lines. Select paid repositories, including D&B Hoovers for financial breakouts and Questel for patent velocity, supplied additional competitive context. The sources listed are illustrative; many others were consulted for triangulation and clarification.

Market-Sizing & Forecasting

A top-down incidence-to-treated-population build was run, using country-level prevalence, diagnostic latency, and therapy-eligibility ratios; results were cross-checked with a bottom-up roll-up of manufacturer sales and sampled average selling prices. Key model inputs include annual diagnosed prevalence shifts, share of patients on long-term prophylaxis, dosing weight averages, ASP erosion following competitive entries, and regional reimbursement ceilings. Forecasts employ a multivariate regression seeded with historical uptake curves and adjusted through scenario analysis for upcoming launches and patent expiries. Where bottom-up gaps persisted, midpoint estimates were imputed using regional analogs and primary insights.

Data Validation & Update Cycle

Outputs pass anomaly screening, variance checks against independent benchmarks, and multi-level analyst review before sign-off. Reports refresh yearly, and interim updates are triggered by pivotal trial readouts, regulatory approvals, or major pricing revisions, ensuring clients receive our latest calibrated view.

Why Mordor's Hereditary Angioedema Therapeutics Baseline Commands Proven Reliability

Published values often diverge because firms use different treated-population pools, therapy baskets, and forecast cadences. Our approach, grounded in diagnosed prevalence and validated dosing patterns, keeps the scope precise yet complete for decision-makers.

Key gap drivers include some publishers folding pipeline molecules into current revenue, others assuming uniform ASPs across regions, and a few applying linear prevalence growth without adjusting for shortening diagnostic delays or switching to oral agents.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.86 B (2025) | Mordor Intelligence | |

| USD 6.53 B (2025) | Global Consultancy A | Includes future-pipeline revenues and global average ASP without regional weighting |

| USD 4.10 B (2023) | Industry Journal B | Earlier base year and exclusion of prophylactic segment beyond C1-INH class |

These comparisons show that Mordor's disciplined scope selection, dual-path modeling, and annual refresh cadence yield a balanced, transparent baseline that stakeholders can readily audit and reproduce for confident planning.

Key Questions Answered in the Report

What is the current Global Hereditary Angioedema Therapeutics Market size?

The Global Hereditary Angioedema Therapeutics Market is projected to register a CAGR of 16.56% during the forecast period (2026-2031)

What is the current size of the hereditary angioedema therapeutics market?

The market was valued at USD 6.83 billion in 2026 and is projected to reach USD 14.69 billion by 2031.

Which region is expected to post the fastest growth through 2031?

Asia-Pacific is forecast to expand at a 17.44% CAGR, outpacing all other regions.

Which treatment class holds the largest revenue share today?

C1 esterase inhibitors accounted for 60.92% of global revenue in 2025.

How quickly are oral kallikrein inhibitors growing?

Oral kallikrein inhibitors are advancing at a 19.12% CAGR, supported by strong uptake of berotralstat.

What are typical annual therapy costs for hereditary angioedema patients?

Annual prophylaxis costs frequently exceed USD 500,000 per patient, posing budget pressure for payers.

Which companies dominate the competitive landscape?

CSL Behring, Takeda, and BioCryst collectively controlled just over 60% of 2025 global revenue.

Page last updated on: