Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

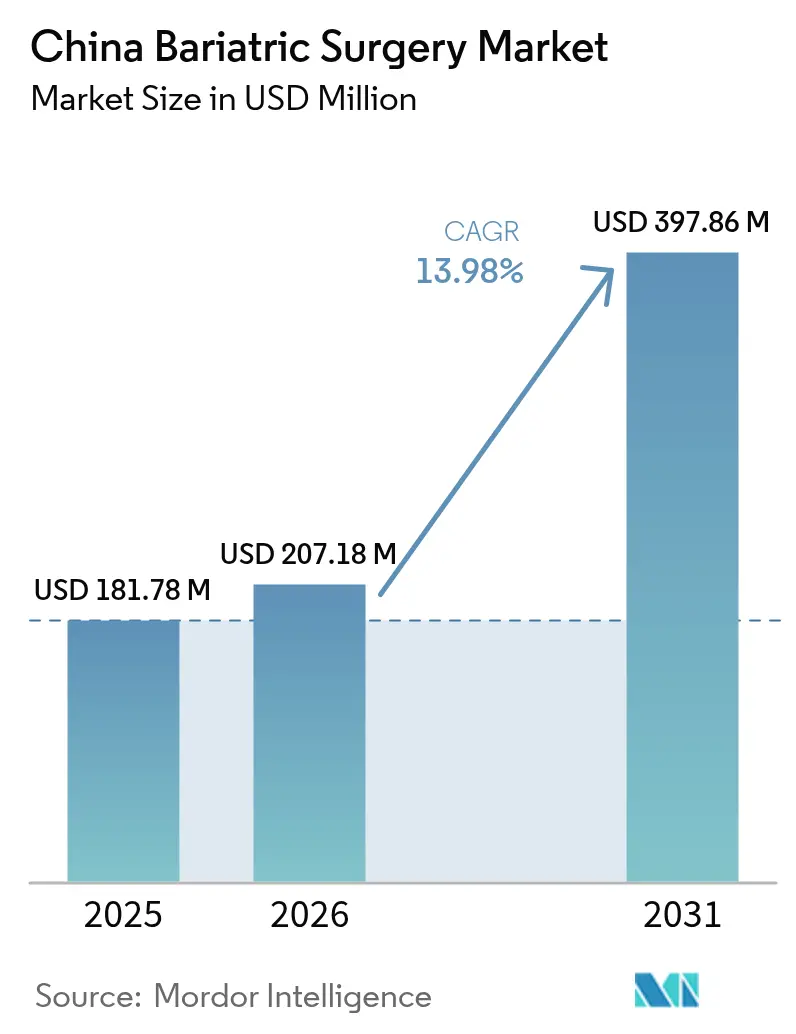

| Base Year Market Size (2025) | USD 181.78 Million |

| Market Size (2026) | USD 207.18 Million |

| Market Size (2031) | USD 397.86 Million |

| Growth Rate (2026 - 2031) | 13.98% CAGR |

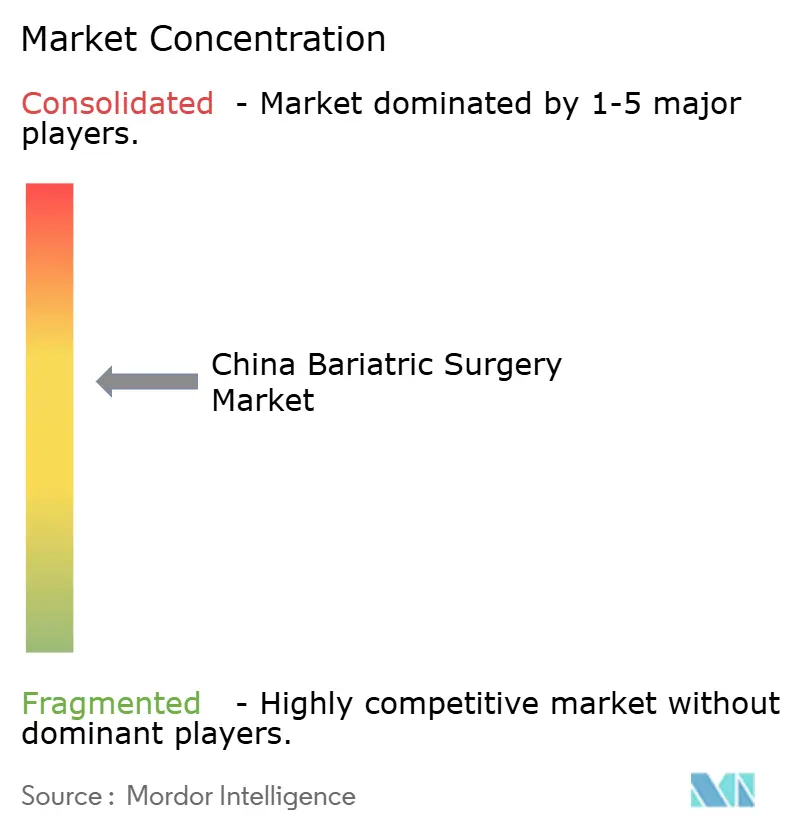

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Bariatric Surgery Market Analysis by Mordor Intelligence

The China bariatric surgery market size was valued at USD 181.78 million in 2025 and estimated to grow from USD 207.18 million in 2026 to reach USD 397.86 million by 2031, at a CAGR of 13.98% during the forecast period (2026-2031). Escalating obesity prevalence, wider surgical eligibility, and continual hospital investment in minimally invasive equipment anchor this trajectory. Government guidelines published in October 2024 lowered BMI thresholds, directly enlarging the candidate pool for metabolic procedures and stimulating device demand. Large public hospitals are modernizing operating suites to include robotic and advanced laparoscopic systems, then cascading best-practice protocols into provincial networks. Parallel pharmaceutical progress strengthens early weight-loss management but also encourages multidisciplinary weight-control programs that ultimately channel severe patients toward surgery. Meanwhile, domestic manufacturers accelerate product localization, compressing acquisition costs and ensuring rapid post-sale service—advantages that reinforce purchasing decisions by publicly funded institutions.

Key Report Takeaways

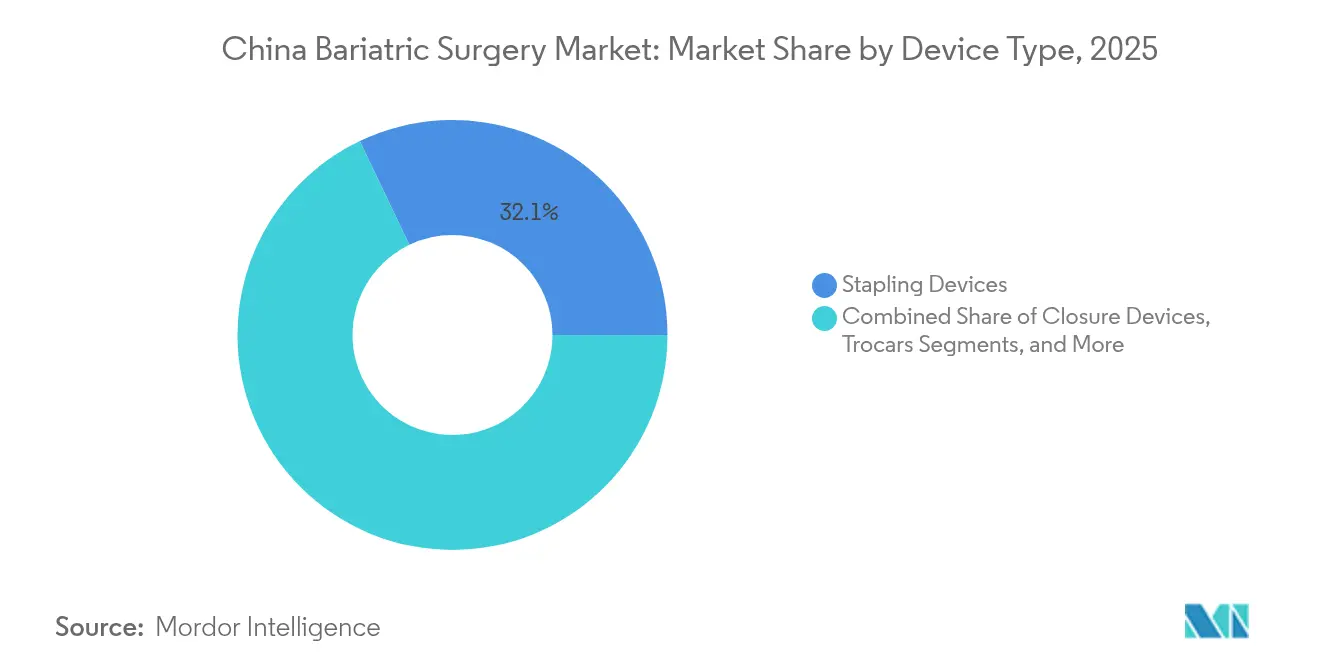

- By device type, stapling instruments held 32.10% of the China bariatric surgery market share in 2025, and gastric balloons are projected to grow at a 15.42% CAGR through 2031.

- By procedure, sleeve gastrectomy captured 74.95% revenue share in 2025; gastric bypass is forecast to expand at a 15.10% CAGR through 2031.

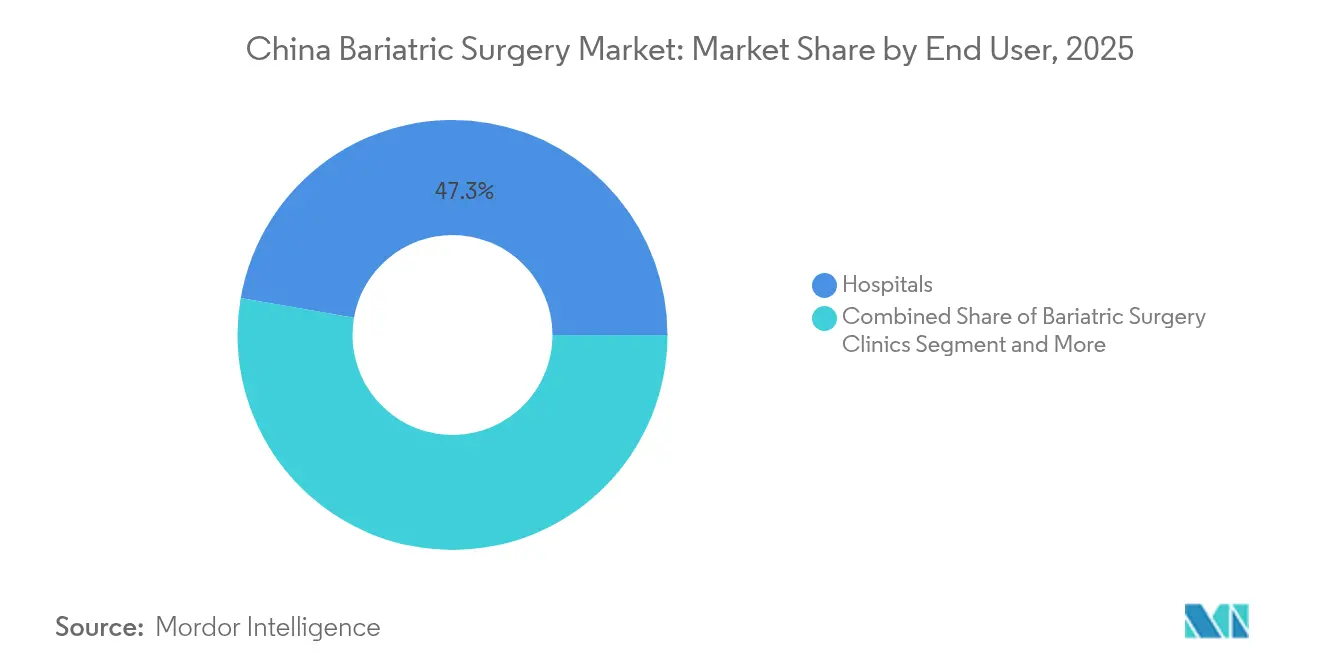

- By end user, hospitals commanded 47.25% of the China bariatric surgery market size in 2025, while specialized bariatric clinics are advancing at a 15.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Bariatric Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity and metabolic disease prevalence | +4.2% | Tier-1 cities and rapidly urbanizing provinces | Long term (≥ 4 years) |

| Government guidelines lowering BMI surgical thresholds | +2.8% | Nationwide, earliest roll-out in major municipalities | Medium term (2-4 years) |

| Rapid adoption of minimally invasive and robotic platforms | +2.1% | Provincial capitals and teaching hospitals | Medium term (2-4 years) |

| Inpatient reimbursement that favors longer peri-operative stays | +1.5% | Universal insurance system, region-specific tariffs | Short term (≤ 2 years) |

| NMPA approval of domestic staple-line reinforcement pads | +1.3% | Leading medical centers | Short term (≤ 2 years) |

| Expansion of the national COMES registry | +0.9% | Countrywide data network | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Obesity and Metabolic Disease Prevalence

Adult overweight and obesity combined are projected to reach 65.3% by 2030, exposing more than 300 million residents to cardiometabolic risk. The National Health Commission warns that obesity-related disorders could consume over RMB 400 billion in direct medical expenditure each year[1]National Health Commission, “Year of Weight Management Implementation Plan,” nhc.gov.cn. Urban dietary shifts toward calorie-dense convenience food, reduced physical activity, and heightened stress collectively accelerate BMI escalation, especially in Beijing, Shanghai, Guangzhou, and Shenzhen. Healthcare payers respond by endorsing surgical therapy for severe disease because longitudinal data confirm superior glycemic control and durable weight loss compared with medication alone. The rising case load drives hospital administrators to expand operating theater capacity, recruit dietitians, and embed behavioral counseling inside peri-operative pathways for optimal long-term outcomes.

Government Guidelines Lowering BMI Thresholds for Surgery Eligibility

The October 2024 National Health Commission obesity guideline introduced BMI ≥ 32.5—or ≥ 27.5 with comorbid diabetes or hypertension—as formal criteria for metabolic surgery. The rule immediately doubles the surgical candidate pool relative to former consensus statements, forcing tertiary hospitals to scale bariatric wards and fellowship programs at a pace. Multidisciplinary evaluation—nutritionist, endocrinologist, surgeon, psychologist—became mandatory for listing approval, driving demand for case managers versed in long-term follow-up. Tier-1 hospitals adopted the standard within six months, and provincial centers are mandated to conform by 2026. Standardized thresholds also strengthen payer confidence, simplifying claims adjudication and reducing out-of-pocket variability for patients.

Rapid Adoption of Minimally Invasive and Robotic Platforms

Teaching hospitals in Shanghai, Beijing, and Shenzhen upgraded to articulated 3-D laparoscopic towers and locally produced robotic systems during 2025, shortening learning curves for complex anastomosis. Domestic vendors offer service contracts, sterile supply packs, and Chinese-language training modules that align with hospital procurement rules. For patients, smaller ports translate to diminished postoperative pain, faster mobilization, and shorter sick leave—an increasingly salient metric for urban professionals. Surgeons credit articulating end effectors and stable camera control for boosting staple-line integrity and excision precision, thereby mitigating leaks and hemorrhage. These tangible clinical improvements, coupled with measured operating times, raise institutional enthusiasm and consolidate robotic allocation into routine bariatric workflow.

Inpatient Reimbursement Rules That Financially Favor Longer Peri-Operative Stays

China’s Diagnosis-Related Groups (DRG) still reimburses bariatric inpatients at incremental daily rates, an incentive that offsets fixed costs of specialist nursing, micronutrient assessment, and behavioral coaching. Consequently, most centers schedule a standard five-night pathway, allowing thorough mobilization instruction and dietary transition. Insurers gain long-run savings from lower readmission and diabetes remission, while hospitals remain budget-neutral or slightly positive on each case. Provincial tariffs differ, but the general structure assures sustainable cash flow for new bariatric service lines, prompting county-level facilities to partner with metropolitan mentors in shared-care arrangements.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device costs | -1.8% | Tier-2/3 cities and rural counties | Medium term (2-4 years) |

| Shortage of fellowship-trained surgeons outside Tier-1 hubs | -1.2% | Inland provinces | Long term (≥ 4 years) |

| Uptake of GLP-1 drugs cannibalizing mild-obesity surgical demand | -0.7% | Urban commercial insurance markets | Medium term (2-4 years) |

| Litigation over micronutrient deficiencies raising insurer scrutiny | -0.4% | Metropolitan courts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure and Device Costs

Total inpatient charges range from RMB 40,000 to RMB 80,000 (USD 5,600-11,200), reflecting imported energy devices, staplers, and prolonged admission time. National insurance reimburses diabetes remission-linked procedures but often excludes pure weight-loss indications, leaving patients to finance residual balances. Device localization trims list prices, yet margins remain thin under volume-based purchasing policies. District-level hospitals struggle to absorb significant capital expenditure for robotics, delaying geographic diffusion and perpetuating treatment disparities between coastal and inland regions.

Shortage of Fellowship-Trained Bariatric Surgeons Outside Tier-1 Cities

Only 1,250 surgeons nationwide report formal metabolic surgery certification, with three-quarters concentrated in large municipalities. Fellowship slots are limited and competitive, compelling provincial clinicians to attend short-course workshops that inadequately cover complex anastomosis. Surgeon scarcity protracts waiting lists, suppresses annual throughput, and forces patients to travel long distances for specialty care. Government-subsidized training fellowships and tele-mentoring programs attempt to accelerate capacity expansion, but measurable workforce equilibrium is unlikely before 2029.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Staplers Retain Lead While Balloons Accelerate

Stapling systems accounted for 32.10% of the China bariatric surgery market in 2025, reflecting their indispensability for longitudinal sleeve creation and gastrojejunostomy construction. The category’s continued dominance rests on iterative reload innovation and new reinforcement accessories that optimize hemostasis. Domestic brands vie on price under centralized procurement, gradually displacing imports in county-level centers. Meanwhile, gastric balloons logged a 15.42% CAGR forecast to 2031. Enhanced silicone materials and outpatient endoscopic placement protocols shorten procedure times, permitting rapid adoption within specialized clinics. As volume rises, ancillary demand for closure devices, trocars, and hemostats grows in parallel, though at lower incremental rates because these consumables already form part of standardized laparoscopic kits. Gastric bands fall out of favor amid long-term erosion risk, and electrical stimulation devices remain niche for investigational cohorts.

Gastric emptying systems and transintestinal stents occupy an emerging frontier, appealing to patients seeking less invasive yet effective interventions. Their commercial trajectory hinges on longitudinal efficacy evidence and NMPA reimbursement categorization. Collectively, these device-level shifts underscore patient appetite for reversible or step-up therapies and providers’ search for differentiated offerings that widen clinical portfolio without inflating capital cost.

By Procedure Type: Sleeve Gastrectomy Continues to Dominate

Sleeve gastrectomy represented 74.95% of all operated cases in 2025, according to the COMES registry, mirroring surgeons' comfort with the technique’s shorter operative time and favorable complication profile. This procedure captured the bulk of starter programs in provincial hospitals because it requires fewer stapler reloads and no jejuno-jejunostomy. Concurrently, gastric bypass is projected to expand at 15.10% CAGR as fellowship-trained teams mature technically and as evidence consolidates around its superior metabolic remission for advanced diabetes. Adjustable gastric banding declines due to late erosion, port malfunction, and high explant rates. Noninvasive balloon and endoscopic sleeve gastroplasty comprise a modest but rising contribution, especially within private standalone clinics targeting cash-pay consumers who prefer day-surgery settings.

Revision surgery constitutes a notable sub-segment as early-generation band patients now present with weight regain or reflux, necessitating conversion to bypass. As the operative cohort ages, demand for conversion and complication management will intensify, supporting bariatric subspecialization within hepatobiliary divisions and raising the value of outcomes-tracked, risk-stratified joint databases.

By End User: Specialized Clinics Gain Momentum

Hospitals provided 47.25% of procedure volume in 2025, leveraging integrated anesthesiology, critical care, and imaging to tackle complex or high-BMI patients. These tertiary centers also host structured obesity boards and clinical trials, positioning themselves as referral anchors. In parallel, dedicated bariatric clinics exhibit 15.28% CAGR through 2031, capitalizing on streamlined scheduling, concierge preoperative testing, and bundled follow-up plans. Such clinics deliver predictable throughput and patient-centric amenities, drawing self-pay and employer-sponsored customers from metropolitan catchment areas. Ambulatory surgery centers and specialty hospitals represent a hybrid pathway for straightforward balloons or low-risk sleeves, contingent on local regulation permitting same-day discharge.

Specialized clinics expand via physician-led partnerships, often leasing operating theater time in contiguous private facilities, thereby minimizing upfront infrastructure investments. Their strategic advantage lies in brand messaging around holistic weight-loss journeys, supported by digital coaching applications that remind patients to record meals, track steps, and attend virtual support groups.

Regulatory Landscape

Bariatric surgery device commercialization in China is governed by the National Medical Products Administration (NMPA) under the Regulations on Supervision and Administration of Medical Devices (State Council Order No. 739). Devices are managed through a risk-based system (Class I filing, and Class II and Class III registration), which shapes clinical evidence, quality-system, and post-market requirements for staples, energy devices, and implantable/endoscopic obesity-treatment devices used in metabolic and bariatric care.

On the care-delivery side, the National Health Commission (NHC) set a national framework for obesity management through its October 2024 obesity guideline that formalized BMI criteria for metabolic surgery and reinforced multidisciplinary pathways. Public policy also elevated obesity as a health-system priority via the Weight Management Year Implementation Plan (June 2024) and the March 2025 notice on establishing weight-management clinics, which supported hospital service-line buildouts that feed surgical volumes. From a manufacturing and compliance standpoint, an additional milestone is the updated medical-device Good Manufacturing Practice framework taking effect on November 1, 2026, raising the bar for domestic and localized suppliers serving hospital tenders.

Competitive Landscape

Market concentration is moderate. Medtronic and Johnson & Johnson maintain first-mover advantage in advanced stapling and energy platforms, yet domestic entrants narrow the technology gap while pricing 25-30% lower under national tenders. Local champions emphasize onshore manufacturing, bilingual user interfaces, and rapid after-sales engineering support, a value proposition that resonates with state hospitals. Device interoperable ecosystems—integrating robotic arms, reloads, sealers, and digital logbooks—create switching costs that incumbents exploit to consolidate share.

Strategic collaborations proliferate: domestic robotics developers license articulation algorithms from academic laboratories, while multinational component suppliers sign joint ventures to qualify for “made-in-China” procurement quotas. Medtronic's 2025 10-K filing highlights China as comprising approximately 7% of global revenues while noting ongoing tender pricing pressures and competitive robotic challenges affecting advanced stapling performance Medtronic[3]Medtronic, “Form 10-K 2025,” medtronic.com. Hospitals negotiate bundled service models combining instrumentation leasing with surgeon proctoring and annual maintenance, smoothing budget spikes and aligning usage with payment streams. Some vendors pilot cloud-connected staplers that archive firing analytics into the COMES registry, enhancing risk stratification and demonstrating outcomes accountability to payers. Persistent cost-containment policy and accelerating local innovation suggest that overall rivalry will sharpen, incentivizing scale economies and perhaps catalyzing the acquisition of niche startups by diversified device conglomerates.

China Bariatric Surgery Industry Leaders

Olympus Corporation

ReShape Lifesciences Inc

Reach surgical

Boston Scientific Corporation

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hospital-led implementation of national obesity programs continues to open whitespace for integrated care models that connect weight-management clinics, multidisciplinary evaluation (endocrinology, nutrition, psychology, surgery), and standardized peri-operative follow-up. The NHC obesity guideline published in October 2024 lowered BMI thresholds for surgical eligibility, expanding the pool of patients who enter these structured pathways and increasing the importance of scalable tools such as case-management workflows, standardized laparoscopic kits, and outcome-tracked devices that fit into public-hospital procurement and quality reporting.

A second opportunity is the step-up continuum between lifestyle/pharmacotherapy and bariatric surgery, particularly in endoscopic or minimally invasive obesity therapies that can be deployed in high-throughput settings. A concrete market signal came from Hangzhou Tangji Medical Technology: its Gastric Bypass Stent System received NMPA approval as a Class III innovative medical device in January 2024, and the company filed an IPO prospectus with the Hong Kong Stock Exchange in February 2026 to fund further development and commercialization. In parallel, device localization and service-contract models used by domestic vendors and multinational incumbents align with tender-driven cost pressure, making total-cost-of-ownership, training, and post-sale support differentiators as robotic and advanced laparoscopic platforms diffuse through tiered hospital networks.

Recent Industry Developments

- February 2026: Hangzhou Tangji Medical Technology filed an IPO prospectus with the Hong Kong Stock Exchange to support commercialization of its Gastric Bypass Stent System. The move highlights investor-backed scaling for endoscopic obesity interventions that sit between lifestyle/pharmacotherapy and traditional bariatric surgery, reinforcing competitive pressure on established device pathways.

- March 2025: China issued a notice on establishing weight-management clinics, pushing capable medical institutions to formalize clinic-based obesity pathways. Standardized referral, multidisciplinary evaluation, and follow-up infrastructure can increase downstream bariatric case flow and raise demand for procedure-ready laparoscopic and endoscopic toolchains within hospital networks.

- June 2024: China launched the Weight Management Year Implementation Plan, marking 2024 to 2026 as a national policy window for obesity prevention and treatment programs. The directive accelerated service-line planning at tertiary hospitals and supports broader adoption of standardized protocols that influence bariatric surgery capacity, training, and device procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue generated in China from bariatric surgery procedures and the related specialized devices used to perform them, across open and laparoscopic approaches, as captured through provider and supplier activity.

Scope exclusions: Cosmetic weight loss procedures, non-surgical weight management programs, and general surgical consumables that are not bariatric-specific are excluded.

Segmentation Overview

- By Device Type

- Assisting Devices

- Suturing Devices

- Closure Devices

- Stapling Devices

- Trocars

- Other Assisting Devices

- Implantable Devices

- Gastric Bands

- Electrical Stimulation Devices

- Gastric Balloons

- Gastric Emptying Systems

- Other Devices

- Assisting Devices

- By Procedure Type

- Sleeve Gastrectomy

- Gastric Bypass

- Adjustable Gastric Banding

- Noninvasive Bariatric Surgery

- Others

- By End User

- Hospitals

- Bariatric Surgery Clinics

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base demand pool and the clinical context behind procedure adoption in China, before any numbers were finalized. We reviewed public sources such as China health statistics releases, World Health Organization obesity indicators, OECD health data where comparable, and peer reviewed clinical journals that discuss bariatric outcomes and utilization patterns.

To translate clinical activity into market value, we also used hospital and academic society publications (including obesity and metabolic surgery registries), customs and trade statistics for relevant device categories, and company annual reports and investor presentations for directional revenue exposure. In parallel, a paid subscription focused on company financials and intelligence and a paid patent database were used selectively to track product launches and estimate pricing direction when public disclosures were limited. These desk sources are illustrative only, and additional public materials were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was completed through expert interviews and structured surveys with bariatric surgeons, hospital procurement and operating room teams, clinic administrators, and local distribution and service participants across major Chinese treatment hubs. Respondent input was used to confirm procedure mix, typical device bundles per case, and pricing ranges, and then to pressure test utilization and growth assumptions against real booking and capacity signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | |

| Mid tier: 60% | Functional/Unit leaders: 31% | |

| Smaller Players: 14% | Managers: 56% |

Market-Sizing & Forecasting

The core model uses a top-down build where the treated patient pool is reconstructed from obesity prevalence, clinical eligibility, and the share of patients who actually receive surgery, and then converted into value using procedure mix and device intensity per procedure. After the first total is obtained, it is checked using selective bottom-up approximations, including supplier and channel feedback on device volumes, sampled pricing for stapling and closure sets, and hospital-level throughput patterns. Adjustments are made where the two views disagree.

Key inputs that were tracked include annual bariatric case volumes, the split between sleeve gastrectomy and bypass-type procedures, average devices used per case (for example staplers, cartridges, trocars, and closure tools), average selling price movement by device class, and hospital adoption of laparoscopic approaches. For forecasting, scenario analysis was used because utilization is sensitive to policy emphasis on obesity care, surgeon training capacity, and patient affordability, and primary experts helped us choose realistic ranges for each driver. When primary feedback suggested missing volumes in smaller cities, the gap was handled by applying utilization ranges to eligible population blocks and then rechecking the implied surgery rate against clinical norms.

Data Validation & Update Cycle

Model outputs were validated in several steps, starting with internal consistency checks across procedure volumes, implied pricing, and device-per-case logic, followed by variance checks against independent signals from public clinical publications and trade indicators. Outliers were investigated and, where needed, assumptions were re-tested through follow-up calls with the most relevant respondent type.

Before sign-off, a separate analyst review confirms the arithmetic, units, and year mapping, and then ensures the narrative aligns with the quantified model. The report is refreshed annually, and interim updates are triggered when material events occur, such as policy changes, reimbursement shifts, or major technology introductions. Right before delivery, a final pass is completed so the published view reflects the latest update.

Mordor Intelligence's China Bariatric Surgery Market Size Versus Other Published Estimates

Published numbers for China bariatric surgery often do not match because the scope can shift between procedure revenue, device revenue, or a blended view, and because different authors anchor to different base years. Differences also show up when pricing is treated as a single national average versus a mix of hospital tiers and city classes.

The main gap comes from whether surgery fees and follow-up care are counted together with device sales, where Mordor Intelligence counts the bariatric surgery market using a defined procedure and device scope tied to open and laparoscopic cases, rather than rolling in broader weight management services.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 181.78 M (2025) | |

| Industry Research Group A | USD 120.00 M (2023) | Uses an earlier base year and appears to rely more on historical revenue reporting, which can understate recent case growth and does not always make procedure mix and device-per-case assumptions explicit. |

| Regional Research Group B | USD 320.00 M (2031) | A longer-range projection can look higher if aggressive uptake is assumed for surgery adoption and ASP progression, and if the method does not clearly separate device revenue from total procedure and care spending. |

Overall, the spread is mainly explained by scope boundaries, base-year choice, and how procedure volumes and pricing are built into the model. By keeping assumptions tied to observable case drivers and rechecking them with provider and channel feedback, the final estimate stays traceable and repeatable even when public data is fragmented.

Key Questions Answered in the Report

How large is the China bariatric surgery market in 2026 and what is its projected value by 2031?

The market is valued at USD 207.18 million in 2026 and is forecast to rise to USD 397.86 million by 2031, registering a 13.98% CAGR.

Which procedure type currently dominates surgical volume in China?

Sleeve gastrectomy holds 74.95% of 2025 procedures, making it the leading surgical option.

What factors are driving the rapid uptake of robotic platforms in Chinese bariatric operating rooms?

Hospitals upgrade to robotic and advanced laparoscopic systems for greater precision, shorter recovery, local service contracts, and favorable procurement pricing.

How do new BMI eligibility guidelines affect patient access to metabolic surgery?

The National Health Commission’s 2024 guidelines lowered BMI thresholds, effectively doubling the eligible patient population and prompting hospitals to expand capacity.

Which device segment is growing the fastest and why?

Gastric balloons are projected to advance at a 15.42% CAGR through 2031, benefiting from minimally invasive endoscopic placement and patient preference for reversible options.

What are the main challenges restraining growth in inland provinces and rural counties?

High device costs, limited reimbursement, and a shortage of fellowship-trained surgeons hinder procedure adoption outside major urban centers.

Page last updated on: