Interspinous Spacers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

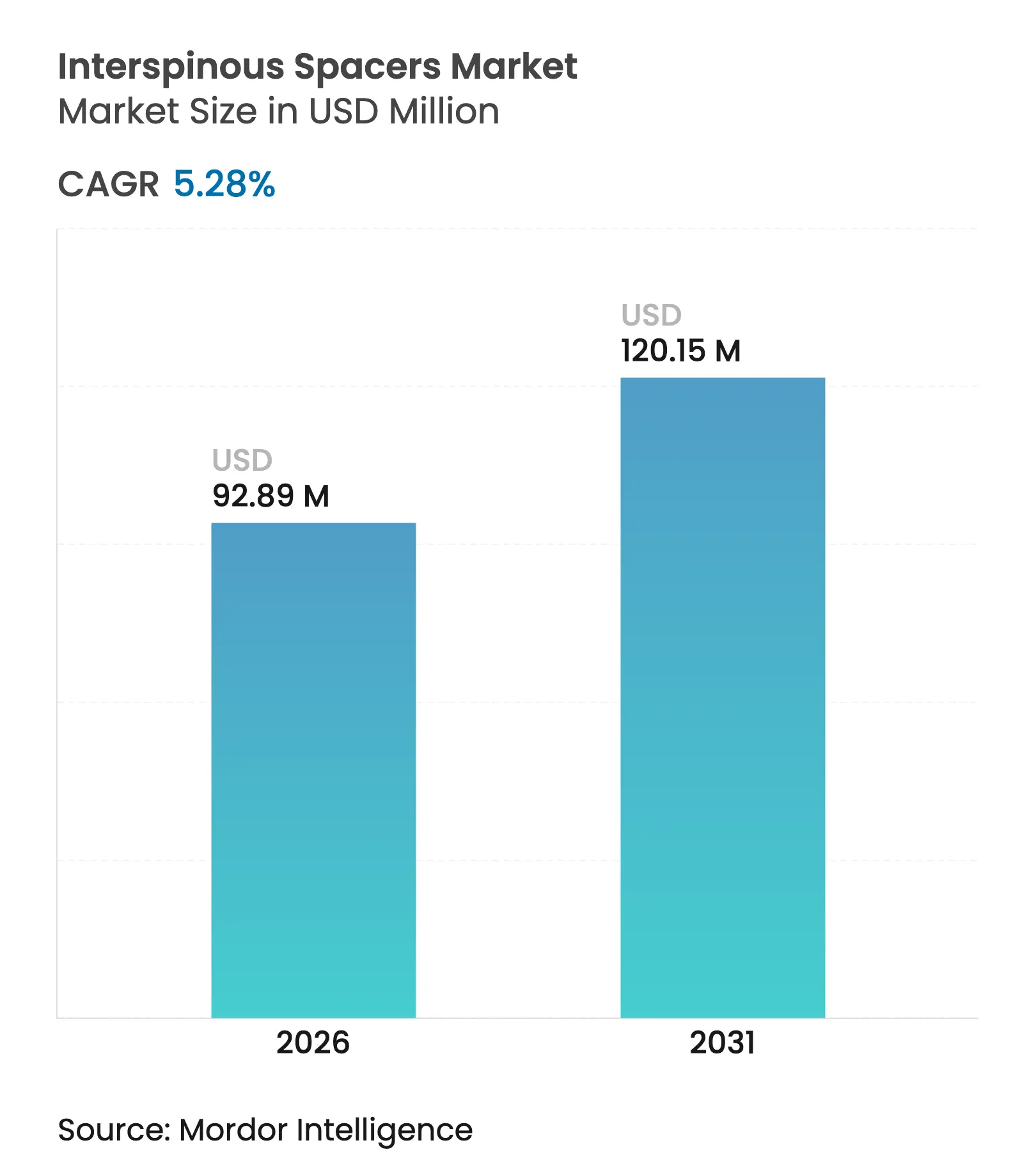

| Market Size (2026) | USD 92.89 Million |

| Market Size (2031) | USD 120.15 Million |

| Growth Rate (2026 - 2031) | 5.28 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Interspinous Spacers Market Analysis by Mordor Intelligence

The interspinous spacers market size is expected to grow from USD 88.23 million in 2025 to USD 92.89 million in 2026 and is forecast to reach USD 120.15 million by 2031 at 5.28% CAGR over 2026-2031. Demand continues to expand as surgeons replace traditional fusion with motion-preserving implants that decompress lumbar stenosis without rigid fixation. Commercial traction is supported by the ageing demographic, growing outpatient spine volumes and steady reimbursement reforms that reward minimally invasive care. Device makers differentiate through biomaterial innovation, hybrid designs that balance motion with stability and data-enabled follow-up systems that document outcomes. Asia-Pacific investment in new surgical centres and North American payer incentives for same-day discharge further strengthen the interspinous spacers market outlook.

Key Report Takeaways

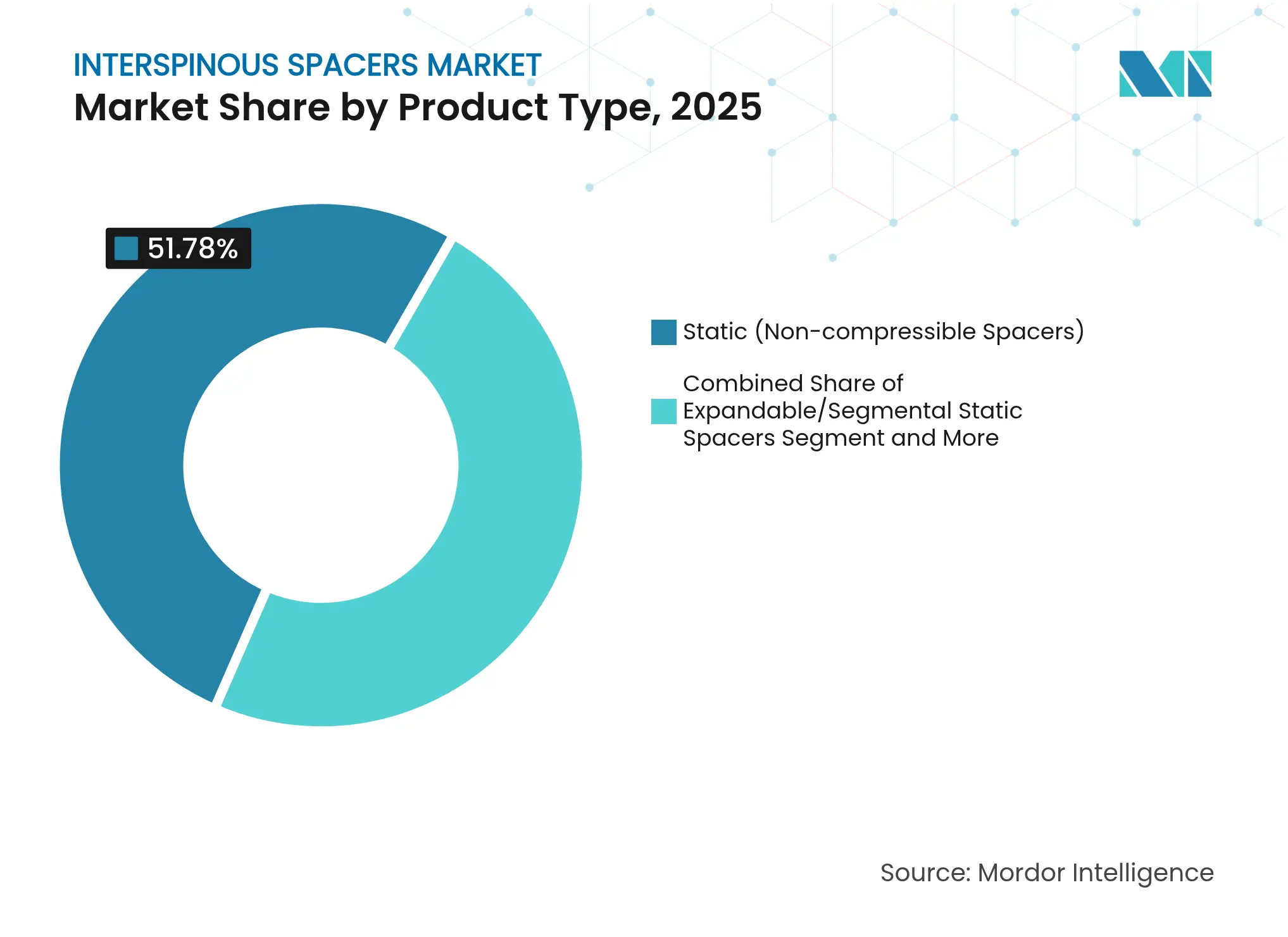

- By product type, static non-compressible devices led with 51.78% revenue share in 2025, whereas hybrid dynamic-static systems are projected to grow at a 11.63% CAGR through 2031.

- By biomaterial, titanium and titanium alloys accounted for 41.96% of the interspinous spacers market share in 2025, while bio-resorbable polymers are set to expand at a 9.32% CAGR to 2031.

- By procedural approach, open posterior techniques held 57.88% of the 2025 interspinous spacers market size and percutaneous methods show the highest projected CAGR at 9.98% over 2026-2031.

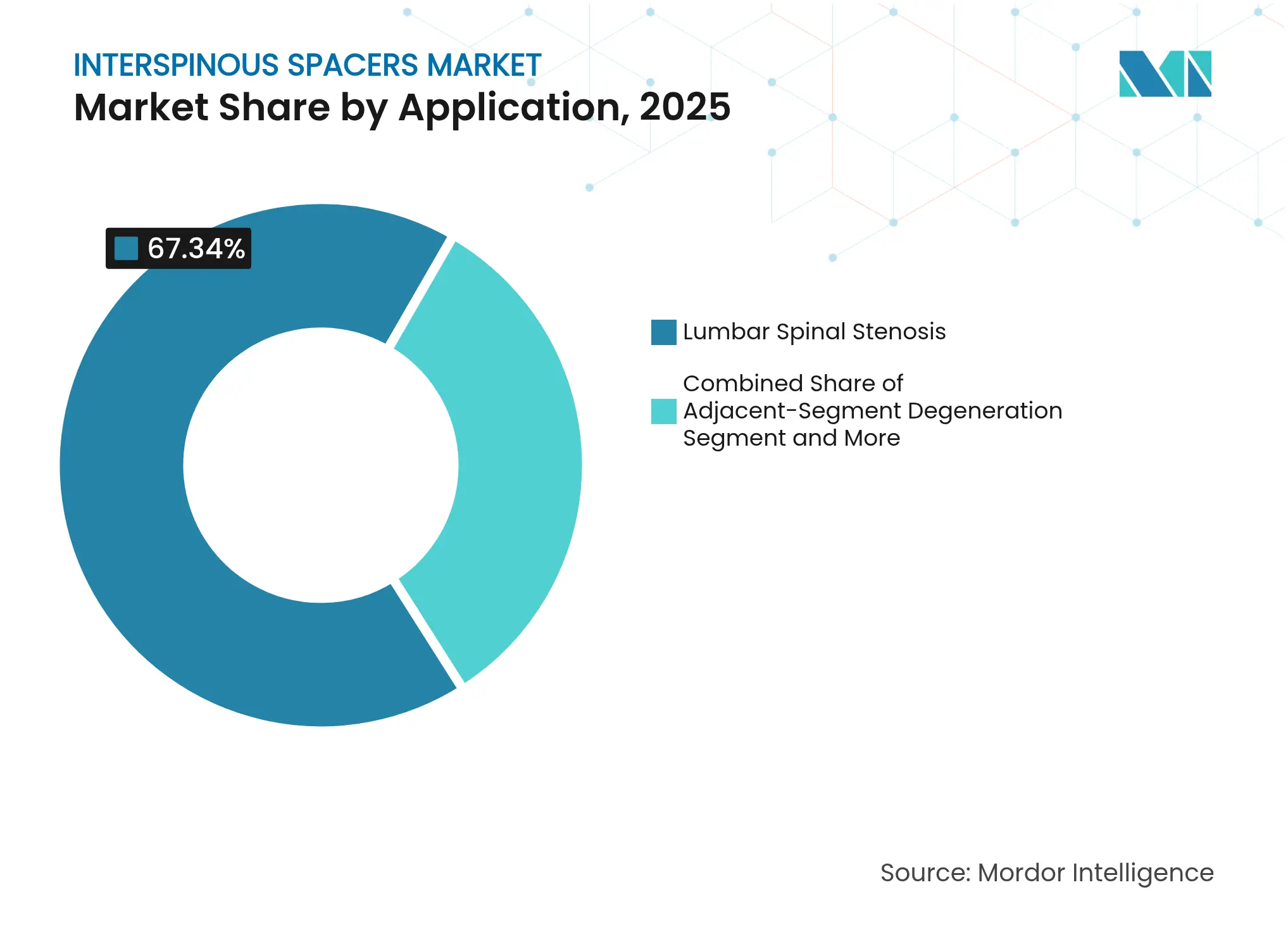

- By application, lumbar spinal stenosis captured 67.34% of 2025 revenue; adjacent-segment degeneration is on track for an 10.59% CAGR to 2031.

- By end-user, hospitals commanded 64.11% of the 2025 interspinous spacers market size, while ambulatory surgical centres are advancing at a 9.84% CAGR.

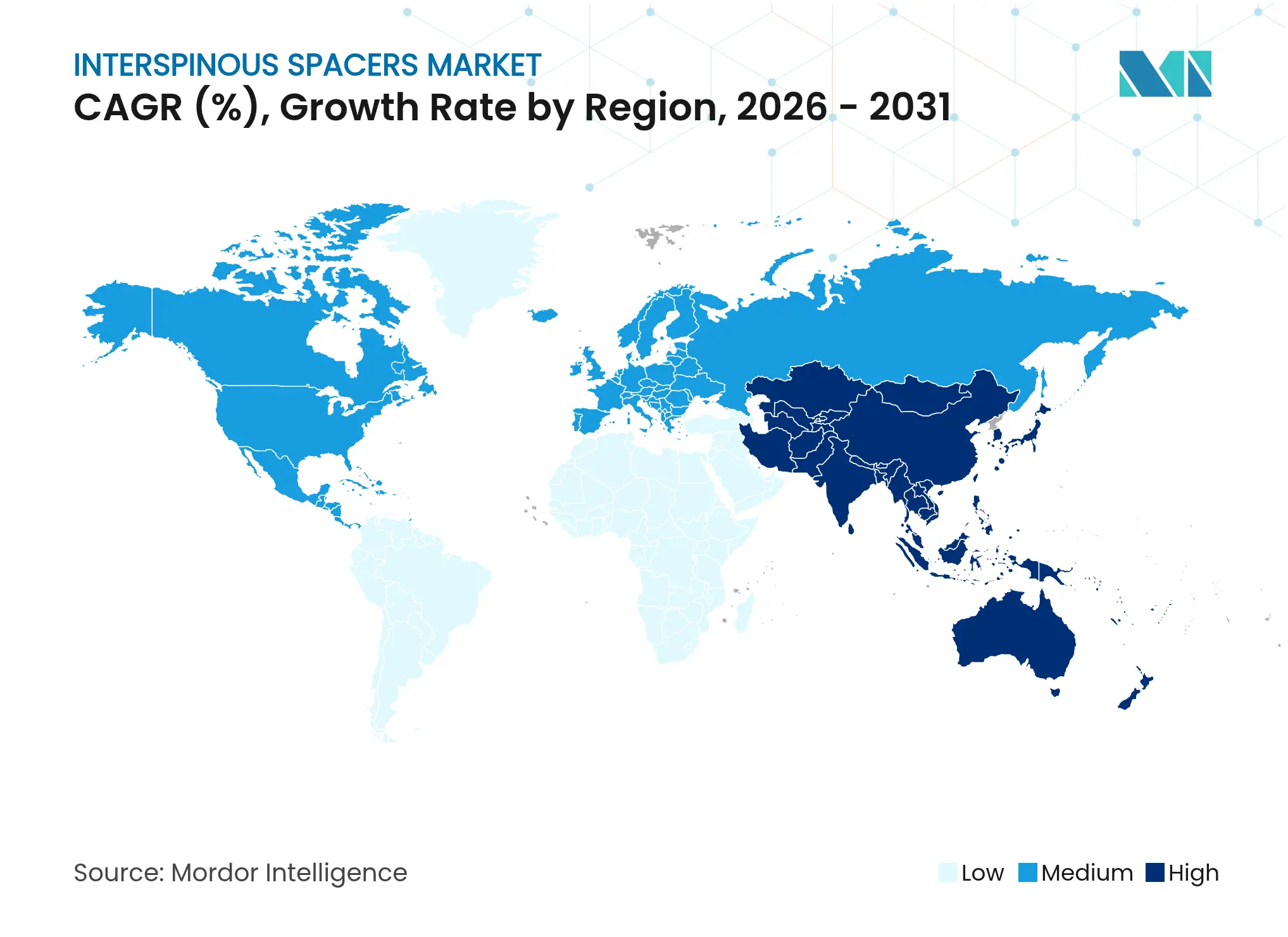

- By geography, North America led with 41.12% revenue share in 2025 and Asia-Pacific is forecast to expand at a 9.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Interspinous Spacers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Demand For Minimally-Invasive Lumbar Decompression

Rising Demand For Minimally-Invasive Lumbar Decompression

| +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global, with concentration in North America & EU

| Impact Timeline:

Medium term (2-4 years)

|

Growing Geriatric Population With Lumbar Spinal Stenosis

Growing Geriatric Population With Lumbar Spinal Stenosis

| +1.8% | Global, accelerated in APAC and North America | Long term (≥ 4 years) | |||

Favorable Reimbursement Revisions For Outpatient Spine

Surgery

Favorable Reimbursement Revisions For Outpatient Spine

Surgery

| +0.9% | North America & EU primary, emerging in APAC | Short term (≤ 2 years) | |||

Rapid Adoption Of Ambulatory Surgical Centers In Emerging

Markets

Rapid Adoption Of Ambulatory Surgical Centers In Emerging

Markets

| +1.1% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) | |||

Advances In Bio-Adaptive, Motion-Preserving Spacer

Materials

Advances In Bio-Adaptive, Motion-Preserving Spacer

Materials

| +0.7% | Global, led by North America and EU innovation hubs | Long term (≥ 4 years) | |||

Cloud-Connected Post-Operative Monitoring Driving Surgeon

Confidence

Cloud-Connected Post-Operative Monitoring Driving Surgeon

Confidence

| +0.5% | North America & EU early adoption, APAC following | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Minimally Invasive Lumbar Decompression

Interspinous spacers enable indirect decompression by distracting spinous processes and preserving motion, which reduces operative time and blood loss compared with laminectomy[1]Rajesh Kumar, “24-Month Outcomes of Indirect Decompression Using a Minimally Invasive Interspinous Fixation Device,” pmc.ncbi.nlm.nih.gov. Surgeons in Asia-Pacific increasingly prefer these minimally invasive techniques, according to AO Spine surveys. Broader access to imaging guidance enhances accuracy, shrinks the learning curve and stimulates device demand.

Growing Geriatric Population with Lumbar Spinal Stenosis

Up to 47% of adults aged ≥ 65 exhibit lumbar stenosis, creating a large candidate pool for motion-preserving treatment. Five-year durability data for stand-alone interspinous decompression supports its suitability in elderly cohorts unable to tolerate fusion. Rapid ageing in Japan and South Korea accelerates procedure volumes across the region.

Favorable Reimbursement Revisions for Outpatient Spine Surgery

The 2025 Medicare final rule granted a 2.9% payment increase for compliant ambulatory centres, raising provider confidence in outpatient spine care. Private insurers mirror Medicare policy, rewarding hospitals and ASCs that shorten stays and improve quality metrics with interspinous devices.

Rapid Adoption of Ambulatory Surgical Centres in Emerging Markets

Procedure migration to ASCs is forecast to lift global volumes by 21% over the next decade, with spine surgery among the fastest movers. Aligned medical device regulations in India and similar markets simplify importation, further encouraging ASC uptake.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Device Revision Rates Beyond Five Years

High Device Revision Rates Beyond Five Years

| -1.4% | Global, more pronounced in cost-sensitive markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-1.4%

| Geographic Relevance:

Global, more pronounced in cost-sensitive markets

| Impact Timeline:

Long term (≥ 4 years)

|

Stringent Post-Market Clinical-Evidence Requirements In EU

MDR

Stringent Post-Market Clinical-Evidence Requirements In EU

MDR

| -0.8% | EU primary, ripple effects in aligned regulatory markets | Short term (≤ 2 years) | |||

Surgeon Learning-Curve Deterring Smaller Hospitals

Surgeon Learning-Curve Deterring Smaller Hospitals

| -0.6% | Global, concentrated in emerging markets and rural areas | Medium term (2-4 years) | |||

Pricing Pressure From Bundled-Payment Spinal Care Models

Pricing Pressure From Bundled-Payment Spinal Care Models

| -0.9% | North America primary, expanding to EU and APAC | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Device Revision Rates Beyond Five Years

Follow-up studies highlight migration, spinous fractures and adjacent-segment degeneration after year 5, prompting payer scrutiny of revision cost exposure. Biomechanical modelling shows hybrid systems reduce peak stress at bone-implant interfaces, which may improve longevity.

Stringent Post-Market Clinical Evidence Requirements in EU MDR

Legacy interspinous spacers must satisfy extended surveillance and documentation standards by 2028, lengthening European launch cycles and adding compliance cost that smaller firms struggle to absorb[2]Medical Device Coordination Group, “MDCG 2021-25 Rev.1,” health.ec.europa.eu.

Segment Analysis

By Product Type: Hybrid Systems Lead Innovation

Static non-compressible implants controlled 51.78% of 2025 revenue, underscoring surgeon familiarity. Yet the hybrid cohort is growing at a 11.63% CAGR as it blends controlled motion with required stability. Finite-element work confirms that hybrid designs maintain physiologic range while reducing facet stress during vibration. Rising clinical evidence positions hybrids to reshape the interspinous spacers market over the forecast period.

The interspinous spacers market continues to diversify as expandable and segmental models give surgeons more intra-operative flexibility. Adaptive materials embedded in hybrid units automatically respond to load, meeting a wider spectrum of pathologies and reframing implant selection discussions inside theatre teams.

Note: Segment shares of all individual segments available upon report purchase

By Biomaterial: Bio-Resorbable Polymers Gain Momentum

Titanium maintained 41.96% share in 2025 owing to proven strength and imaging clarity. Surgeons now pursue resorbable PLGA and PLA formats that eliminate long-term foreign body and imaging artefacts and are climbing at a 9.32% CAGR. Custom 3D-printed bioresorbable implants tailored to patient anatomy are emerging at point of care, signalling another catalyst inside the interspinous spacers market.

Pioneering trials show resorbable polylactic acid spacers achieving solid fusion when combined with autograft, bypassing complex bone-graft procurement. Developers continue to refine degradation timelines so structural support disappears only after the spinal column remodels.

By Minimally Invasive Approach: Percutaneous Techniques Advance

Open posterior procedures still account for 57.88% of volume, but percutaneous methods are rising at 9.98% CAGR as imaging navigation simplifies accurate placement through small portals. Faster mobilisation and reduced opioid use reinforce patient preference for these approaches.

Surgeon education programmes and AI-guided planning systems further lower entry barriers, encouraging smaller hospitals to integrate percutaneous interspinous spacer workflows. As a result, the interspinous spacers market is expected to feature a wider mix of care sites across urban and secondary cities.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Application: Adjacent-Segment Degeneration Drives Growth

Lumbar spinal stenosis represented 67.34% of 2025 demand, validating spacers as a mainstream decompression option. Nevertheless, cases addressing adjacent-segment degeneration are accelerating at 10.59% CAGR as prior-fusion patients seek motion-preserving revision. This trend underscores a pivotal expansion vector inside the interspinous spacers market.

Specialised devices optimised for post-fusion anatomy minimise further destabilisation and enable targeted decompression without extensive hardware removal. Hybrid surgical techniques that combine limited fusion with spacer implantation illustrate how flexible instrumentation broadens the therapeutic envelope.

Note: Segment shares of all individual segments available upon report purchase

By End-User: ASCs Capture Market Share

Hospitals accounted for 64.11% of the 2025 interspinous spacers market size, leveraging comprehensive imaging and intensive-care capacity. Ambulatory centres, however, will be the primary growth engine at 9.84% CAGR, buoyed by payer policy and patient preference for same-day discharge.

ASC expansion is particularly strong in cost-sensitive economies where lower overhead aids affordability. Broader tele-monitoring and enhanced recovery protocols improve safety, allowing ASCs to manage increasingly complex lumbar cases while preserving quality benchmarks.

Geography Analysis

North America sustained 41.12% share in 2025 on the back of high procedure volumes, structured reimbursement and an installed base of spine surgeons experienced in interspinous spacer techniques. Medicare’s 2025 payment adjustment and bundled care pilots continue to reward outpatient pathways, thereby preserving positive momentum for the interspinous spacers market.

Asia-Pacific is the fastest growing geography at a 9.14% CAGR. Regional health ministries pour capital into surgical robotics, endoscopic suites and surgeon fellowship programmes. Japan’s PMDA fast-track nurtures novel implant approvals while China’s expanding middle class drives self-pay uptake for motion preservation options.

Europe maintains steady demand despite MDR compliance pressure. Transitional allowances until 2028 permit legacy interspinous spacer sales, though manufacturers must intensify post-market studies to retain CE marks. Uptake is strongest in Germany and France where public payers fund minimally invasive decompression to reduce lengthy rehab associated with fusion. Emerging markets in the Middle East, Africa and South America contribute additional upside as private hospital networks import leading brands and partnered training expands the regional surgeon base.

Competitive Landscape

Market Concentration

Moderate consolidation defines the interspinous spacers market. Leading companies promote wide product ranges that cover static, hybrid and resorbable devices, supplemented by clinical evidence bundles and digital monitoring services. Investment tilts toward materials science, 3D printing and AI-based decision support that elevate outcome visibility and surgeon confidence.

Stryker’s January 2025 sale of its U.S. spinal implants portfolio to VB Spine gives the acquirer rights to Mako Spine robotics and Copilot navigation, altering competitive balance. Medtronic integrates AI-driven patient-reported data into cloud dashboards, closing feedback loops and strengthening surgeon loyalty. Globus Medical launched a porous-PEEK ALIF spacer in March 2025, signalling ongoing material experimentation within adjacent spinal platforms. Small innovators push niche resorbable and sensor-enabled models that larger firms may target for acquisition to fill portfolio gaps and extend reach into high-growth segments of the interspinous spacers market.

Interspinous Spacers Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Globus Medical launched COHERE ALIF Spacer, the first porous PEEK interbody spacer for ALIF surgery.

- January 2025: Life Spine received FDA clearance for the ProLift Pivot Expandable Spacer System.

Table of Contents for Interspinous Spacers Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Demand For Minimally-Invasive Lumbar Decompression

- 4.2.2Growing Geriatric Population With Lumbar Spinal Stenosis

- 4.2.3Favorable Reimbursement Revisions For Outpatient Spine Surgery

- 4.2.4Rapid Adoption Of Ambulatory Surgical Centers In Emerging Markets

- 4.2.5Advances In Bio-Adaptive, Motion-Preserving Spacer Materials

- 4.2.6Cloud-Connected Post-Operative Monitoring Driving Surgeon Confidence

- 4.3Market Restraints

- 4.3.1High Device Revision Rates Beyond Five Years

- 4.3.2Stringent Post-Market Clinical-Evidence Requirements In EU MDR

- 4.3.3Surgeon Learning-Curve Deterring Smaller Hospitals

- 4.3.4Pricing Pressure From Bundled-Payment Spinal Care Models

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Static (Non-compressible Spacers)

- 5.1.2Expandable/Segmental Static Spacers

- 5.1.3Dynamic (Compressible Spacers)

- 5.1.4Hybrid Dynamic-Static Systems

- 5.2By Biomaterial

- 5.2.1PEEK

- 5.2.2Titanium & Titanium Alloys

- 5.2.3Silicone & Polyurethane

- 5.2.4Bio-resorbable Polymers

- 5.3By Minimally-Invasive Approach

- 5.3.1Open Posterior Approach

- 5.3.2Percutaneous/Endoscopic Approach

- 5.4By Application

- 5.4.1Lumbar Spinal Stenosis

- 5.4.2Degenerative Disc Disease

- 5.4.3Adjacent-Segment Degeneration

- 5.4.4Others

- 5.5By End-User

- 5.5.1Hospitals

- 5.5.2Orthopedic & Spine Clinics

- 5.5.3Ambulatory Surgical Centers

- 5.5.4Academic & Research Centers

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Stryker Corporation

- 6.3.2Boston Scientific Corporation

- 6.3.3Johnson & Johnson (DePuy Synthes)

- 6.3.4Globus Medical, Inc.

- 6.3.5Zimmer Biomet Holdings Inc.

- 6.3.6Alphatec Spine Inc.

- 6.3.7Life Spine Inc.

- 6.3.8Aurora Spine Inc.

- 6.3.9Paradigm Spine (RTI Surgical)

- 6.3.10Medtronic plc

- 6.3.11NuVasive Inc.

- 6.3.12Surgalign Holdings Inc.

- 6.3.13Premia Spine Ltd.

- 6.3.14Vertebral Technologies Inc.

- 6.3.15Orthofix Medical Inc.

- 6.3.16SpineArt SA

- 6.3.17Back Bone Innovations LLC

- 6.3.18Wenzel Spine Inc.

- 6.3.19Xtant Medical Holdings Inc.

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Interspinous Spacers Market Report Scope

As per the scope of the report, Interspinous spacers, also known as interspinous process decompression systems, are devices implanted between vertebral spinous processes. These spacers are made up of a very strong but lightweight metal that is biocompatible to the human body. The Interspinous Spacers Market is segmented by Type (Static and Dynamic), Application (Lumbar Spinal Stenosis and Degenerative Disc Diseases), End-User (Hospitals, Orthopedic Clinics, and Ambulatory Surgical Centers (ASCs)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.