China GPU Immersion Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

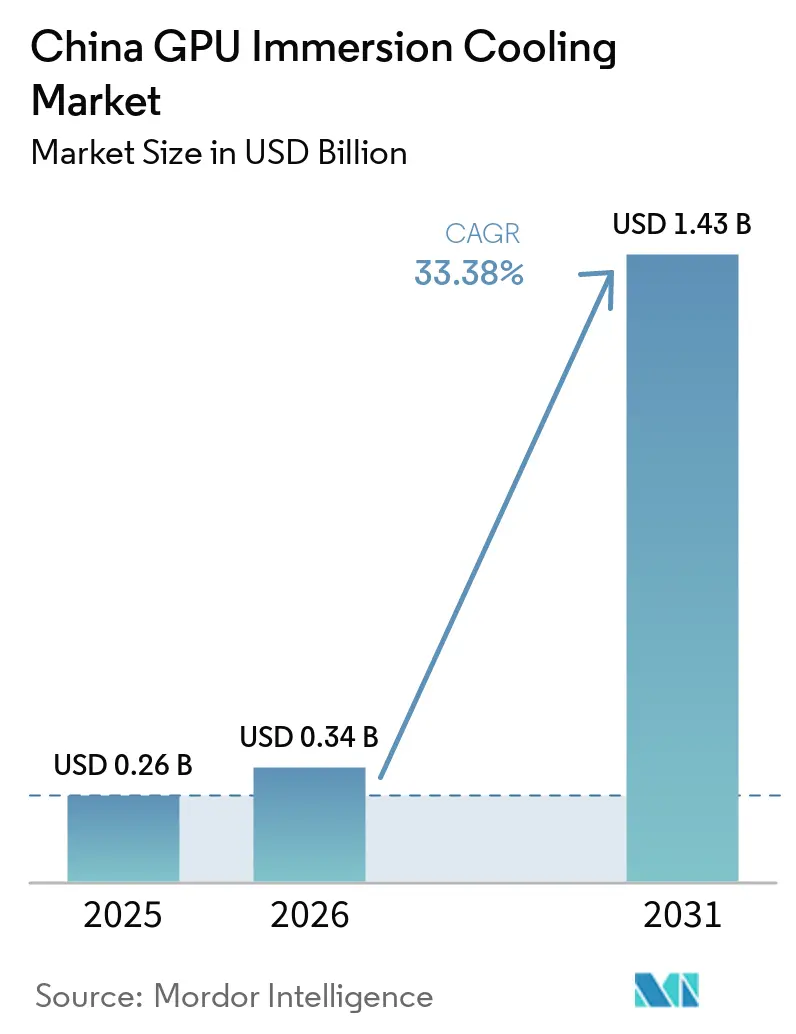

| Base Year Market Size (2025) | USD 0.26 Billion |

| Market Size (2026) | USD 0.34 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 33.38% CAGR |

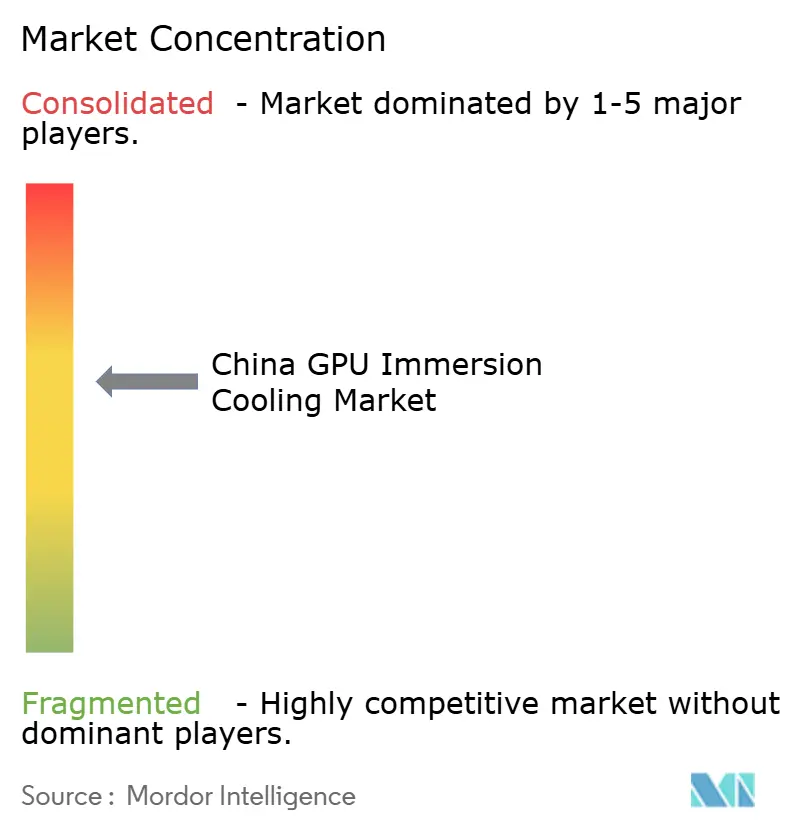

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China GPU Immersion Cooling Market Analysis by Mordor Intelligence

The China GPU immersion cooling market size is expected to be USD 0.34 billion in 2026 and reach USD 1.43 billion by 2031, growing at a CAGR of 33.38% from 2026 to 2031. Demand is accelerating as hyperscale operators confront next-generation GPUs rated above 700 W, while Beijing’s power-usage-effectiveness (PUE) mandate below 1.3 tightens energy-efficiency targets. Domestic rollouts of immersion-ready servers, government subsidies for green data centers and the East Data West Computing program that channels workloads to cooler northern provinces jointly reinforce adoption. Suppliers that bundle turnkey racks, fluid distribution and control software now capture a larger price premium than stand-alone tank vendors, because integration risk has become the primary purchase barrier. Although dielectric-fluid supply constraints remain, joint ventures such as the 2026 Shell-Sinopec plant indicate capacity relief by 2027, supporting sustained double-digit expansion of the China GPU immersion cooling market.

Key Report Takeaways

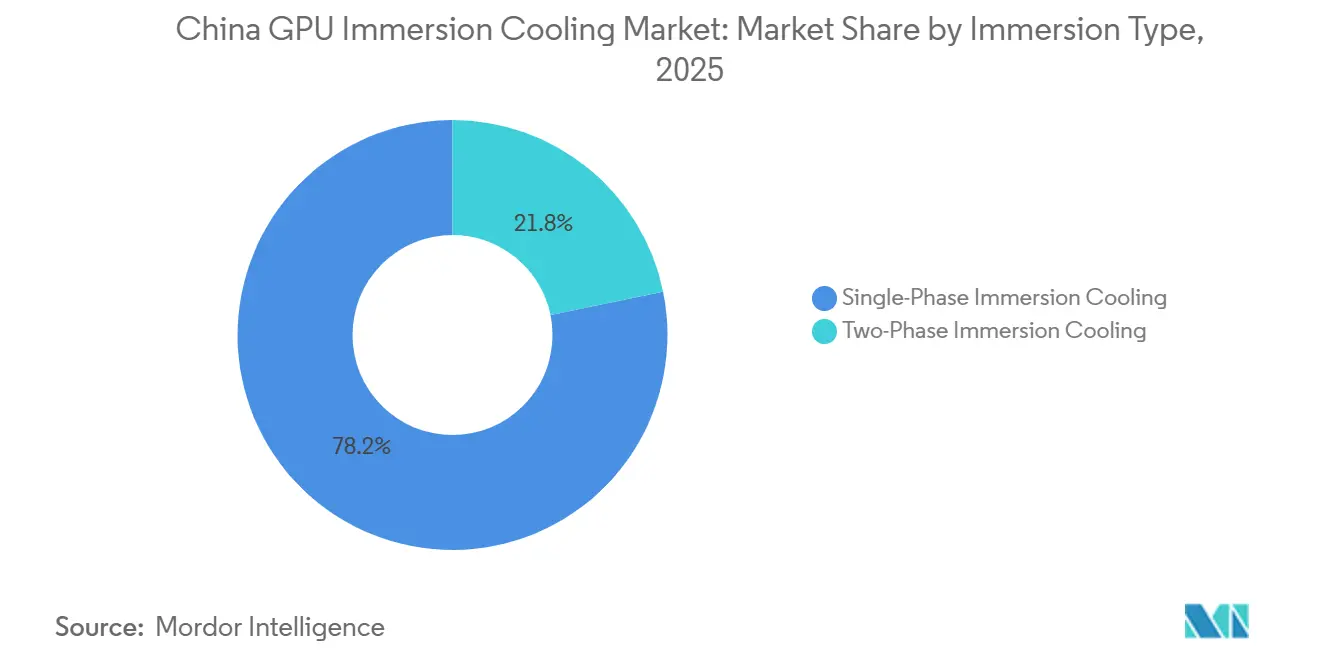

- By immersion type, single-phase systems led with 78.22% of China GPU immersion cooling market share in 2025, while two-phase solutions are projected to grow at a 33.67% CAGR to 2031.

- By solution type, immersion-optimized GPU server systems captured the largest revenue slice at 55.34% in 2025, and they are the fastest-expanding solution at a 33.74% CAGR through 2031.

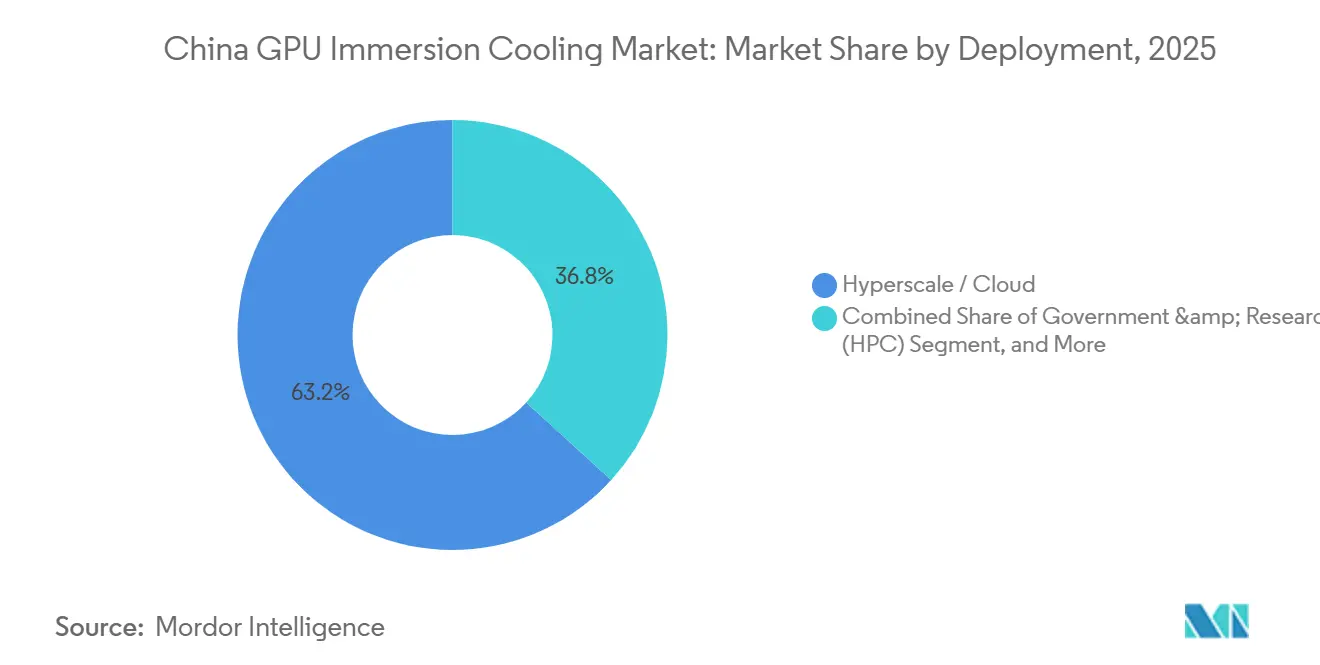

- By deployment model, hyperscale and cloud installations accounted for 63.21% of 2025 revenue, yet enterprise projects represent the most rapid climb at a 33.86% CAGR over 2026-2031.

- By GPU power density, the 300 W-700 W bracket held 51.34% of 2025 revenue, but above-700 W configurations are forecast to post the quickest rise with a 33.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China GPU Immersion Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI Model Training Workloads in Chinese Data Centers | +12.5% | National (Beijing-Tianjin-Hebei, Yangtze River Delta, Greater Bay Area) | Short term (≤ 2 years) |

| Government Carbon-Neutrality Mandates for Data Center PUE Reduction | +8.2% | National, enforced via NDRC and MIIT quotas | Medium term (2-4 years) |

| Emergence of Immersion-Ready 700 + W GPU Reference Designs from OEMs | +6.8% | National, early hyperscale adoption | Medium term (2-4 years) |

| Accelerating Expansion of Domestic GPU Manufacturing Capabilities | +4.1% | Beijing, Jinan, Shenzhen | Long term (≥ 4 years) |

| Rising Electricity Tariffs in Tier-1 Cities Encouraging Thermal Efficiency | +3.7% | Beijing, Shanghai, Shenzhen, Guangzhou | Short term (≤ 2 years) |

| Availability of Subsidized Industrial Parks in Cooler Northern Provinces | +2.9% | Inner Mongolia, Ningxia, Gansu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging AI Model Training Workloads in Chinese Data Centers

China’s installed base of AI-oriented GPUs tripled between 2024 and 2025, and MIIT projects domestic output to hit 300,000 units in 2026.[1]Ministry of Industry and Information Technology, “AI Chip Production Targets 2026,” MIIT.GOV.CN Model-training clusters such as DeepSeek’s planned 50,000-GPU facility in Inner Mongolia run at sustained loads of 350 W-700 W per chip, driving thermal densities beyond the economic reach of air cooling. Sugon’s 60,000-GPU installation in Zhengzhou demonstrates that immersion architectures reclaim 40% floor area by removing hot-aisle containment and supplemental chillers. Although inference nodes proliferate at the edge, training jobs dominate immersion adoption because they draw the highest continuous power. National algorithm-registration rules that compel on-premises compute for sensitive data amplify GPU demand, further tightening the thermal envelope.

Government Carbon-Neutrality Mandates for Data Center PUE Reduction

The National Development and Reform Commission’s February 2025 directive obliges new data centers to achieve PUE below 1.3, while existing sites must retrofit to 1.5 by 2027. Beijing augments the policy with a CNY 0.10 (USD 0.013) kWh surcharge on sites above PUE 1.35, imposing multi-million-yuan penalties on a 10 MW facility.[2]Beijing Municipal Government, “Differential Electricity Pricing for Data Centers,” BEIJING.GOV.CN Alibaba’s Hangzhou campus records a 1.09 PUE with single-phase immersion versus 1.25 under air flow, thanks to 30%-35% auxiliary-power savings. MIIT’s Green Data Center badge fast-tracks grid connections for projects under PUE 1.2, and counties such as Helinge’er layer 1% subsidies atop utility discounts, tipping return-on-capital decisively toward immersion.

Emergence of Immersion-Ready 700 + W GPU Reference Designs From OEMs

NVIDIA’s H200 and AMD’s MI300X shipped in 2025 with factory-validated immersion reference boards.[3]NVIDIA Corporation, “H200 Immersion Cooling Reference Design,” NVIDIA.COM Sugon’s I980-G80 server employs diamond-copper thermal modules exceeding 1,000 W m-K to sustain 200 kW-per-rack densities without custom cold plates. Inspur’s NF5498, released December 2025, features immersion-grade connectors and coatings that shrink deployment from weeks to days. Warranty certainty and plug-and-play racks eliminate historical hesitation among enterprises, and hyperscalers value the liability shift back to hardware makers as GPU thermal envelopes widen.

Accelerating Expansion of Domestic GPU Manufacturing Capabilities

Huawei’s Ascend 910C entered volume production in late 2025, with forecast shipments of 15,000 units in 2026. The March 2025 Sugon-Hygon merger created a vertically integrated designer that now supplies more than 60% of government HPC installs. Domestic chip makers bundle immersion systems to differentiate against export-restricted imports, while MIIT earmarked CNY 50 billion (USD 6.94 billion) for cooling-technology R&D, cutting capital hurdles for startups in Shenzhen and Zhejiang. Inspur’s hybrid approach, pairing foreign silicon with local thermal IP, underscores a de-risked supply chain that boosts the China GPU immersion cooling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Domestic Supply Chain for High-Grade Dielectric Fluids | -5.3% | National, acute in Tier-1 cities | Short term (≤ 2 years) |

| Fire Codes and Building Standards Lagging Immersion Installations | -3.8% | Beijing, Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| Water-Based Adiabatic Alternatives Competing on Capex | -2.1% | Inner Mongolia, Ningxia, Gansu | Medium term (2-4 years) |

| Perceived Warranty Risk by GPU Vendors for Immersion Use | -1.6% | National, enterprise focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Supply Chain for High-Grade Dielectric Fluids

3M’s August 2025 Novec exit removed the dominant fluorocarbon source, forcing operators to qualify domestic substitutes such as Uni-President Petrochemical’s IMF F6210. Prices for single-phase fluid plunged from CNY 640,000 (USD 89,000) t-1 in 2024 to CNY 200,000 (USD 27,900) t-1 by early 2026, yet supply is concentrated among three producers, raising procurement risk. Two-phase fluids remain scarcer and costlier because local producers lack mid-boiling-point chemistries. Shell and Sinopec’s January 2026 joint venture targets 5,000 t annual capacity by 2027, but hyperscalers pre-buy 18-24 months of stock, inflating working capital.

Fire Codes and Building Standards Lagging Immersion Installations

China’s GB50016-2014 fire code predates liquid cooling and offers no spill-containment guidance. The T/CI964-2025 industry standard spells out fluid-storage rules but lacks provincial enforcement teeth. Beijing demands secondary containment equal to 110% of fluid volume, whereas Shanghai adds vapor detection that can add up to CNY 1 million (USD 0.139 million) per site. Retrofit delays stretch six-to-twelve months, steering operators toward inland greenfields where approvals are quicker and land cheaper, thereby shaping the regional pattern of the China GPU immersion cooling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Immersion Type: Single-Phase Leads, Two-Phase Gains Traction

Single-phase designs held 78.22% of China GPU immersion cooling market size in 2025 because mineral-oil fluids cost CNY 35,000-105,000 (USD 4,860-14,583) t-1, far below two-phase fluorocarbons. Alibaba’s Hangzhou and Zhangbei campuses validated 1.05 PUE with single-phase tanks, proving that complex phase-change loops are not mandatory for efficiency targets. Two-phase systems, however, extract latent heat and return it as building warming, cutting total facility energy use by 18% during winter at the Zhengzhou supercomputing node.

Looking ahead, two-phase capacity is set to rise at a 33.67% CAGR because northern provinces can exploit low ambient temperatures for passive rejection. Yet price parity hinges on domestic fluorocarbon output scaling after 2028. For now, enterprises favor single-phase because maintenance is simpler and third-party service networks are mature. Government HPC buyers weigh energy-recovery credits more heavily, nudging the segment mix slowly toward two-phase.

By Solution Type: Turnkey Servers Capture Integration Premium

Immersion-optimized GPU server systems secured the biggest slice of China GPU immersion cooling market share at 55.34% in 2025 and will remain the primary growth engine. Sugon’s I980-G80 rack cuts deployment from six weeks to ten days, eliminating field retrofits. Inspur’s NF5498 arrives with fluid-resistant coatings, shifting thermal-validation liability to the OEM and reassuring risk-averse CIOs.

Dielectric fluids present lower invoice totals because they amortize over five-to-seven years, whereas servers refresh triennially. Stand-alone tank makers face price pressure from new domestic entrants who discount Western gear by 30%-40%. Vendors now bundle multi-year fluid-service contracts, turning capex into opex and aligning budgets with cloud business models, which supports uptake across the China GPU immersion cooling industry.

By Deployment: Hyperscale Dominates, Enterprise Outpaces in Growth

Hyperscale and cloud operators generated 63.21% of 2025 revenue as Alibaba, Tencent and Baidu rolled out multi-megawatt clusters. China Telecom’s 10,000-GPU Zhenwu array marks the largest single immersion site to date, underscoring state-owned carrier commitment. Hyperscalers enjoy 25%-30% lower per-rack costs thanks to volume, but tariff spikes to CNY 0.800 (USD 0.11) kWh in Beijing narrow the advantage for enterprise buyers.

Enterprises therefore post the quickest climb at 33.86% CAGR to 2031. Subsidy programs that refund up to 20% of retrofit spend further sweeten the payback. Edge-AI workloads spur adoption of 10-rack modular tanks such as ICEraQ Nano, well suited to constrained real-estate sites. Government and research HPC remains lumpy, tied to multiyear budget cycles, but two-phase heat-reuse incentives keep that niche attractive.

By GPU Power Density: Above-700 W Tier Accelerates

The legacy 300 W-700 W class still dominates China GPU immersion cooling market size at 51.34% in 2025, yet shipments of NVIDIA H200, AMD MI300X and Huawei Ascend 910C are tilting spend toward the above-700 W class. Sugon’s C8000 V3.0 racks sustain 200 kW per rack without custom cold plates, making immersion the default path at scale.

Below-300 W boards fade as operators retire older inference farms. Mid-density GPUs weigh air versus immersion, but electricity premiums in Tier-1 metros skew TCO in favor of liquid tanks within 18 months. At the high end, direct-to-chip plates compete, yet hyperscale buyers pick immersion because they gain three-fold rack density and sidestep chilled-water plumbing retrofits.

Geography Analysis

Coastal hubs, Beijing-Tianjin-Hebei, Yangtze River Delta, and the Greater Bay Area, captured roughly 60% of 2025 revenue thanks to proximity to end-users, mature grid links, and the presence of Alibaba, Tencent, and Baidu. Beijing’s surcharge on PUE-inefficient sites and Shanghai’s stringent fire-safety rules push operators toward immersion for both compliance and footprint relief. Shenzhen benefits from adjacent hardware factories that slash logistics time for tanks and racks.

Inland corridors supported by the East Data West Computing plan, Inner Mongolia, Ningxia, and Gansu, are now the fastest-growing territories. Hohhot and Helinge’er offer electricity as low as CNY 0.28 (USD 0.039) kWh plus up to 1% combined subsidies, a cost profile hard to match on the coast. China Mobile’s 100,000-server Hohhot campus validates that colder climates and lower tariffs offset telecom-backhaul gaps.

The regional split encourages divergent procurement: coastal operators favor turnkey immersion-server racks to minimize construction time in expensive real estate, while inland projects adopt modular tanks that scale as demand ramps. Domestic vendors such as Zhejiang Tiangong build service bases in Hohhot and Qingyang to win contracts that stipulate local support, underlining how geography molds competitive advantages inside the China GPU immersion cooling market.

Competitive Landscape

No vendor exceeds 15% share; the top five, Sugon, Alibaba InnoChill, Green Revolution Cooling, LiquidStack and Envicool, collectively own about 40%-45%. Domestic integrators leverage MIIT subsidies and sovereign-compute clauses to sell tank-and-fluid bundles below Western price points, whereas multinationals pursue joint ventures to satisfy local IP preferences.

Hyperscale-oriented suppliers co-engineer platforms with operators, locking in demand via custom firmware and workload tuning. Enterprise-focused entrants pitch standardized modular tanks compatible with mixed server generations, appealing to customers with staggered upgrade cycles. Differentiation centers on thermal-module metallurgy, diamond-copper composites out-perform aluminum on watt-per-gram metrics, and predictive maintenance software that flags fluid degradation before failures.

Patent filings surged in 2025, Sugon registered 12 immersion patents and Inspur 8, concentrating on phase-change heat-transfer films and vapor-recovery valves. Low-cost disruptors such as Shenzhen Lianli and Zhejiang Tiangong undercut incumbents by up to 40%, courting price-sensitive enterprises. The competitive dynamic suggests gradual consolidation once dielectric-fluid supply stabilizes and scale efficiencies matter more than bespoke engineering.

China GPU Immersion Cooling Industry Leaders

Huawei Technologies Co., Ltd.

Inspur Electronic Information Industry Co., Ltd.

Sugon Information Industry Co., Ltd.

GRC (Green Revolution Cooling, Inc.)

LiquidStack Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sugon commissioned a 60,000-GPU phase-change cluster at the Zhengzhou supercomputing node, the country’s largest immersion deployment to date.

- January 2026: Shell and Sinopec formed a joint venture to produce 5,000 t y-1 immersion-grade fluids in Zhejiang, aiming for 2027 start-up.

- December 2025: Inspur launched the NF5498 GPU server with factory-fitted immersion connectors, cutting rack deployment to under ten days.

- October 2025: Alibaba expanded its InnoChill single-phase platform to Zhangbei, sustaining 1.09 PUE across multiple regions.

China GPU Immersion Cooling Market Report Scope

The GPU Immersion Cooling Market in China pertains to the industry segment focused on the adoption and development of immersion cooling technologies specifically designed for Graphics Processing Units (GPUs).

The China GPU Immersion Cooling Market Report is Segmented by Immersion Type (Single-Phase, Two-Phase), Solution Type (Tanks/Systems, Dielectric Fluids, Immersion-Optimized GPU Server Systems), Deployment (Hyperscale/Cloud, Enterprise, Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Immersion Cooling |

| Two-Phase Immersion Cooling |

| Immersion Cooling Tanks / Systems |

| Dielectric Fluids |

| Immersion-Optimized GPU Server Systems |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Below 300W |

| 300W - 700W |

| Above 700W |

| By Immersion Type | Single-Phase Immersion Cooling |

| Two-Phase Immersion Cooling | |

| By Solution Type | Immersion Cooling Tanks / Systems |

| Dielectric Fluids | |

| Immersion-Optimized GPU Server Systems | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government and Research (HPC) | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W |

Key Questions Answered in the Report

What Is the Current China GPU Immersion Cooling Market Size and How Fast Will It Grow?

The China GPU immersion cooling market size is projected at USD 0.34 billion in 2026 and is forecast to surge to USD 1.43 billion by 2031 at a 33.38% CAGR.

Which Immersion Type Captures the Largest Market Share in China?

Single-phase immersion held 79% of China GPU immersion cooling market share in 2025, supported by lower fluid costs and simpler system architecture.

Why Are Chinese Hyperscale Data Centers Shifting to Immersion Cooling?

Operators deploy immersion cooling to meet strict sub-1.3 PUE mandates, accommodate 700 + W GPUs and cut electricity costs in Tier-1 cities where tariffs reached CNY 0.800 kWh (USD 0.11) in 2025.

How Will Dielectric-Fluid Supply Issues Affect Future Adoption?

3M's Novec exit tightened supply, but domestic plants backed by Shell and Sinopec aim to deliver 5,000 t y-1 of immersion-grade fluid by 2027, which should ease price volatility.

Which Segments Are Growing Fastest Within the Market?

Immersion-optimized GPU server systems are expanding at a 33.74% CAGR, and the above-700 W GPU density tier is rising at a 33.72% CAGR as high-power chips enter mass production.

What Regions in China Are Attracting New Immersion-Cooled Data Centers?

Inland provinces such as Inner Mongolia, Ningxia and Gansu are growing quickest because they provide low-cost power, cooler climates and government subsidies for green data-center builds.

Page last updated on: