China GPU Liquid Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.28 Billion |

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 11.23 Billion |

| Growth Rate (2026 - 2031) | 31.38% CAGR |

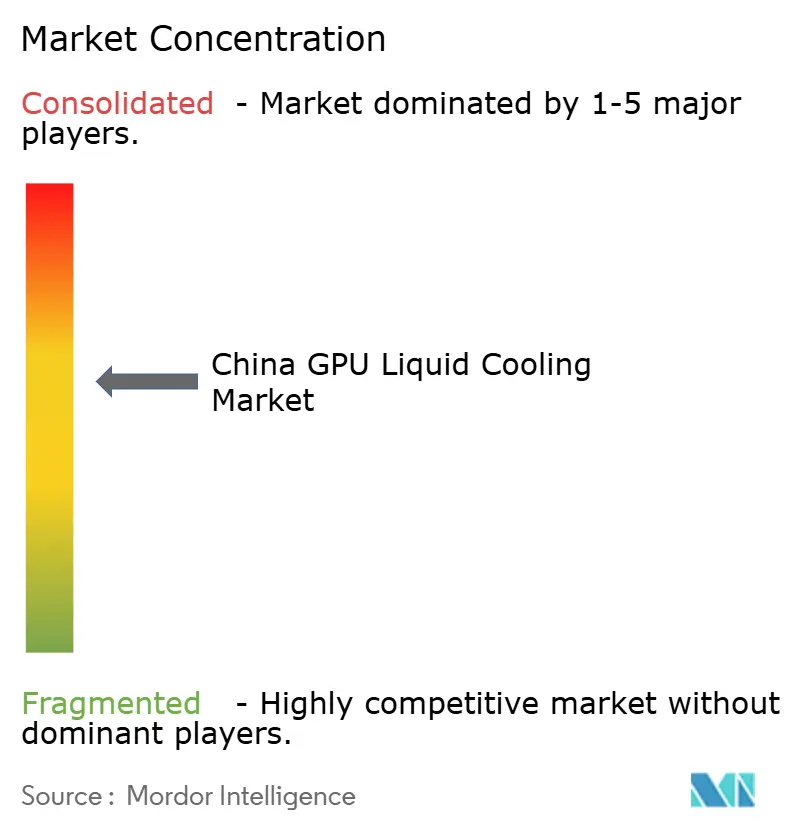

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China GPU Liquid Cooling Market Analysis by Mordor Intelligence

The China GPU liquid cooling market size was valued at USD 2.28 billion in 2025 and estimated to grow from USD 2.87 billion in 2026 to reach USD 11.23 billion by 2031, at a CAGR of 31.38% during the forecast period (2026-2031). Rapid hyperscale AI build-outs, national energy-efficiency mandates, and GPUs exceeding 700 W thermal design power have pushed liquid cooling from niche to mainstream adoption. Beijing’s approval for leading cloud providers to buy more than 400,000 NVIDIA H200 accelerators signals an unprecedented wave of high-density racks that air systems cannot manage economically. Capital spending by Alibaba Cloud, Tencent, and Baidu continues to climb, while provincial “East Data West Compute” hubs in Inner Mongolia, Gansu, Guizhou, and Ningxia integrate liquid cooling at greenfield sites to meet sub-1.25 PUE targets. Domestic suppliers, buoyed by export controls on advanced U.S. chips, are localizing cold-plate assemblies and coolant distribution units, steadily compressing unit costs and widening access for enterprise users.

Key Report Takeaways

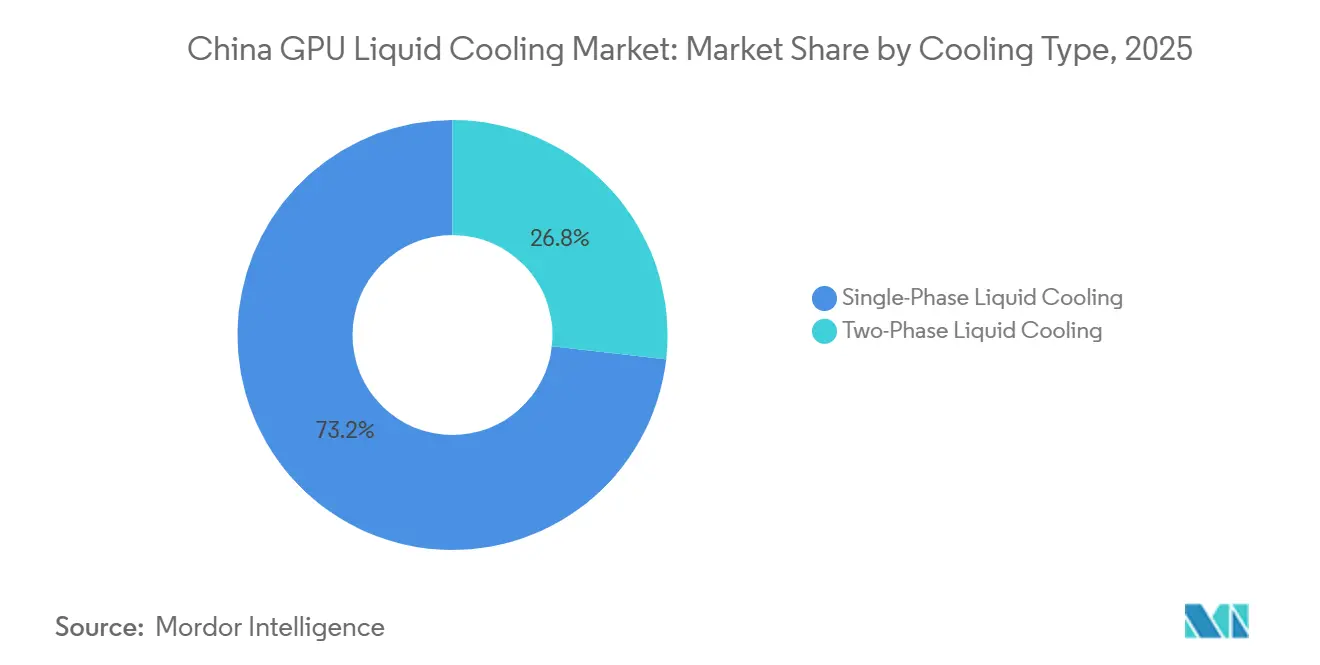

- By cooling type, single-phase liquid cooling led with 73.20% revenue share in 2025, whereas two-phase immersion is on track to grow at a 31.67% CAGR through 2031 and is the fastest-rising segment.

- By cooling level, component-level cold plates accounted for 55.45% of 2025 sales, while rack-level solutions are projected to accelerate at a 31.76% CAGR to 2031.

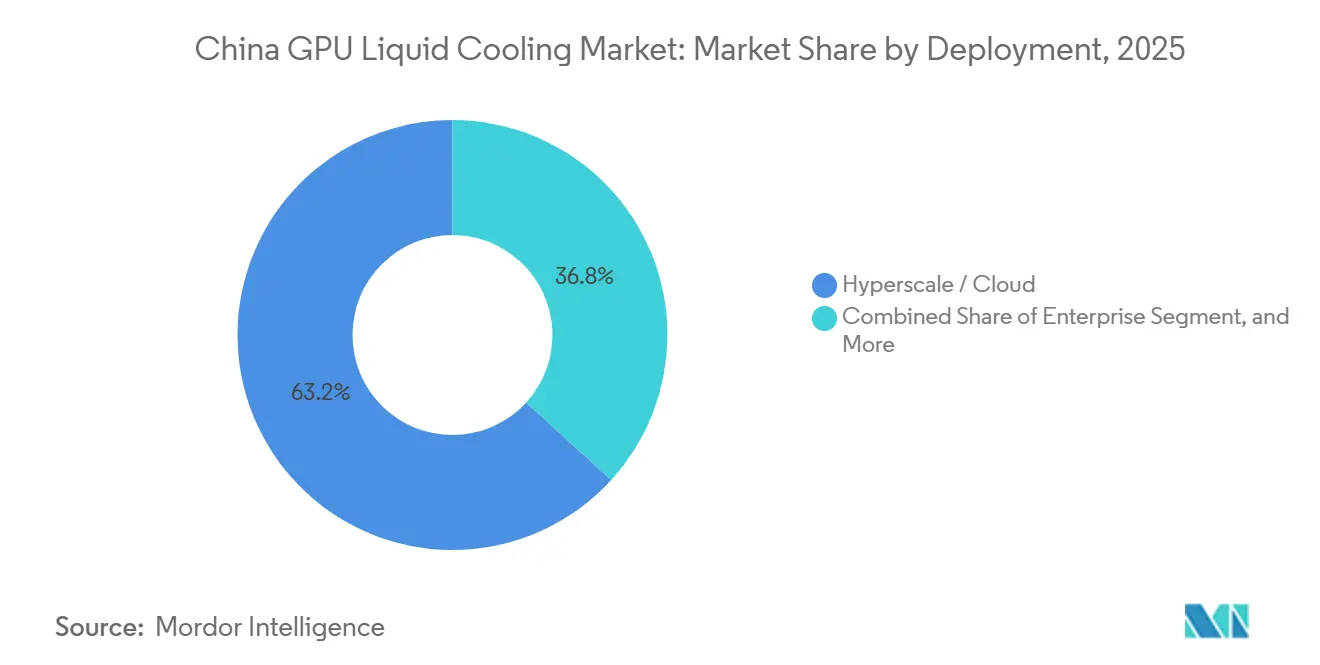

- By deployment, hyperscale and cloud installations commanded 63.22% of 2025 spending, but enterprise installations are forecast to post the highest 31.86% CAGR as mid-tier firms shift training and inference on premises.

- By GPU power density, the 300 W-700 W bracket claimed 51.56% of 2025 turnover; however, GPUs above 700 W are expected to advance at a 32.11% CAGR and will outpace all other density classes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China GPU Liquid Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of AI Training Workloads in Chinese Hyperscale Data Centers | +9.2% | National footprint, concentrated in Beijing-Tianjin-Hebei, Yangtze River Delta, and Greater Bay Area | Medium term (2-4 years) |

| Rising GPU Power Densities Beyond 700 W Necessitating Liquid Cooling | +8.5% | National, with fastest acceleration in tier‑1 cities and provincial AI hubs | Short term (≤ 2 years) |

| Rapid Build‑Out of Provincial AI Computing Clusters Under the “East Data West Compute” Program | +7.8% | Western regions with coordinated eastern compute nodes | Long term (≥ 4 years) |

| Export Restrictions on Advanced GPUs Accelerating Domestic Liquid‑Cooled Accelerator R&D | +3.1% | National, with R&D concentration in Beijing, Shanghai, and Shenzhen | Long term (≥ 4 years) |

| Government Incentives for Energy‑Efficient Data Center Cooling | +1.9% | National, supported by pilot programs in Beijing, Shanghai, Shenzhen, and Guangzhou | Medium term (2-4 years) |

| Growing Preference for Immersion‑Ready GPU Reference Designs Among ODM Server Makers | +0.9% | National, centered on manufacturing hubs in Guangdong, Jiangsu, and Zhejiang | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of AI Training Workloads in Chinese Hyperscale Data Centers

Chinese hyperscalers are scaling clusters from tens to hundreds of petaflops, and liquid cooling keeps junction temperatures stable even when utilization exceeds 80%.[1]Bloomberg News, “China Approves Nvidia H20 Chip Orders for Alibaba, Tencent,” bloomberg.com Alibaba Cloud’s USD 52.7 billion, three-year infrastructure plan places cold-plate racks at the center of next-generation language-model training, preventing fan energy from eroding overall PUE. Baidu is retrofitting legacy facilities after thermal loads quadrupled, while Tencent doubled AI capex to USD 5 billion for 2026, deploying immersion tanks that sustain 100-200 kW per rack. Sustained demand for sovereign AI models ensures continuous GPU utilization that only liquid cooling can support.

Rising GPU Power Densities Beyond 700 W Necessitating Liquid Cooling

NVIDIA’s Vera Rubin family arrives in H2 2026 with liquid cooling as standard and board power at or above 1,000 W, eliminating air systems for flagship AI training racks. Delta Electronics already offers 1.5 MW coolant distribution units sized for fifteen 100 kW NVL72 racks, while Huawei’s liquid-cooled 800 G switches prevent thermal throttling in fabric elements. Economics also favor liquid cooling—higher density allows smaller footprints and lowers HVAC overhead.

Rapid Build-Out of Provincial AI Computing Clusters Aligned With “East Data West Compute

The National Development and Reform Commission earmarked USD 6 billion for eight inter-linked hubs, triggering more than USD 138 billion in cumulative capex for GPU farms that must beat a 1.25 PUE ceiling.[2]National Development and Reform Commission, “Implementation Plan for the Overall Layout of National Integrated Big Data Centers,” ndrc.gov.cn Inner Mongolia’s Ulanqab node alone is installing over 30,000 liquid-cooled GPU servers, while Xinjiang’s Hami project leverages a desert climate and immersion tanks to meet 1.15 PUE. The western clusters transmit model outputs eastward over high-bandwidth optical links, so operators optimize energy efficiency rather than proximity, reinforcing liquid cooling’s role.

Export Restrictions on Advanced GPUs Accelerating Domestic Liquid-Cooled Accelerator R&D

U.S. controls on H100 and H200 sales pushed Chinese vendors such as Sugon and Phytium to fast-track homegrown accelerators packaged with immersion solutions. Sugon’s C8000 V3.0 rack hits 900 kW and delivers 1.04 PUE, matching or beating imported GPU platforms.[3]Sugon Corp., “Sugon Unveils C8000 V3.0 Megawatt-Scale Immersion Liquid Cooling Platform,” sugon.com Lingyi Zhizao became the sole mainland vendor qualified to supply cold-plate manifolds for NVIDIA Rubin, slashing dependency on overseas components. Domestic innovation is therefore entwined with liquid cooling progress.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX Compared With Air‑Cooling Retrofits | −1.4% | National, with stronger impact in tier‑2 and tier‑3 cities | Short term (≤ 2 years) |

| Supply‑Chain Dependency on Imported Dielectric Fluids Amid Geopolitical Tensions | −0.7% | National, with procurement concentrated through coastal ports | Medium term (2-4 years) |

| Limited Standardization Across Component‑Level Cold‑Plate Solutions | −0.4% | National, with fragmentation most acute among ODM server suppliers | Medium term (2-4 years) |

| StringentCybersecurity Approval Processes for Liquid‑Cooled Cloud Deployments in Government Workloads | −0.3% | National, with the strictest enforcement in Beijing, Shanghai, and Shenzhen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX Compared With Air Cooling Retrofits

Cold-plate assemblies, quick connectors, and CDUs can lift initial budgets 40-60%, discouraging operators below the 50 kW per rack threshold. Component costs are concentrated in metallurgy and precision machining, areas where scale economies are still maturing. Intel’s comparative TCO study, however, shows breakeven in under five years once racks top 100 kW, thanks to lower HVAC bills and higher space utilization. Manufacturers such as Midea are investing USD 138 million in high-volume CDU plants to reduce unit pricing by up to 30% before 2028, easing this barrier.

Supply Chain Dependency on Imported Dielectric Fluids Amid Geopolitical Tensions

Two-phase immersion still depends on fluorinated fluids from 3M and Solvay, which hold intellectual-property advantages in dielectric stability and boiling-point uniformity. Domestic chemical groups are ramping R&D, but commercial-grade substitutes lag on conductivity metrics. Shenling Environment has committed USD 94 million to develop local coolants, while hyperscalers stockpile imported fluids as a hedge. Any export disruption would tighten supply and widen cost gaps, particularly for operators committed to phase-change immersion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Type: Single-Phase Dominance Faces Two-Phase Disruption

Single-phase architectures captured the largest China GPU liquid cooling market share at 73.20% in 2025, buoyed by compatibility with standard 42U racks and relatively simple maintenance. Delta’s 4 RU and 6 RU in-rack CDUs connect quick-release hoses to Neptune-enabled Lenovo servers that cool H100 and H200 GPUs without plumbing changes to facility loops. This segment still wins most retrofit projects where operators migrate cabinets gradually to liquid. In contrast, two-phase immersion is already the preferred choice for megawatt-class AI training halls: Sugon’s C8000 V3.0 tanks achieve 900 kW per rack, shaving PUE to 1.04 and freeing floor space for denser network fabrics. Because power envelopes for Vera Rubin exceed 1 kW per device, the above-700 W density band will tilt procurement toward two-phase systems despite their higher fluid budgets. ODM and hyperscale pilots in H2 2026 will determine the pace at which immersion replaces cold plates for greenfield builds across the China GPU liquid cooling market.

Adoption patterns indicate that roughly 22% of new Chinese data centers commissioned in 2026 integrated some form of liquid cooling, of which two-phase immersion accounted for only 4%. The gap arises from training inertia and the higher cost of fluorinated fluids, yet hyperscalers value immersion’s ability to eliminate cold plates from maintenance schedules. Intel and Alibaba Cloud validated single-phase immersion to 100 kW racks at 1.09 PUE, demonstrating a mid-step that could blur boundaries between cold-plate and immersion approaches. As GPU wattage climbs, two-phase systems will absorb the fastest growth slice, reinforcing their role in the future mix of the China GPU liquid cooling market.

By Cooling Level: Component Cold Plates Lead, Rack Solutions Accelerate

Component-level cooling held 55.45% of 2025 spending, mainly because GPU vendors ship reference designs with integrated cold plates. Upgrades on a node-by-node basis simplify billing for enterprises and allow operators to target only mission-critical racks. Tier-1 automotive heat-exchange companies like Yinlun Co. have adapted microchannel plates achieving 98% batch-to-batch consistency, boosting trust among hyperscale buyers. However, rack-level systems, featuring integrated manifolds and in-line CDUs, are growing at a 31.76% CAGR and gaining share of the China GPU liquid cooling market size as hyperscalers chase 150 kW-plus cabinets. XFusion’s FusionPoD eliminates hot aisles, delivering pPUE of 1.06 across 144 CPUs plus GPUs, and H3C’s 800 G liquid-cooled switch ties the network into the same fluid loop, removing air gaps.

Rack solutions bundle plumbing, leak detection, and monitoring, which lowers engineering time on the data-hall floor. These all-inclusive racks, often shipped in ISO containers, can be craned into bare shells at provincial AI hubs, shortening time-to-compute. For operators retrofitting downtown Beijing or Shanghai colocation, component cold plates remain favored because they avoid cutting concrete for new facility loops. Therefore, both levels will coexist; yet the strongest revenue delta to 2031 sits with racks, adding scale to the China GPU liquid cooling market size.

By Deployment: Hyperscale Anchors Market, Enterprise Surges

Hyperscale and cloud installations generated 63.22% of 2025 revenue, reflecting Alibaba Cloud’s USD 52.7 billion road map and Tencent’s USD 5 billion 2026 budget. These operators integrate two-phase immersion and rack-scale cold plates to optimize each white-space square meter, especially in Beijing-Tianjin-Hebei where land leases exceed USD 1,000 per square meter annually. Government HPC centers, funded through the East Data West Compute budget, represent an additional wave of demand and lean on domestic accelerators to circumvent export rules. The China GPU liquid cooling market share within government clusters is therefore rising as provincial tenders stipulate sub-1.25 PUE targets.

Enterprise use, however, is the fastest-growing slice at a 31.86% CAGR. Corporations in finance, automotive, and pharmaceuticals are buying off-the-shelf immersion racks from Kortrong and Stone Holdings to train private LLMs in secure on-premise zones. Avoiding cloud API fees while ensuring data sovereignty helps justify the higher upfront spend. Turnkey racks with pre-filled coolant, sealed manifolds, and remote monitoring lower operational expertise thresholds. Edge AI, though nascent, is testing liquid loops in base-band cell-tower huts and autonomous-vehicle garages where vibration and space constraints challenge air systems.

By GPU Power Density: Above-700 W Segment Drives Growth

The 300 W-700 W class held 51.56% revenue share in 2025, riding the installed base of H100 and MI250X accelerators. Single-phase cold plates meet thermal headroom for these devices in urban colocation sites. Yet once Rubin Ultra lands at 1 kW per GPU and NVL72 racks hit 160 kW, two-phase immersion tanks become essential. This above-700 W slice will log the highest 32.11% CAGR, collecting the majority of incremental revenue by 2031 within the China GPU liquid cooling market. Delta’s 1.5 MW CDU distributes secondary water to up to fifteen NVL72 racks, while Huawei’s liquid-cooled 800 G fabrics handle the network side to eliminate mixed cooling regimes. As GPUs at the edge climb past 400 W due to complex inference jobs, even telco micro-modules will adopt compact cold-plate loops.

Below 300 W devices remain air-cooled today, yet cooling vendors are prototyping closed-loop micro-bath blocks for dense video analytics and industrial machine-vision clusters. Although small in dollar terms, these pilots could prime liquid technology for future edge rollouts and extend the addressable China GPU liquid cooling market.

Geography Analysis

Beijing-Tianjin-Hebei, the Yangtze River Delta, and the Greater Bay Area host most hyperscale footprints, driven by proximity to talent, IXPs, and enterprise customers. Beijing’s differential electricity tariffs penalize PUE above 1.3, prompting operators to retrofit cold-plate loops quickly. Shanghai demands PUE under 1.3 for all new halls, so two-phase immersion appears in design docs even before land purchase. Guangdong’s five-year digital plan subsidizes up to 20% of incremental liquid-cooling capex, favoring local ODM racks.

Western provinces enjoy the fastest expansion because low ambient temperatures and abundant renewables cut operating cost. Inner Mongolia’s Ulanqab hub deploys 30,000 liquid-cooled GPU servers and hits 1.15 PUE, while Xinjiang’s desert climate supports phase-change tanks with minimal chiller infrastructure. Guizhou’s Gui’an New Area caps tariffs under USD 0.05 per kWh, letting immersion clusters run 24/7 training passes for sovereign LLMs. These hubs ship inference caches back east across optical backbones, balancing compute load and energy availability.

Tier-2 cities such as Chengdu, Wuhan, and Xi’an are rolling out municipal AI centers funded by local treasuries. JD.com’s Wuhan hall spent USD 137 million to install 2,000 liquid-cooled GPU servers, confirming interest from e-commerce and logistics giants. Baotou and other Inner Mongolia towns leverage proximity to wind farms, cutting secondary-loop condenser energy needs. Adoption remains slower in secondary markets due to steeper per-rack CAPEX, but provincial incentives that tie subsidies to PUE thresholds gradually swing ROI in favor of liquid systems.

Competitive Landscape

In 2026, no single supplier commands more than 15% of the revenue, underscoring the fragmented and competitive nature of the industry. Companies such as Inspur, Lenovo, Huawei, Sugon, and H3C, which maintain strong ties to government entities, dominate the ODM server volume. These firms primarily supply racks to enterprises and provincial clusters, playing a significant role in the market. On the international stage, specialists like Asetek, CoolIT, LiquidStack, and Submer have successfully secured proof-of-concept contracts at global cloud hubs located in Shenzhen and Shanghai. Their success is attributed to their extensive experience and proven track records in long immersion technology, which has made them highly sought after. Meanwhile, hyperscalers are increasingly taking control of their design processes. For instance, Alibaba Cloud, in collaboration with Intel, has developed a single-phase immersion pod that achieves an impressive 1.09 PUE. This innovation not only enhances energy efficiency but also reduces reliance on third-party suppliers, thereby lowering associated costs. Additionally, Lingyi Zhizao's inclusion in NVIDIA's Rubin manifold initiative reflects Beijing's strategic focus on fostering localized thermal component development, further emphasizing the importance of domestic innovation in the sector.

New entrants are emerging from adjacent industries, bringing fresh perspectives and expertise to the market. Yinlun, for example, is applying its precision engineering capabilities from automotive heat-exchangers to the development of GPU plates, showcasing its ability to adapt to new technological demands. Similarly, Midea is leveraging its extensive knowledge in HVAC systems to create high-efficiency CDUs, supported by a significant USD 138 million investment in its manufacturing plant. This investment underscores Midea's commitment to advancing its capabilities in this space. Kortrong, on the other hand, is targeting midsize enterprises by offering full-immersion rack solutions specifically designed for organizations that lack dedicated facility engineers.

These tailored solutions address a critical gap in the market, enabling smaller enterprises to adopt advanced technologies without requiring extensive in-house expertise. Currently, the primary technological challenges in the industry revolve around software solutions for managing coolant flow and detecting leaks, rather than advancements in raw metallurgy. To address these challenges and secure customer loyalty, vendors are increasingly bundling telemetry SDKs with their hardware offerings. This approach not only enhances the functionality of their products but also ensures long-term customer engagement and retention.

China GPU Liquid Cooling Industry Leaders

Inspur Group

Lenovo Group Limited

Huawei Technologies Co., Ltd.

Sugon Information Industry Co., Ltd.

H3C Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sugon unveiled the C8000 V3.0 megawatt-scale immersion platform achieving 900 kW per rack and 1.04 PUE.

- April 2026: Yinlun Co. introduced microchannel cold plates with 98% thermal-performance consistency for AI clusters.

- March 2026: Huawei released the CloudEngine XH9230-128DQ-LC 800 G liquid-cooled switch.

- February 2026: H3C launched the S9827 800 G liquid-cooled switch, cutting power 11% versus air versions.

China GPU Liquid Cooling Market Report Scope

The GPU Liquid Cooling Market in China pertains to the development, adoption, and commercialization of liquid cooling solutions specifically engineered for Graphics Processing Units (GPUs).

The China GPU Liquid Cooling Market Report is Segmented by Cooling Type (Single-Phase Liquid Cooling and Two-Phase Liquid Cooling), Cooling Level (Component-Level Cooling and Server/Rack-Level Cooling), Deployment (Hyperscale/Cloud, Enterprise, Government and Research HPC, and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Liquid Cooling |

| Two-Phase Liquid Cooling |

| Component-Level Cooling |

| Server / Rack-Level Cooling |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Edge AI |

| Below 300W |

| 300W - 700W |

| Above 700W |

| By Cooling Type | Single-Phase Liquid Cooling |

| Two-Phase Liquid Cooling | |

| By Cooling Level | Component-Level Cooling |

| Server / Rack-Level Cooling | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government and Research (HPC) | |

| Edge AI | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W |

Key Questions Answered in the Report

What is the current and projected value of the China GPU liquid cooling market?

The China GPU liquid cooling market is expected to reach USD 2.87 billion in 2026 and grow to USD 11.23 billion by 2031, registering a 31.38% CAGR.

Which cooling type leads sales in China?

Single-phase liquid cooling dominated the market with a 73.20% revenue share in 2025, while two-phase immersion cooling represents the fastest-growing segment.

Why are GPUs above 700 W important for liquid cooling adoption?

GPUs exceeding 700 W TDP make air cooling economically and technically impractical, this power segment is forecast to grow at a 32.11% CAGR as next-generation architectures such as NVIDIA Rubin enter deployment.

How do regional policies shape demand?

Beijing, Shanghai, and Guangdong enforce low-PUE requirements and offer subsidies that accelerate liquid cooling adoption, while western AI hubs leverage low-cost renewable energy to support megawatt-scale compute clusters.

Which companies are key players?

Key participants include Inspur, Lenovo, Huawei, Sugon, H3C, Asetek, CoolIT, LiquidStack, and Submer, alongside hyperscale operators developing in-house liquid-cooling systems.

What is the biggest barrier to wider usage?

High upfront CAPEX, typically 40-60% higher than air-cooled systems, remains the largest barrier, although declining costs for coolant distribution units (CDUs) and cold plates are gradually narrowing the gap.

Page last updated on: