Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.81 Billion |

| Market Size (2026) | USD 19.98 Billion |

| Market Size (2031) | USD 24.43 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

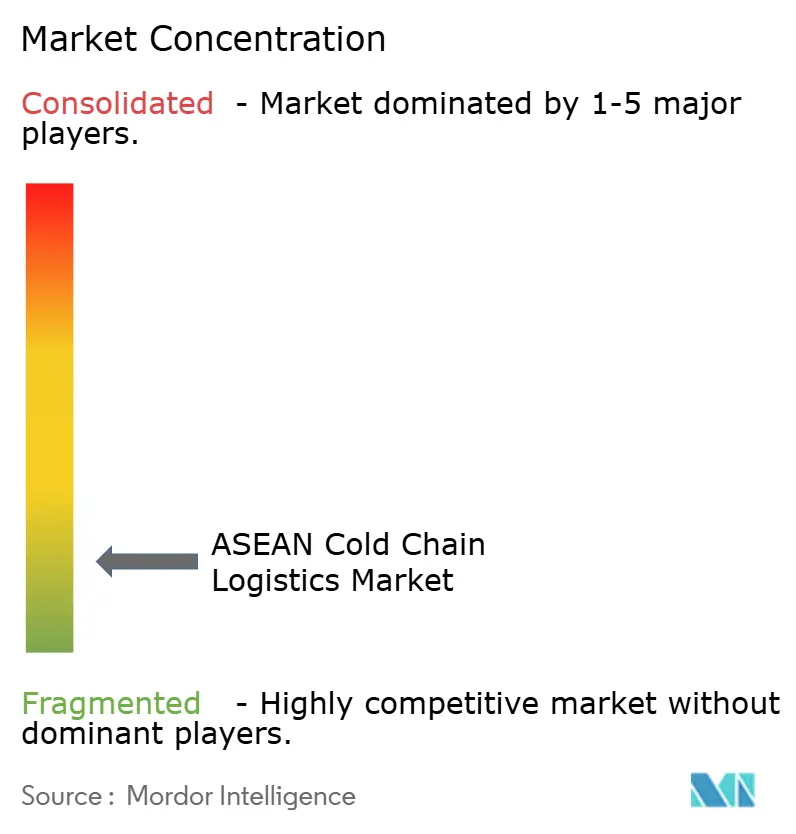

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Cold Chain Logistics Market Analysis by Mordor Intelligence

The ASEAN Cold Chain Logistics Market size is projected to expand from USD 18.81 billion in 2025 and USD 19.98 billion in 2026 to USD 24.43 billion by 2031, registering a CAGR of 4.94% between 2026 to 2031.

The ASEAN cold chain logistics market is gradually strengthening as regional food supply chains become more organized and export-oriented. Countries with strong seafood, meat, and tropical fruit production, such as Thailand, Vietnam, and Indonesia, are increasing investments in refrigerated storage and temperature-controlled transportation to reduce post-harvest losses and support exports. At the same time, the expansion of modern retail, quick-commerce grocery platforms, and pharmaceutical distribution is pushing demand for more reliable cold chain infrastructure across the region. However, the market remains uneven, with developed hubs like Singapore having advanced logistics capabilities while several emerging ASEAN economies still face gaps in cold storage capacity and distribution networks. As a result, logistics companies are focusing on building regional cold storage hubs, improving monitoring technologies, and strengthening cross-border supply chains to capture growing demand.

Key Report Takeaways

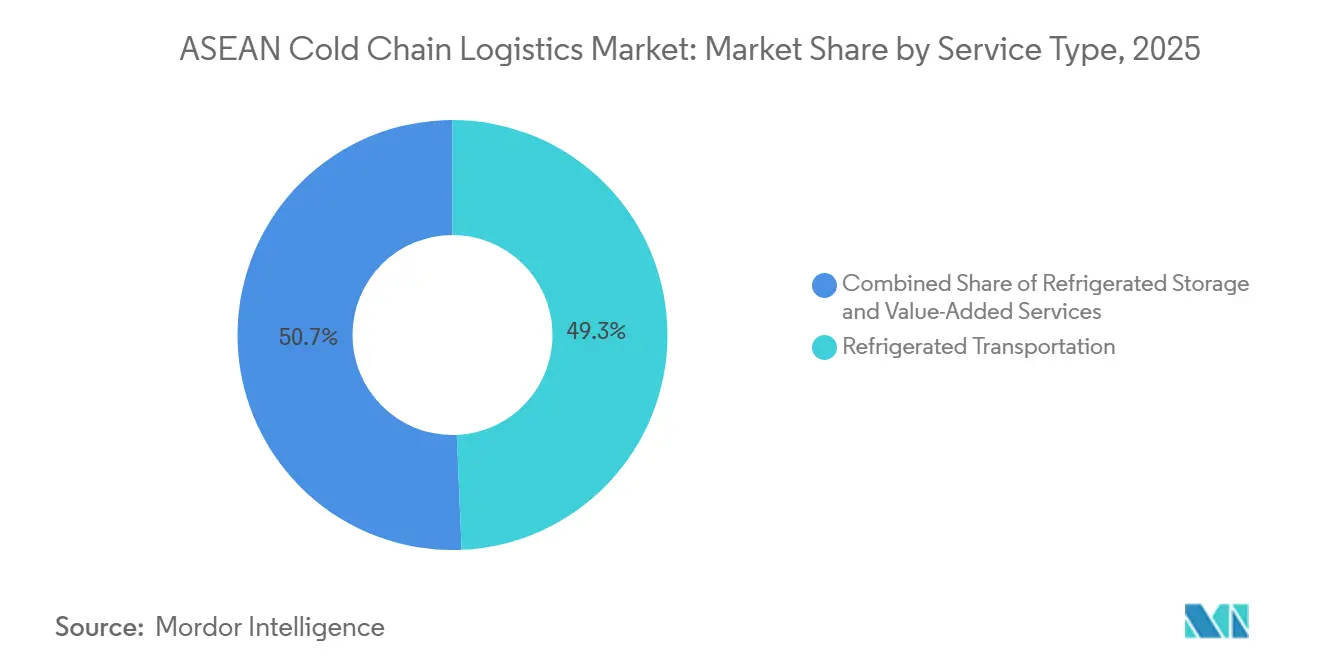

- By service type, refrigerated storage led the ASEAN Cold Chain Logistics Market share with 49.3% in 2025, while value-added services are projected to grow at a 5.7% CAGR during 2026-2031.

- By temperature type, frozen goods accounted for a 42.6% share in 2025, while chilled flows are set to expand at a 5.2% CAGR through 2026-2031.

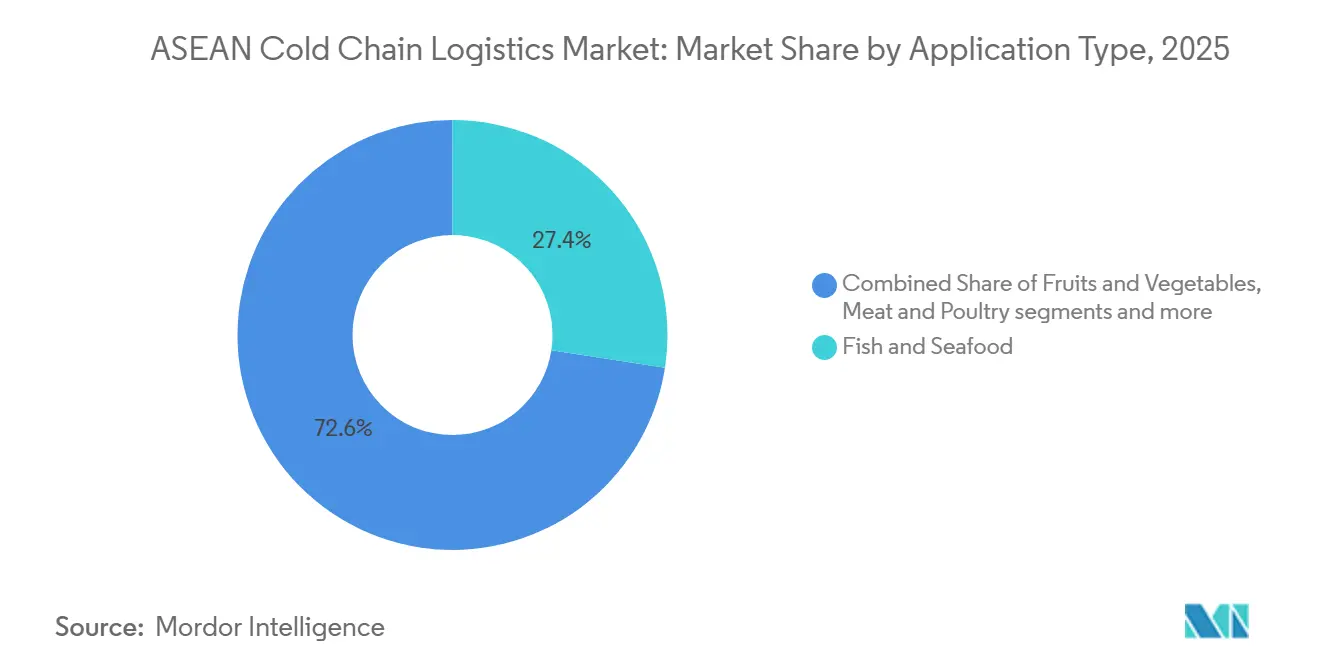

- By application, fish and seafood held a 27.4% share of the ASEAN Cold Chain Logistics Market size in 2025, while vaccines and clinical-trial materials recorded the fastest growth at a 5.5% CAGR through 2026-2031.

- By geography, Indonesia captured a 22.4% share in 2025, while Thailand is the fastest-growing at a 5.1% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Middle-Class Disposable Income Driving Demand for Imported Frozen and Chilled Goods | +1.2% | Indonesia, Philippines, Vietnam, Thailand (urban centers) | Medium term (2-4 years) |

| Modern Retail and Supermarket Chain Expansion Across Tier-2 And Tier-3 Cities | +0.8% | Indonesia (Medan, Makassar, Surabaya), Vietnam, Philippines, Thailand | Short term (≤ 2 years) |

| FDI Inflows in Greenfield Cold Storage and Distribution Center Development | +0.9% | Vietnam (Dong Nai, Long An), Thailand, Indonesia, Philippines | Medium term (2-4 years) |

| Government Food Security Programs Mandating Post-Harvest Cold Storage Capacity | +0.7% | Philippines, Indonesia, Vietnam (Mekong Delta), Thailand, Laos | Medium term (2-4 years) |

| Aquaculture Industry Boom in Vietnam, Thailand, and Indonesia Boosting Seafood Cold Logistics | +0.6% | Vietnam (Mekong Delta: 70% of aquaculture), Thailand (coastal), Indonesia (Sulawesi) | Short term (≤ 2 years) |

| Regional Free Trade Agreements (RCEP, CPTPP) are Facilitating Chilled Agri-Food Trade Flows | +0.5% | ASEAN-wide (especially Vietnam, Thailand, Malaysia, Singapore) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Middle-Class Disposable Income Driving Demand for Imported Frozen and Chilled Goods

Rising incomes in large ASEAN economies are driving demand for imported proteins, premium dairy, and ready-to-cook formats requiring reliable frozen and chilled transport. Urban retailers are increasing temperature-sensitive assortments to meet higher demand for freshness and quality. In Muslim-majority markets, halal-certified frozen meals and processed foods necessitate segregated storage and compliance with halal logistics rules, boosting demand for certified providers.[1]Halal Product Assurance Agency, “Government Regulation 42/2024,” BPJPH, bpjph.halal.go.id Seasonal disruptions, like storm seasons in the Philippines, highlight the need for stockpiles and reliable distribution routes. These trends are fueling growth in the ASEAN cold chain logistics market as buyers prioritize custody control for sensitive cargo.

Modern Retail and Supermarket Chain Expansion Across Tier-2 and Tier-3 Cities

Convenience and grocery chains are scaling beyond capitals into secondary cities, which creates distributed demand for short-haul chilled replenishment and micro-fulfillment. E-Mart24’s 2026 plan to open 130 stores in Malaysia, Cambodia, and Laos introduces 24-hour formats that require consistent 2-8°C storage and delivery routines for beverages and ready meals. Indonesia’s Alfamart is extending its footprint across secondary islands, which deepens route density for chilled fleets serving towns that previously relied on ambient stock. Retailers are bringing in remote temperature monitoring and exception alerts for cold cases, which tightens coordination between stores and upstream distribution and raises expectations for data visibility from carriers and warehouses.[2]Health Sciences Authority, “Good Distribution Practice,” HSA, hsa.gov.sg This buildout shifts the ASEAN cold chain logistics market toward modular cross-docks, right-sized cold rooms, and flexible trucking. Providers that can scale smaller nodes and adjust routing quickly are gaining an edge over operators concentrated in large centralized sites.

FDI Inflows in Greenfield Cold Storage and Distribution Center Development

Foreign and regional investors are injecting capital into multi-temperature warehousing and pharma-ready logistics, often within zones offering fiscal incentives and green designs. LOTTE Global Logistics began constructing a cold-chain site in Dong Nai in March 2025, aiming for GDP-certified spaces and seafood blast-freezing by May 2026. UPS expanded its Singapore cold-chain footprint in June 2025, adding ultra-low freezers and real-time custody tracking for biologics and clinical trials. Large projects incorporate rooftop solar, battery backup, and energy-efficient refrigeration to ensure stability during grid stress and extreme weather. Government investment agencies and subregional programs prioritize logistics in growth corridors, spurring private builds for refrigerated storage and distribution. These developments enhance multi-country coverage and service standards in the ASEAN cold chain logistics market.

Government Food Security Programs Mandating Post-Harvest Cold Storage Capacity

Food security budgets now include mandates for post-harvest cold rooms to reduce losses and strengthen buffer stocks for staples and fresh foods. The Philippines allocated PHP 3 billion in June 2025 for 99 facilities, addressing regional supply gaps for fruits, vegetables, and fisheries. Indonesia’s 2025 budget includes USD 7.1 billion for food security, focusing on storage upgrades and logistics digitalization to enhance climate resilience. Vietnam’s agriculture ministry aims to increase pallet positions through 2028 to support seafood exports and quality compliance. These programs require HACCP, ISO 22000, or GDP standards, transitioning volumes to audited facilities, and benefiting the ASEAN cold chain logistics market by aligning with importers’ quality requirements.[3]General Statistics Office of Vietnam, “Exports and Trade,” GSO Vietnam, gso.gov.vn

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Inconsistencies and Varying Cold Chain Standards Across Member States | -0.4% | ASEAN-wide (Indonesia, Philippines, Vietnam, Myanmar, Cambodia, Laos) | Long term (≥ 4 years) |

| High Upfront Capital Expenditure Deterring SME Cold Chain Operators | -0.6% | Indonesia (rural, outer islands), Philippines (Mindanao, Visayas), Vietnam, Cambodia | Medium term (2-4 years) |

| Competition From Informal and Unregulated Cold Storage Providers is Undercutting Prices | -0.3% | Indonesia, Philippines, Vietnam (Mekong Delta), Myanmar, Laos | Short term (≤ 2 years) |

| Climate Vulnerability and Extreme Weather Disrupting Cold Chain Continuity | -0.5% | Philippines, Vietnam, Thailand, Indonesia, Myanmar (coastal and low-lying areas) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Inconsistencies and Varying Cold Chain Standards Across Member States

Halal and pharmaceutical regulations vary by country, complicating facility design, staff training, and cross-border documentation. Indonesia’s Regulation 42/2024 mandates halal-only cold rooms and dedicated handling flows, increasing costs for certified sites. Malaysia’s MS 2400 standard requires segregation across logistics zones, raising configuration and audit demands. Singapore’s HSA GDP rules enforce validated equipment and chain-of-custody for pharmaceutical logistics, unlike some neighboring markets. These differences increase onboarding costs and risk shipment delays due to misaligned paperwork. Large integrators with centralized compliance programs adapt faster, influencing market share in the ASEAN cold chain logistics market.

High Upfront Capital Expenditure Deterring SME Cold Chain Operators

Building and operating validated cold capacity requires refrigeration systems, backup power, and monitoring tools that many SMEs find difficult to finance. Fisheries in the Philippines continue to face high post-harvest losses due to limited cold rooms and blast freezers at landing sites, which shows how financing gaps translate into spoilage. Electricity tariffs and grid reliability issues add to cost and risk, and they can stretch breakeven volumes for small facilities that are not part of multi-tenant or networked footprints. Operators without resilient power and monitoring capacity face higher product-loss risk during outages and storms, which lowers lender confidence and access to affordable credit. These constraints push the ASEAN cold chain logistics market toward consolidation by players with stronger balance sheets and multi-tenant models. As larger providers expand, some remote zones may see fewer service options than before, which raises last-mile costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Anchors Market, Value-Added Accelerates

Refrigerated storage commands 49.3% share in 2025, while value-added services are growing fastest at 5.7% CAGR as brand owners outsource blast-freezing, repackaging, GDP-compliant labeling, and validated packing for life-sciences loads. Within the ASEAN cold chain logistics market size context, pharma-focused nodes with -80°C capacity and digitized custody are expanding as operators build GDP-ready environments for clinical-trial materials and biologics. UPS doubled Singapore capacity in June 2025, adding ultra-low freezers and visibility features that help healthcare shippers meet audit requirements and timing constraints. Road remains the primary mode for intra-country logistics and uses GPS-linked telemetry for exception handling and route optimization in sensitive lanes. Maritime networks continue to scale inter-island connectivity for frozen foods, and regional carriers have signaled reefer expansion to serve domestic and export flows. Airfreight supports time-bound biologics and high-care shipments, where transit integrity and chain-of-custody records define provider choice.

Public warehousing dominates, where importers and distributors prefer scalable, asset-light access rather than private investment that may be exposed to regulatory change. Private cold rooms remain critical for vertically integrated processors that prioritize control of inventory turns, blending, and export readiness. Thailand’s new multi-temperature warehouse commissioned near Bangkok in December 2024 highlights a build pattern that supports e-commerce and retail consolidation as store networks expand. In pharmaceuticals, GDP rules steer flows toward audited facilities and handling zones with validated equipment, which supports premium service differentiation. As energy resilience and monitoring become standard, service expectations are rising across the ASEAN cold chain logistics market, and providers are using compliance status to signal capability. The ASEAN cold chain logistics industry is therefore shifting toward higher service baselines supported by documentation and technology adoption.

By Temperature Type: Frozen Leads, Chilled Gains on Urban Retail

Frozen goods at -18 to 0°C hold a 42.6% share in 2025, led by export-driven seafood and poultry that require longer holding times and vessel-aligned shipping. Chilled flows at 0 to 5°C are expanding faster at a 5.2% CAGR as convenience formats scale across ASEAN and rely on tighter tolerances and multiple daily replenishments. Ultra-low temperature segments below -20°C are growing with mRNA and cell therapy pipelines, and new -80°C infrastructure in regional hubs is enabling longer-distance healthcare lanes with active-temperature containers and validated handling. Frozen remains the anchor due to export scheduling and buffer stocks for seafood processors, yet the margin opportunity is tilting toward chilled, where short shelf life, tighter temperature bands, and frequent turns deter under-invested competition. Operators that invest in electronic monitoring and responsive routing gain trust from retailers and healthcare clients who measure performance with strict excursion thresholds.

Ambient-controlled lanes remain relevant for items that are heat-sensitive but stable above 15°C, though the focus in ASEAN’s urban centers is on chilled assortments that align with daily shopping habits. The ASEAN cold chain logistics market is adapting capacity to balance these needs, and the service mix is trending toward more frequent, smaller-lot deliveries in major cities. Digital logs and audit trails are becoming a norm in chilled operations, which ties facilities and carriers more closely to store networks and regulatory expectations. Frozen categories continue to rely on sea freight and cross-border trucking for regional distribution, while air lanes serve premium fresh and healthcare shipments on tight schedules. In practice, temperature regimes shape capacity plans for warehouses, fleets, and nodes, and they influence where providers invest next in the ASEAN cold chain logistics industry.

By Application: Traditional Proteins Meet Biologic Disruption

Fish and seafood hold a 27.4% share in 2025, reflecting strong export programs and greater traceability requirements that drive demand for validated storage and documented handling. Vietnam’s March 2025 launch of electronic catch documentation has reduced border times and claims, which supports both chilled and frozen categories in premium markets. Vaccines and clinical-trial materials are the fastest-growing application at 5.5% CAGR, supported by new GDP-certified capacity and ultra-low equipment across key hubs. Quality and custody expectations in these lanes exceed food-grade thresholds, which elevate documentation and monitoring requirements throughout multi-tenant facilities. As audit norms spread, exporters and healthcare shippers gravitate to providers that can evidence continuous control rather than only storage capacity.

Ready-to-eat meals, dairy, bakery, and produce expand alongside modern retail penetration as stores tailor chilled assortments for fresh consumption and grab-and-go meals. Halal logistics rules in Indonesia and Malaysia shape facility layouts and routes for meat and prepared foods, which reinforces demand for certified multi-temperature nodes. Seafood traceability systems are informing multi-commodity practices in shared warehouses and cross-docks, which helps standardize processes and reduce compliance risks. Within the ASEAN cold chain logistics market size view, vaccines and trial materials represent a growing revenue mix that improves seasonality balance for facilities serving seafood and other food categories. This broadens the addressable demand for licensed providers that invest early in certifications and monitoring technology.

Geography Analysis

Indonesia holds the largest share in 2025 and is supported by a substantial food-security budget and a national logistics blueprint that aims to improve infrastructure and digitize workflows for greater resilience. Government programs include post-harvest cold storage and warehouse upgrades, which help reduce losses and stabilize stocks for staples and perishables. Primary clusters in Java handle significant volumes, while islands in Kalimantan, Sulawesi, and Papua face higher operating costs due to grid reliability and distance to markets. Providers with resilient power, flexible capacity, and route planning capabilities are better positioned to expand service coverage. With growing retail and healthcare demand, Indonesia remains a focal point in the ASEAN cold chain logistics market for both domestic distribution and export-aligned storage.

Thailand is projected to grow fastest through 2031, driven by the Eastern Economic Corridor’s role as a regional manufacturing and export hub and the commissioning of multi-temperature warehouses near Bangkok. These facilities support modern retail and e-commerce flows, which require rapid-turn chilled and frozen handling and closer collaboration with carriers. Policy support for climate-resilient infrastructure encourages energy-efficient systems and protected sites that can maintain uptime during severe weather. Thailand’s connectivity to neighboring markets improves cross-border flows and enables multi-country procurement strategies that rely on consistent cold integrity. Together, these shifts upgrade service baselines and attract new entrants that can meet modern quality and monitoring expectations in the ASEAN cold chain logistics market.

Vietnam continues ramping up cold capacity with fiscal incentives for logistics investments and with projects that serve both food and life sciences shipments. The 2025-2026 timeline for new facilities in Dong Nai includes GDP-certified pharma zones and seafood blast-freezing, which enhances utilization and reduces seasonality exposure. Singapore remains a regulated gateway for life sciences, and recent expansions added ultra-low freezers and custody controls to meet audit needs. Malaysia’s halal standards support regional consolidation for compliant flows, while the Philippines accelerates build-outs of cold rooms and modular sites to improve access in dispersed island geographies. RCEP and CPTPP processes anchor these developments by encouraging expedited treatment for perishables and standardized documentation that lifts cross-border predictability in the ASEAN cold chain logistics market.

Competitive Landscape

Competitive intensity is rising as global integrators scale certified capacity and digital controls, while regional specialists retain edges in local compliance and last-mile coverage. DHL inaugurated Malaysia’s first dual-certified facility at KLIA in February 2026 with validated 15-25°C and 2-8°C zones for biologics and vaccines, which signals higher service expectations in regional healthcare lanes. UPS doubled healthcare capacity in Singapore in 2025, adding ultra-low freezers and real-time chain-of-custody capabilities that appeal to clinical-trial sponsors. These moves highlight how audit-readiness and temperature discipline have become primary selection factors in the ASEAN cold chain logistics market.

Mergers, acquisitions, and platform expansions are consolidating capacity and accelerating market entry across priority corridors. Lineage Logistics completed a USD 4.4 billion IPO in 2024 and then acquired ColdPoint for USD 223 million, which expanded its frozen-storage footprint across Southeast Asia and adjacent regions. New and expanded sites also remain central to growth, such as Linfox’s 19,000-square-meter, 28,000-pallet Bangkok-area warehouse supporting modern retail and e-commerce flows. YCH Group’s SuperPort in Vinh Phuc integrates net-zero design with multimodal positioning, which aligns with multinational buyers that emphasize emissions reporting and energy resilience. These developments reinforce the multi-country reach and rising service baselines in the ASEAN cold chain logistics market.

Operational resilience is a key differentiator as severe weather and flooding strain networks and power grids. WMO reporting on devastating rainfall underscores the need for backup power and mobile capacity that can be positioned ahead of storms to protect healthcare and high-value food loads. Regional ocean carriers are expanding reefer capacity for inter-island and export routes, which helps stabilize flows of frozen and chilled goods despite episodic disruptions. Digital traceability in fisheries has moved from pilots to operational programs, which raises the bar for real-time data and documented histories across facilities and carriers. Collectively, these factors shape a competitive pattern where technology adoption, compliance credentials, and resilience planning drive share gains in the ASEAN cold chain logistics market.

ASEAN Cold Chain Logistics Industry Leaders

Deutsche Post DHL

Nippon Express

United Parcel Service (UPS)

Yusen Logistics (Part of NYK Line)

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Supply Chain launched Malaysia's first dual-certified pharmaceutical cold-chain facility at Kuala Lumpur International Airport, a 38,000-square-foot site with validated 15-25°C and 2-8°C zones, supporting biologics and vaccine distribution under HSA and JAKIM compliance.

- June 2025: UPS Healthcare doubled its Singapore cold-chain capacity by commissioning an 11,500-square-meter GDP-certified facility near Changi Airport, equipped with -80°C ultra-low freezers and real-time chain-of-custody tracking for clinical-trial materials and mRNA vaccines.

- April 2025: Deutsche Post DHL Group allocated EUR 500 million (USD 520 million) to expand cold-chain infrastructure in Asia-Pacific, including CRYOPDP acquisition and GDP/GMP-certified sites in China, Malaysia, Singapore, and Australia, under a EUR 2 billion DHL Health Logistics plan by 2030.

- March 2025: LOTTE Global Logistics is building a USD 34 million cold-chain center in Dong Nai, Vietnam, with GDP-certified zones and blast-freezing for seafood, set to open by May 2026.

ASEAN Cold Chain Logistics Market Report Scope

Cold chain refers to temperature-controlled logistics procedures. A complete background analysis of the ASEAN Cold Chain Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and geopolitical impact analysis is included in the report.

The ASEAN cold chain logistics market is segmented by service, temperature, application, and geography. By service, the market is segmented by storage, transportation, and value-added service. By temperature, the market is segmented into ambient, chilled, Deep-Frozen/Ultra-Low, and frozen. By application, the market is segmented into Fruits and Vegetables, Meat and Poultry, Fish and Seafood, Dairy and Frozen Desserts, and other applications, and by geography, the market is segmented by Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines, and the Rest of ASEAN.

The report offers market size and forecasts for the ASEAN cold chain logistics market in value (USD) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5°C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen/Ultra-Low (less than-20°C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

By Geography

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Malaysia |

| Philippines |

| Rest of ASEAN |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen/Ultra-Low (less than-20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

| By Geography | Singapore | |

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Malaysia | ||

| Philippines | ||

| Rest of ASEAN | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the ASEAN cold chain logistics market?

The ASEAN cold chain logistics market size was USD 18.81 billion in 2025 and is projected to reach USD 24.43 billion by 2031 at a 4.9% CAGR during 2026-2031.

Which service types are expanding fastest in the ASEAN cold chain logistics market?

Value-added services such as blast-freezing, GDP-compliant labeling, and clinical-trial kitting are projected to grow the fastest at a 5.7% CAGR during 2026–2031, while refrigerated storage remained the largest segment by share in 2025.

Which temperature regime leads demand in the ASEAN cold chain logistics market?

Frozen flows at -18 to 0°C led with a 42.6% share in 2025, while chilled logistics at 0 to 5°C is growing faster due to the expansion of convenience retail and fresh assortments.

Which applications contribute most to volumes in the ASEAN cold chain logistics market?

Fish and seafood held the largest share at 27.4% in 2025, while vaccines and clinical-trial materials post the highest growth due to GDP-certified hubs and ultra-low equipment during 2026–2031.

Which countries are most influential in the ASEAN cold chain logistics market?

Indonesia led with a 22.4% share in 2025 due to its scale and policy support, while Thailand is the fastest-growing market with a 5.1% CAGR through 2031, supported by new multi-temperature facilities.

How do trade pacts influence operations in the ASEAN cold chain logistics market?

RCEP and CPTPP encourage expedited treatment and e-certification for perishables, which reduces delays and rewards certified multi-country networks with stronger cross-border reliability.

Page last updated on: