Asia-Pacific Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

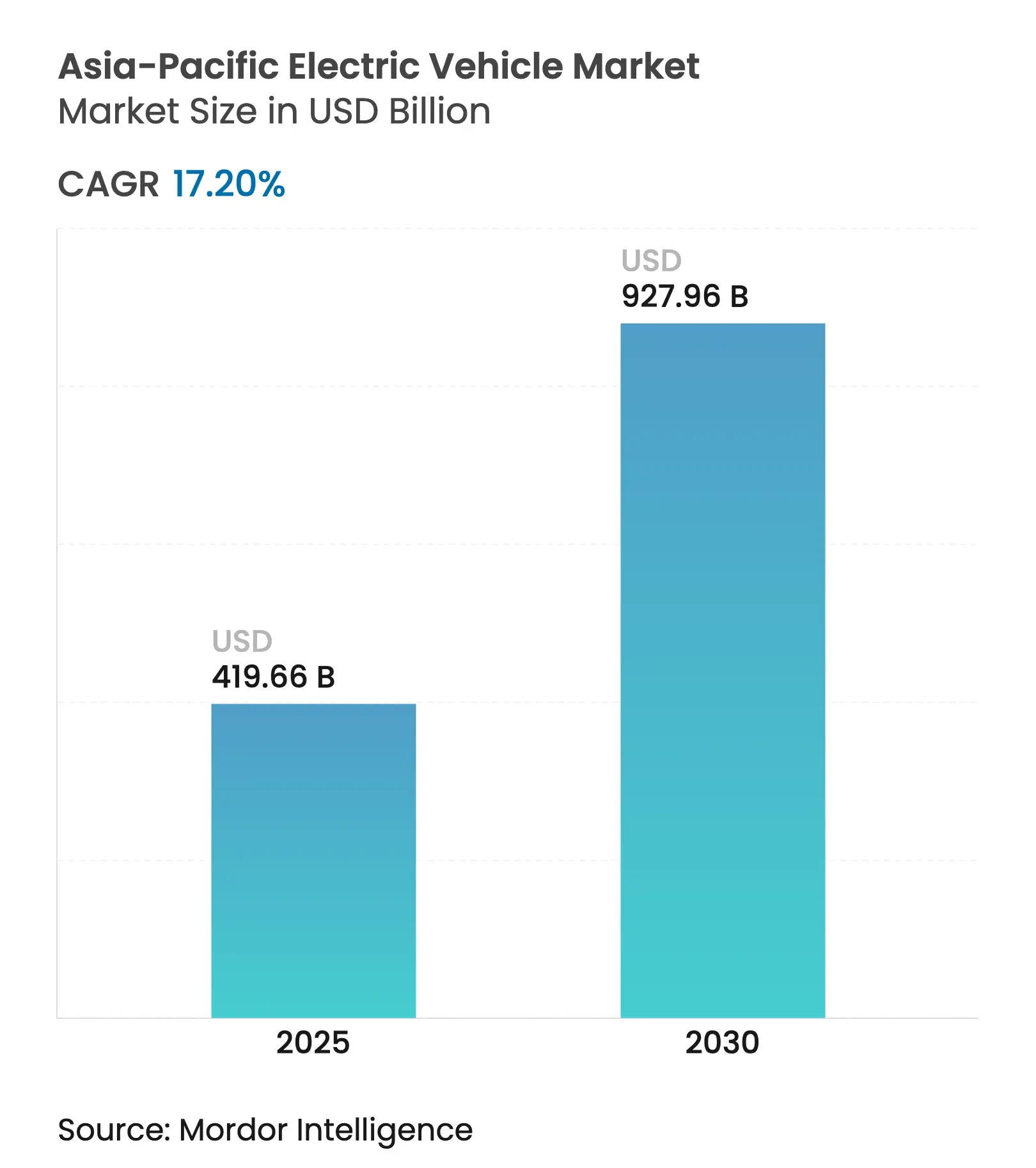

| Market Size (2025) | USD 419.66 Billion |

| Market Size (2030) | USD 927.96 Billion |

| Growth Rate (2025 - 2030) | 17.20 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Asia-Pacific Electric Vehicle Market Analysis by Mordor Intelligence

The Asia Pacific Electric Vehicle market size is valued at USD 419.66 billion and is projected to reach USD 927.96 billion by 2030, registering a 17.20% CAGR during the forecast period. Government incentives, zero-emission mandates, and the growth of local battery manufacturing fuel this expansion. These measures aim to reduce greenhouse gas emissions and promote sustainable transportation solutions. As battery prices decline and fast-charging infrastructure expands, the cost gap with internal combustion vehicles shrinks, making electric cars more accessible to consumers. China leads in demand, offering significant opportunities for domestic suppliers to scale operations and innovate. This dominance has also prompted production shifts to emerging markets such as India, Indonesia, and Thailand, where governments actively support the development of local manufacturing capabilities to meet growing regional demand.

Key Report Takeaways

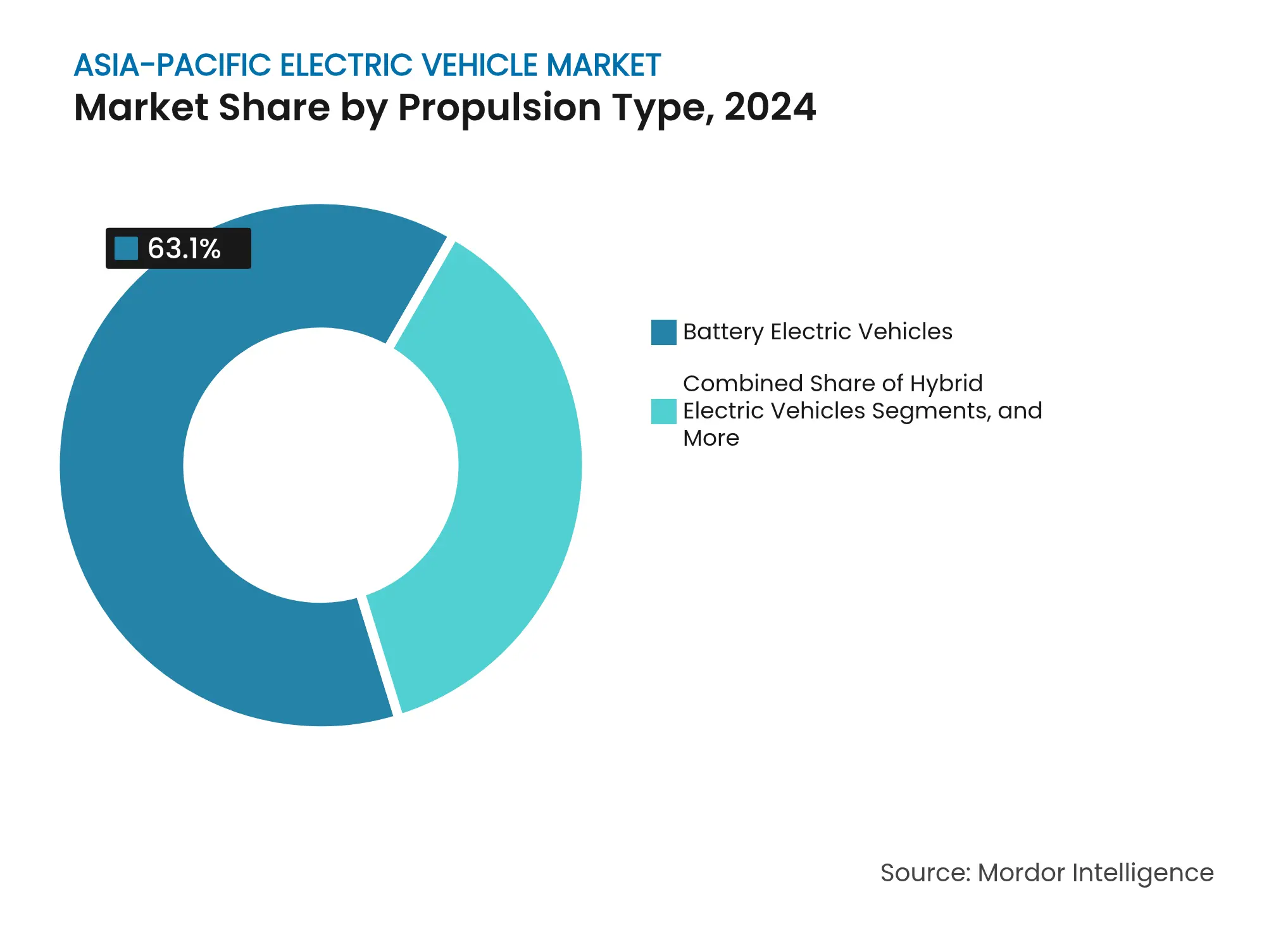

- By propulsion type, battery electric vehicles held 63.12% share of the Asia-Pacific electric vehicle market in 2024, while fuel-cell models are set to expand at 28.85% CAGR to 2030.

- By vehicle type, passenger cars led with 71.38% share of the Asia-Pacific electric vehicle market in 2024; commercial vehicles are forecast to advance at 18.42% CAGR through 2030.

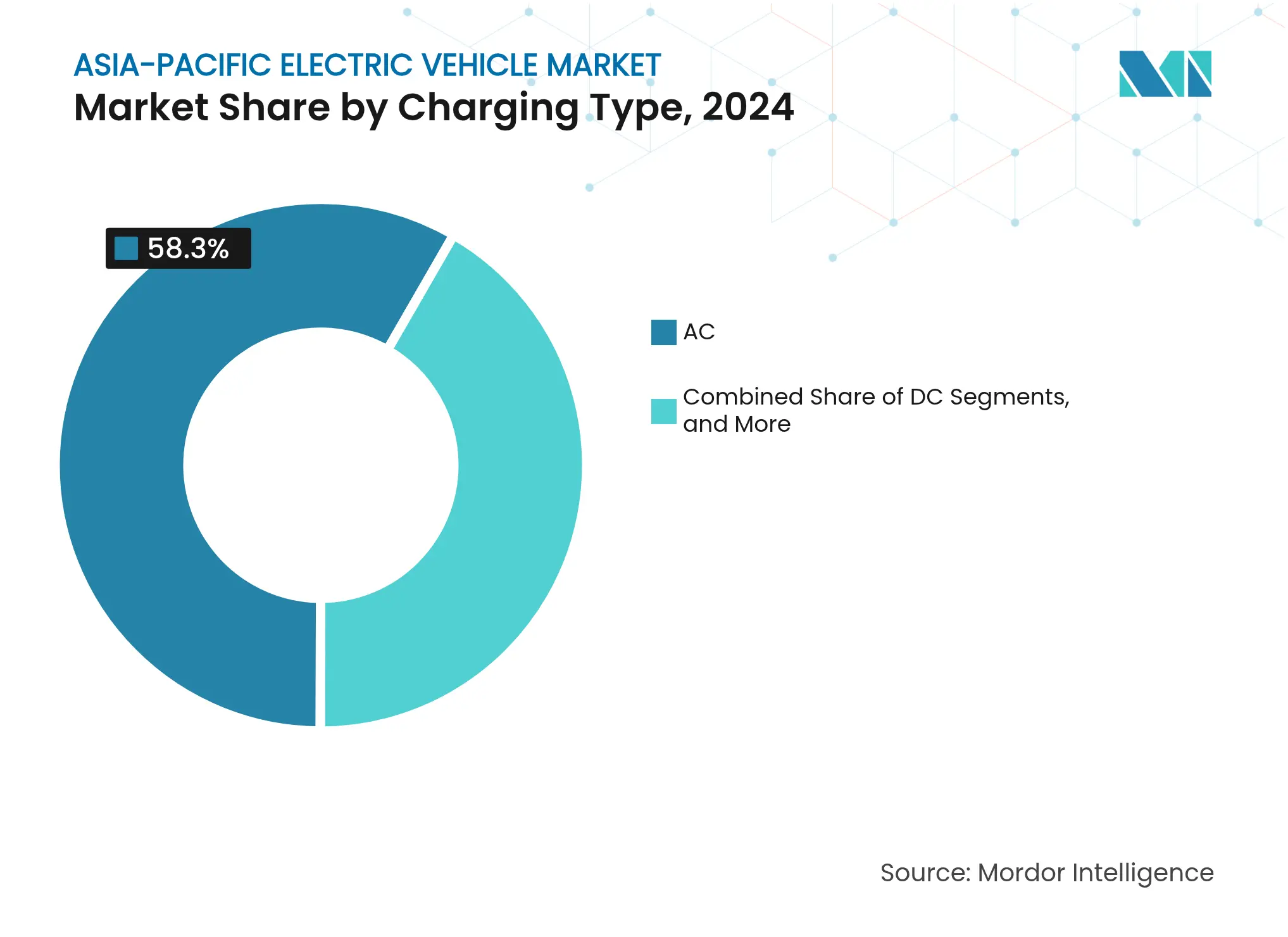

- By charging type, AC (less than 22 kW) stations accounted for 58.27% share of the Asia-Pacific electric vehicle market in 2024, whereas ultra-fast/megawatt systems are poised for a 32.05% CAGR during 2025-2030.

- By vehicle class, mid-priced models captured 67.92% share of the Asia-Pacific electric vehicle market in 2024, but the luxury segment is projected to rise at a 20.48% CAGR by 2030.

- By Country, China commanded a 61.08 % share of the Asia-Pacific electric vehicle market in 2024, while India is on course for a 24.13% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Electric Vehicle Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government Incentives and Zero-Emission Mandates Government Incentives and Zero-Emission Mandates | +4.3% | China, India, ASEAN | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+4.3% | Geographic Relevance:China, India, ASEAN | Impact Timeline:Medium term (2-4 years) |

Rapid Expansion of Fast-Charging Networks Rapid Expansion of Fast-Charging Networks | +3.8% | China, Japan, South Korea; extending to ASEAN | Short term (≤ 2 years) | |||

Falling Battery Prices and Shift to LFP/Solid-State Falling Battery Prices and Shift to LFP/Solid-State | +3.1% | Manufacturing hubs in China, Japan | Long term (≥ 4 years) | |||

Corporate Fleet Decarbonization Push Corporate Fleet Decarbonization Push | +2.5% | Urban clusters across Asia-Pacific | Medium term (2-4 years) | |||

V2G Monetization Pilots Gaining Scale V2G Monetization Pilots Gaining Scale | +1.9% | Japan, South Korea, Selected EU Pilot Regions | Medium term (2-4 years) | |||

Battery-Passport Traceability Regulation Battery-Passport Traceability Regulation | +1.7% | Global, Focus on Europe, China | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Government Incentives and Zero-Emission Mandates

Policy harmonization across Asia-Pacific creates unprecedented market momentum, with China's extension of EV subsidies through 2027 complementing India's Production Linked Incentive scheme and outlays of USD 26 billion[1]"Government Scales Up PLI Budget to Accelerate Manufacturing," PIB, pib.gov.in. Thailand's EV3.5 policy mandates 30% electric vehicle production by 2030, creating regulatory certainty that drives long-term investment decisions. Indonesia has set a target to deploy 2 million electric vehicles and 12 million electric two-wheelers by 2030[2]Adli Azayaka Huda, "Indonesian Electric Vehicle Boom: A temporary trend or a long-term vision?," IISD, www.iisd.org. This initiative primarily aims to reduce carbon emissions, as the transportation sector remains one of the country's most significant contributors to CO2 emissions.

These mandates increasingly incorporate local content requirements, with Malaysia requiring 40% local assembly for EV tax exemptions and Vietnam offering charging infrastructure subsidies exclusively for domestically manufactured vehicles. This forces global manufacturers to establish regional production capabilities rather than rely on imports.

Rapid Expansion of Fast-Charging Networks

Accelerated investments in EV charging infrastructure are transforming market dynamics. Range anxiety, previously a significant barrier, has become a strategic advantage for early adopters. In China, the deployment of extensive public charging networks highlights firm governmental and private sector commitments to facilitating mass EV adoption. Similarly, Japan is investing substantially in ultra-fast charging corridors to enhance network connectivity and reduce charging durations.

In Australia, funding initiatives support establishing fast-charging sites across regional areas, addressing geographic challenges that have historically constrained EV adoption in rural markets. These strategic deployments are improving accessibility and fostering confidence among consumers and fleet operators regarding long-distance EV travel. Beyond basic charging infrastructure, Vehicle-to-Grid (V2G) monetization pilots in South Australia and Thailand are demonstrating the potential of advanced charging solutions to generate additional revenue streams, fundamentally altering total cost of ownership calculations for fleet operators.

Falling Battery Prices and Shift to LFP/Solid-State

Battery technology evolution creates cost advantages that accelerate market penetration. Lithium Iron Phosphate (LFP) batteries achieve significant cost reduction compared to traditional lithium-ion, offering superior thermal stability and longer cycle life. CATL's Qilin battery technology delivers 10-minute charging to 80% capacity, addressing the primary consumer concern about charging convenience. In comparison, solid-state battery developments from Toyota and QuantumScape promise 50% weight reduction and 2x energy density by 2027. Chinese manufacturers' LFP dominance creates supply chain advantages, with BYD's Blade Battery technology licensing to other manufacturers establishing LFP as the preferred chemistry for mass-market vehicles, while premium segments increasingly adopt silicon nanowire anodes that offer 30% capacity improvements over conventional graphite electrodes.

Corporate Fleet Decarbonization Push

Enterprise sustainability mandates drive B2B adoption that creates economies of scale for consumer markets, with logistics companies pursuing operational cost advantages through electric commercial vehicles that offer significantly lower fuel costs and reduced maintenance requirements. BYD's partnership with Grab to deploy electric cars across Southeast Asia demonstrates how ride-sharing platforms accelerate consumer acceptance while creating predictable demand for charging infrastructure investments. Corporate procurement cycles increasingly incorporate total cost of ownership models that favor electric vehicles despite higher upfront costs, with fleet operators reporting significant operational savings over 5-year periods when factoring in fuel, maintenance, and regulatory compliance costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Upfront Cost in Emerging ASEAN Markets High Upfront Cost in Emerging ASEAN Markets | -2.8% | Indonesia, Philippines, Vietnam, Malaysia | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-2.8% | Geographic Relevance:Indonesia, Philippines, Vietnam, Malaysia | Impact Timeline:Short term (≤ 2 years) |

Rural Grid Constraints for Fast Charging Rural Grid Constraints for Fast Charging | -1.9% | India, Indonesia, Rural China, Philippines | Medium term (2-4 years) | |||

Rising Trade Barriers on Chinese EVs Rising Trade Barriers on Chinese EVs | -2.2% | Southeast Asia, Europe, North America | Medium term (2-4 years) | |||

Lithium-Price Volatility Lithium-Price Volatility | -1.6% | Global, Focus on China, Australia, South America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Cost in Emerging ASEAN Markets

Price sensitivity in developing markets creates adoption barriers despite government incentives, with electric vehicles commanding a significant premium over ICE equivalents in Indonesia, the Philippines, and Vietnam. Currency volatility exacerbates affordability challenges, with Indonesian Rupiah depreciation increasing imported battery costs in 2024, while local assembly requirements force manufacturers to establish production capabilities before achieving economies of scale. Financing infrastructure limitations compound the challenge, as traditional auto loans fail to account for electric vehicle residual values and total cost of ownership advantages, requiring new financial products that incorporate energy savings and government incentives into affordability calculations.

Rural Grid Constraints for Fast Charging

Infrastructure limitations in rural areas constrain market expansion beyond urban centers, with India's rural electrification program struggling to provide a consistent power supply for fast-charging requirements. Grid stability concerns limit fast-charging installations to areas with robust electrical infrastructure, creating a geographic divide that favors urban adoption while constraining rural penetration necessary for nationwide market development. Power generation capacity constraints require coordinated infrastructure investments, with charging network expansion dependent on grid modernization programs that extend implementation timelines and increase capital requirements for market development.

Segment Analysis

By Propulsion Type: Battery Electric Dominance Faces Fuel-Cell Disruption

Battery Electric Vehicles hold a 63.12% share of the Asia-Pacific electric vehicle market in 2024, while Fuel-Cell Electric Vehicles emerge as the fastest-growing propulsion segment at 28.85% CAGR through 2030. This is due to strategic investments in hydrogen infrastructure by Japan and South Korea, which position fuel cells for commercial vehicle applications where weight and range advantages justify higher costs. Hybrid electric cars maintain steady demand in markets with limited charging infrastructure. In contrast, plug-in hybrid electric vehicles serve as a transition technology for consumers hesitant to commit to full electrification.

Battery technology standardization efforts by the China Association of Automobile Manufacturers create interoperability advantages that reduce manufacturing costs and improve consumer confidence. In contrast, solid-state battery developments promise to eliminate range anxiety concerns that favor hybrid solutions in rural markets. Premium market expansion for fuel cell technology, complementing commercial vehicle applications with consumer-focused luxury positioning that leverages hydrogen's rapid refueling advantages over battery charging times.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: Commercial Acceleration Challenges Passenger Dominance

Passenger cars captured 71.38% share of the Asia-Pacific electric vehicle market in 2024, but commercial vehicles are projected to post an 18.42% CAGR, narrowing the gap by 2030. Parcel-delivery electrification in Jakarta, Mumbai, and Shenzhen draws on low-maintenance e-vans that cut fuel bills significantly over five-year horizons.

Regulatory green zones block ICE freight from downtown Seoul and Beijing, propelling e-truck uptake. Fleet telematics proves downtime reductions via predictive maintenance, enhancing ROI cases. Passenger segment growth increasingly tilts toward compact SUVs, with over-the-air software updates and infotainment ecosystems forming new battlegrounds for brand loyalty. Shared-mobility operators further amplify commercial demand, blurring the traditional passenger-versus-fleet demarcation.

By Charging Type: Ultra-Fast Growth Challenges AC Dominance

AC points under 22 kW represented 58.27% of the Asia-Pacific electric vehicle market in 2024. They controlled the largest installed base market share, but ultra-fast and megawatt systems will grow 32.05% through 2030. Japan’s CHAdeMO 3.0 now supports plug-and-charge and bidirectional energy flows, anchoring V2G programs that remunerate owners during peak-demand events.

DC fast hubs around malls and transit centers benefit from rising battery capacities, ensuring single-stop weeklong ranges for urban commuters. Battery-swap technology, led by NIO, underpins taxi and ride-hail segments where uptime trumps ownership economics. Interoperability regulations in India mandate at least one combined charging system (CCS) connector per station, improving inclusivity. As grid capacity scales, profit pools migrate from connection fees to energy-as-a-service and dynamic load-balancing solutions.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Class: Luxury Premiumization Drives Technology Adoption

Mid-priced models held 67.92% of the Asia-Pacific electric vehicle market in 2024, while the luxury tier is forecast to expand at a 20.48% CAGR through 2030. High-end launches such as the Tesla Model S Plaid and BMW iX deploy 100 kWh-plus packs delivering 500 km ranges, establishing benchmarks that gradually trickle down to mainstream trims. Chinese newcomers NIO and Xpeng position tech-first branding with Level-3 autonomy and immersive cockpit HMIs, challenging incumbents on connected-services value.

Battery-as-a-service subscriptions help decouple hardware price from energy storage, softening luxury entry points while guaranteeing residual value. Premium EV buyers also become early adopters for solid-state and silicon-anode packs, accelerating economies of scale. Meanwhile, tax-bracket thresholds in India and Thailand keep sticker prices for mid-range models within subsidy eligibility, ensuring the volume backbone remains intact.

Geography Analysis

China holds a 61.08% share of the Asia-Pacific electric vehicle market in 2024, highlighting strong policy support, manufacturing scale, and consumer acceptance, driving global competitiveness. Market maturity fosters technology exports, with CATL and BYD establishing Southeast Asian facilities to meet regional demand and bypass Western trade barriers. Domestic competition between automakers like Geely, SAIC, NIO, and Xpeng accelerates innovation. Urban emission regulations and rural electrification programs expand EV adoption and charging infrastructure.

India, the fastest-growing market with a 24.13% CAGR during the forecast period, benefits from government policies, manufacturing incentives, and consumer financing programs addressing affordability. The Production Linked Incentive scheme attracts global manufacturers, while Tata Motors and Mahindra leverage local expertise to compete. Two-wheeler electrification leads adoption, driven by urban air quality concerns. Rural grid limitations necessitate solutions like battery swapping and solar-powered charging stations.

ASEAN markets emerge as manufacturing hubs through coordinated policies. Indonesia’s USD 1 billion BYD investment, Thailand’s EV3.5 incentives, and Malaysia’s local content requirements attract production investments. Vietnam’s charging subsidies and the Philippines’ import duty exemptions support regional demand. Japan and South Korea maintain technology leadership with Toyota’s hydrogen strategy and Samsung SDI’s solid-state battery research, focusing on advanced technology exports over cost advantages.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

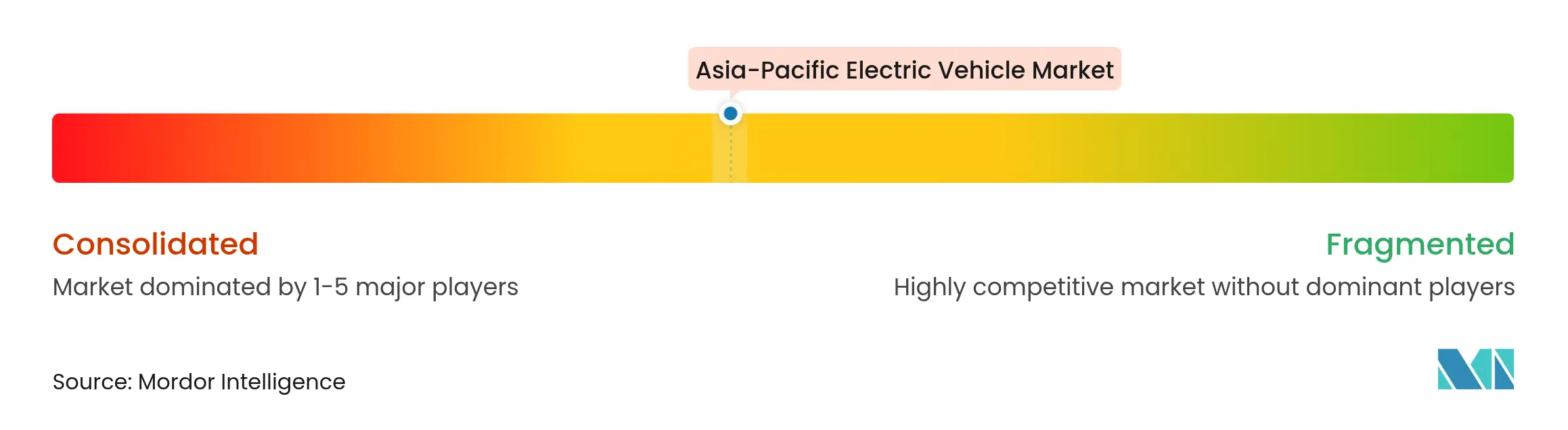

Market Concentration

Market concentration varies dramatically across sub-regions. China's consolidated structure, dominated by BYD, Tesla, and domestic manufacturers, contrasts sharply with fragmented competition in India and ASEAN markets, where local assembly requirements create opportunities for established automakers and emerging players. Chinese manufacturers leverage vertical integration advantages, controlling battery production, charging infrastructure, and vehicle assembly to achieve cost leadership that enables aggressive international expansion despite trade barriers imposed by Western markets.

White-space opportunities emerge in commercial vehicle electrification, rural market penetration, and charging infrastructure monetization, where established automotive manufacturers face competition from technology companies, energy utilities, and mobility service providers entering the ecosystem. Patent filings in solid-state battery technology and vehicle-to-grid integration create competitive moats, with Japanese and Korean companies maintaining technology leadership despite Chinese manufacturing scale advantages. Regulatory influence from local content requirements and emission standards creates geographic competitive advantages, forcing global manufacturers to establish regional production capabilities rather than rely on centralized manufacturing strategies that previously dominated the automotive industry.

Asia-Pacific Electric Vehicle Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Chery unveiled the Fulwin X3L, its latest range-extended electric SUV in China. Buyers can choose from one 4WD variant and three RWD options. The RWD variants of the Fulwin X3L, equipped with a 185kW/300Nm permanent magnet synchronous motor and a choice of either a 20.64kWh or 33.68kWh lithium-iron phosphate battery, boast an electric-only range of 135km or 215km.

- September 2025: Tata Motors revealed that its electric small commercial vehicles (SCVs) now have access to over 25,000 public charging stations throughout India. Strategically positioned at key logistics points, these stations are distributed across more than 150 cities, including major urban hubs.

Table of Contents for Asia-Pacific Electric Vehicle Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Government Incentives And Zero-Emission Mandates

- 4.2.2Rapid Expansion Of Fast-Charging Networks

- 4.2.3Falling Battery Prices And Shift To LFP/Solid-State

- 4.2.4Corporate Fleet Decarbonization Push

- 4.2.5V2G Monetization Pilots Gaining Scale

- 4.2.6Battery-Passport Traceability Regulation

- 4.3Market Restraints

- 4.3.1High Upfront Cost In Emerging ASEAN Markets

- 4.3.2Rural Grid Constraints For Fast Charging

- 4.3.3Rising Trade Barriers On Chinese EVs

- 4.3.4Lithium-Price Volatility

- 4.4Value/Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Investment and Funding Landscape

5. Market Size and Growth Forecast (Value (USD) and Volume (Units))

- 5.1By Propulsion Type

- 5.1.1Battery Electric Vehicles

- 5.1.2Hybrid Electric Vehicles

- 5.1.3Plug-in Hybrid Electric Vehicles

- 5.1.4Fuel-Cell Electric Vehicles

- 5.2By Vehicle Type

- 5.2.1Passenger Cars

- 5.2.2Commercial Vehicles

- 5.2.3Two Wheelers

- 5.2.4Three Wheelers

- 5.3By Charging Type

- 5.3.1AC (Less than 22 kW)

- 5.3.2DC Fast (More Than 50 kW to 350 kW)

- 5.3.3Ultra-fast/Megawatt

- 5.3.4Battery-Swapping

- 5.4By Vehicle Class

- 5.4.1Mid-priced

- 5.4.2Luxury

- 5.5By Country

- 5.5.1China

- 5.5.2Japan

- 5.5.3India

- 5.5.4South Korea

- 5.5.5Indonesia

- 5.5.6Thailand

- 5.5.7Malaysia

- 5.5.8Vietnam

- 5.5.9Philippines

- 5.5.10Singapore

- 5.5.11Australia

- 5.5.12New Zealand

- 5.5.13Rest of Asia-Pacific

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1BYD Co. Ltd.

- 6.4.2SAIC Motor Corp.

- 6.4.3Tesla Inc.

- 6.4.4BMW AG

- 6.4.5Geely Auto Group

- 6.4.6Hyundai Motor Company

- 6.4.7Kia Corporation

- 6.4.8Toyota Motor Corporation

- 6.4.9Nissan Motor Co. Ltd.

- 6.4.10Honda Motor Co. Ltd.

- 6.4.11Tata Motors Ltd.

- 6.4.12Mahindra and Mahindra Ltd.

- 6.4.13Xpeng Inc.

- 6.4.14NIO Inc.

- 6.4.15Great Wall Motor Co.

- 6.4.16Changan Automobile

- 6.4.17VinFast Auto Ltd.

- 6.4.18GAC Aion

- 6.4.19Yutong Bus Co.

- 6.4.20Proterra Inc.

- 6.4.21Stellantis N.V.

- 6.4.22Yamaha Motor Co.Ltd.

- 6.4.23Hero MotoCorp Limited

7. Market Opportunities and Future Outlook

- 7.1White-space and Unmet-need Assessment

Asia-Pacific Electric Vehicle Market Report Scope

An electric vehicle (EV) operates on an electric motor instead of an internal combustion engine that generates power by burning a mix of fuel and gases. Due to rising pollution, global warming, and depleting natural resources, EVs are becoming a possible replacement option for current-generation automobiles across the region.

The Asia-Pacific electric vehicle market is segmented by propulsion type, vehicle type, charging type, and country.

By propulsion type, the market is segmented into battery electric vehicles, hybrid electric vehicles, plug-in hybrid electric vehicles, and fuel cell electric vehicles. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By charging type, the market is segmented as normal charging and fast charging. By country, the market is segmented into China, India, Japan, South Korea, and Rest of Asia-Pacific.

The report offers market size and forecasts in value (USD) and volume (units) for all the above segments.