Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

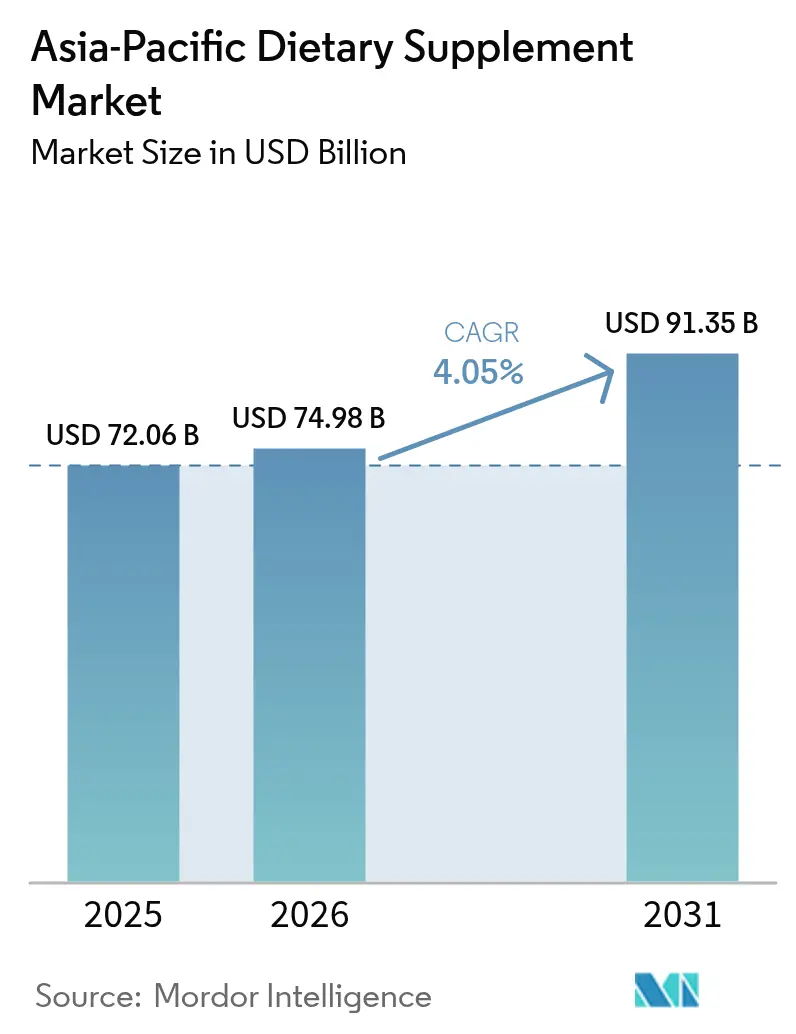

| Base Year Market Size (2025) | USD 72.06 Billion |

| Market Size (2026) | USD 74.98 Billion |

| Market Size (2031) | USD 91.35 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Dietary Supplement Market Analysis by Mordor Intelligence

Asia-Pacific dietary supplements market size in 2026 is estimated at USD 74.98 billion, growing from 2025 value of USD 72.06 billion with 2031 projections showing USD 91.35 billion, growing at 4.05% CAGR over 2026-2031. The supplements market expansion is driven by consumers' increased focus on preventive healthcare and immune support, digital adoption in distribution and marketing channels, and market acceptance of various supplement formats, including gummies, powders, and liquid concentrates. China maintains its position as the primary growth driver, supported by its population size and health awareness levels. South Korea and Japan show higher revenue per user through premium products with specialized ingredients and improved bioavailability. Besides, India's expanding middle class and health awareness contribute substantially to volume growth. The e-commerce sector continues to reshape distribution through direct-to-consumer models and marketplace platforms. Market demand for clean-label and plant-based products is decreasing the synthetic ingredients' market share. Furthermore, regulatory standards in China, Japan, and Australia have increased operational costs through quality control and documentation requirements. These regulations strengthen established brands' positions by enhancing consumer confidence through product safety standards and efficacy claim verification.

Key Report Takeaways

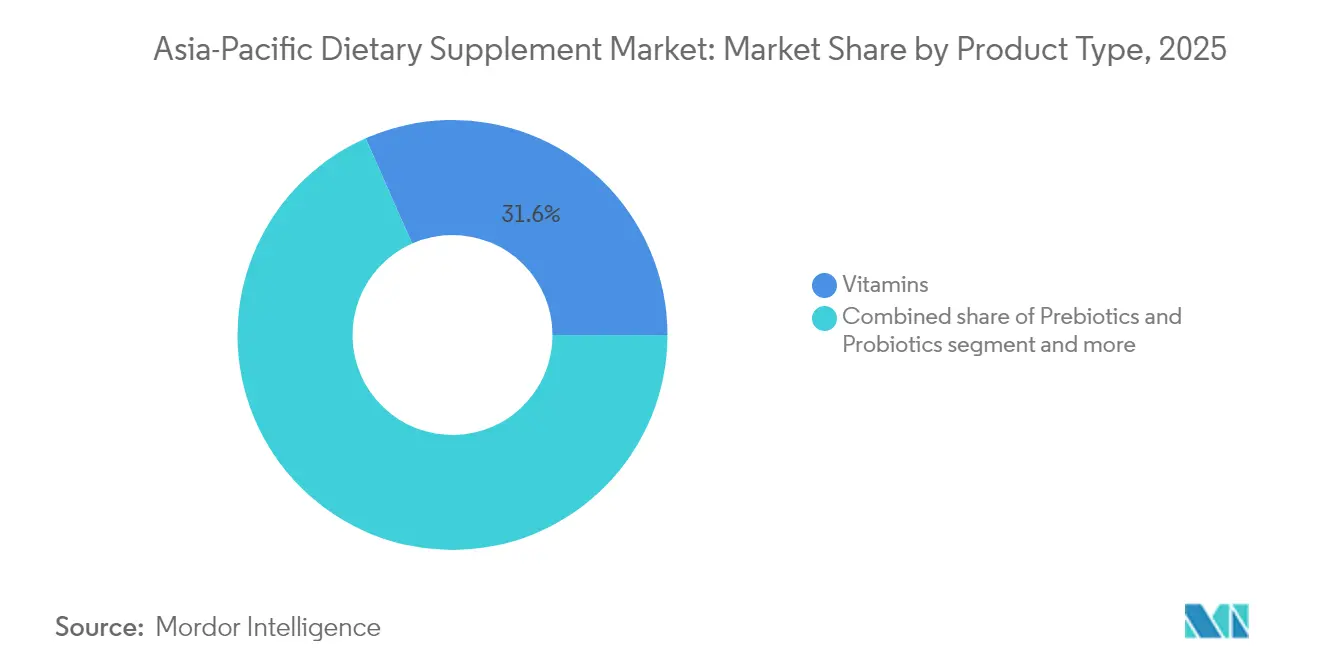

- By product type, vitamins led with 31.62% revenue share in 2025; prebiotics and probiotics are projected to advance at a 6.13% CAGR through 2031.

- By form, tablets dominated with a 44.58% share in 2025, while gummies are set to expand at a 6.21% CAGR to 2031.

- By source, synthetic/fermentation-derived products captured 45.37% of the Asia-Pacific dietary supplements market share in 2025; plant-based lines are expected to grow at a 5.31% CAGR.

- By consumer group, women accounted for 33.46% of sales in 2025, whereas the children’s segment is forecast to post a 6.63% CAGR.

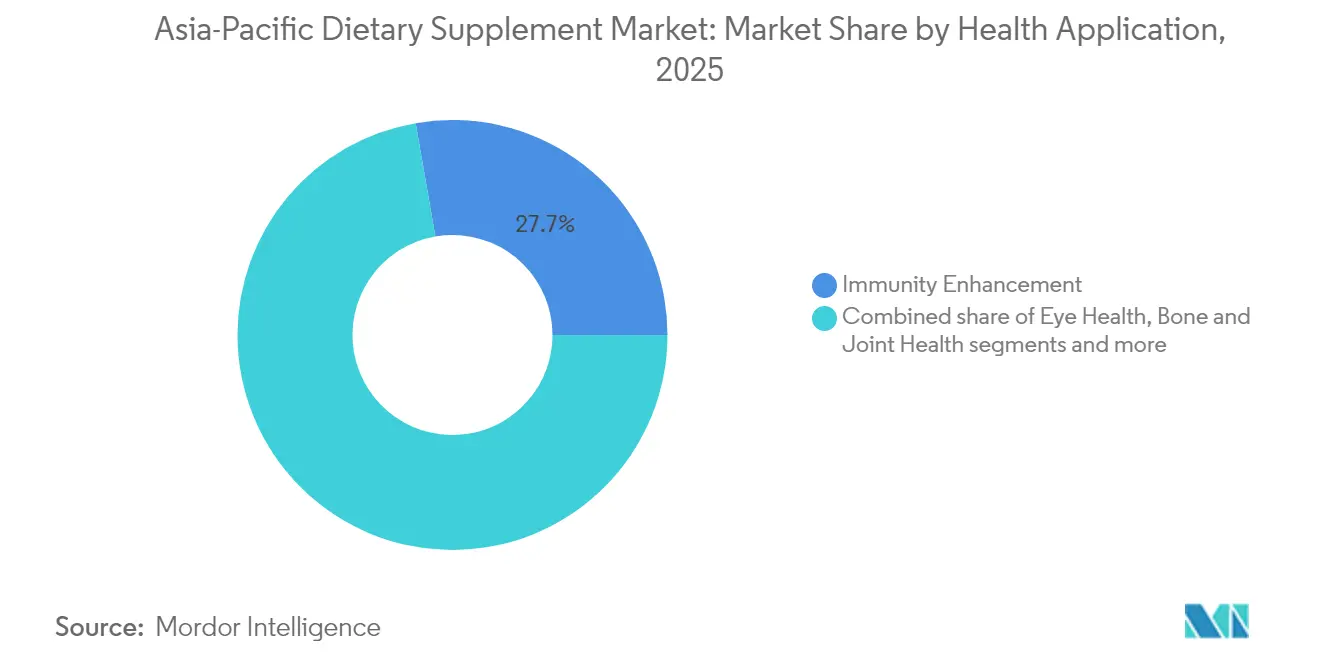

- By application, immunity enhancement products held a 27.74% share in 2025; energy and weight management supplements are positioned for a 4.8% CAGR.

- By distribution channel, specialty stores controlled 39.52% revenue in 2025; online retail is projected to scale at 4.86% CAGR.

- By geography, China contributed 49.02% revenue in 2025; India is on track for a 5.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Dietary Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing expenditure on health and wellness | +1.2% | Global, with highest impact in China, Japan, Australia | Medium term (2-4 years) |

| Rising awareness of preventive healthcare is boosting supplement use | +1.5% | Pan-regional, particularly strong in urban centers | Medium term (2-4 years) |

| Growing preference for clean-label, plant-based and vegan formulas | +0.9% | Australia, Japan, South Korea, urban India | Short term (≤ 2 years) |

| High elderly population in Japan and China fuels age-specific supplements | +1.1% | Japan, China, South Korea | Long term (≥ 4 years) |

| Rise in demand for herbal supplements | +0.8% | India, China, Thailand, with spillover to Southeast Asia | Medium term (2-4 years) |

| E-commerce expansion drives growth in supplement market | +1.0% | China core, rapid expansion in India, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing expenditure on health and wellness

The increasing disposable income in China, Japan, and Australia has driven higher per-capita spending on nutrition products, reflecting heightened health awareness among consumers. Cross-border e-commerce platforms have improved access to premium brands, accelerating this trend. Consumers are transitioning from basic vitamin supplements to specialized formulations that target specific health needs. Retailers in the market have identified that product bundles combining immunity, joint care, and cognitive health supplements often result in significant increases in average basket values. This indicates consumers' willingness to invest in comprehensive health solutions that address multiple concerns simultaneously. In Singapore and South Korea, corporate wellness programs now include dietary supplements in their preventive health allowances. This development signals growing institutional demand for wellness products as organizations recognize the benefits of promoting employee health. These market dynamics support portfolio premiumization across the Asia-Pacific dietary supplements market, contributing to increased revenue for companies operating in this space.

Rising awareness of preventive healthcare is boosting supplement use

Consumers increasingly recognize dietary supplements as essential components of their health strategies. This trend is prominent across Asia-Pacific, where governments in China and Thailand implement educational initiatives and public health programs to promote early health intervention. These programs focus on educating the public about dietary supplement benefits and encouraging healthier lifestyle choices. In Australia, health insurance companies are responding to this trend by offering discount programs for policyholders who regularly use dietary supplements. Insurance providers analyze medical records and purchase histories to reward preventive health practices, encouraging long-term wellness behaviors among their customers. Urban millennials in India, particularly in metropolitan areas, show specific preferences in dietary supplement consumption. Their primary motivations include immune system enhancement, sustained energy levels, and internal beauty benefits. This demographic's health-conscious approach influences their purchasing decisions, particularly favoring supplements that address these specific needs. These combined factors expand the customer base and increase supplement consumption frequency across demographics, driving substantial growth in the Asia-Pacific dietary supplements market.

Growing preference for clean-label, plant-based and vegan formulas

Consumer preferences are shifting toward clean-label and plant-based dietary supplements in the Asia-Pacific region. The demand for products with natural ingredients, transparent sourcing, and minimal processing reflects increasing health consciousness and environmental awareness. This trend is particularly prominent among younger consumers and vegetarians, who actively seek supplements aligned with their lifestyle choices and dietary restrictions. Products with plant-based ingredients demonstrate higher repeat-purchase rates, as consumers value their natural origins, perceived health benefits, and environmental sustainability. This consumer behavior has led manufacturers to incorporate botanical extracts with traceable origins, including ingredients sourced from specific regions or traditional medicinal plants. These formulation changes strengthen consumer trust by providing detailed information about ingredient sources, processing methods, and supply chain transparency. The emphasis on clean-label products and natural formulations has created opportunities for manufacturers to implement premium pricing strategies in the competitive Asia-Pacific dietary supplements market, especially for products featuring unique botanical ingredients and documented sustainability practices.

High elderly population in Japan and China fuels age-specific supplements

The Asia-Pacific region has a growing elderly population, creating significant market opportunities and reshaping consumer preferences in the dietary supplements industry. According to the National Bureau of Statistics of China, approximately 22% of China's population is aged 60 and above as of 2024, representing a substantial and expanding consumer base for targeted nutritional products [1]Source: National Bureau of Statistics of China, "Population distribution in China in 2023 and 2024, by broad age group", stats.gov.cn. This demographic shift has led to increased demand for age-specific supplements targeting bone density, vision care, and mobility, with consumers showing particular interest in preventive healthcare solutions. Products containing collagen peptides or calcium citrate have gained significant traction among older consumers, driving sales growth and product innovation in the nutrition segment. The combination of an aging population, increased health awareness, and growing disposable income creates sustained, long-term demand for dietary supplements in the Asia-Pacific market, establishing a robust foundation for manufacturers and retailers to expand their product portfolios and market presence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality products weaken consumer trust | -0.8% | Pan-regional, particularly severe in India, Thailand, Philippines | Medium term (2-4 years) |

| Lack of standardization in labeling and dosage causes confusion | -0.6% | Most significant in emerging markets (India, Thailand, Vietnam) | Short term (≤ 2 years) |

| Stricter rules tighten grip on dietary supplements and related products | -0.4% | China, Japan, Australia, with spillover effects regionwide | Medium term (2-4 years) |

| Rising consumer scepticism and lack of trust | -0.7% | Regionwise, with highest impact in markets with recent quality scandals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and low-quality products undermine trust

The market impact of counterfeit and adulterated supplements reduces consumer trust, especially in emerging markets. These products often contain incorrect labeling, harmful contaminants, and inaccurate nutritional content declarations. The expansion of unregulated e-commerce platforms has intensified this problem, as these channels often lack robust verification mechanisms and proper quality control measures. Major manufacturers have begun implementing authentication technologies to address these concerns, with companies like Amway deploying blockchain-based traceability systems that enable product verification through smartphone applications. These systems allow consumers to track the supplement's journey from manufacturing to retail, ensuring product authenticity and compliance with quality standards. However, these authentication solutions remain concentrated in premium segments, leaving mass market products susceptible to counterfeiting and adulteration risks.

Lack of standardized labelling and dosage

Regulatory differences across countries necessitate market-specific nutrition labels and warning statements, which increase packaging costs and extend product launch timelines. Companies must comply with diverse regulatory frameworks that require distinct packaging designs and labeling content for each market, including specific font sizes, warning statements, and ingredient declarations. The approval process for new botanical ingredients varies significantly by country, with China taking up to 24 months longer than Indonesia, creating market entry barriers and impacting product development plans. Despite industry associations' efforts to harmonize regulations across ASEAN nations, progress remains slow due to varying national priorities, regulatory approaches, and legislative frameworks. The absence of standardized regulations continues to affect profit margins in the Asia-Pacific dietary supplements market, particularly impacting smaller companies entering the region. These companies must dedicate substantial resources to meet compliance requirements across multiple jurisdictions while managing separate inventory systems, multiple packaging suppliers, and market-specific quality control measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prebiotics and Probiotics Gain Momentum

The vitamins category dominates the Asia-Pacific dietary supplements market with a 31.62% revenue share in 2025, driven by consistent consumer use for essential micronutrient intake. The prebiotics and probiotics segment is projected to grow at a 6.13% CAGR through 2031, exceeding the market's overall growth rate. In Japan, medical professionals regularly recommend synbiotic supplements following antibiotic treatments, increasing pharmacy sales. The perceived connection between gut health and immune function among Southeast Asian consumers supports substantial growth in shelf-stable, spore-based probiotic products.

Research and development in functional probiotic strains continue to expand as companies pursue patents for evidence-based health claims. China's streamlined Blue Hat registration process for specific lactobacillus strains encourages increased domestic fermentation investments. The introduction of postbiotic products that do not require refrigeration expands distribution opportunities through convenience stores. These developments strengthen the Asia-Pacific dietary supplements market through a dynamic microbiome segment that draws both venture funding and industry partnerships.

By Form: Gummies Reshape the Consumption Experience

Tablets dominate the market with a 44.58% share in 2025, driven by their cost-effectiveness and high active ingredient capacity. The Asia-Pacific dietary supplement market demonstrates substantial growth in gummy formulations, with a CAGR of 6.21%. Consumers, specifically younger demographics and urban professionals, select these chewable supplements instead of traditional pills due to their ease of consumption and taste profile. Companies such as Olly and Goli have established operations in India and Southeast Asia with vitamin and probiotic gummies, targeting health-conscious millennials and Generation Z consumers. The improved sensory characteristics of gummies increase consumption compliance, particularly among children and consumers who have difficulty swallowing pills.

Moreover, in the Asia-Pacific dietary supplements market, capsules and softgels remain key delivery formats due to convenience and accurate dosing. Liquid formats demonstrate increased market penetration based on absorption efficiency and consumption advantages. Markets including China, Japan, and India exhibit higher demand for liquid supplements, specifically in the vitamin and herbal extract categories. Manufacturers Swisse and Herbalife have expanded their product portfolios with liquid collagen formulations and herbal tonics to address this market demand for consumable health supplements.

By Source: Plant-Based Inputs Accelerate

In the Asia-Pacific dietary supplement market, synthetic or fermentation-derived ingredients constitute 45.37% of category spending in 2025. These ingredients offer operational efficiency, quality consistency, and production cost advantages for large-scale manufacturing, allowing companies to fulfill the growing demand for vitamins, probiotics, and amino acids at competitive prices. Major multivitamin manufacturers in Japan and South Korea implement fermentation-derived B vitamins and synthetic vitamin C in their standardized formulations. Plant-based alternatives are growing at a 5.31% CAGR, driven by increasing consumer focus on sustainability and animal-free products. Australian retailers have introduced "Plant-Powered" shelf sections to highlight algae-sourced DHA and pea-protein fortified powders. In China, millennial consumers demonstrate a preference for brands that disclose regenerative farming practices for botanical ingredients like ashwagandha.

Moreover, animal-derived ingredients, including collagen, fish oil, and gelatin, maintain sustained demand in the Asia-Pacific dietary supplement market, particularly in beauty, joint health, and omega-3 supplements. Consumers in Japan, South Korea, and China frequently use marine collagen and fish oil capsules for skin health and anti-aging benefits. Companies such as Meiji (Japan) and GNC manufacture marine collagen powders and soft gels to address beauty-from-within consumer preferences.

By Consumer Group: Children’s Health Surges

Women account for 33.46% of the dietary supplements market in 2025, with consistent demand for prenatal vitamins, bone health minerals, and beauty-focused formulations, including collagen and biotin. The children's segment is projected to grow at a 6.63% CAGR through 2031, driven by increased parental spending in China following the end of the one-child policy. Parents are particularly investing in immune support, cognitive development, and growth supplements. Vision health supplements containing lutein and zeaxanthin show strong growth due to increased screen time usage among children and teenagers, with manufacturers creating child-friendly formats such as reading glasses-shaped gummy bears and fruit-flavored chewables.

Regulatory bodies have implemented more stringent safety limits for fat-soluble vitamins in children's supplements, particularly vitamins A, D, E, and K, directing product development toward scientifically validated dosages. In South Korea, the integration of fortified yogurt products enriched with calcium, vitamin D, and probiotics in school meal programs has helped normalize supplement consumption among children. These systematic developments contribute to establishing long-term supplement usage patterns from an early age, significantly expanding the Asia-Pacific dietary supplements market penetration across multiple demographic segments.

By Health Application: Energy and Weight Management Gains Pace

Immunity enhancement products generated 27.74% of revenue in the dietary supplements market across Asia-Pacific in 2025. The COVID-19 pandemic increased consumer interest in preventive healthcare, driving demand for vitamins, minerals, and herbal extracts that support immune function. Companies such as Himalaya and Swisse expanded their immunity-focused product lines, including vitamin C, zinc, and herbal supplements, across India, China, and Southeast Asian markets. Besides, the energy and weight management supplements segment is expected to grow at a CAGR of 4.8%, supported by increased gym memberships and heightened body image consciousness. Products combining green tea catechins with resistant starch address consumer demand for integrated gut health and weight management benefits. Indonesian fitness influencers are promoting caffeine-free pre-workout gummies as alternatives to traditional stimulant-based supplements.

Meanwhile, the demand for bone and joint health supplements, along with gastrointestinal and gut health products, remains substantial in Asia-Pacific's dietary supplement market. The aging population and urban consumers seek supplements that support mobility and digestion. Companies such as Blackmores and Amway provide collagen, calcium, and probiotic supplements to meet the needs of Asia-Pacific consumers focused on maintaining joint flexibility and digestive health.

By Distribution Channel: Online Retail Outpaces All Others

Specialty stores hold a 39.52% revenue share in 2025, driven by knowledgeable staff providing product guidance and package promotions for complementary supplements. The online retail segment projects a 4.86% CAGR, benefiting from China's same-day delivery infrastructure and India's expanding rural internet connectivity through fiber-optic networks. According to the Ministry of Communications, India recorded 954.40 million total Internet subscribers as of March 2024, with 398.35 million subscribers in rural regions. The BharatNet project aims to deliver broadband infrastructure to rural households through Optical Fibre Cable (OFC) connectivity across all Gram Panchayats (GPs). Of the 222,000 Gram Panchayats planned under the two phases of BharatNet, 213,000 are now operational. The Amended BharatNet Program intends to implement Optical Fibre connectivity to 42,000 unserved GPs and 384,000 villages based on demand, while targeting 15 million rural home fibre connections . Also, Douyin's livestreaming capabilities facilitate instant purchases during interactive sessions where hosts demonstrate products and address customer inquiries, while Key Opinion Leaders provide product validation through testimonials and usage experiences.

Cross-border e-commerce platforms provide access to premium imported products without local registration requirements, enabling direct purchases of international brands. Subscription services strengthen customer retention through automated monthly deliveries with personalized nutritional guidance and lifestyle content. Direct selling companies operate hybrid models where distributors create online communities to maintain customer relationships through virtual consultations and group discussions. These digital advancements reshape distribution channels in the Asia-Pacific dietary supplements market, improving consumer engagement and product accessibility.

Geography Analysis

China accounts for 49.02% of regional turnover in 2025, establishing its dominant position in the Asia-Pacific dietary supplements market. The market shows increasing segmentation, with younger consumers seeking specialized products like joint-protective peptides for esports users. India demonstrates the highest growth rate at 5.27% CAGR, driven by increasing disposable incomes and expanding pharmacy networks. The Food Safety and Standards Authority's simplified regulations facilitate faster market entry for herbal products, establishing India as an emerging force in the regional market.

Japan maintains steady growth, supported by an aging population focused on healthy aging. In Japan, individuals aged 65 and older account for 36.25 million people, representing 29.3% of the total population, as reported by the Ministry of Internal Affairs and Communications . Products with cognitive, mobility, and skin elasticity benefits show strong demand, while the Food with Function Claims system enhances product credibility. Digital adoption through app-based dosage management improves consumer compliance. Moreover, South Korea maintains significant market influence from beauty supplements. The Ministry of Food and Drug Safety's strict quality requirements maintain market integrity. Korean companies utilize their beauty industry reputation to expand collagen product distribution across ASEAN markets. Australia demonstrates market maturity through robust regulatory compliance and informed consumers. The Therapeutic Goods Administration's Listed Medicine framework builds consumer trust, supported by pharmacies serving dual roles as retailers and educational resources. Southeast Asian markets, particularly Thailand and Vietnam, present growth opportunities due to expanding middle-class populations. Regional manufacturers adapt products to local preferences, such as kalamansi-flavored vitamin C supplements, to strengthen market presence.

Competitive Landscape

The Asia-Pacific dietary supplements market demonstrated moderate fragmentation, with a mix of global companies, regional specialists, and emerging digital brands operating in the region. Major companies in the region are dominating the premium dietary supplement market through branded products that emphasize quality, research validation, and health benefits. This market structure generates a diverse competitive environment across the Asia-Pacific region, integrating regional expertise with international product development. Some of the major players in the market include Abbott Laboratories, Herbalife Nutrition Ltd., Amway Corporation, and Haleon Plc.

Product development speed has become a key competitive factor. Innovation cycles have been reduced to 12-18 months as companies utilize contract manufacturers with versatile production capabilities for gummies, powders, and liquid shots. Companies are increasing their research and development investments, with major players allocating revenue for clinical studies. Companies form joint ventures to navigate regional regulations, as demonstrated by Otsuka's partnerships with Chinese e-pharmacies to secure Blue Hat approvals for brain-health beverages.

Pharmaceutical companies entering the market use their established safety monitoring systems to highlight their drug development expertise. Food manufacturers utilize their flavor development capabilities to enhance their chewable supplements. These dynamics create an evolving market environment where partnerships and acquisitions continue to influence market share distribution in the Asia-Pacific dietary supplements market.

Asia-Pacific Dietary Supplement Industry Leaders

-

Abbott Laboratories

-

Herbalife Nutrition Ltd.

-

Amway Corporation

-

Bayer AG

-

Haleon Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Akesis Biologics, a biotechnology company that originated from the National University of Singapore (NUS), introduced MastGut, its first gut health supplement designed to provide therapeutic protection for the digestive system.

- April 2025: Biome Australia Limited expanded its Activated Probiotics range with two new women's health products. The company launched Biome Her Pessary, a vaginal probiotic containing Lactobacillus acidophilus LA02 and Lactobacillus fermentum LF10 strains, which demonstrated effectiveness in reducing vaginal thrush recurrence.

- September 2024: Bene Esse developed four plant-based supplements for digestive health. The products specifically addressed gas and bloating, liver health, irritable bowel syndrome (IBS), and constipation. The company formulated these products based on scientific research and clinical evidence.

Asia-Pacific Dietary Supplement Market Report Scope

Dietary supplements are mainly consumed to enhance the intake of essential nutritional components in the human body.

The market report of dietary supplements is segmented by type into vitamins, minerals, proteins and amino acids, herbal supplements, fatty acids, probiotics, and other types. by distribution channel. The market is segmented into supermarkets/hypermarkets, pharmacies and drug stores, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into China, Japan, India, Australia, and the Rest of Asia-Pacific.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Vitamins |

| Minerals |

| Fatty Acids |

| Protein and Amino Acids |

| Prebiotic and Probiotic Supplements |

| Herbal Supplements |

| Enzymes |

| Blended Supplements |

| Others |

By Form

| Tablets |

| Capsules and Softgels |

| Powders |

| Gummies |

| Liquids |

| Others |

By Source

| Plant-based |

| Animal-based |

| Synthetic/Fermentation-derived |

By Consumer Group

| Mens |

| Womens |

| Kids/Childrens |

By Health Application

| General Health and Wellness |

| Bone and Joint Health |

| Energy and Weight Management |

| Gastrointestinal and Gut Health |

| Immunity Enhancement |

| Cardiovascular Health |

| Diabetes Management |

| Cognitive and Mental Health |

| Skin, Hair and Nail Care |

| Eye Health |

| Other Health Applications |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Channels |

| Direct Selling |

| Other Distribution Channels |

By Geography

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Indonesia |

| Singapore |

| Thailand |

| Rest of Asia-Pacific |

| By Product Type | Vitamins |

| Minerals | |

| Fatty Acids | |

| Protein and Amino Acids | |

| Prebiotic and Probiotic Supplements | |

| Herbal Supplements | |

| Enzymes | |

| Blended Supplements | |

| Others | |

| By Form | Tablets |

| Capsules and Softgels | |

| Powders | |

| Gummies | |

| Liquids | |

| Others | |

| By Source | Plant-based |

| Animal-based | |

| Synthetic/Fermentation-derived | |

| By Consumer Group | Mens |

| Womens | |

| Kids/Childrens | |

| By Health Application | General Health and Wellness |

| Bone and Joint Health | |

| Energy and Weight Management | |

| Gastrointestinal and Gut Health | |

| Immunity Enhancement | |

| Cardiovascular Health | |

| Diabetes Management | |

| Cognitive and Mental Health | |

| Skin, Hair and Nail Care | |

| Eye Health | |

| Other Health Applications | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Channels | |

| Direct Selling | |

| Other Distribution Channels | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Singapore | |

| Thailand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific dietary supplements market?

The market is worth USD 74.98 billion in 2026 and is set to grow to USD 91.35 billion by 2031 at a 4.05% CAGR.

Which country holds the largest share of the Asia-Pacific dietary supplements market?

China leads with 49.02% of regional revenue in 2025.

Which segment is expanding fastest by product type?

Prebiotics and probiotics are forecast to grow at an 6.13% CAGR, the highest among all product types.

How quickly is the online channel growing?

Online retail sales of supplements are expected to increase at a 4.86% CAGR, outpacing every other distribution channel.

Page last updated on: