Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.14 Billion |

| Market Size (2026) | USD 20.04 Billion |

| Market Size (2031) | USD 25.24 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia Pacific Chocolate Market Analysis by Mordor Intelligence

The Asia Pacific chocolate market size is expected to grow from USD 19.14 billion in 2025 to USD 20.04 billion in 2026 and is forecast to reach USD 25.24 billion by 2031 at 4.72% CAGR over 2026-2031. This growth is attributed to increasing disposable incomes, rapid urbanization, and a growing preference for premium Western-style confections. China, India, and major cities in Southeast Asia are leading this trend, with younger consumers favoring products that highlight unique flavors, origin, and health benefits. The expansion of modern retail and e-commerce has enhanced chocolate accessibility, particularly in Tier 2 and Tier 3 cities, driving sales growth. Demand for artisanal, organic, and health-oriented chocolates is rising, especially in Japan, South Korea, and Australia, fueled by flavor innovations. Festivals such as Lunar New Year, Diwali, and Christmas boost seasonal demand, as chocolates are popular gift choices. To capitalize on this growing market, cocoa suppliers are increasing investments in integrated sourcing, digital commerce, and cold-chain logistics, focusing on secondary and tertiary cities. However, challenges such as cocoa price volatility and evolving sugar-tax policies create cost pressures, favoring agile brands with strong procurement and reformulation capabilities.

Key Report Takeaways

- By product type, white and milk variants together held 60.83% of the Asia Pacific chocolate market share in 2025, while dark chocolate recorded the fastest 6.55% CAGR through 2031.

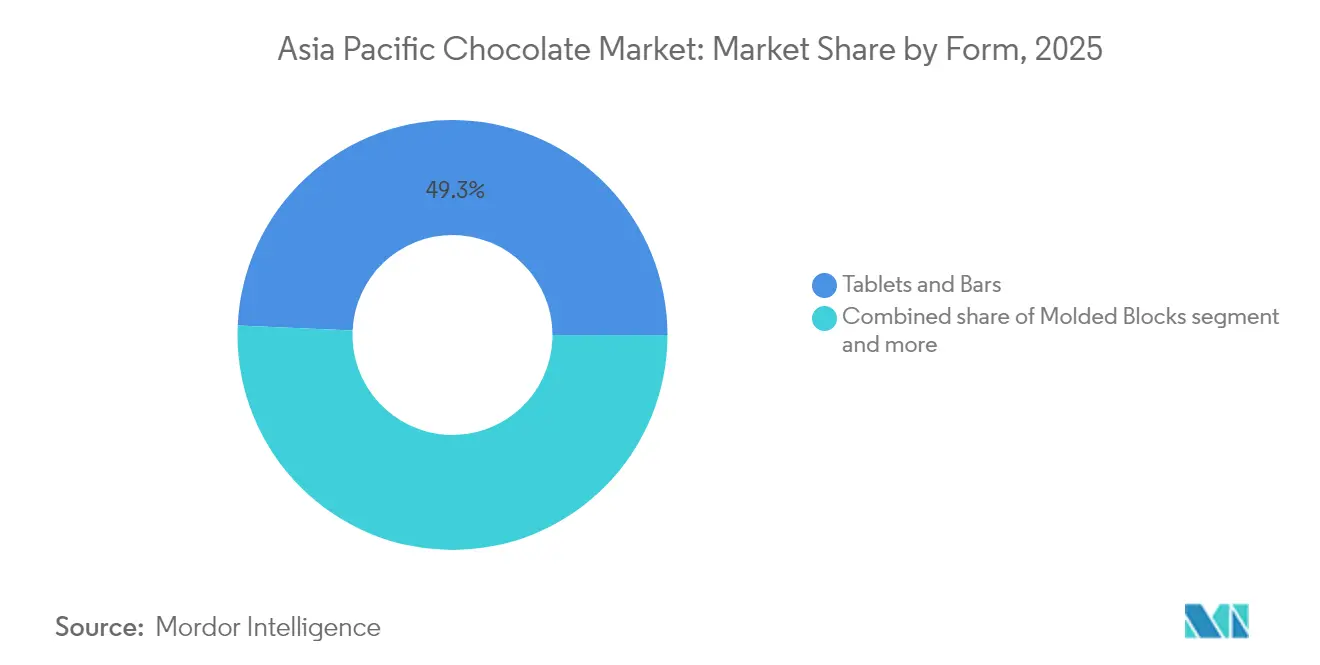

- By form, the tablets and bar segment accounted for 49.30% of the Asia Pacific chocolate market size in 2025, and molded blocks are projected to grow at a 5.55% CAGR between 2026-2031.

- By price range, the mass segment accounted for 74.35% of the Asia Pacific chocolate market size in 2025, and the premium projected to grow at a 5.74% CAGR between 2026-2031.

- By distribution channel, convenience stores captured 38.40% revenue share in 2025, whereas online retail is advancing at a 5.38% CAGR through 2031.

- By geography, China led with 31.05% Asia Pacific chocolate market share in 2025; Malaysia is forecast to expand at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for dark chocolate's health halo | +1.2% | Global, strongest in Japan, Singapore, Australia | Medium term (2-4 years) |

| Product innovation targeting Gen-Z and millennials | +0.9% | Urban centers across China, India, Southeast Asia | Short term (≤ 2 years) |

| Adoption of single-origin SE-Asian cocoa by bean-to-bar brands | +0.6% | Malaysia, Indonesia, Thailand, premium segments globally | Long term (≥ 4 years) |

| Urbanization and Changing Lifestyles | +1.1% | China, India, Vietnam, Indonesia secondary cities | Medium term (2-4 years) |

| Western Lifestyle Influence and Increasing Chocolate Awareness | +0.8% | Tier-2 cities in China and India, ASEAN urban areas | Medium term (2-4 years) |

| Sustainability-driven demand for certified cocoa/chocolate | +0.4% | Japan, Australia, Singapore, export-oriented production | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing preference for dark chocolate's health halo

Dark chocolate, recognized as a functional food, is experiencing a 6.87% CAGR, surpassing the growth of the traditional milk chocolate segment, particularly among health-conscious consumers. Urbanization significantly influences this trend, as a large share of food consumption occurs in cities, driving demand for processed foods with perceived health benefits. With the rising prevalence of lifestyle diseases such as obesity, diabetes, and cardiovascular conditions, consumers are increasingly opting for snacks that combine indulgence with health advantages. For example, in 2023, the Organisation for Economic Co-operation and Development (OECD) reported that 4.9% of adults in South Korea are obese[1]Source: Organisation for Economic Co-operation and Development (OECD), "Obesity Rates Around the World", oecd.org. In emerging markets like India and China, the rapid adoption of healthier eating habits and increasing disposable incomes have further boosted dark chocolate consumption. Manufacturers are leveraging this trend by promoting antioxidant properties and emphasizing cacao content. At the same time, regulatory authorities are intensifying scrutiny of health claims to ensure compliance with food safety standards. Despite a twofold increase in cocoa prices, dark chocolate producers have maintained profit margins through premium positioning. This 'health halo' effect is particularly strong in developed Asia Pacific markets, where consumers are willing to pay more for products with perceived health benefits.

Product innovation targeting gen-z and millennials

Gen-Z consumers are driving the adoption of social commerce in the Asia Pacific, significantly transforming chocolate product development and marketing strategies. Thai chocolate producers, supported by the Thai Trade Association of Cacao and Chocolate's industry development initiatives, are leading this trend with localized flavor innovations such as fish-sauce caramel bars and tom yum-infused products. Both Gen Z and Millennials are drawn to unique and adventurous flavors like matcha, yuzu, chili, salted caramel, and fruit-infused chocolates. Limited edition and capsule collections generate social media buzz, increasing engagement and sales. Formats such as bite-sized pieces, snack bars, and bespoke gift boxes appeal to consumers seeking convenience and shareability. Digital-native brands are utilizing omnichannel strategies, integrating social media and experiential marketing to effectively reach younger demographics. This trend is further supported by the growing Gen Z population in the region. For example, in 2024, 13.7% of Australia's population was aged 20-29, according to the Australian Bureau of Statistics[2]Source: Australian Bureau of Statistics, "Population distribution in Australia", abs.gov.au. Manufacturers are accelerating innovation cycles to meet generational demands for authenticity, sustainability messaging, and visually appealing packaging designs. This demographic shift creates opportunities for smaller players to disrupt established market leaders through targeted product development and direct-to-consumer approaches.

Urbanization and changing lifestyles

Urban areas are consuming an increasing share of global food production. In the Asia Pacific, urbanization is driving greater demand for convenient, packaged chocolate products that cater to fast-paced lifestyles. The World Bank reported a 3.9% GDP growth for East Asia and the Pacific in 2024[3]Source: World Bank, "GDP Growth", worldbank.org, enhancing urban consumer spending power. Simultaneously, domestic consumption is shifting towards processed foods and dining out. The growth of supermarkets and convenience stores is improving chocolate accessibility, particularly in secondary cities where modern retail formats are gradually replacing traditional markets. Urban diets are increasingly incorporating ultra-processed foods, with chocolate benefiting from its dual role as a treat and a quick energy source for busy professionals. Additionally, infrastructure advancements in urban centers are strengthening cold-chain logistics, essential for distributing premium chocolate. This reduces spoilage and supports innovations in temperature-sensitive products. The urbanization trend is also driving demand for portion-controlled and on-the-go packaging formats, which align with commuter consumption habits.

Western lifestyle influence and increasing chocolate awareness

Western lifestyle adoption accelerates chocolate consumption in emerging Asia Pacific markets, supported by overseas tourist arrivals in China reached 131.9 million visitors to China alone during 2024, according to the National Bureau of Statistics of China[4]Source: National Bureau of Statistics of China, "Overseas visitor arrivals in China", stat.gov.cn. Cultural exchange through tourism and media exposure normalizes chocolate consumption beyond traditional gift-giving occasions, expanding daily consumption patterns. Urban areas are experiencing a rise in international food chains and Western-style cafes, introducing chocolate-based beverages and desserts to local consumers. Multinational manufacturers are driving awareness through educational initiatives and marketing campaigns, integrating chocolate into celebrations and personal indulgence rituals. The growing coffee culture highlights chocolate's role in enhancing espresso drinks, creating opportunities for cross-category consumption. Additionally, digital media and social platforms are reinforcing these Western lifestyle aspirations, establishing chocolate as a symbol of modernization and global connectivity for the expanding middle class.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cocoa price volatility | -0.8% | Global supply chains, manufacturing cost centers | Short term (≤ 2 years) |

| Sugar-tax regulations and health concerns over sugar | -0.5% | Malaysia, Thailand, Pacific Islands, India | Medium term (2-4 years) |

| Limited cold-chain in Tier-3 and rural Asia-Pacific | -0.3% | Rural Indonesia, India, Philippines, Vietnam | Long term (≥ 4 years) |

| Shelf-space pressure from indigenous sweets | -0.2% | Traditional retail channels, cultural preference areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cocoa price volatility

In 2024, cocoa futures exhibited extreme volatility. Prices surged from approximately USD 2,750 per tonne to a peak of over USD 10,000 in March, before stabilizing at around USD 8,800. This sharp increase forced manufacturers to promptly adjust prices and reformulate products. In response to the price hike, Japanese manufacturers, including major players like Nestlé and Morinaga, raised prices on chocolate confections. KitKat, in particular, implemented both price increases and package size reductions to maintain market accessibility. West Africa, a critical region for global cocoa production, is facing supply disruptions in 2024. Adverse weather and political instability have resulted in structural supply deficits, leading to an expected decline in global cocoa output. Small-scale confectioners, with their limited purchasing power, are disproportionately affected. For example, Singapore-based artisan producers like Embrace Chocolate are now paying double for raw cocoa beans compared to early 2024 prices. To navigate these challenges, many are turning to alternative ingredients, adopting shrinkflation strategies, and diversifying supply chains to regions such as Indonesia and other parts of the Asia Pacific. However, a significant challenge remains: new cocoa trees require 3-4 years to mature and begin production.

Sugar-tax regulations and health concerns over sugar

Jurisdictions across the Asia Pacific are expanding sugar taxation frameworks. Malaysia has introduced an excise tax of MYR 0.47 per 100g on chocolate premixes, while Thailand's tiered excise structures are altering confectionery pricing. Pacific Island nations have implemented high import duties on chocolate products as part of their strategies to prevent non-communicable diseases. The region is also experiencing growing adoption of front-of-package labeling initiatives. However, regulatory compliance demands significant investments in product development and labeling systems, particularly for export-oriented manufacturers operating across jurisdictions with varying standards. Health concerns are driving market segmentation opportunities for reduced-sugar and sugar-free alternatives, though consumer acceptance remains low in traditional chocolate categories. To address evolving regulatory requirements while preserving taste profiles, manufacturers are increasingly focusing on natural sweeteners and portion control strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains Health-Conscious Momentum

Dark chocolate is projected to grow at a CAGR of 6.55% through 2031, driven by shifts in consumer behavior towards its perceived health benefits and premium positioning. Manufacturers, highlighting antioxidant content and cacao percentages, position dark chocolate as a functional food, justifying its premium pricing even amidst fluctuating cocoa costs. In 2025, white and milk chocolates command a dominant 60.83% market share. Their widespread appeal, rooted in familiar taste profiles and competitive pricing, is especially pronounced in emerging markets where chocolate consumption is still evolving. Milk chocolate's creamy texture, enhanced by dairy integration, resonates with traditional Asian tastes, while white chocolate finds its niche in confectionery and baking.

Thai chocolate producers are pushing boundaries in the dark chocolate realm, infusing local flavors like fish-sauce caramel and tom yum, crafting premium products that resonate culturally. In developed Asia Pacific markets, the 'health halo' effect is pronounced, with urban consumers, increasingly health-conscious, willing to pay a premium for perceived functional benefits. This trend is bolstered by urbanization, concentrating these demographics in major cities. However, as health claims come under heightened scrutiny from regulatory bodies, manufacturers are now mandated to back their antioxidant and wellness assertions with clinical evidence and thorough compliance documentation.

By Form: Tablets and Bars Lead Despite Molded Innovation

Tablets and bars that command 49.30% market share in 2025, driven by portion control preferences and premium positioning strategies. This segment benefits from strong consumer familiarity and efficient manufacturing processes, enabling extensive distribution across various retail channels. Pralines and truffles cater to premium gifting occasions and maintain stable demand in developed markets, while other chocolate forms serve specialized purposes, such as baking ingredients and industrial food services.

Molded blocks are projected to grow at a 5.55% CAGR through 2031. Innovations in molded blocks address the needs of health-conscious consumers, with manufacturers designing specialized shapes and textures that yield higher margins compared to traditional bars. The Malaysian Cocoa Board's Bagan Datuk Single Origin chocolate initiative highlights government support for value-added processing, emphasizing traceability to specific plots and unique drying techniques. Diversification in forms enables manufacturers to differentiate products beyond flavor profiles, enhancing premium positioning and profitability. Additionally, the flexibility of molded formats supports limited edition launches and seasonal variations, encouraging consumer trials and strengthening brand engagement.

By Price Range: Premium Segment Accelerates Despite Mass Market Scale

Mass market products hold a 74.35% share in 2025, highlighting rising incomes and increasing consumer sophistication in urban centers across Asia Pacific. The mass market segment benefits from well-established distribution networks and affordable pricing, driving volume growth in emerging economies where chocolate consumption is still maturing. On the other hand, the premium chocolate sector is expected to grow at a 5.74% CAGR through 2031. This premium positioning helps manufacturers manage volatile cocoa costs with higher margins, while mass market players focus on operational efficiency and economies of scale to sustain profitability.

Cross-border e-commerce platforms are expanding access to premium chocolates. The premium segment gains momentum from the recovery in tourism, showcasing growth that surpasses pre-pandemic levels. Artisanal and bean-to-bar producers cater to the premium market by emphasizing single-origin offerings and sustainability, although their limited scale restricts penetration into the mass market. By segmenting price ranges, brands can develop portfolio strategies that effectively capture both volume and margin opportunities across diverse consumer groups.

By Distribution Channel: Online Retail Disrupts Convenience Store Leadership

Convenience stores secured a 38.40% market share in 2025, driven by the expansion of cross-border e-commerce and the preferences of digital-native consumers. These stores capitalize on their extensive presence to promote impulse purchases, particularly in urban areas where high foot traffic and commuter patterns drive frequent chocolate sales. Supermarkets and hypermarkets deliver a broad product range and promotional opportunities, while specialty and gourmet stores target premium customers with curated offerings and distinctive retail experiences.

Online retail channels are expected to grow at a CAGR of 5.38% through 2031. These platforms establish direct connections with consumers, often utilizing subscription models that bypass traditional retail margins. They also leverage consumer data to drive product innovation. While advancements in temperature-controlled logistics support the online sale of premium chocolates, the absence of cold-chain infrastructure in rural areas limits market growth. This shift in retail channels aligns with broader trends, highlighting the importance of omnichannel strategies to engage a diverse consumer base.

Geography Analysis

China holds a significant 31.05% market share in 2025, driven by its large population and rapid urbanization. Foreign brands dominate the Chinese market, with Mars leading in market share. Ferrero's presence highlights a trend of consolidation among international players. Mondelez's acquisition of a majority stake in Evirth in November 2024 reflects continued confidence in foreign investments, particularly in the untapped frozen baked goods category. Government policies promoting domestic consumption and urbanization provide structural support for the chocolate market's growth. However, traditional confectionery preferences and price sensitivity among emerging consumers remain key challenges.

Japan's market is mature, characterized by sophisticated consumer preferences and established distribution networks. E-commerce is the only distribution channel experiencing growth, driven by increasing digital adoption and direct-to-consumer strategies that bypass traditional retail margins. Inbound tourism also contributes to market growth. In 2024, Japan's confectionery exports reached record levels in both quantity and value, supported by a depreciating yen and global demand for Japanese flavors such as matcha and yuzu.

Malaysia is the fastest-growing market, with a projected CAGR of 6.05% through 2031. This growth is fueled by government initiatives that support local cocoa production and downstream processing, creating integrated value chains. The Malaysian Cocoa Board's efforts to secure commercial partners for Bagan Datuk Single Origin chocolate demonstrate institutional support for premium product development and traceability systems. The region has significant supply capacity for refined fats and sugars used in confectionery manufacturing, with EUDR-compliant production and traceability platforms that help manufacturers mitigate regulatory compliance risks. While countries like Indonesia, Thailand, and Singapore, along with other Southeast Asian markets, benefit from economic development and urbanization, rural infrastructure challenges limit their distribution capabilities. Developed markets such as Australia and New Zealand focus on premium positioning, whereas smaller Pacific Island nations face import dependency and infrastructure constraints, hindering market growth.

Competitive Landscape

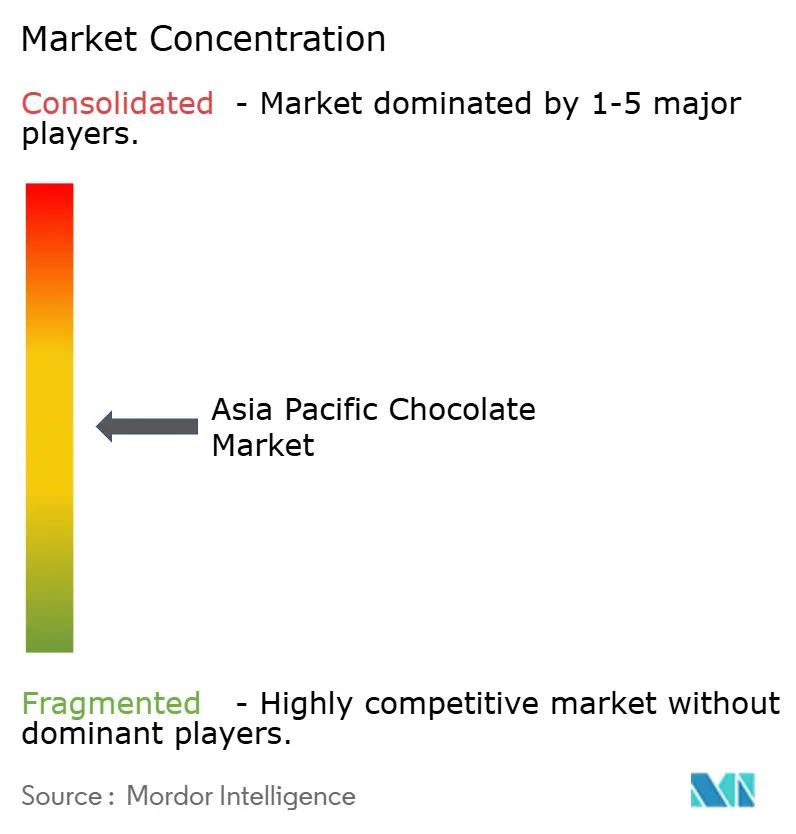

The Asia Pacific chocolate market is moderately concentrated, with established multinationals competing against emerging regional players and artisanal bean-to-bar producers across various price points and distribution channels. Strategic consolidation is accelerating through acquisitions, such as Nestlé's planned completion of Hsu Fu Chi's purchase in April 2025 and Mondelez's acquisition of a majority stake in Evirth, highlighting ongoing foreign investment in local manufacturing capabilities and distribution networks. Companies are adopting technology to enhance supply chain traceability and ensure compliance with sustainability standards. For instance, FGV Holdings has implemented digital platforms for supplier risk screening and deforestation monitoring to meet EUDR requirements. Cross-border e-commerce platforms are enabling smaller players to enter international markets, while subscription services are fostering direct-to-consumer relationships, bypassing traditional retail margins and providing valuable consumer data insights for product development.

Major multinational corporations lead the Asia Pacific chocolate market, employing strategic initiatives to maintain their competitive positions. Product innovation remains a priority, with companies consistently introducing new flavors, healthier variants, and premium offerings to meet evolving consumer preferences. These corporations demonstrate operational agility by building robust distribution networks and adopting omnichannel strategies to expand their market reach. Investments in research and development facilities are increasingly focused on key markets such as China, Japan, and India to accelerate innovation and shorten product development cycles. Strategic partnerships with local players, e-commerce platforms, and retail chains are becoming essential for market penetration and growth. Expanding manufacturing facilities in emerging markets, along with sustainability initiatives in sourcing and production, underscores the industry's commitment to long-term growth and environmental responsibility. Leading players in the market include Chocoladefabriken Lindt and Sprüngli AG, Ferrero International S.p.A., Mars Incorporated, Mondelēz International Inc., and Nestle SA.

Premium single-origin positioning and health-conscious formulations are emerging as white-space opportunities, particularly as cocoa price volatility pressures margins for mass-market players while creating opportunities for specialized producers. Orion Holdings has achieved regional expansion success, generating over KRW 200 billion in operating profit from its China operations, with dividend repatriation strategies supporting facility expansions and mergers and acquisitions. Regulatory compliance frameworks are increasingly shaping competitive dynamics, with RSPO certification, MSPO standards, and sustainability reporting becoming prerequisites for market access rather than differentiation. The competitive landscape favors companies that effectively navigate supply chain sustainability requirements while maintaining cost competitiveness amid fluctuating commodity prices and evolving consumer preferences for transparency and health-conscious products.

Asia Pacific Chocolate Industry Leaders

-

Mars Incorporated

-

Mondelēz International Inc.

-

Nestlé SA

-

Chocoladefabriken Lindt and Sprüngli AG

-

Ferrero International S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Cadbury Dairy Milk has introduced 'Milkinis', a milk crème-filled chocolate, as part of its strategic expansion into India's agribusiness market, supported by a comprehensive marketing campaign.

- July 2025: Campco rolled out three new chocolate products at its headquarters in Mangaluru, India: Dark Delight dark chocolate, Dome Delight premium truffles, and Campco's orange eclairs.

- April 2025: Nestlé has fully acquired the Chinese confectionery firm Hsu Fu Chi, taking ownership from the Hsu family. This strategic acquisition not only weaves Hsu Fu Chi into Nestlé's expansive vision for China but also harnesses Nestlé's vast distribution channels to bolster its snacking and confectionery ventures in the region.

- August 2024: Mondelez India introduced its Cadbury Silk desserts range through a new campaign. The campaign features a couple savoring the Cadbury Silk Desserts, emphasizing the brand's latest offerings.

Asia Pacific Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel. Australia, China, India, Indonesia, Japan, Malaysia, New Zealand, South Korea are covered as segments by Country.

By Product Type

| Dark Chcolate |

| White and Milk Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Specialty and Gourmet Stores |

| Online Retail Channels |

| Other Distribution Channels |

By Country

| China |

| Japan |

| India |

| Thailand |

| Singapore |

| Malaysia |

| Indonesia |

| South Korea |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Dark Chcolate |

| White and Milk Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialty and Gourmet Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| By Country | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Malaysia | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms