Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

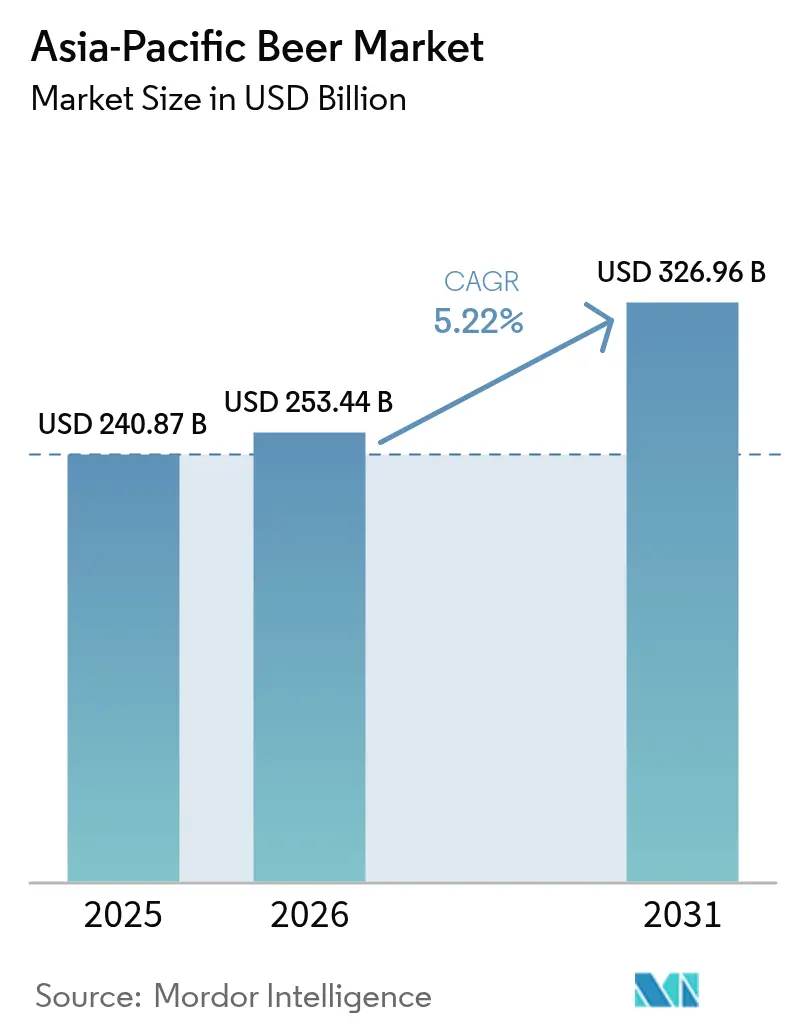

| Base Year Market Size (2025) | USD 240.87 Billion |

| Market Size (2026) | USD 253.44 Billion |

| Market Size (2031) | USD 326.96 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Beer Market Analysis by Mordor Intelligence

The Asia-Pacific beer market size is expected to grow from USD 240.9 billion in 2025 to USD 253.44 billion in 2026 and is forecast to reach USD 326.86 billion by 2031 at a 5.22% CAGR over 2026-2031. Brewers are now prioritizing premiumization, non-alcoholic launches, and margin-focused channel strategies over sheer volume. This shift is evident as Anheuser-Busch InBev reports a 4.8% increase in revenue per hectoliter in China, even with an 8.6% drop in volume. In countries like India, Vietnam, and Indonesia, rising middle-class incomes are driving a trade-up behavior, boosting demand for premium segments. Additionally, sustainability mandates favoring aluminum cans, a rebound in tourism enhancing on-trade sales, and AI-driven supply-chain efficiencies are creating a wider gap between industry innovators and laggards. Meanwhile, regulatory changes, such as liquor-tax harmonization in Japan and surging special-consumption taxes in Vietnam, are reshaping pricing dynamics and portfolio strategies. Companies that adapt quickly to these evolving trends are likely to gain a competitive edge in the market.

Key Report Takeaways

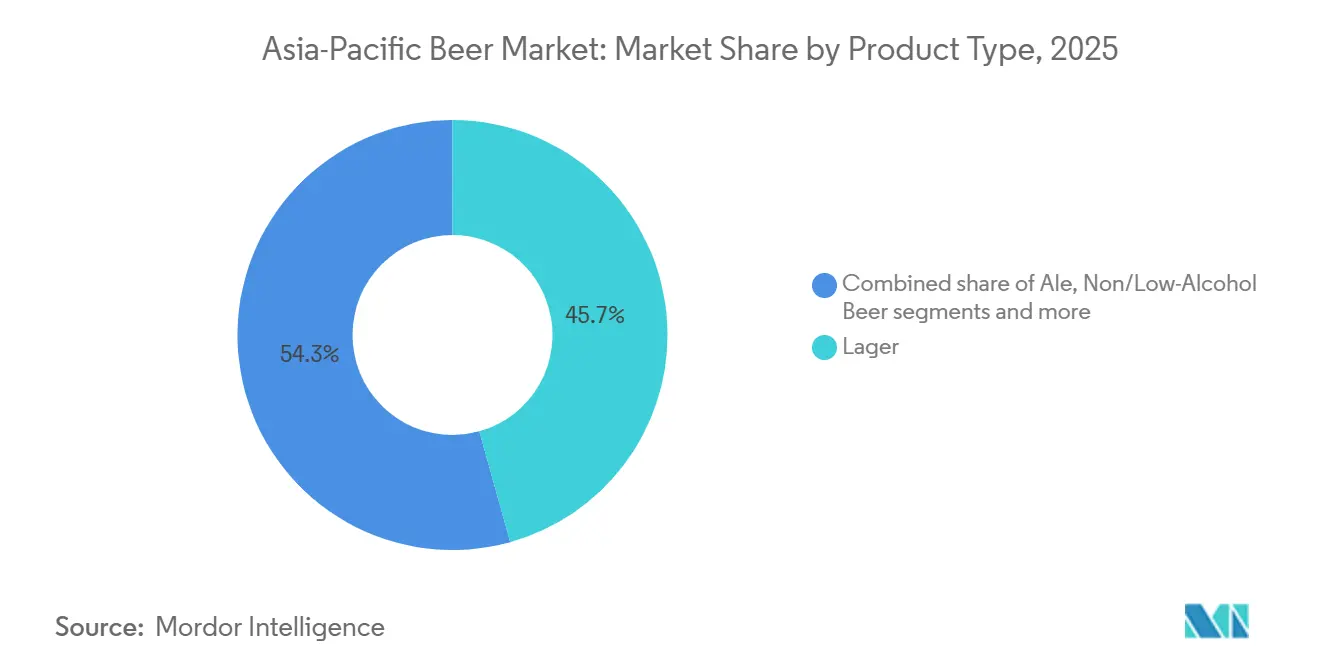

- By product type, lager led with a 45.68% share in 2025 while non- and low-alcohol variants are projected to advance at a 7.92% CAGR through 2031, making them the fastest growing category in the Asia-Pacific beer market.

- By category, standard beer accounted for 65.05% of revenue in 2025, and premium offerings are poised to grow at a 7.18% CAGR during 2026-2031, supported by rising disposable incomes in urban India and Vietnam.

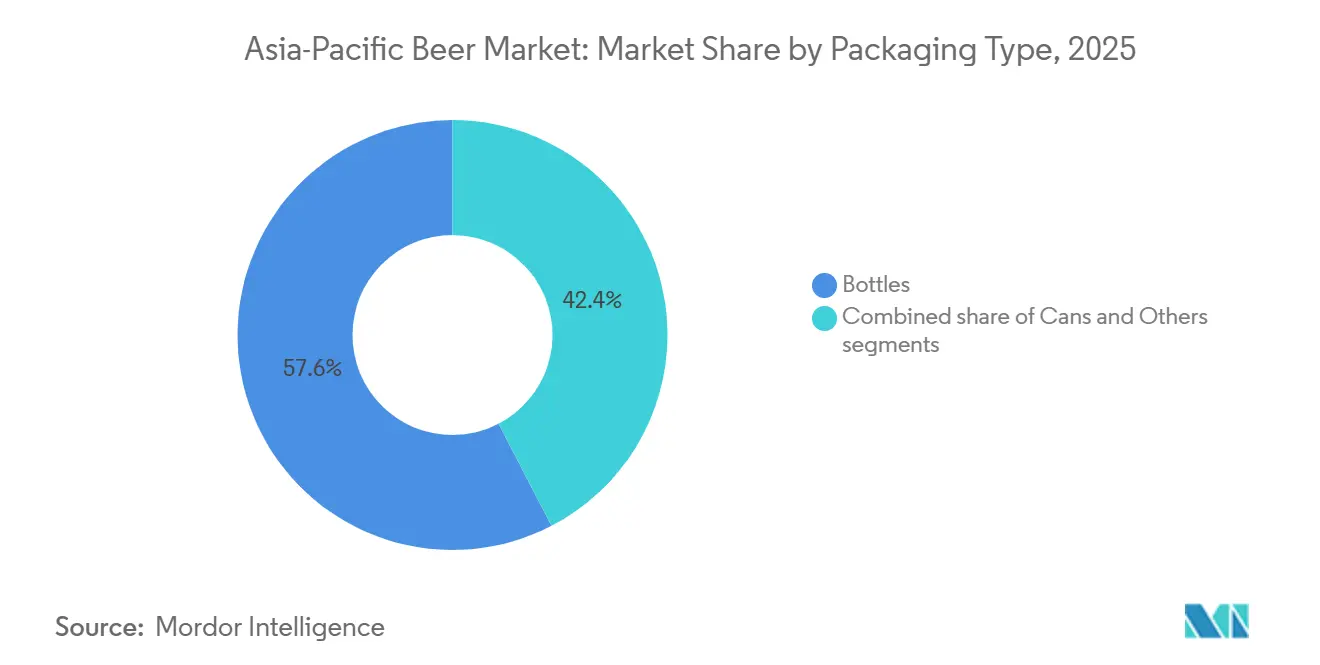

- By packaging type, bottles held 57.62% share in 2025, whereas cans are on track for a 6.04% CAGR to 2031 as aluminum’s 50% lower carbon footprint aligns with emerging EPR rules in China, India, and Vietnam.

- By distribution channel, off-trade captured 61.70% of sales in 2025, yet on-trade venues are rebounding at a 6.82% CAGR through 2031 amid tourism recovery in Thailand and Singapore.

- By geography, China commanded 31.20% of regional revenue in 2025 while Vietnam is forecast to expand at a 7.65% CAGR, underpinned by beer representing 91.5% of total alcohol consumption and continuing tourist inflows.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brewery and craft-beer expansion across Asia-Pacific | +0.8% | India, Vietnam, China (tier-2/3 cities), Indonesia, Thailand | Medium term (2-4 years) |

| Premiumization driven by rising middle-class incomes | +1.2% | India, Vietnam, Indonesia, Philippines, China (urban centers) | Long term (≥ 4 years) |

| Product innovation (flavor, low/no-alc, functional) | +0.9% | Global, with early adoption in Japan, South Korea, Singapore, Australia | Short term (≤ 2 years) |

| Tourism and hospitality channel growth | +0.7% | Thailand, Vietnam, Singapore, Malaysia, Indonesia | Short term (≤ 2 years) |

| AI-enabled supply-chain and demand forecasting | +0.3% | Global, led by multinational brewers in China, Japan, Australia | Medium term (2-4 years) |

| Govt-led barley/hops modernization programs | +0.4% | China, India, Australia (agricultural policy zones) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Brewery and craft-beer expansion across Asia-Pacific

India now boasts over 500 microbreweries, a tenfold increase since 2015. However, new entrants face 28 distinct state regulations, often encountering licensing delays of 12 to 18 months. In a pivotal move on June 23, 2025, India's Food Safety and Standards Authority (FSSAI) rolled out new regulations[1]Source: Food Safety and Standards Authority, "Food Safety and Standards (Alcoholic Beverages) Regulations, " fssai.gov.in. These regulations acknowledged categories like nitro craft beer, ready-to-drink alcoholic beverages (with an alcohol by volume of 0.5–15%), mead, and country liquors. Meanwhile, in Vietnam, as domestic craft production gains momentum, the value of imported crafts has dwindled from USD 650 million in 2022 to USD 549 million in 2024. This shift comes as on-premise demand realigns under Decree 100. In China, as urbanization intensifies, tier-2 and tier-3 cities are seeing a surge in new brewpubs. Yet, U.S. craft exports to China, hampered by tariff frictions, only reached USD 19.49 million in 2024. Local players adept at navigating permitting and distribution are seizing market share, outpacing global giants hindered by corporate compliance timelines. Furthermore, joint-venture and contract-brewing models are emerging as a strategic, low-risk avenue for scaling production near demand hubs.

Premiumization driven by rising middle-class incomes

In 2025, Anheuser-Busch InBev raised its revenue per hectoliter in China by 4.8%, even as volumes dipped by 8.6%. This move underscores a successful strategy prioritizing margins over sheer volume. Forecasts indicate that India's beer market, valued at USD 9.2 billion in 2023, is set to surge to USD 14.6 billion by 2027. This growth is attributed to an expanding middle class shifting its consumption from traditional strong spirits. Meanwhile, Vietnam's beer production is projected to jump from 4,233.5 million liters in 2023 to 6,409.6 million liters by 2028, buoyed by rising disposable incomes and a thriving tourism sector. To counteract the pinch from raw-material inflation and escalating excise duties, global brewers are turning to premium SKUs, especially as urban consumers increasingly associate higher prices with superior quality. This trend positions premium offerings as both a shield and a weapon in the margin game. The beer market's evolution reflects changing consumer preferences and economic dynamics across regions.

Product innovation in flavor and low or no alcohol

Asahi, anticipating consumer wellness trends and tightening drink-drive regulations, aims to have low- or non-alcohol lines constitute 20% of its portfolio by 2025. In 2024, breweries in Singapore rolled out probiotic beer, targeting health-conscious millennials with its functional claims. Heineken, in 2024, launched Tiger Crystal, a lower-calorie lager, in Shanghai, catering to the city's urban fitness culture. That same year, Carlsberg introduced Tuborg Seltzer in China, aiming to maintain shelf presence amidst the rising popularity of RTD alternatives. To meet retailers' demand for newsworthy SKUs that command premium shelf space, brands are increasingly rotating flavors and extending functional offerings. These developments highlight the industry's shift toward innovation to align with evolving consumer preferences.

Tourism and hospitality channel growth

In 2024, Thailand welcomed 28 million visitors and set its sights on 40 million for 2025, boosting beer sales in hotels and bars[2]Source: Tourism Authority of Thailand, "Thailand Welcomes Over 35 Million Visitors in 2024: A Milestone Paving the Way for 2025, " tatnews.org. Vietnam's international arrivals hit 17.5 million by November 2024, marking a 43% surge and reviving the draft beer scene in its major cities[3]Source: DEPARTMENT OF GRASSROOTS INFORMATION AND EXTERNAL INFORMATION, "Vietnam welcomed 1.7 million international visitors in November, " vietnam.vn. Singapore recorded 15.8 million visitors in 2024, contributing to the Asia-Pacific region's tourism rebound to 82% of pre-pandemic figures. On-premise channels, commanding a 20-30% price premium over retail, have become vital for profitability, especially as experience-driven consumers flock back to nightlife. In response, brewers are introducing draft-only lines and exclusive SKUs in hospitality, aiming to secure these lucrative accounts. This trend highlights the growing importance of aligning product offerings with evolving consumer preferences in the post-pandemic era. Additionally, the recovery in tourism is expected to further stimulate demand for premium and craft beer options in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent taxation and advertising regulations | -0.9% | Vietnam, India, Thailand, Australia, Japan, South Korea | Short term (≤ 2 years) |

| Health-driven moderation and abstinence trends | -0.6% | Japan, South Korea, Australia, Singapore, urban China | Medium term (2-4 years) |

| Climate-driven barley/hops supply shocks | -0.5% | Global, acute in Australia, China, India (agricultural zones) | Long term (≥ 4 years) |

| Rising RTD and hard-seltzer competition | -0.7% | Australia, Japan, South Korea, Singapore, urban China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent taxation and advertising regulations

By 2030, Vietnam plans to raise its special-consumption tax on certain goods from 65% in 2025 to 80% in 2026, eventually hitting 100%. This move is set to squeeze profit margins and challenge the price sensitivity of consumers. In India, a hefty 100% import duty on beer, combined with state taxes that claim 60-75% of the retail price, has resulted in a fragmented market divided into 28 regulatory segments. Australia imposes one of the world's highest excise taxes on beer, set at AUD 2.26 per liter, translating to roughly USD 1.45. Meanwhile, Japan's gradual consolidation of liquor taxes diminishes the historical cost advantage of happoshu, a light beer, and could steer consumers towards more value-oriented beers. In Thailand, the Alcoholic Beverage Control Act tightens promotional activities, diminishing the elasticity of on-trade sales and complicating efforts to build brand recognition.

Health-driven moderation and abstinence trends

In Japan and South Korea, younger generations are increasingly adopting wellness narratives promoted by public health agencies, leading to a decline in per capita consumption. Meanwhile, Vietnam's Decree 100, which criminalizes any alcohol consumption before driving, is driving a shift towards smaller packs and lower-alcohol choices. Asahi's ambitious target of 20% non-alcoholic sales underscores the brewing giant's strategy for navigating the trend of moderation. In Australia and Singapore, premium retailers, once exclusive to imports, are now showcasing craft zero-proof beers. Brewers find themselves at a crossroads: while investing in non-alcoholic SKUs could cannibalize their core lager sales, not innovating at all risks losing market share to startups focused on wellness. This shift highlights the growing influence of health-conscious consumer preferences on the global alcoholic beverages market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Alcoholic Variants Reshape Portfolio Mix

Lager, accounting for 45.68% of the total share in 2025, remains the dominant segment in the Asia-Pacific beer market. Its supremacy is attributed to efficient production, cost-effectiveness, and a flavor profile tailored to the region's warm climates. While established international and local brands enjoy sustained loyalty, demand has begun to stabilize in more mature markets. In response to shifting consumer preferences, brewers like Heineken are rolling out lower-calorie options, such as Tiger Crystal. Such strategic innovations, albeit measured, ensure that lager retains its pivotal position in the region's beer landscape, even amidst a deceleration in growth. Additionally, the segment benefits from strong distribution networks that ensure widespread availability across urban and rural areas.

Non- and low-alcohol beer is rapidly gaining traction, with projections indicating a robust 7.92% CAGR through 2031. This surge can be attributed to heightened health consciousness and stringent zero-alcohol driving laws. Retailers are bolstering this trend by dedicating more shelf space to functional and alcohol-free products. Both regional players and global brewers are seizing the opportunity, diversifying their portfolios with premium zero-proof lines to enhance profit margins. This evolution underscores a market split: while mass-market lagers drive volume, premium non-alcoholic variants are the key to profitability. Furthermore, advancements in brewing technology are enabling producers to improve the taste and quality of non-alcoholic offerings, further driving consumer acceptance.

By Category: Premium Tier Outpaces Standard Despite Volume Headwinds

In 2025, standard beer dominated the Asia-Pacific beer market, accounting for 65.05% of total revenue. This segment's stronghold is bolstered by extensive distribution networks, competitive pricing, and a robust presence in rural and semi-urban areas. While its growth has slowed, standard beer remains pivotal for brewers, ensuring both scale and supply-chain efficiency across varied markets. These standard lines not only anchor brand portfolios but also safeguard market reach in economies sensitive to pricing. Yet, brewers face a hurdle: rising material and tax costs threaten to squeeze margins in this foundational category.

Premium beer is on a rapid ascent, with projections indicating a 7.18% CAGR through 2031, outpacing the regional average of 5.22%. This surge is largely fueled by urban hubs in India, Vietnam, and Indonesia, where affluent consumers are increasingly opting for quality and brand prestige. To capitalize on this premiumization trend, brewers are rolling out imported and limited-edition variants, justifying their elevated prices while countering input cost pressures. Notably, companies like Carlsberg are bolstering regional capacities, with a pronounced focus on premium lines at their brewery in India. Consequently, as premium beer carves out a larger market share, its profitability is set to rise, steadily closing the gap with standard offerings.

By Packaging Type: Sustainability Mandates Accelerate Can Adoption

In 2025, bottled beer dominated the Asia-Pacific market, making up 57.62% of total sales. This stronghold is largely due to the widespread use of returnable-glass systems in Southeast Asia, bolstering both circular-economy initiatives and cost-effectiveness. Glass packaging is particularly favored in the premium on-trade segment, symbolizing quality and a rich heritage. Leading brewers consistently choose glass for their flagship lager brands and key consumption moments. Yet, the growth of this format faces hurdles from rising logistics costs and stricter environmental regulations. Despite these challenges, glass remains a preferred choice for markets emphasizing tradition and premium positioning.

Canned beer is on the rise, projected to grow at a 6.04% CAGR until 2031. Aluminum cans, boasting a carbon footprint that's about 50% lighter than glass, are in sync with the new Extended Producer Responsibility (EPR) regulations taking shape in China, India, and Vietnam. This eco-friendly edge, combined with their portability and trendy designs, strikes a chord with the younger, urban demographic. Retailers and e-commerce platforms prefer cans for their lightweight and stackable nature, enhancing both shelf space and delivery efficiency. Investments like Heineken Vietnam’s state-of-the-art canning plant underscore the industry's shift towards greener procurement standards. Additionally, the rising popularity of canned craft beers further supports the segment's growth trajectory.

By Distribution Channel: On-Trade Rebounds as Tourism Recovers

Off-trade remained the dominant distribution channel in the Asia-Pacific beer market, capturing 61.70% of total share in 2025. This strength reflects enduring at-home drinking habits established during the pandemic, reinforced by retail modernization and greater cold-chain reach. E-commerce platforms and convenience stores in countries like India and Vietnam continue to drive consistent off-trade growth. Brewers are increasingly using shopper data and loyalty apps to tailor promotions and enhance visibility across retail networks. As omnichannel strategies develop, off-trade retains its critical role in maintaining reach and stability across markets.

On-trade is emerging as the fastest-growing channel, forecast to expand at a 6.82% CAGR through 2031. The rebound of tourism, nightlife, and business travel, particularly in destinations such as Thailand and Singapore, is fueling renewed demand in bars, restaurants, and hotels. Brewers are launching draft-only or exclusive on-premise variants to capture premium margins and strengthen brand equity. This revival positions the on-trade segment to outpace the broader market baseline in value terms. As regulatory shifts and experiential preference reshape consumption, balancing on- and off-trade presence will define brewer competitiveness.

Geography Analysis

In 2025, China accounted for 31.20% of the regional revenue. However, as younger consumers moderated their intake, volumes contracted. This shift prompted brewers to rationalize their SKUs, resulting in a 4.8% increase in revenue per hectoliter. While coastal regions embraced premiumization, inland provinces lagged and remained sensitive to price hikes. Furthermore, a regulatory push for ingredient transparency in 2027 is set to heighten formulation costs. China's heavy reliance on imported barley, meeting 90% of its malting needs, leaves its margins vulnerable to fluctuations in freight and currency. Brewers are expected to explore alternative sourcing strategies to mitigate these risks.

Vietnam is on track to be the fastest-growing market, boasting a 7.65% CAGR through 2031. This growth is buoyed by beer's dominance, making up 91.5% of alcohol consumption, a 43% surge in tourist arrivals in 2024, and expansions like Heineken's new 500 million-liter facility in Tien Giang. However, an escalating special-consumption tax, aiming for a full 100% by 2030, poses a significant margin challenge, pushing brewers towards intensified premium pricing strategies. Additionally, the growing middle class in Vietnam is expected to further drive demand for premium beer products.

India's market value is set to jump from USD 9.2 billion in 2023 to an estimated USD 14.6 billion by 2027. Yet, per-capita consumption remains stagnant at around 2 liters, hindered by steep 100% import duties and a convoluted state regulatory landscape. In a bid to tap into premium niches with heftier margins, global brewers are expanding capacities in Odisha and Rajasthan, even amidst regulatory challenges. Meanwhile, Japan and South Korea are aligning tax rates across various beer types, a move that could redirect demand back to mainstream lagers and lessen the cost disparity with happoshu. Despite facing high excise taxes, Australia thrives on a vibrant premium craft culture and a commendable per-capita expenditure. On the other hand, frontier markets like Indonesia and the Philippines show promise due to rising urbanization and tourism. However, unpredictability in policies, as evidenced by multinational withdrawals from Myanmar in 2024, poses a significant hurdle. Rising disposable incomes in these frontier markets could further unlock growth potential in the coming years.

Regulatory Landscape

Alcohol regulation in Asia-Pacific is tightening around health, labeling, advertising, and place-based controls, which is raising compliance costs and increasing SKU and pack-format complexity across markets. In Australia, Food Standards Australia New Zealand (FSANZ) gazetted mandatory energy labelling for most packaged alcoholic beverages in August 2025, with a transition period running to August 13, 2028. Enforcement commenced in February 2026 under the Australia New Zealand Food Standards Code, pushing brewers and importers to update label artwork and manage run-down of legacy inventory.

In Southeast Asia, Vietnam and Thailand have added specificity to operating rules. Vietnam signed Decree No. 342/2025/ND-CP in December 2025 (effective February 15, 2026) to elaborate the Law on Advertising for beer and other alcoholic beverages, while the Ministry of Industry and Trade issued Circular No. 39/2026/TT-BCT in June 2026 promulgating QCVN 30:2026/BCT, a national technical standard for alcoholic beverages effective January 1, 2027, with a defined timetable for quality and conformance documentation. Thailand's Alcoholic Beverage Control Committee issued eight announcements effective May 12, 2026 under the Alcoholic Beverage Control Act B.E. 2551 that designate prohibited areas for alcohol sale and consumption, reinforcing the need for on-trade and off-trade partners to adapt at the store level and venue level.

Competitive Landscape

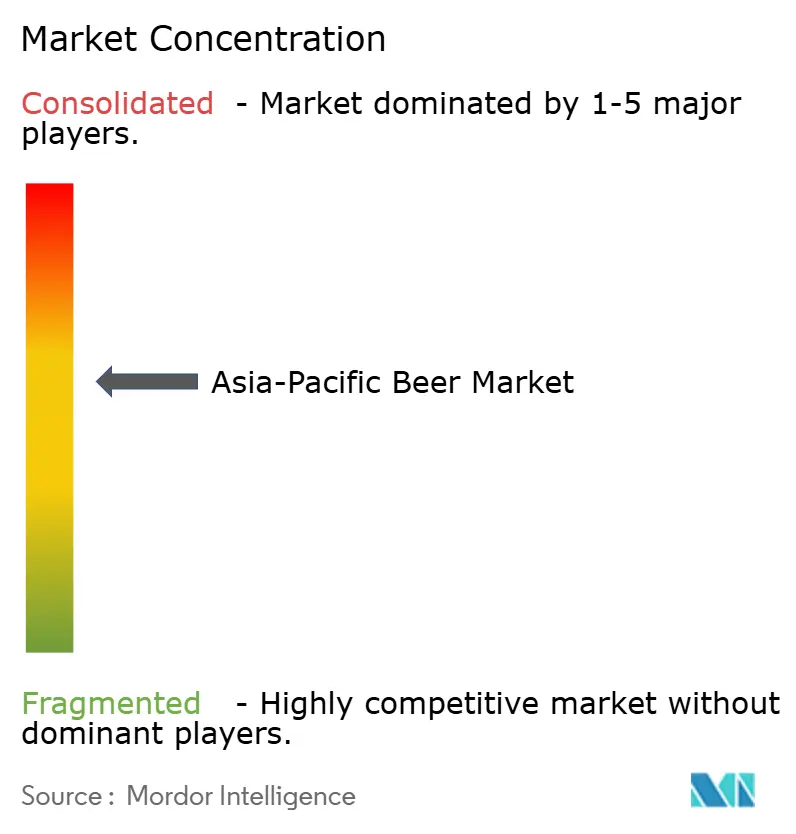

The Asia-Pacific beer market reflects moderate fragmentation, where five global majors contend with strong domestic leaders. Anheuser-Busch InBev, Heineken, Carlsberg, Asahi, and Kirin command a significant share of the premium and super-premium segments. In contrast, domestic leaders like China Resources Beer, Tsingtao, Thai Beverage, and San Miguel reign supreme in mainstream categories. The strategic withdrawals of Heineken and Kirin from Myanmar in 2024 highlight the impact of geopolitical shifts, steering investments towards the more stable markets of Vietnam and India.

Portfolio premiumization stands as the primary strategy; AB InBev's 4.8% revenue uptick per hectoliter in China, despite a dip in volume, underscores a focus on margin preservation over mere market share. With over USD 270 million poured into capacity expansions in 2024, Vietnam and India are set to see an addition of 700 million liters, a testament to the firms' bullish outlook on demand. Meanwhile, as craft brands and ready-to-drink (RTD) products blur category lines, innovations like Tuborg Seltzer in China emerge as defensive responses.

Technology is carving out competitive edges: Heineken Vietnam's adoption of AI forecasting sets it apart from smaller competitors, widening the operational efficiency gap. As climate fluctuations jeopardize input costs, the allure of integrating barley and hops into the supply chain intensifies. Companies that harmonize sustainability commitments with shifts to aluminum cans and renewable energy will find favor with global retailers. Moreover, adept navigation of regulations, particularly in India's intricate state-level landscape and Vietnam's tightening excise policies, offers established players a distinct advantage.

Asia-Pacific Beer Industry Leaders

-

Anheuser-Busch InBev

-

Asahi Group Holdings, Ltd.

-

Heineken NV

-

Carlsberg Group

-

Kirin Holdings Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premium portfolio building and cross-border route-to-market reconfiguration are creating whitespace for scale players and strong local partners, especially where tourism-led on-trade recovery supports margin-led growth. In July 2026, Carlsberg and Sapporo announced a strategic partnership that includes a Singapore-based joint venture for Southeast Asia and Hong Kong, backed by a USD 643 million investment for a 25% stake, which underscores the growing use of regional platforms for premium brand distribution rather than country-by-country buildouts.

Operational execution and sustainability-linked packaging shifts are also generating investment opportunities across breweries and supply chains, particularly for cans and compliant labeling. Heineken Vietnam expanded investment to raise Da Nang brewery capacity by 50% to 500 million liters per year (April 2026), and Heineken Malaysia outlined a regional supply chain shift in which Malaysia and Vietnam supply Singapore while the Tuas brewery transitions to a logistics and innovation hub (March 2026). These moves align with rising regulatory requirements such as Australia's mandated energy labelling and Vietnam's move toward a national technical standard effective in 2027, favoring producers that can execute faster label changes, optimize multi-country inventory, and deploy digital manufacturing and energy-management systems, including Boonrawd Brewery’s February 2026 agreement with REPCO NEX (SCG Chemicals) to implement Digital Reliability Solutions for smart manufacturing and energy management.

Recent Industry Developments

- July 2026: Carlsberg Group and Sapporo Breweries entered a strategic partnership, including Sapporo's USD 643 million investment for a 25% stake in a Singapore-based joint venture covering Southeast Asia and Hong Kong. The structure extends premium portfolio reach through shared regional platforms and is slated to be established in December 2026, supporting wider distribution and coordinated go-to-market execution across multiple Asia-Pacific countries.

- May 2026: Budweiser Brewing Company APAC disclosed updates alongside its Q1 2026 reporting that pointed to volume stabilization and growth in India while continuing investment emphasis in China. The disclosure highlights how large brewers are balancing premiumization and route-to-market spend across the region's biggest profit pools rather than pursuing volume at any cost.

- August 2024: XXXX launched XXXX Ultra Zero Carb in Australia, expanding the brand's presence in the zero/low carbohydrate proposition within mainstream beer. The move strengthened competitive positioning against moderation-driven shifts and adjacent better-for-you alcohol alternatives that are taking shelf space in modern off-trade channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the total value of beer sold across Asia-Pacific, counted across mainstream and premium offerings and tracked across key packaging and sales channels.

Scope exclusions: We do not count adjacent alcoholic drinks such as cider, ready-to-drink mixes, wine, or spirits under this market boundary.

Segmentation Overview

-

By Product Type

- Ale

- Lager

- Non/Low-Alcohol Beer

- Other Beer Types

-

By Category

- Standard

- Premium

-

By Packaging Type

- Bottles

- Cans

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Other Off-Trade Channels

-

By Geography

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Vietnam

- Philippines

- Malaysia

- Singapore

- New Zealand

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

We start with desk research to build the fact base around beer production, trade, and consumption signals in Asia-Pacific, because these inputs are the most repeatable anchors for a value model. Public sources such as national statistics offices, customs and trade portals, UN Comtrade-style trade series, and food and beverage regulators help us read category direction and any policy impact on imports and pricing.

To tighten assumptions, we also review company annual reports, investor presentations, and credible press coverage on pricing moves, pack changes, and channel expansion in the region. Where needed, paid subscriptions that track company financials and news, plus shipment-level import and export records, are used to sanity check trends and to avoid relying on one data stream. These desk research sources are illustrative, and many other public and paid references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions, particularly where price per liter shifts quickly due to tax changes, premiumization, or pack-size moves. We spoke with supply-side and channel-side stakeholders, and we also validated with local market observers across major APAC beer countries, so the model aligns with what is actually being sold and at what price level in each channel.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 39% | |

| Smaller Players: 16% | Managers: 47% |

Market-Sizing & Forecasting

The main sizing path is top-down, where production and trade data is used to reconstruct the regional beer demand pool and then converted into value using price per liter logic by country and channel. To keep it grounded, the totals are corroborated through selective bottom-up approximations, such as sampled price points by pack type, channel mix checks, and a supplier and importer roll-up in markets where disclosures are available.

Key inputs that shape the model include beer volume trends (liters), the on-trade versus off-trade split, packaging mix shifts between bottles and cans, premium share movement, and tax and duty changes that affect shelf pricing. Because data coverage varies by country, gaps are handled by using proxy indicators like import intensity, category growth rates from public statistics, and interview-based ranges on ASP progression, and then the results are reconciled back to the regional total.

For forecasting, we rely on scenario analysis tied to a short list of drivers, including expected consumption growth, real price movement, premiumization pace, and channel normalization after travel and hospitality swings. Where time series is stable, simple exponential smoothing is used on volume, and then pricing is layered on using the agreed primary ranges so the value forecast stays explainable and repeatable.

Data Validation & Update Cycle

Outputs are checked through multiple steps, starting with internal variance checks on price per liter, channel splits, and implied per-capita consumption levels so outliers are surfaced early. When the model produces a jump that cannot be explained by taxes, packaging changes, or a clear volume swing, we recheck assumptions and, if needed, reconnect with respondents for confirmation.

Before sign-off, the figures are reviewed against independent signals like trade movement, public production indicators, and reported category performance commentary, and then the logic is re-tested at country level before rolling up to APAC. The report is refreshed annually, with interim updates when material events occur, and a final freshness pass is completed right before delivery so clients receive the most current view.

Mordor Intelligence's Asia Pacific Beer Market Sizing Compared With Other Published Estimates

Published market values for Asia-Pacific beer can differ widely because of the timing of currency conversion, the pricing level used, and the update frequency. Differences also show up when one study leans more on trade value, while another leans more on consumer spending, which changes what is included.

A refresh-led gap is common in this market because beer prices move with taxes, premium mix, and pack formats, so older ASP assumptions can remain in the model longer than they should. By revalidating price per liter and channel mix close to the base year, and applying consistent currency timing, Mordor Intelligence reduces drift that can come from stale wholesale-price series or from mixing retail and ex-producer values.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 240.87 B (2025) | |

| Global Consultancy A | USD 297.89 B (2024) | Uses a different base year and revenue framing, and the APAC country coverage and channel treatment are not clearly itemized, which can inflate totals when higher retail-price points are implicitly captured. |

| Trade Analytics Publisher B | USD 44.40 B (2024) | Values are stated in nominal wholesale prices tied to producers and importers and exclude retail margins and other downstream costs, which typically produces a much smaller number than consumer-facing value models. |

The spread across the three figures is mainly explained by pricing level and update timing, rather than by one single demand assumption. When scope is kept strictly to beer and the ASP logic is refreshed using near-term channel checks, the final value is easier to trace back to liters, mix, and pricing steps that can be repeated year after year.

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific beer market by 2031?

It is forecast to reach USD 326.86 billion, growing at a 5.22% CAGR from 2026 to 2031.

Which product type is growing fastest within Asia-Pacific beer?

Non- and low-alcohol variants are advancing at a 7.92% CAGR through 2031 as health and regulatory factors gain importance.

Why are aluminum cans gaining share in Asia-Pacific beer packaging?

Cans have a 50% lower carbon footprint than glass and align with new producer-responsibility rules, driving a 6.04% CAGR to 2031.

Which geography is forecast to grow fastest in regional beer sales?

Vietnam leads with a 7.65% CAGR thanks to high beer share of alcohol consumption and strong tourism growth.

Page last updated on: