Asia Pacific Base Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

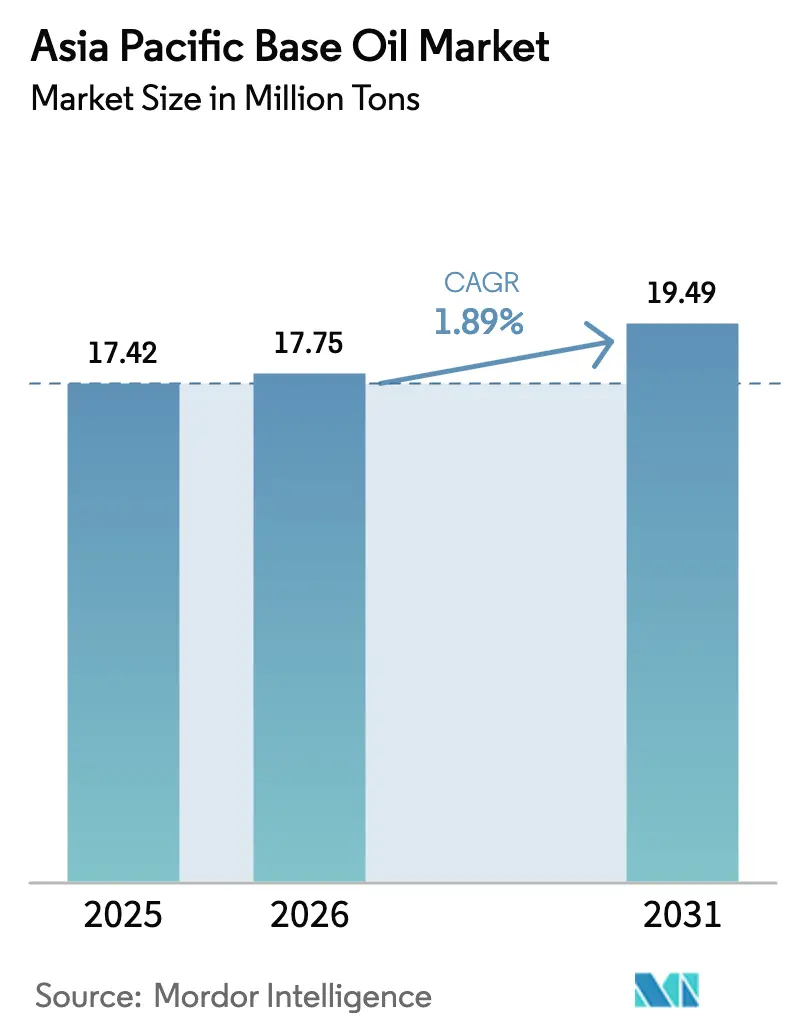

| Base Year Market Size (2025) | 17.42 Million tons |

| Market Volume (2026) | 17.75 Million tons |

| Market Volume (2031) | 19.49 Million tons |

| Growth Rate (2026 - 2031) | 1.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Base Oil Market Analysis by Mordor Intelligence

The Asia Pacific Base Oil Market size was valued at 17.42 million tons in 2025 and is estimated to grow from 17.75 million tons in 2026 to reach 19.49 million tons by 2031, at a CAGR of 1.89% during the forecast period (2026-2031). Stricter emission regulations in China and India are accelerating the shift from Group I toward Group II and Group III grades, while electric-vehicle (EV) adoption is beginning to chip away at internal-combustion-engine lubricant demand. Integrated refiners with hydrocracking upgrades in Ningbo, Tahe, and Singapore are boosting Group II output faster than regional offtake, creating a heavy-grade surplus that pressures merchant blenders. Engine oil demand remains resilient thanks to longer drain intervals, two-wheeler delivery fleets, and low-SAPS formulations, yet the Asia Pacific Base Oil market faces a widening quality gap as low-sulfur premium stocks grow scarcer in inland areas. Consolidation among teapot refiners, API 1509 base-stock interchange rules, and emerging circular-economy mandates will shape supply dynamics through 2031.

Key Report Takeaways

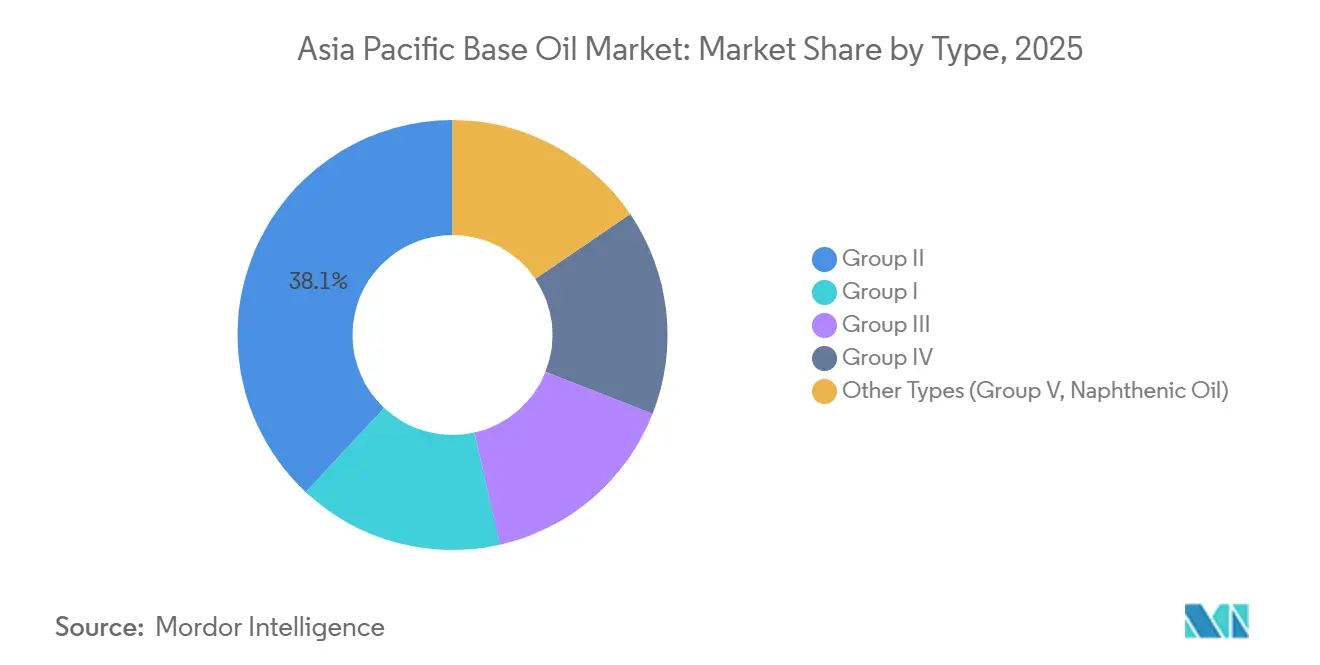

- By type, Group II captured 38.05% of the Asia Pacific base oil market share in 2025, while Group III is forecast to expand at a 3.30% CAGR to 2031.

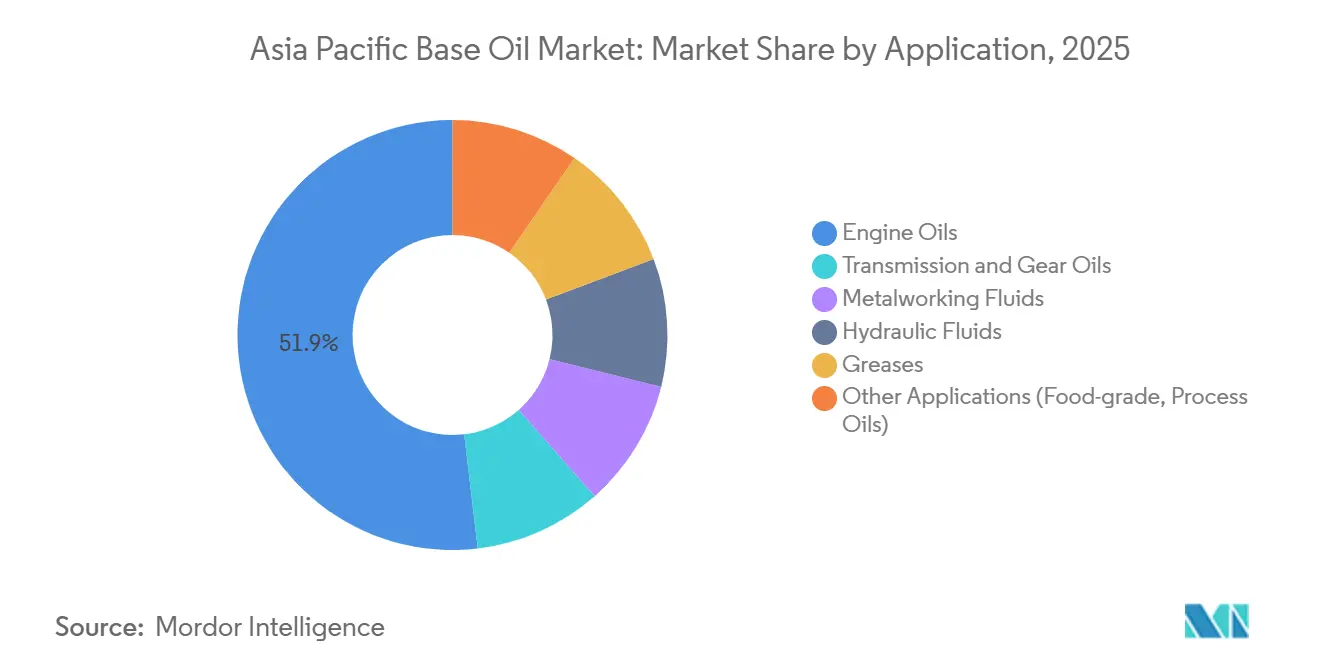

- By application, engine oils accounted for 51.87% of the Asia Pacific base oil market size in 2025 and are advancing at a 2.75% CAGR through 2031.

- By geography, China led with 46.02% volume in 2025; India is the fastest-growing market at a 2.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on base oil market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia Pacific Base Oil Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shift from Group I to Group II base stocks due to tightening emission norms | +0.6% | China, India, ASEAN core (Thailand, Indonesia, Vietnam) | Medium term (2-4 years) |

| Rising demand for high-performance automotive lubricants in China and India | +0.5% | China, India | Short term (≤ 2 years) |

| OEM-driven drain-interval extensions favouring premium Group III/IV stocks | +0.4% | Global, with concentration in Japan, South Korea, China | Medium term (2-4 years) |

| Adoption of re-refined base oils under circular-economy policies | +0.2% | Singapore, China, India | Long term (≥ 4 years) |

| Surge in two-wheeler delivery fleets accelerating low-viscosity engine-oil uptake | +0.3% | India, Indonesia, Vietnam, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Shift from Group I to Group II Base Stocks Due to Tightening Emission Norms

India’s BS VI and China 6 standards limit sulfur to 10 ppm, forcing blenders to abandon Group I stocks for cleaner Group II alternatives. ExxonMobil’s Singapore Resid Upgrade Project added 20,000 barrels per day of Group II capacity in September 2025 to serve this demand[1]ExxonMobil, “Singapore Resid Upgrade Project Starts Up,” corporate.exxonmobil.com. Japan’s JASO GLV-2 spec for ultra-high-viscosity-index oils is pushing Group III adoption in hybrids. Rural India and inland China still rely on Group I for price-sensitive segments, creating a parallel supply chain that will persist until 2028. Mid-tier refiners are fast-tracking hydrocracker revamps to stay relevant, yet cash-flow constraints limit upgrades to coastal assets.

Rising Demand for High-Performance Automotive Lubricants in China and India

China produced 30.2 million vehicles in 2024, with turbocharged engines exceeding 60% of output, up from 45% in 2020. Turbocharged units run hotter, so OEMs specify Group II or Group III oils to prevent oxidation. India’s passenger-vehicle sales reached 4.2 million units in fiscal 2025, with SUVs claiming 48% of registrations. Carmakers such as Maruti Suzuki pre-fill engines with API SP oils, locking the aftermarket into premium grades. This preference compresses the addressable pool for Group I stocks, which now serve mostly heavy-duty diesel fleets.

OEM-Driven Drain-Interval Extensions Favouring Premium Group III/IV Stocks

Toyota’s 2025 hybrid service schedules stretch oil changes to 15,000 kilometers when 0W-16 or 0W-20 Group III formulations are used. Hyundai and Kia apply similar regimes for GDI engines to avoid low-speed pre-ignition. GS Caltex, with 275,000 barrels per day of heavy-oil upgrading, supplies Group III stocks that underpin these longer drains. Premium SKUs enjoy USD 200–300 per-ton pricing spreads over commodity grades, yet additive packages cost USD 150–200 per ton, squeezing blenders that lack scale.

Adoption of Re-Refined Base Oils Under Circular-Economy Policies

China’s Ministry of Ecology and Environment requires collectors to divert 30% of used lubricants to licensed re-refiners by 2026[2]Ministry of Ecology and Environment, China, “Guidelines on Used-Oil Collection,” mee.gov.cn. Neste’s USD 2.1 billion Singapore expansion can transform waste fats into Group II-equivalent stocks, opening a renewable feedstock pool. India’s Extended Producer Responsibility framework imposes collection targets, but patchy enforcement outside tier-1 cities limits feed quality. Re-refined oils sell at a USD 50–100 per-ton discount to virgin Group II, yet concerns over batch consistency deter mainstream adoption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV penetration curbing long-term ICE-lubricant demand | -0.5% | China, Thailand, India | Medium term (2-4 years) |

| Persistent oversupply in heavy grades (SN 500/BS) depressing prices | -0.3% | China, Singapore, South Korea | Short term (≤ 2 years) |

| Quality-perception barriers limiting re-refined base-oil adoption | -0.1% | India, ASEAN (Indonesia, Vietnam) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Penetration Curbing Long-Term ICE-Lubricant Demand

Battery-electric vehicles need 70% less lubricant than gasoline cars, a reality most visible in China, where EV sales reached 9.5 million units in 2024, equal to 35% of passenger-car volume. Thailand hit EV price parity in 2024, and India’s two-wheeler electrification rate is scaling fast. Commercial trucks and off-highway gear remain ICE-dominated, but passenger-car lubricant pools will continue shrinking, setting a ceiling on long-term Asia Pacific Base Oil market growth.

Persistent Oversupply in Heavy Grades (SN 500/Bright Stock) Depressing Prices

Sinopec’s Tahe upgrade and CNOOC’s Daxie expansion have injected unplanned heavy barrels into a saturated market, pushing SN 500 spot prices in Singapore down 15% year-on-year in H1 2025. Teapot refiners that survived the 2023–24 consolidation wave are exporting surplus volumes, eroding margins for merchant suppliers. Integrated majors hedge by channeling bright-stock output into marine and industrial lubes, but smaller blenders face shrinking spreads that may trigger further consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Group II Dominance Meets Group III Momentum

Group II held 38.05% of the Asia Pacific base oil market in 2025, owing to emission-driven demand for low-sulfur stocks. The Asia Pacific Base Oil market size for Group III is forecast to expand at a 3.30% CAGR, the fastest among all grades, propelled by turbocharged and hybrid powertrain requirements. ExxonMobil’s new EHC 340 MAX extra-heavy Group II grade targets sectors that once relied on bright stock. Petronas and Pertamina’s planned 800-tons-per-day Group III plant in Indonesia will deepen regional supply diversity. Margin gaps between Group II and Group III have narrowed to USD 150–200 per ton, encouraging blenders to switch applications without prohibitive cost penalties.

Legacy Group I capacity now supports niche heavy-duty diesel and industrial fluids, but continues to lose share. Indian Oil Corporation’s Panipat revamp and HPCL’s LOBS upgrades will convert significant Group I throughput into Group II and Group III by 2026, accelerating the trend. Group IV PAO remains below 5% of regional volume yet commands premium pricing in aerospace, while Group V naphthenics serve stable specialty segments. Overcapacity risks persist if new hydrofinish units outpace high-grade demand, but refinery rationalization in inland China may remove marginal Group I assets by 2029.

By Application: Engine Oils Lead, Metalworking Fluids Trail

Engine oils absorbed 51.87% of demand in 2025, and the segment is advancing at a 2.75% CAGR through 2031, the swiftest among applications. OEM-mandated low-viscosity grades such as 0W-20 and 5W-30 require Group II or Group III stocks that resist oxidation and support fuel-economy gains. API’s SP and ILSAC’s GF-6 specs embed these requirements, effectively steering volume toward premium bases. Transmission-fluid demand faces long-run headwinds as EVs use simple reducers, but manual and CVT fluids remain relevant for legacy fleets.

Metalworking fluids track manufacturing activity, which stayed robust in China, India, and Vietnam, sustaining demand despite automation headwinds. Hydraulic fluids benefit from infrastructure megaprojects such as India’s Bharatmala and metro expansions, which use equipment that is slow to electrify. Among the greases, lithium-complex and polyurea formulations are gaining ground as EV motor bearings demand higher thermal stability. Food-grade, transformer, and process-oil niches remain small yet profitable, with demand tied to regulatory compliance rather than macro cycles.

Geography Analysis

China contributed 46.02% of regional volume in 2025, anchored by Sinopec and CNOOC’s refining scale. However, oversupply in heavy grades and peaking gasoline demand are eroding margins. The base oil market in India is growing fastest at a 2.98% CAGR, supported by Indian Oil Corporation’s USD 20 billion refinery expansion plan and HPCL’s Barmer greenfield project, which will cut import dependency from 36% in 2024 to an estimated 22% in 2028. Japan and South Korea exhibit stable demand but act as export hubs for specialty grades; GS Caltex alone ships significant Group III tonnage to Southeast Asia.

ASEAN economies are emerging growth pockets. Thailand’s USD 1.44 billion EV investment program has yet to dent ICE production, keeping lubricant demand buoyant. Indonesia and Vietnam attract foreign investment in manufacturing, feeding demand for metalworking and hydraulic fluids. Petronas Lubricants’ 220,000-tons-per-year Group III plant in Malaysia and the planned Indonesia JV position ASEAN as a future premium-base-oil hub. Australia and New Zealand, while small, provide steady marine and mining lubricant demand that values high-viscosity stocks.

Competitive Landscape

The Asia-Pacific Base Oil market is moderately fragmented. State-owned refiners such as Sinopec, CNOOC, and Indian Oil Corporation leverage integration to buffer base-oil price swings. ExxonMobil’s 20,000-barrel-per-day Group II expansion in Singapore folds into a fuels-plus-chemicals complex that maximizes margins. Shell and CNOOC’s Huizhou Phase 3 project, approved in January 2025, includes linear alpha olefin capacity that feeds synthetic PAO production, signaling a strategic pivot toward premium Group IV grades.

Re-refiners and specialty blenders occupy circular-economy niches. Neste’s USD 2.1 billion project in Singapore demonstrates the capital intensity required to scale renewable feedstock conversion. Chennai Petroleum invests INR 700–800 million annually to upgrade LOBS units for Group II/III output, highlighting regional ambition. Smaller blenders partner with additive majors to match performance without refining assets, yet margin compression in commodity grades hastens consolidation. API 1509 interchange rules lower technical barriers for re-refiners, but lingering quality perceptions limit their share below 5%.

Asia Pacific Base Oil Industry Leaders

SK On Co., Ltd.

Exxon Mobil Corporation.

Saudi Arabian Oil Co.

Chevron Corporation

GS Caltex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CNOOC commissioned the Daxie refinery expansion in Ningbo, doubling crude capacity to 240,000 barrels per day and installing a 2-million-tons-per-year hydrocracker for Group II feedstocks.

- January 2025: Shell and CNOOC received approval for a Phase 3 expansion of their Huizhou joint venture, adding 1.6 million tons per year of ethylene and LAO capacity to support synthetic base-oil production.

Asia Pacific Base Oil Market Report Scope

Base oils are the raw materials used to make lubricants, and their properties greatly influence the performance and characteristics of the finished lubricant. It is produced by extracting and treating high-viscosity material from narrow distillation cuts of vacuum gasoil or vacuum resid.

The Asia-Pacific base oil market is segmented by type, application, and geography. By type, the market is segmented into group I, group II, group III, group IV, and other types (group V and naphthenic). By application, the market is segmented into engine oils, transmission and gear oils, metalworking fluids, hydraulic fluids, greases, and other applications (food-grade lubricants, process oil, etc.). The report also covers the market size and forecasts for base oil in 5 countries across the Asia-Pacific region. For each segment, the market sizing and forecasts have been done based on volume (tons).

| Group I |

| Group II |

| Group III |

| Group IV |

| Other Types (Grouo V, Naphthenic Oil) |

| Engine Oils |

| Transmission and Gear Oils |

| Metalworking Fluids |

| Hydraulic Fluids |

| Greases |

| Other Applications (Food-grade, Process Oils) |

| China |

| India |

| Japan |

| South Korea |

| ASEAN Countries |

| Rest of Asia-Pacific |

| ByType | Group I |

| Group II | |

| Group III | |

| Group IV | |

| Other Types (Grouo V, Naphthenic Oil) | |

| By Application | Engine Oils |

| Transmission and Gear Oils | |

| Metalworking Fluids | |

| Hydraulic Fluids | |

| Greases | |

| Other Applications (Food-grade, Process Oils) | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected volume of the Asia Pacific Base Oil market in 2031?

The market is forecast to reach 19.49 million tons by 2031, growing at a 1.89% CAGR from 2026.

Which base-oil type is expanding fastest in the Asia-Pacific?

Group III leads growth at a 3.30% CAGR through 2031, boosted by OEM demand for high-viscosity-index stocks.

Why are Group I stocks losing share in the region?

Tightening emission norms in China and India mandate low-sulfur formulations that Group I cannot meet, pushing demand toward Group II and Group III grades.

How is EV adoption affecting lubricant demand?

Battery-electric vehicles need 70% less lubricant than ICE models, cutting long-term engine-oil volumes, especially in China, where EV penetration hit 35% of sales in 2024.

Which country shows the fastest base-oil demand growth?

India leads with a projected 2.98% CAGR through 2031, supported by refinery upgrades and vehicle-fleet expansion.

What role do re-refined base oils play in the Asia-Pacific?

Re-refined oils remain below 5% of supply but are gaining traction under circular-economy mandates in China, Singapore, and India, despite quality-perception challenges.

Page last updated on: