Auto-Injectors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

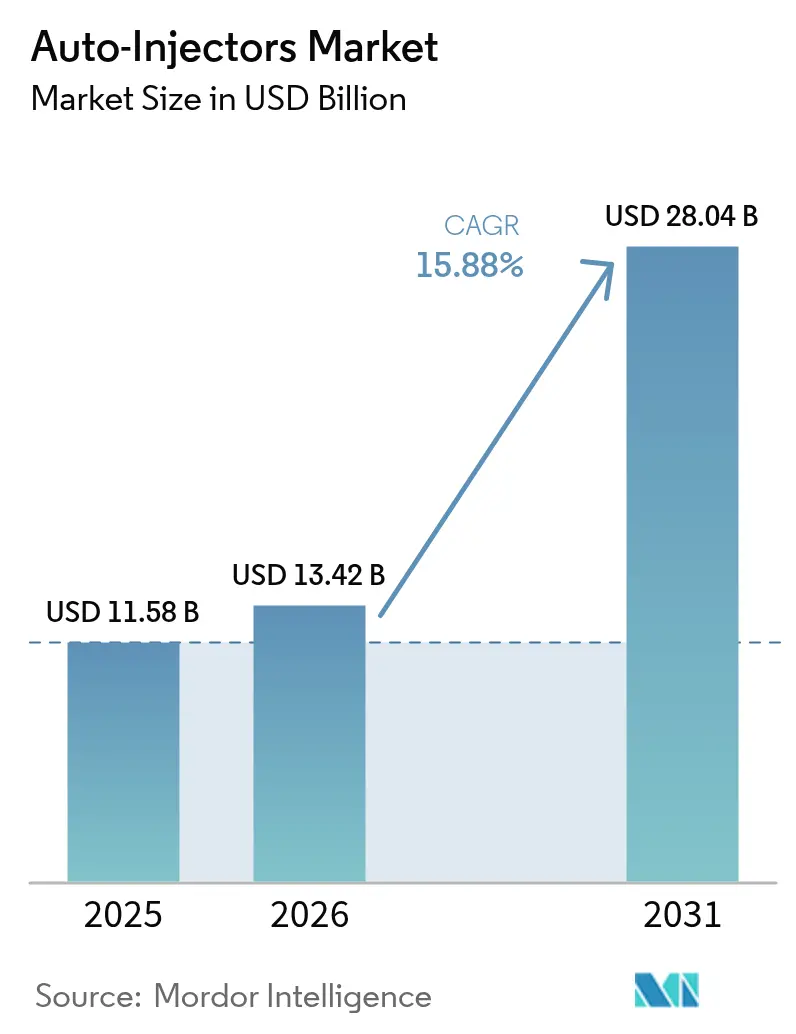

| Market Size (2026) | USD 13.42 Billion |

| Market Size (2031) | USD 28.04 Billion |

| Growth Rate (2026 - 2031) | 15.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Auto-Injectors Market Analysis by Mordor Intelligence

The auto-injectors market size is expected to grow from USD 11.58 billion in 2025 to USD 13.42 billion in 2026 and is forecast to reach USD 28.04 billion by 2031 at 15.88% CAGR over 2026-2031. Rising biologic drug launches, a larger chronic disease population and a decisive shift toward self-administration are synchronizing to propel demand. Regulatory agencies are clearing novel formats at a faster clip, illustrated by the first needle-free epinephrine alternative in more than three decades approved in 2024. Emergency-preparedness stock-piles, multi-billion-dollar capacity additions from leading manufacturers and sustained payer support for home-care therapies amplify momentum. Even so, specialty-component shortages and stricter combination-device rules underline the need for resilient supply chains and robust quality controls.

Key Report Takeaways

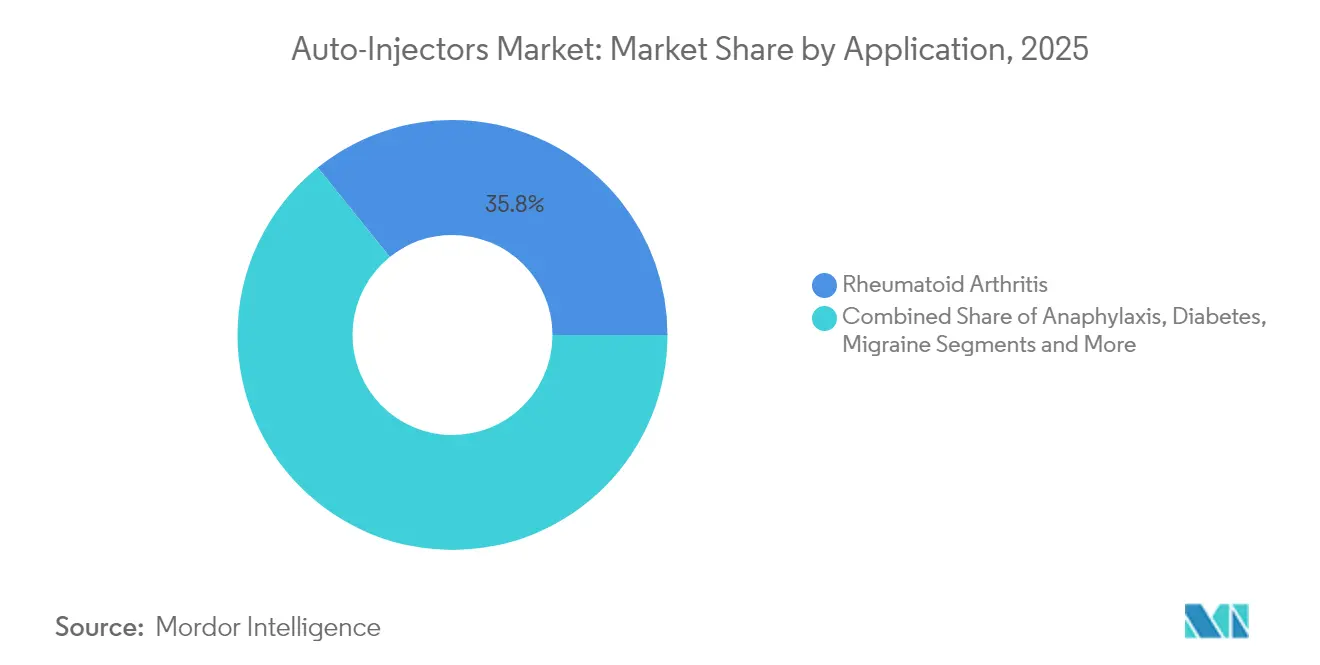

- By application, rheumatoid arthritis held 35.78% of the auto-injectors market share in 2025, while anaphylaxis is poised to expand at 18.63% CAGR through 2031.

- By usability, disposable formats dominated 2025 revenue at 68.77%, but connected smart auto-injectors are advancing at a 19.61% CAGR to 2031.

- By device technology, spring-loaded systems accounted for 61.65% of the auto-injectors market size in 2025; wearable on-body injectors are rising at 17.98% CAGR through 2031.

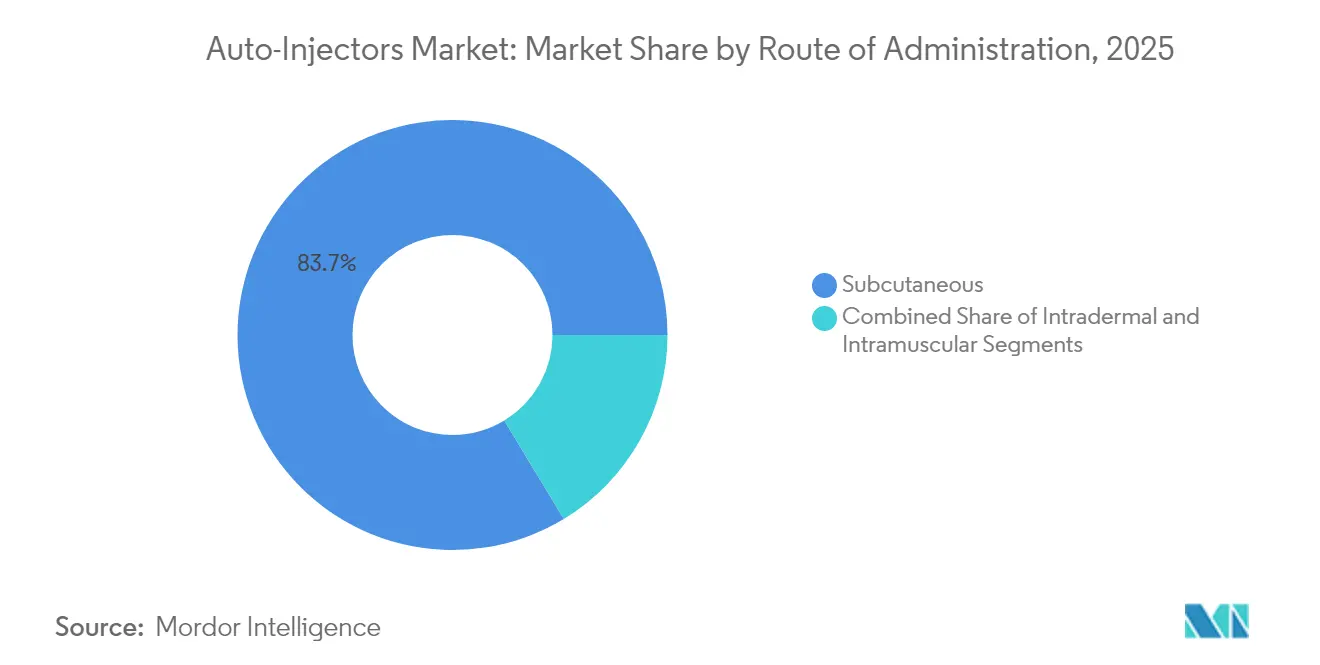

- By route of administration, subcutaneous delivery captured 83.66% share in 2025, whereas intradermal routes are forecast to grow 17.29% CAGR to 2031.

- By end user, home-care settings commanded 52.91% share of the auto-injectors market size in 2025, and ambulatory surgical centers will log the fastest CAGR at 17.22% to 2031.

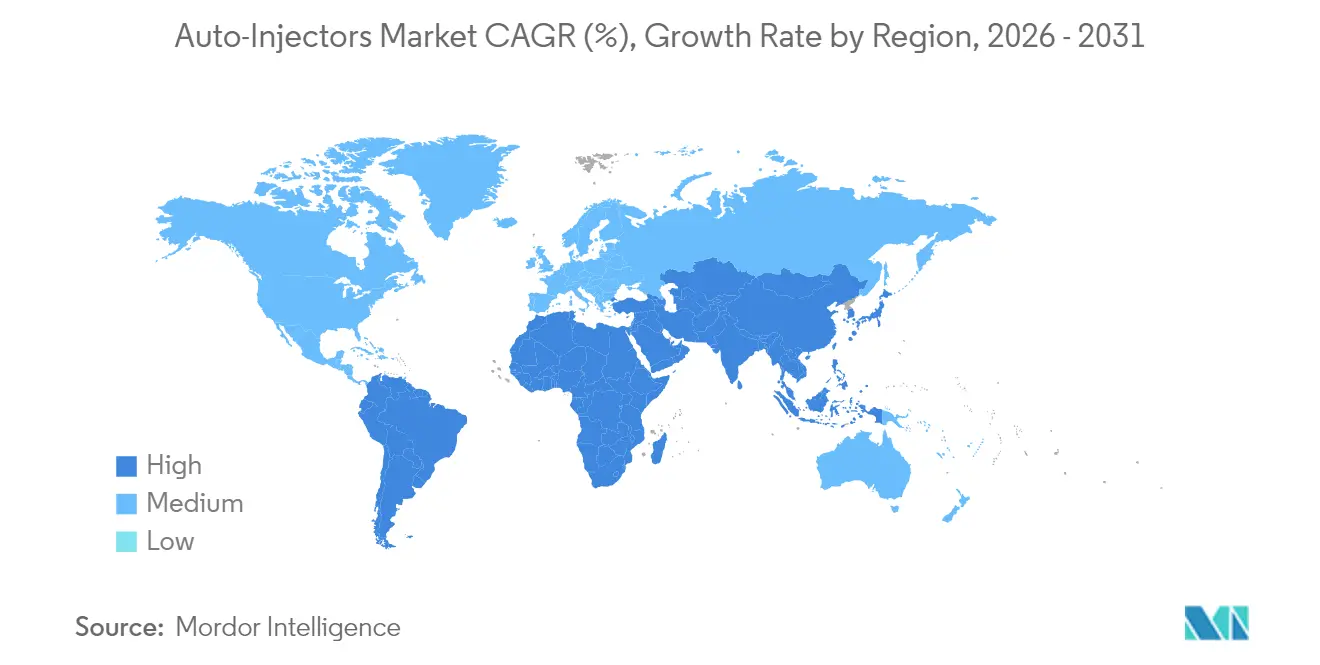

- North America led with 43.88% share in 2025, while Asia-Pacific is tracking the highest regional CAGR at 17.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Auto-Injectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of biologic drugs requiring self-injection | +4.2% | Global, concentrated in North America and EU | Long term (≥ 4 years) |

| Rising incidence of chronic autoimmune diseases | +3.8% | Global, highest in developed markets | Medium term (2-4 years) |

| Shift to home-based care/self-administration | +3.1% | North America and EU primary, APAC emerging | Medium term (2-4 years) |

| Connectivity and adherence-analytics integration | +2.4% | North America and EU core, selective APAC uptake | Long term (≥ 4 years) |

| Government stock-piling of epinephrine devices | +1.8% | North America primary, EU secondary | Short term (≤ 2 years) |

| Expansion of micro-needle, needle-free platforms | +1.3% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth Of Biologic Drugs Requiring Self-Injection

Large-volume subcutaneous biologics already account for close to 15% of all biopharmaceuticals and their share is climbing. Manufacturers are increasingly re-formulating intravenous therapies as self-injectable options to relieve infusion-center congestion, demonstrated by the 2025 approval of a self-injection version of Vyvgart Hytrulo. Autoimmune regimens built around B-cell-targeting biologics show similar transitions that place precision delivery demands on devices. High viscosity and varied dose volumes are steering engineers toward tighter tolerances, advanced materials and intuitive user interfaces. The result is a pipeline of sophisticated platforms that favour the auto-injectors market over traditional syringes.[1]Jakob Lange, “Navigating large-volume subcutaneous injections of biopharmaceuticals: a systematic review of clinical pipelines and approved products,” mAbs, tandfonline.com

Rising Incidence Of Chronic Autoimmune Diseases

Enhanced diagnostic capabilities and ageing populations are pushing autoimmune prevalence upward, reinforcing steady device uptake. World Health Organization data links unsafe care to millions of deaths, underscoring the value of reliable self-administration solutions. In multiple sclerosis therapy, 70% of patients rate the latest RebiSmart model as appealing, and almost 90% of specialist nurses call it very good or excellent. Wider biosimilar availability – now offered at up to 65% discounts – also expands access. Yet adherence gaps persist, with research showing that 41% of adrenal-insufficiency patients cannot self-inject during crises, so simplified design and structured training remain priorities.[2]World Health Organization, “Global Patient Safety Report 2024,” iris.who.int

Shift To Home-Based Care/Self-Administration

Payment reforms and supportive technology are actively moving treatment into living rooms. Medicare’s 2.7% 2025 rate boost for home-health agencies pairs with policies obliging providers to evaluate patient readiness for self-care. Artificial-intelligence-driven analytics in diabetes care demonstrate predictive accuracy in hypoglycaemia alerts, broadening confidence in at-home management. Devices such as the enFuse on-body system illustrate adoption speed, with 60% of eligible users switching within four months. Financial enablers like the USD 35 insulin cap in Part B and Part D further remove barriers, positioning home care as the centre of growth for the auto-injectors market.[3]Centers for Medicare & Medicaid Services, “Medicare Program; CY 2025 Home Health PPS Rate Update,” federalregister.gov

Connectivity & Adherence-Analytics Integration

Connected platforms now deliver real-time dosing data, transforming adherence measurement from recall based to objective. The BD Evolve on-body injector features programmable delivery plus audible and visual cues that confirm completion. Cross-indication electronic aids are appearing, leveraging shared functionality to maximise scale economies. Cybersecurity threats are a growing concern because healthcare IoT holds sensitive data, prompting layered defences that combine encryption, strict access controls and frequent penetration tests. Regulatory authorities are also stepping in, with the EMA mandating detailed life-cycle and labelling protocols for smart drug-device combinations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient preference for alternative drug-delivery modes | -2.1% | Global, higher in needle-phobic populations | Medium term (2-4 years) |

| Stringent combination-device regulatory pathways | -1.8% | EU and North America primary, emerging markets secondary | Long term (≥ 4 years) |

| Supply-chain fragility for specialty plastics & springs | -1.4% | Global, concentration risk in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Cyber-security & data-privacy concerns in smart devices | -0.9% | North America and EU primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patient Preference For Alternative Drug-Delivery Modes

Needle anxiety continues to deter certain users, fuelling demand for nasal, oral or microneedle solutions. ARS Pharmaceuticals booked USD 7.8 million in Q1 2025 sales of neffy after only a few months on the market, with over 5,000 prescriptions written. Capital inflows into dissolvable microarray start-ups confirm investors see lasting potential in needle-free formats. The challenge is achieving pharmacokinetic parity across indications, and emergency settings require especially clear patient instructions. Notably, 99% of subjects in SIMLANDI trials found the device easy to use, which suggests user-centred design can mitigate needle aversion.

Stringent Combination-Device Regulatory Pathways

Drug-device products face layered oversight that can prolong approval timelines. The EMA now requests conformity evidence against General Safety and Performance Requirements under Article 117, increasing documentation workload. In the United States, some interchangeable biosimilars have gained clearance without new clinical trials, yet novel mechanisms still endure lengthy validation cycles. Smaller firms often lack the resources to address divergent global rules, which can delay launches by up to 18 months. Industry proposals call for risk-based approaches to balance patient safety with innovation cadence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Autoimmune Dominance Faces Emergency Treatment Disruption

Rheumatoid arthritis retained 35.78% of the auto-injectors market share in 2025 on the back of mature biologic protocols and well-established self-injection routines. Conversely, anaphylaxis is the quickest climber, advancing at 18.63% CAGR to 2031 as food allergy diagnoses rise and school-stock mandates spread. Multiple sclerosis treatments continue to benefit from device upgrades such as RebiSmart 3.0, which 70% of patients find appealing. Diabetes-related use is changing through artificial-intelligence-enabled predictive analytics that support tighter glucose control. Migraine, psoriasis and cardiovascular indications round out the therapeutic spread, each commanding custom engineering from single-dose simplicity to large-volume precision.

Patient expectations now extend beyond reliable drug delivery to encompass connectivity, discretion and minimal pain. Emergency products must remain intuitive under stress, while chronic-disease devices gain traction when adherence data integrate seamlessly with digital health portals. These differing priorities encourage platform diversification and sustain innovation activity across the auto-injectors market.

By Usability/Type: Smart Connectivity Disrupts Traditional Disposable Dominance

Disposable units still generated 68.77% of revenue in 2025 because of convenience and proven manufacturing economies. Connected smart formats, however, are soaring at a 19.61% CAGR to 2031 as payers recognise the clinical and economic value of validated adherence. Nine in ten payers now agree that connectivity closes therapeutic gaps, and more than four in five are open to modest price premiums. Re-usable devices keep a foothold in cost-sensitive settings and for drugs that need flexible dosing, yet infection-control protocols increasingly favour single-use disposables.

Adoption remains gated by data-security obligations and clinician workflow integration. Even so, iterative firmware upgrades and user-experience refinements are resolving early-generation shortcomings. This dynamic positions smart platforms as a core growth driver for the auto-injectors market and a differentiator for entrants seeking to bypass incumbent scale advantages.

By Device Technology: Wearable Innovation Challenges Spring-Loaded Incumbency

Spring-loaded mechanisms accounted for 61.65% of 2025 sales, reflecting decades of optimisation that deliver consistent performance at low cost. Wearable on-body injectors now register the highest growth at 17.98% CAGR, propelled by biologics that require 5 mL to 20 mL volumes and patient desire for discrete, needle-concealed dosing. Early commercial data from the enFuse platform highlight strong user acceptance. Gas-propelled and electromechanical systems serve smaller but critical niches where viscosity or precision necessitates additional force control, while microneedle patches are carving out vaccine and dermatology opportunities.

Component availability is a decisive success factor. Mature spring suppliers and polymer converters provide predictable lead times, whereas newer electromechanical assemblies face longer qualification cycles. Firms capable of vertically integrating or building multi-sourced supply networks are better placed to protect continuity and scale production in the auto-injectors market.

By Route of Administration: Subcutaneous Supremacy Enables Intradermal Innovation

Subcutaneous delivery retained an 83.66% share in 2025 as it balances absorption, comfort and broad clinical applicability across autoimmune, metabolic and oncology indications. Intradermal routes are expanding at 17.29% CAGR, buoyed by heightened interest in dose-sparring vaccines and skin-targeted immunotherapies. Intramuscular dosing preserves relevance for emergency epinephrine, though nasal-spray alternatives signal looming disruption.

Route choice influences every element of device architecture from needle gauge to injection speed. Subcutaneous biologics favour silicone-oil-free barrels and controlled glide enhancements, whereas intradermal systems need exact penetration depth to leverage cutaneous immune response. Companies that tailor micro-engineering to these nuances are well positioned to sustain share in the auto-injectors market.

By End-User: Home Care Ascendancy Reshapes Healthcare Delivery

Home-care environments captured 52.91% of global revenue in 2025, cemented by Medicare’s expanded reimbursement for self-administered biologics. Ambulatory surgical centres are pacing fastest at 17.22% CAGR as payers channel elective procedures away from hospitals. Clinics remain essential for initiation and training but their relative share is ebbing as device simplicity improves.

Remote-monitoring algorithms further enable decentralised therapy by flagging anomalies in adherence or physiologic markers, allowing timely interventions without clinic visits. Health-system cost pressures and patient convenience preferences underpin a structural rise in home-based management, reinforcing sustained demand for reliable self-injection devices across the auto-injectors market.

Geography Analysis

North America led the auto-injectors market with 43.88% share in 2025, thanks to mature reimbursement frameworks, strong biologics pipelines and proactive emergency-preparedness programs. Recent capacity expansions, including a USD 4.1 billion facility in North Carolina and parallel projects by other majors, reinforce supply for regional demand. The Health Resources Priorities and Allocations System also guarantees allocation priority during crises, providing an additional safety net for public health. Still, the FDA’s warning letter to BD reminds stakeholders that quality-system diligence is non-negotiable.

Asia-Pacific is the fastest-growing region, advancing at 17.74% CAGR through 2031. Regulatory harmonisation initiatives are easing cross-border submissions, and governments are investing heavily in healthcare infrastructure. Japan exhibits strong emergency-anaphylaxis adoption yet low school-administration rates signal latent upside. China’s evolving innovation framework and India’s cost-efficient manufacturing expand the regional value chain. Demographic shifts toward higher chronic-disease incidence present a durable demand base that is converting into tangible device volumes for the auto-injectors market.

Europe records steady growth underpinned by clear EMA guidance on drug-device combinations and receptive biosimilar policies that compress treatment costs. Recent approvals of nasal epinephrine and continued capital outlays for medical-system production bolster supply security. Article 117 conformity requirements elevate compliance workloads, but industry stakeholders view the long-term payoff as greater patient confidence. Taken together, these dynamics position Europe as a stable, innovation-friendly arena within the global auto-injectors market.

Competitive Landscape

The auto-injectors industry shows moderate consolidation, with competition migrating from price to platform capabilities. A pending USD 16.5 billion acquisition will bind fill-finish capacity directly to a leading diabetes franchise, signalling deeper vertical integration. BD is pouring USD 10 million into domestic safety-engineered injection capacity, widening its moat in a category that still favours scale.

Collaborative networks are another hallmark. Ypsomed’s long-running alliances with more than 15 glass and elastomer suppliers support over 150 active projects, giving partners turnkey access to validated component ecosystems. Emerging disruptors such as ARS Pharmaceuticals and Micron Biomedical leverage single-product focus to accelerate novel formats, while wearable-specialist Enable Injections claims early leadership in large-volume delivery.

Regulatory acumen and manufacturing quality are the twin pillars of sustainable advantage. FDA guidance that spotlights critical-quality attributes pushes firms with robust validation toolkits to the front of tender lists. Simultaneously, cyber-risk management differentiates connected-device contenders, as hospital IT teams demand hardware that integrates smoothly with security frameworks. These forces collectively shape a landscape where both incumbents and challengers must marry engineering excellence with compliance fluency to expand share in the auto-injectors market.

Auto-Injectors Industry Leaders

Ypsomed

Abbvie

Amgen

Teva Pharmaceuticals

Biogen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The FDA cleared GSK’s 200 mg/mL Benlysta autoinjector for paediatric lupus nephritis.

- May 2025: The FDA approved Amneal’s Brekiya, the first DHE autoinjector for acute migraine and cluster headaches.

- May 2025: Sandoz launched Pyzchiva (ustekinumab) autoinjector across Europe.

- January 2025: The FDA accepted Eisai’s BLA for Leqembi subcutaneous autoinjector for weekly maintenance dosing in early-stage Alzheimer’s disease.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the auto-injectors market as revenue from purpose-built spring or gas-powered devices that deliver a pre-measured dose of prescription medication by subcutaneous, intramuscular, or intradermal routes without manual plunger depression. It captures disposable, reusable, and smart formats supplied empty or prefilled to biopharma partners and directly to providers or patients.

Scope Exclusion: We exclude pen injectors, conventional syringes, jet injectors, and bulk drug sales, so the device baseline is not overstated.

Segmentation Overview

- By Application

- Rheumatoid Arthritis

- Multiple Sclerosis

- Anaphylaxis

- Diabetes

- Migraine

- Psoriasis

- Cardiovascular Diseases

- Others

- By Usability / Type

- Disposable Auto-Injectors

- Re-usable Auto-Injectors

- Connected / Smart Auto-Injectors

- By Device Technology

- Spring-Loaded

- Gas-Propelled

- Electromechanical

- Needle-Free / Micro-Needle

- Wearable On-Body Injectors

- By Route of Administration

- Subcutaneous

- Intramuscular

- Intradermal

- By End-User

- Home-Care Settings

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed device engineers, biologic drug product managers, hospital pharmacy directors, and patient advocacy nurses across North America, Europe, and Asia. These conversations helped us verify ASP ranges, home use adoption, and likely regulatory timing, allowing us to close gaps left by desk sources and triangulate assumptions.

Desk Research

We collected publicly available data from sources such as the U.S. FDA 510(k) and PMA listings, Eudamed notices, the CDC National Diabetes Statistics System, EFPIA production reports, and UN Comtrade trade volumes, which clarified device approvals, chronic disease pools, and regional import values. Company 10-Ks, investor decks, and association white papers (Injectable Drug Delivery Alliance and Arthritis Foundation) revealed average selling prices and unit shipments. Paid platforms including D&B Hoovers for financial splits and Dow Jones Factiva for news helped gauge competitive moves. This list is illustrative, and there are many other references that informed validation and context.

Market-Sizing & Forecasting

We build a top-down demand pool from treated patient volumes for rheumatoid arthritis, multiple sclerosis, anaphylaxis, and diabetes, and then sense-check it through selective bottom-up roll-ups of supplier revenue and sampled ASP multiplied by units. Chronic disease prevalence, annual biologic launches, device ASP progression, home self-administration penetration, and regulatory approval counts feed a multivariate regression that extends forecasts to 2030. Where bottom-up data are patchy, regional penetration proxies agreed during expert calls bridge the gap.

Data Validation & Update Cycle

Model outputs pass a three-layer review that we've standardized across studies and include automated variance scans, senior analyst peer checks, and research manager sign-off. Reports refresh every twelve months, with interim adjustments when material events such as landmark approvals occur, ensuring clients always receive the latest baseline.

Why Mordor's Autoinjectors Baseline Commands Reliability

Published estimates diverge because providers mix drug revenue with device sales, apply differing ASP ladders, and refresh on varied cadences.

The comparison shows that by limiting scope to genuine auto injectors, grounding variables in transparent sources, and refreshing annually, Mordor delivers the balanced, defensible baseline decision makers need.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.58 B (2025) | Mordor Intelligence | |

| USD 9.20 B (2024) | Global Consultancy A | Excludes reusable formats and smart variants |

| USD 63.72 B (2024) | Industry Journal B | Includes finished drug revenue alongside devices |

Key Questions Answered in the Report

How big is the Global Auto-Injectors Market?

The Global Auto-Injectors Market size is expected to reach USD 13.42 billion in 2026 and grow at a CAGR of 15.88% to reach USD 28.04 billion by 2031.

What is the current value of the auto-injectors market?

The auto-injectors market size is USD 13.42 billion in 2026.

How fast is the auto-injectors market expected to grow?

It is forecast to expand at a 15.88% CAGR, reaching USD 28.04 billion by 2031.

Which therapeutic area holds the largest share?

Rheumatoid arthritis represents 35.78% of the market in 2025.

Which region is growing the quickest?

Asia-Pacific is projected to post the highest regional CAGR at 17.74% through 2031.

What technology segment is gaining the most traction?

Wearable on-body injectors are the fastest-growing device technology, rising at 17.98% CAGR.

How are smart auto-injectors influencing payer decisions?

Nine in ten payers believe connected devices fulfil unmet needs and most are willing to pay premiums for adherence data that help improve outcomes.

Page last updated on: