Transfer Case Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

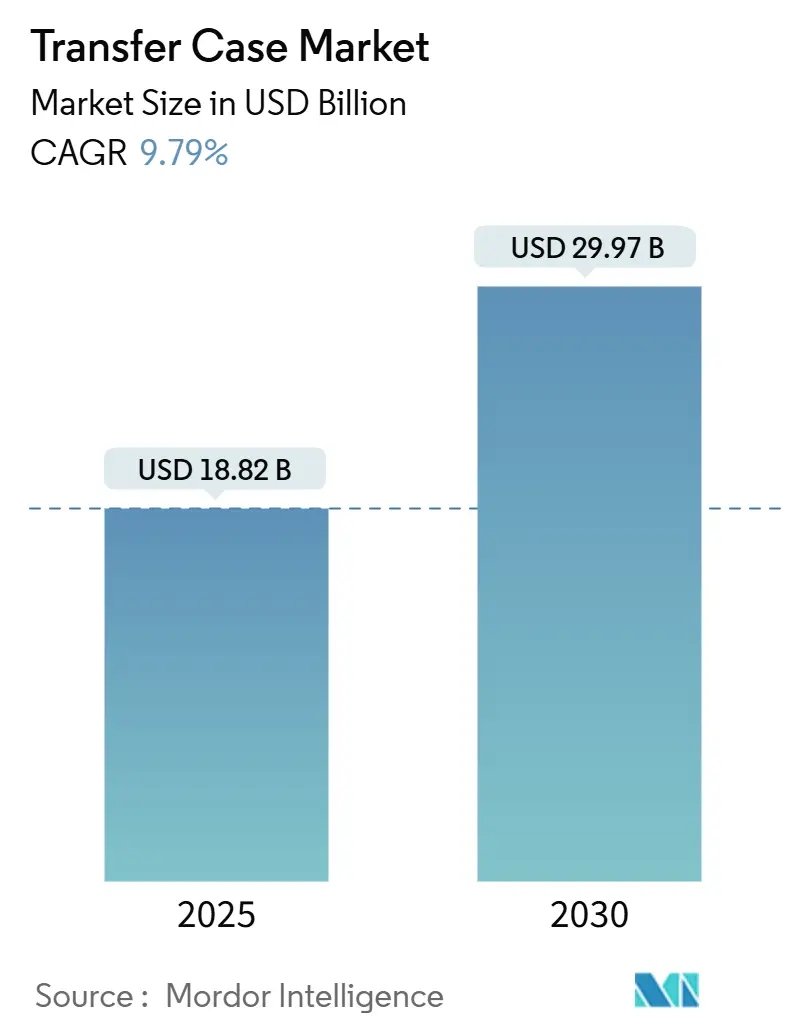

| Market Size (2025) | USD 18.82 Billion |

| Market Size (2030) | USD 29.97 Billion |

| Growth Rate (2025 - 2030) | 9.79% CAGR |

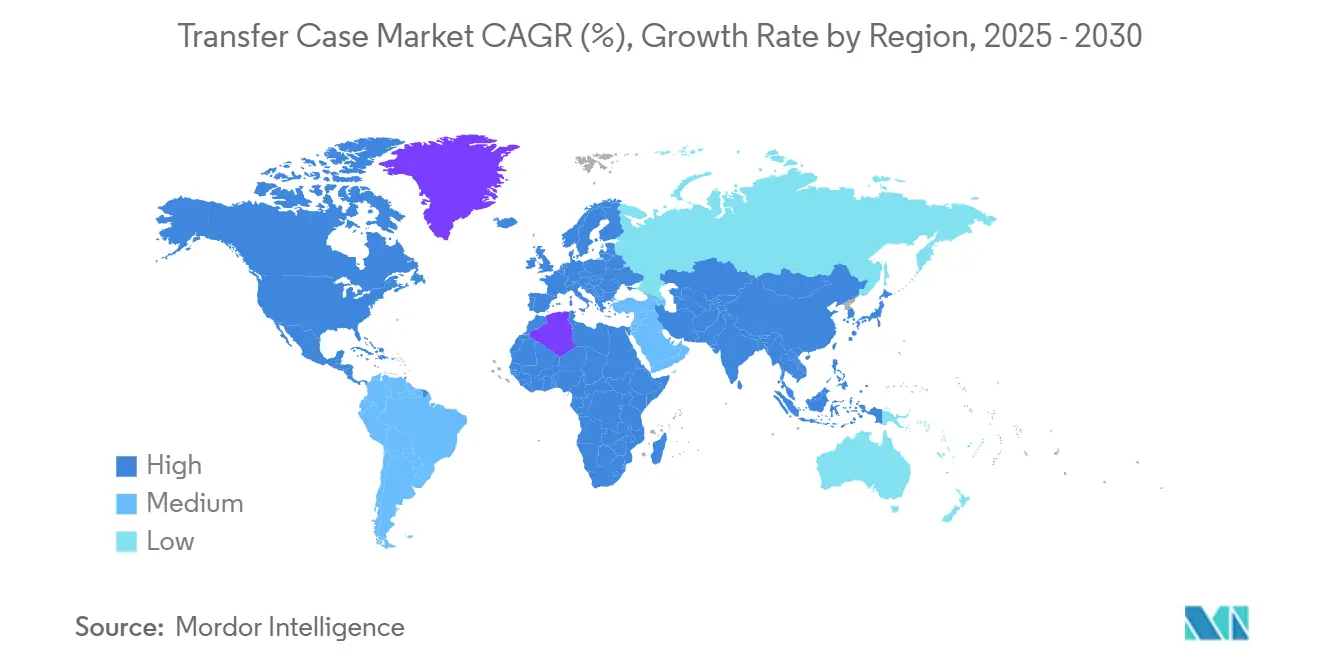

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Transfer Case Market Analysis by Mordor Intelligence

The transfer case market size reached USD 18.82 billion in 2025 and is projected to rise to USD 29.97 billion by 2030, expanding at a 9.79% CAGR during the forecast period. Strong demand for sophisticated AWD and 4WD systems in SUVs, pickup trucks, and light commercial vehicles is accelerating revenue, while OEMs focus on fuel-efficient driveline architectures and predictive maintenance technology sustains long-term growth. Chain-driven designs still account for the bulk of installations, yet gear-driven variants are posting the quickest volume gains as fleets demand higher durability. ESOF adoption is rising sharply because electronic controls integrate seamlessly with vehicle stability programs and enable data-rich telematics services. Disconnectable AWD, lubrication-monitoring sensors, and PHEV-friendly auxiliary transfer cases are opening new value pools for suppliers. Regionally, Asia-Pacific leads both output and unit demand, whereas the Middle East and Africa post the steepest growth as infrastructure spending, SUV penetration, and electrification initiatives converge.

Key Report Takeaways

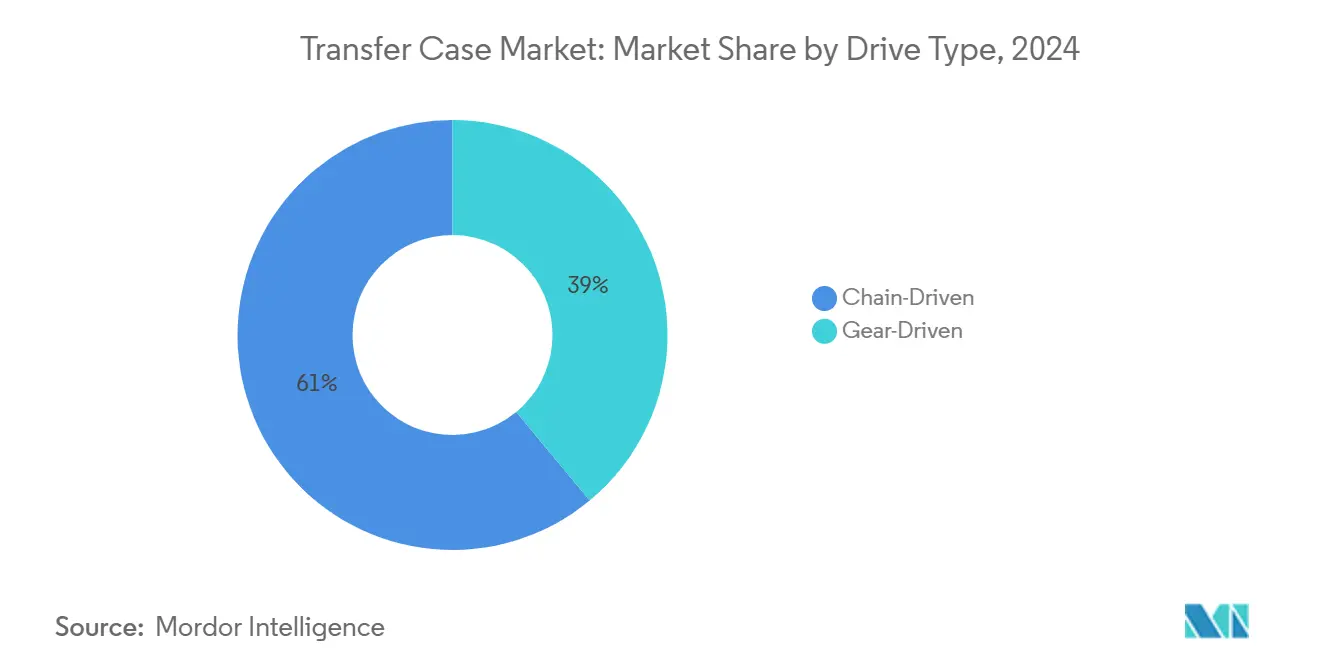

- By drive type, chain-driven systems held 61.01% revenue share of the transfer case market in 2024, while gear-driven systems are forecast to grow at an 8.41% CAGR through 2030.

- By shift type, ESOF units commanded a 68.41% share of the transfer case market in 2024 and are projected to expand at a 7.93% CAGR to 2030.

- By 4WD type, AWD configurations captured 74.23% share of the transfer case market in 2024 and will advance at a 9.25% CAGR over the forecast period.

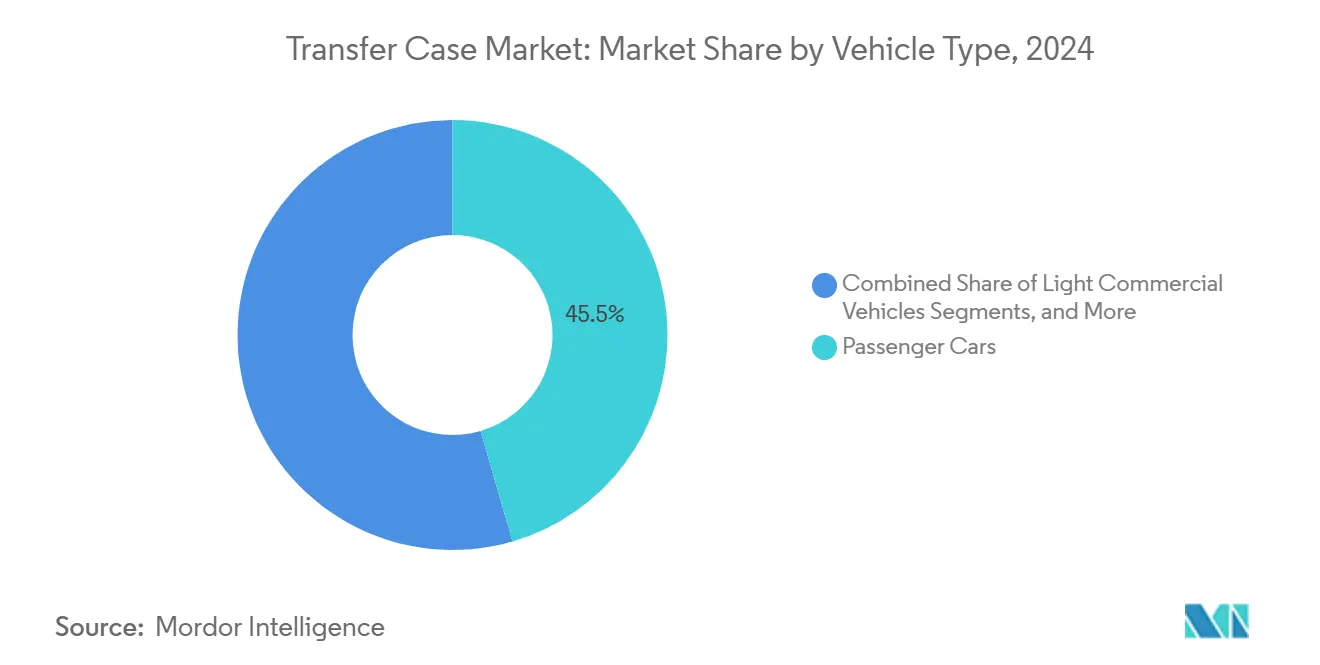

- By vehicle type, passenger cars controlled a 45.51% share of the transfer case market in 2024, whereas light commercial vehicles (LCVs) are set to post the fastest 7.61% CAGR through 2030.

- By sales channel, Original equipment manufacturer (OEM) deliveries represented 82.02% share of the transfer case market in 2024. Yet, the aftermarket is slated to climb at a 6.38% CAGR through 2030, as vehicle age and right-to-repair measures lift replacement demand.

- By geography, Asia-Pacific accounted for a 39.34% share of the transfer case market in 2024; the Middle East and Africa are expected to register a 10.13% CAGR to 2030.

Global Transfer Case Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Demand for SUVs and Pickups | +3.2% | Global, strongest in Asia-Pacific and MEA | Medium Term (2-4 years) |

| Adoption of Advanced ESOF Systems | +2.1% | North America and EU, expanding to Asia-Pacific | Short Term (≤ 2 years) |

| Growth of Off-Highway and LCV Segments | +1.8% | Asia-Pacific core, spill-over to MEA | Long Term (≥ 4 years) |

| Lubrication Sensors for Predictive Maintenance | +1.4% | Global, led by premium OEMs | Medium Term (2-4 years) |

| Push Toward Disconnectable AWD | +0.9% | EU and North America | Short Term (≤ 2 years) |

| PHEV Auxiliary Transfer Cases with E-Axles | +0.5% | Global, incentive-driven PHEV markets | Long Term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for SUVs and Pickup Trucks with 4WD/AWD

Global SUV registrations hit new highs in 2024 and continue to climb, pulling transfer case volumes upward. Automakers are bundling increasingly sophisticated driveline components into high-margin trims to differentiate products and offset commodity cost pressure. Hyundai’s dual-motor hybrid transmission illustrates how OEMs embed transfer case capability inside broader electrified drivetrains, preserving AWD performance while shrinking packaging footprints[1]Deepankar Sadekar, "Hyundai unveils next-generation hybrid powertrain," team-bhp.com. Such integration supports platform flexibility as vehicle lines must accommodate ICE, hybrid, and PHEV configurations.

Increasing Adoption of Advanced Electronic Shift-on-the-Fly Systems

Modern ESOF units contain predictive algorithms that pre-engage AWD using weather feeds, GPS data, and driver behavior analytics, enabling proactive traction management. BorgWarner’s supply deal with SAIC Maxus reflects growing demand for transfer cases that double as data hubs, capturing diagnostics and supporting over-the-air calibration[2]Exro, Canada, “Coil Driver technology for Stellantis’ next-generation electric powertrains", marklines.com. Suppliers monetize this data via software subscriptions that extend beyond hardware sales, turning mechanical components into connected revenue streams.

Growth of Off-Highway and LCV Segments in Emerging Markets

India’s expanding e-commerce networks rely on LCVs capable of tackling mixed-surface routes, which pushes 4WD penetration into sub-3.5-ton classes. Transfer case makers are deploying powder-metallurgy housings that cut weight as much as 15%, boosting payload without sacrificing durability. The strategy balances cost sensitivity with fleet demands for reliability under harsh operating conditions.

OEM Integration of Transfer-Case Lubrication Sensors for Predictive Maintenance

Predictive maintenance integration represents a fundamental shift from reactive to proactive service models, with transfer case lubrication monitoring as an early indicator of broader drivetrain health. Modern sensors can detect oil degradation, contamination levels, and temperature anomalies that precede mechanical failures by thousands of miles. The strategic implication extends beyond maintenance cost reduction—OEMs leverage this data to optimize warranty reserves, adjust service intervals, and identify design improvements for future generations. Fleet operators value these systems for reducing unplanned downtime, creating a premium market segment willing to pay higher initial costs for lower total cost of ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost and Weight Penalty of Mechanical Systems | -2.6% | Global, affecting mass-market segments | Medium Term (2-4 years) |

| BEV Penetration Eliminating Transfer Cases | -2.3% | EU and China lead, NA follows | Long Term (≥ 4 years) |

| Tightening Right-to-Repair Laws Shifting Aftermarket Economics | -0.9% | North America, Europe – growing policy debate | Medium Term (2-4 years) |

| Shortage of Precision Forgings and Powder-Metal Gears | -0.8% | Global, with acute risk in Asia-Pacific supply chains | Short Term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost and Weight Penalty of Mechanical Transfer Cases

Complex gearing and robust casings add 20-30 kg and several hundred USD to vehicle BOMs, constraining adoption in price-sensitive models. Automakers weigh capability benefits against fuel economy and emissions penalties, especially where alternative electronic traction controls can substitute under most driving scenarios. Suppliers respond by downsizing housings and using advanced alloys, yet the trade-off remains a headwind in entry-level segments.

Rapid BEV Penetration Eliminating Conventional Transfer Cases

BEVs with multi-motor layouts split torque electronically, removing the need for a mechanical transfer case altogether. Toyota’s AWD-i places an electric motor on the rear axle, while Rivian’s tri-motor R2 independently vectors wheel torque[3]"AWD-I (R)EVOLUTION OF ALL-WHEEL DRIVE," toyota.pl. Both demonstrate superior traction without added driveline mass. As government incentives and charging infrastructure improve, especially in China and Europe, conventional transfer case demand could erode faster than the sunset of ICE powertrains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: Chain-Driven Dominance Faces Gear-Driven Challenge

Chain-driven designs represented 61.01% of the transfer case market share in 2024, favored for smooth operation and lower cost in passenger vehicles. Gear-driven units, however, are catching up with an 8.41% forecast CAGR as fleets prioritize durability and torque capacity. Higher margins and lower lifecycle costs make gear-driven products attractive to suppliers and commercial operators.

Chain-driven producers respond with upgraded chain metallurgy and optimized lubrication to narrow the durability gap. Yet gear-driven solutions remain the default in heavy-duty and off-highway vehicles. Suppliers seeking growth invest in modular architectures that allow quick swapping between chain and gear sets on a standard housing, giving OEMs flexibility across trim levels.

By Shift Type: ESOF Systems Accelerate Integration

ESOF platforms held a 68.41% share of the transfer case market in 2024 and will outpace MSOF through 2030 as connected vehicle ecosystems scale. The transfer case market size for ESOF units is projected to grow at a CAGR of 7.93% during the forecast period, driven by software-enabled services. Predictive engagement based on telematics data elevates both safety and efficiency, while remote diagnostics cuts warranty costs for OEMs.

MSOF persists in niche off-road and emerging-market applications where electronic architectures are minimal. Yet as right-to-repair laws disseminate diagnostic tools, even cost-sensitive regions are moving toward simpler electronic modules that deliver basic predictive functions without premium price tags. This middle path offers suppliers an entry point into second-tier OEMs.

By 4WD Type: AWD Dominance Reflects Efficiency Mandates

AWD systems captured 74.23% share of the transfer case market in 2024, and their 9.25% CAGR underscores regulatory and consumer tilt toward on-demand traction during the forecast period. Disconnectable AWD lowers parasitic losses, making the layout more fuel-efficient than permanent 4WD.

Traditional 4WD retains footholds in extreme off-road and work-truck segments where full-time capability is mandatory. Yet emerging software-controlled clutch packs are narrowing performance differences, suggesting 4WD’s share will continue to slide in favor of adaptive AWD even in light trucks.

By Vehicle Type: Passenger Cars Lead Despite Commercial Growth

Passenger cars remained the largest revenue generator with 45.51% share of the transfer case market in 2024, buoyed by premium SUV demand in North America, China, and Europe. LCVs post the fastest 7.61% CAGR as e-commerce and infrastructure projects proliferate in India, Southeast Asia, and parts of Africa. The transfer case market share for LCV applications is set to rise several points by 2030, tightening competition among suppliers targeting weight-optimized designs.

Commercial buyers emphasize total cost of ownership, rewarding suppliers that deliver longer service intervals and predictive diagnostics. Passenger-car OEMs, meanwhile, differentiate through smooth NVH characteristics and slick shift strategies integrated with ADAS features.

By Sales Channel: OEM Dominance Faces Aftermarket Resilience

Original Equipment Manufacturers (OEM) fitments accounted for 82.02% share of the transfer case market in 2024, reflecting the deep integration of modern transfer cases with vehicle ECUs. Yet a growing pool of aging SUVs and pickup trucks supports a healthy replacement and performance-upgrade aftermarket. Right-to-repair legislation in the United States and the EU eases access to diagnostic data, enabling independent shops to handle increasingly electronic units and sustaining a 6.38% aftermarket CAGR through 2030.

Electronic complexity still poses tooling and skill barriers for smaller workshops, steering many consumers back to dealer networks. Remanufacturers such as ATC Drivetrain invest in EV component rebuilding to stay relevant as hybrid and PHEV drivelines capture share.

Geography Analysis

Asia-Pacific held a 39.34% share of the transfer case market in 2024, anchored by China’s scale and India’s fast-growing LCV shipments. Regional exports to the Middle East surge as Chinese brands leverage cost advantages to penetrate price-sensitive SUV tiers. India fosters domestic motor production, reducing rare-earth dependence and anchoring local transfer case supply chains.

North America ranks second, driven by high-value pickup and large-SUV models that routinely specify AWD. American Axle’s acquisition of Dowlais Group broadens local content for OEMs seeking dual-path solutions that span ICE and electric drivelines. BEV uptake lags Europe, preserving mechanical transfer case demand over the near term.

Europe combines steady AWD volumes with aggressive emissions targets, pushing refinements such as Haldex electro-hydraulic couplings in transverse layouts and Torsen differentials in longitudinal architectures. The Middle East and Africa clock the fastest 10.13% CAGR as infrastructure expansion, rugged terrain, and rising electrification incentives stoke demand for capable yet efficient AWD systems.

Competitive Landscape

In January 2025, American Axle absorbed Dowlais Group for USD 1.44 billion, forming a USD 12 billion powertrain supplier that spans mechanical and electric drivelines. The deal mirrors a broader shift toward scale and technology breadth as suppliers hedge against BEV disruption. BorgWarner’s collaboration with Stellantis on Coil Driver electronics underlines strategic diversification into power electronics and software.

Market leaders are investing in disconnectable AWD clutches, lubrication-sensor analytics, and e-axle auxiliary transfer cases. Means Industries promotes a hydraulic-free controllable clutch for electric AWD that cuts package size and improves engagement speed. Magna’s eDS Duo partnership with Mercedes-Benz showcases legacy transfer case expertise morphing into electric torque-vectoring roles. New entrants focus on modular, software-defined systems that plug into standardized power electronics stacks, heightening competitive pressure on incumbent mechanical specialists.

Transfer Case Industry Leaders

-

BorgWarner Inc.

-

Magna International Inc.

-

GKN Automotive Ltd.

-

ZF Friedrichshafen AG

-

Aisin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sollers Transmission Production LLC, part of the SOLLERS Group, commenced production of electromechanical transfer cases. These are designed for the Sollers ST6 and ST8 pickups, along with the UAZ Patriot, Pickup, and the all-wheel-drive Profi models.

- February 2025: BorgWarner announced a partnership to supply SAIC Maxus with two cutting-edge transfer cases. These systems enhance vehicle performance and support Maxus's expansion into international markets. One transfer case features mechanical locking for on-demand functionality, while the other, a high-torque model, is optimized for superior off-road performance. Developed and manufactured in China, these advanced systems are scheduled to enter mass production in 2026.

Global Transfer Case Market Report Scope

| Gear-Driven |

| Chain-Driven |

| Manual Shift on the Fly (MSOF) |

| Electronic Shift on the Fly (ESOF) |

| Four-Wheel Drive (4WD) |

| All-Wheel Drive (AWD) |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| Drive Type | Gear-Driven | |

| Chain-Driven | ||

| Shift Type | Manual Shift on the Fly (MSOF) | |

| Electronic Shift on the Fly (ESOF) | ||

| 4WD Type | Four-Wheel Drive (4WD) | |

| All-Wheel Drive (AWD) | ||

| Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the transfer case market in 2025?

The transfer case market size is USD 18.82 billion in 2025.

What is the projected CAGR for transfer cases through 2030?

The market is expected to register a 9.79% CAGR between 2025 and 2030.

Which drive type leads global sales?

Chain-driven transfer cases held 61.01% share in 2024, maintaining leadership in passenger vehicles.

Which region is growing fastest?

The Middle East & Africa is projected to expand at a 10.13% CAGR through 2030.

How are BEVs affecting transfer case demand?

Multi-motor BEV architectures remove mechanical transfer cases, posing a -2.3% drag on forecast CAGR, especially in Europe and China.

Which technology trend offers new revenue streams for suppliers?

ESOF units with predictive algorithms create data-driven service opportunities beyond initial hardware sales.

Page last updated on: