Artificial Kidney Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

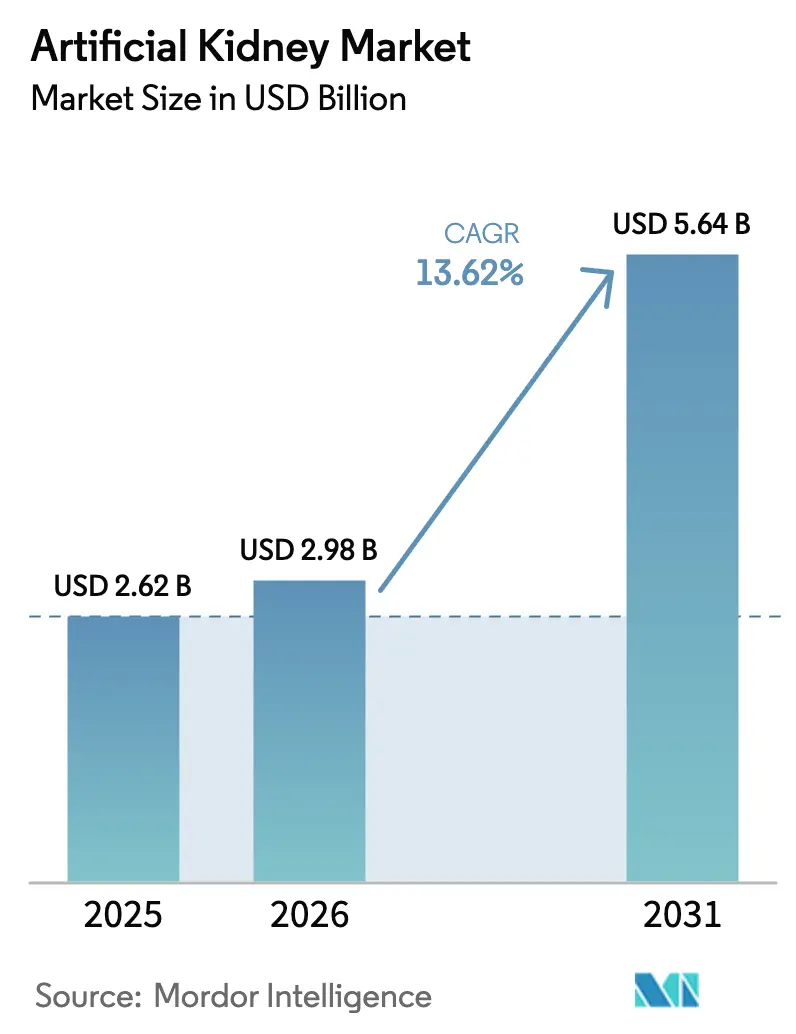

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

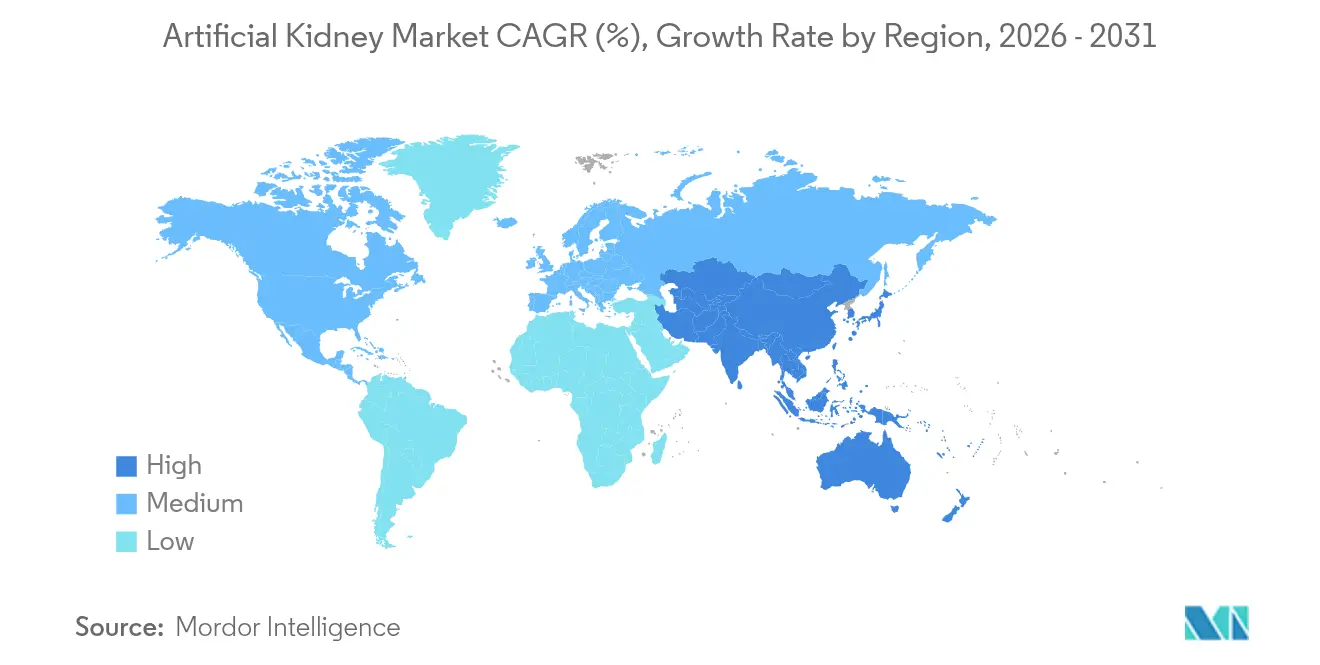

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Kidney Market Analysis by Mordor Intelligence

The artificial kidney market size was valued at USD 2.62 billion in 2025 and estimated to grow from USD 2.98 billion in 2026 to reach USD 5.64 billion by 2031, at a CAGR of 13.62% during the forecast period (2026-2031). Portable hemodialysis systems, bio-artificial implants, and policy support for home therapies steer this expansion. FDA approval for xenotransplantation trials in February 2025 signals official backing for alternative kidney solutions, while Medicare’s higher reimbursement for home dialysis boosts adoption across the United States. Asia-Pacific’s rapid uptake of wearable and portable devices complements North America’s entrenched leadership, and continued venture capital inflows into bio-artificial technologies sustain a vibrant innovation pipeline. Strategic divestitures by large incumbents sharpen competitive focus on high-growth niches within the artificial kidney market.

Key Report Takeaways

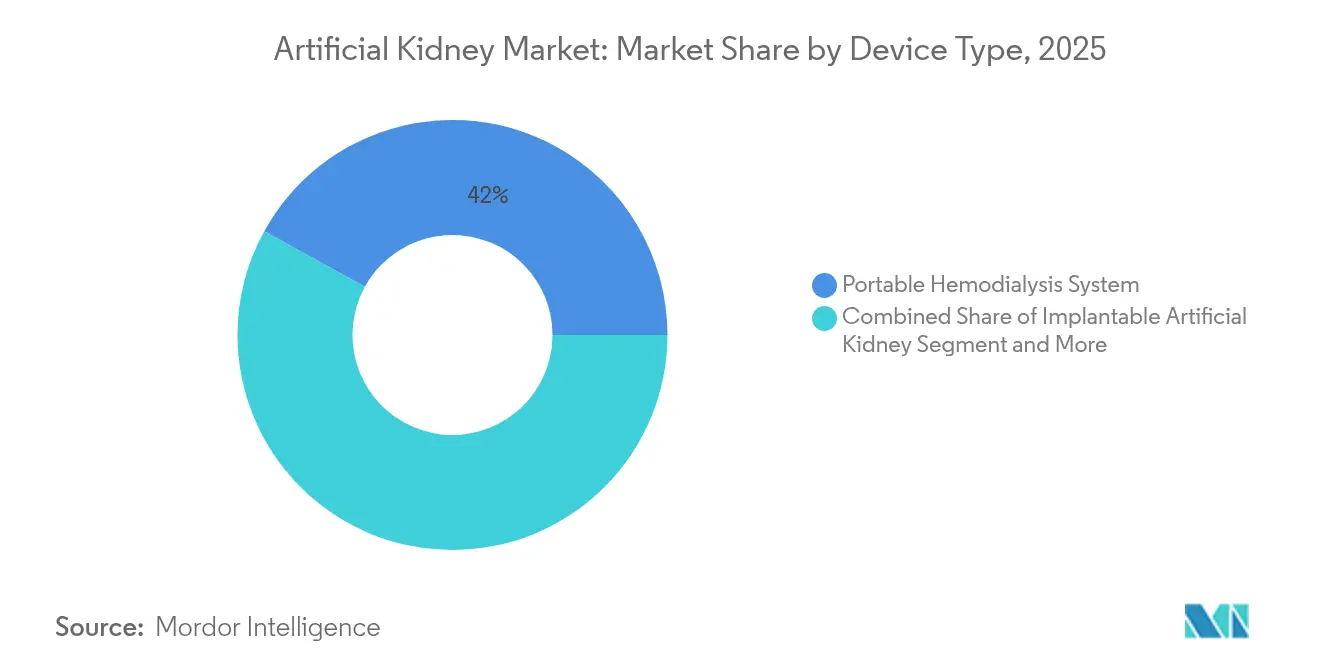

- By device type, portable hemodialysis systems led with 41.98% of artificial kidney market share in 2025, whereas bio-artificial kidneys are on track to expand at 21.58% CAGR to 2031.

- By technology, hemodialysis-based devices held 55.05% revenue share in 2025; sorbent regeneration technology is projected to advance at 16.98% CAGR through 2031.

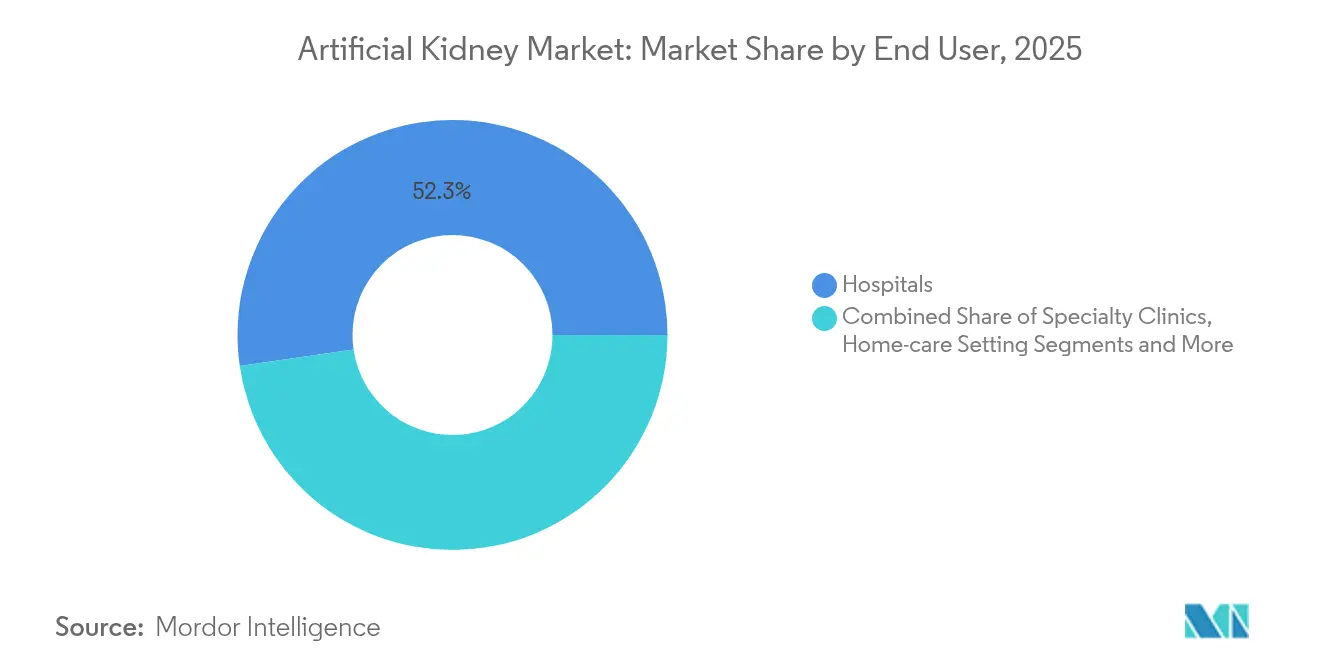

- By end user, hospitals accounted for 52.31% share of the artificial kidney market size in 2025, while home-care settings are growing at 19.65% CAGR between 2026 and 2031.

- By geography, North America dominated with 39.55% share in 2025, but Asia-Pacific is forecast to grow at 18.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Artificial Kidney Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CKD & ESRD prevalence | +3.2% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Scarcity of donor kidneys | +2.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Shift to home & ambulatory dialysis | +2.1% | North America and Europe, widening to Asia-Pacific | Medium term (2-4 years) |

| AI-enabled personalized dialysis dosing | +1.6% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Nano-electrokinetic portable device advances | +1.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Government pay-for-outcomes renal programs | +1.2% | North America, select European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising CKD & ESRD Prevalence

Worldwide chronic kidney disease cases reached 673 million in 2024, with global mortality climbing to 18.29 per 100,000 population[1]Kathleen Otley, “Global, Regional, and National Burden of Chronic Kidney Disease,” BMC Public Health, biomedcentral.com. Diabetes-linked CKD deaths dominate these figures, driving sustained demand for artificial kidney market solutions focused on aging patients. Medicare spent USD 29 billion on hemodialysis in 2024, underscoring the cost pressure on health systems. Asia-Pacific bears the heaviest load, with 450 million people affected and annual therapy costs at USD 23,358 per patient. These epidemiological trends amplify the artificial kidney market’s long-term growth engine and accelerate adoption of portable and implantable alternatives.

Scarcity of Donor Kidneys

Only 21,000 deceased donor kidney transplants occurred in the United States during 2024, leaving more than 92,000 patients on waiting lists. The median transplant waiting time exceeds five years, elevating interest in bio-artificial and xenotransplantation alternatives. FDA clearance for trials using genetically modified pig kidneys in February 2025 signals regulatory momentum that reinforces the artificial kidney market. Global therapy coverage gaps, where only 74% of countries can treat more than half of eligible patients, further widen opportunity for scalable artificial kidney solutions.

Shift to Home & Ambulatory Dialysis

Medicare’s 2025 payment rule raised the base rate to USD 273.82 per home session, extending coverage to acute kidney injury cases. This financial boost elevates the artificial kidney market trajectory by reducing facility dependence. Outset Medical’s TabloCart with prefiltration and Fresenius Medical Care’s next-generation home systems enable patients to treat themselves safely outside clinics. European programs that promote provider incentives and patient education reinforce similar uptake.

AI-Enabled Personalized Dialysis Dosing

Japanese researchers built machine-learning tools that predict CKD progression and dialysis initiation, drawing on nationwide clinical databases[2]Yuko Tanaka, “Development of Artificial Intelligence Systems for Chronic Kidney Disease,” JMA J., jmaj.jp. MediBeacon’s transdermal fluorescence monitoring, approved in China, provides continuous GFR assessment without blood draws. Clinical studies show strong correlations between AI-monitored biomarkers and antibiotic clearance, enabling accurate drug dosing during continuous renal replacement therapy. These advances shorten hospital stays and enhance patient safety, strengthening the artificial kidney market outlook.

Restraints Impact Analysis of Artificial Kidney Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product and procedure costs | -2.4% | Global, most acute in developing markets | Medium term (2-4 years) |

| Device biocompatibility and clotting risks | -1.8% | Global, regulatory focus in North America and Europe | Short term (≤ 2 years) |

| Reimbursement uncertainty for novel devices | -1.6% | North America and Europe | Short term (≤ 2 years) |

| Limited surgical skills for implantables | -1.2% | Global, particularly in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product & Procedure Costs

Private insurers paid USD 10,149 per month for outpatient dialysis in 2024, compared with Medicare’s USD 3,364, revealing significant affordability gaps. Labor shortages and rising material costs threaten rural clinic viability. China may lose USD 558 billion over the coming decade in kidney care expenses. High R&D investment in biocompatible materials and lengthy clinical trials push selling prices higher, limiting early uptake of premium devices in the artificial kidney market.

Device Biocompatibility & Clotting Risks

An FDA draft guidance in October 2024 sharpened chemical-analysis expectations for membrane materials. Polysulfone dialyzers can trigger thrombocytopenia, and complement activation remains a challenge despite new synthetic membranes. These complexities slow regulatory approvals and increase monitoring costs, tempering momentum within the artificial kidney market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Artificial Kidney Market Segment Analysis

By Device Type:

Rapid Innovation in Bio-Artificial SystemsBio-artificial kidneys post a 21.58% CAGR through 2031, the fastest expansion within the artificial kidney market. The KidneyX-backed implant from the University of California San Francisco integrates silicon nanopore filters with living renal tubule cells, promising complete autonomy from external power sources. Portable hemodialysis units, such as Quanta’s SC+, maintain 41.98% revenue leadership in 2025 after securing FDA clearance.

Implantable designs under investigation at UCLA Health employ nanocellulose ultrafiltration and electrodeionization to eliminate dialysate. The artificial kidney market size for implantables is projected to expand rapidly once pivotal trials demonstrate safety and durability. Wearable concepts, including the belt-worn 11-pound system advanced through FDA expedited pathways, aim to restore patient mobility during therapy.

By Technology:

Sorbent Regeneration Improves EfficiencySorbent regeneration devices grow at 16.98% CAGR, outpacing other modalities due to their ability to recycle dialysate with minimal water. Hemodialysis-based machines commanded 55.05% of artificial kidney market size in 2025, powered by Fresenius Medical Care’s 5008X launch, which delivered 23% mortality reduction against standard high-flux therapies.

Nano-electrokinetic ICP innovations from Seoul National University showcase peritoneal dialysis purification without filters, signaling future miniaturization potential. The NEPHRON+ sensor suite complements these advances by introducing real-time fluid analytics. Collectively, these breakthroughs reinforce the artificial kidney market as a hub for multidisciplinary engineering progress.

By End User:

Home-Care Settings Transform Treatment ModelsHome-care settings record 19.65% CAGR through 2031, making them the fastest-growing venue in the artificial kidney market. Policy drivers, such as remote-monitoring reimbursement and virtual training codes in the 2025 Physician Fee Schedule, ease the transition from clinic to living room. Hospitals nonetheless retain 52.31% share in 2025, functioning as hubs for acute care and training.

Specialty clinics deploy Terumo’s Rika platform, now installed at 98 U.S. centers, with management targeting 100 sites by mid-2025. Military hospitals participate in pivotal trials for cytopheretic devices, broadening user diversity. Educational mandates in the Improving Access to Home Dialysis Act ensure patients understand modality choices, accelerating diffusion across the artificial kidney market.

Geography Analysis

North America Artificial Kidney Market

North America holds 39.55% of artificial kidney market share in 2025, supported by robust reimbursement frameworks and multiple FDA breakthrough designations for wearable systems. The ESRD Prospective Payment System set a USD 273.82 per-treatment rate that sustains provider economics. Despite this strength, supply chain shortages of hemodialysis bloodlines in 2025 exposed infrastructure fragility. FTC scrutiny of noncompete clauses may boost talent mobility and device innovation.

APAC Artificial Kidney Market

Asia-Pacific leads growth at 18.05% CAGR through 2031 due to aging populations and rising diabetes prevalence. Chinese approvals for renal denervation and transdermal GFR monitoring speed device availability. Japan’s AI-enabled CKD database improves early detection, supporting earlier therapy initiation. Vantive’s USD 1 billion commitment to digital dialysis underscores private-sector confidence in the region.

Europe Artificial Kidney Market

Europe experiences steady expansion under value-based healthcare mandates. Multinational trials for the Carry Life UF system demonstrate cross-border collaboration on advanced peritoneal dialysis technologies. Policy forums that target home dialysis inequity spur reimbursement reforms, yet variability in provider incentives slows uniform adoption. Harmonized EMA pathways simplify clinical trial administration, benefitting exporters that aim to scale within the artificial kidney market.

Competitive Landscape

Market concentration is moderate as large incumbents restructure portfolios while specialized entrants attract capital. Baxter’s USD 3.8 billion divestiture of its Vantive kidney care business to Carlyle Group created a focused entity with 23,000 staff and dedicated R&D funding. Medtronic and DaVita formed Mozarc Medical to merge engineering and clinical expertise for home therapies.

Academic partnerships challenge incumbents. UCSF’s bio-artificial implant, developed under the KidneyX initiative, exemplifies university–industry collaboration that could leapfrog conventional machines. Venture-backed AWAK Technologies closed a USD 20 million Series B round to fund pivotal trials of a 2-kg peritoneal dialysis device.

Regulatory pressures shape strategy. The FDA’s tighter biocompatibility scrutiny raises R&D costs, favoring firms with strong QMS infrastructure. FTC examination of noncompetes may erode labor retention moats at the largest dialysis chains, enabling start-ups to recruit seasoned engineers and clinicians. Collectively, these forces sustain a dynamic artificial kidney market where cost leadership, clinical evidence, and user convenience dictate competitive advantage.

Artificial Kidney Industry Leaders

B. Braun Melsungen AG

Asahi Kasei Medical Co. Ltd.,

Nikkiso Co., Ltd

Fresenius Medical Care AG & Co. KGaA

Nipro Corporation

- *Disclaimer: Major Players sorted in no particular order

Artificial Kidney Market Companies Covered in this Report

- Fresenius

- Baxter

- Medtronic

- B. Braun

- DaVita

- Nipro

- Nikkiso Co. Ltd.

- Asahi Kasei

- AWAK Technologies

- Outset Medical

- Quanta Dialysis Technologies

- Xcorporeal Inc.

- Nanodialysis BV

- SB-KAWASUMI Laboratories Inc.

- Medica S.p.A.

- Toray Medical Co. Ltd.

- Cantel Medical

- Biolife Medical

- Blood Purification Technologies Inc.

- Diality Inc.

Recent Industry Developments in Artificial Kidney Market

- April 2025: Seoul National University researchers demonstrated a nano-electrokinetic peritoneal dialysis prototype that removed 30% metabolic waste in animal studies.

- August 2024: Diality received FDA 510(k) clearance for its haemodialysis platform, advancing portable treatment options.

- February 2024: Fresenius Medical Care gained FDA clearance for the 5008X Hemodialysis System, introducing high-volume hemodiafiltration therapy in the United States.

Artificial Kidney Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the artificial kidney market as all advanced renal-replacement devices, wearable, portable, or implantable, that filter patients' blood outside a conventional dialysis center and are sold as finished medical equipment worldwide. Mordor Intelligence counts silicon-membrane hemodialyzers, sorbent-regeneration units, and bio-artificial kidneys that integrate living cells with micro-filters.

Scope exclusion: Traditional in-center dialysis consoles, dialysis consumables, and transplant pharmaceuticals lie outside this scope.

Segments Covered in This Report

- By Device Type

- Wearable Artificial Kidney

- Implantable Artificial Kidney

- Portable Hemodialysis System

- Bio-artificial (Cell-seeded) Kidney

- By Technology

- Hemodialysis-based Devices

- Peritoneal Dialysis-based Devices

- Sorbent-based Regeneration Tech

- Nano-electrokinetic ICP Devices

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Home-care Settings

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with nephrologists, biomedical engineers, procurement managers, and patient advocates across North America, Europe, and Asia-Pacific confirm adoption rates, realistic average selling prices, and regulatory milestones, closing gaps left by secondary evidence.

Desk Research

Tier-one public sources such as the World Health Organization, United States Renal Data System, European Renal Association, and UN demographic files provide prevalence, procedure volumes, and population baselines. Regulatory filings, patent portals, and customs data illuminate technology maturity and trade flows.

Analysts then review 10-K filings, investor presentations, clinical journals like Kidney International, and news archived through D&B Hoovers and Dow Jones Factiva to map revenues, pricing corridors, and launch timelines. Numerous additional references beyond those cited inform data collection and clarification.

Market-Sizing & Forecasting

A top-down reconstruction of the end-stage renal disease pool and dialysis penetration, adjusted for device eligibility and replacement cycles, forms the demand core. Results are sense-checked through selective bottom-up triangulation of sampled shipments and quoted ASPs. Key variables include CKD prevalence, reimbursement expansion, home-hemodialysis uptake, approval pipeline, and regional income. Multivariate regression projects these drivers to 2030, while scenario analysis tests breakthrough approval timing. Elasticities from comparable renal devices bridge data voids where bottom-up detail is scarce.

Data Validation & Update Cycle

Outputs undergo variance checks against sales disclosures, clinical trial enrollments, and import statistics; anomalies trigger re-verification. A three-stage peer review precedes publication. Reports refresh annually, with interim updates when major approvals, safety recalls, or currency swings materially affect the baseline.

How Mordor Intelligence's Artificial Kidney Market Size Compares to Other Published Estimates

Published estimates often diverge because publishers vary device inclusion, pricing assumptions, and refresh cadence. Decision-makers face figures that swing widely, stalling strategy.

Gaps typically arise when studies bundle dialysis consumables, mix prototype implants with marketed devices, freeze ASPs, or fix exchange rates for the forecast horizon. Mordor isolates commercial hardware only, updates FX quarterly, and blends regulatory probability with clinician uptake curves, yielding balanced, decision-ready values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.62 Billion (2025) | Mordor Intelligence | |

| USD 10.22 Billion (2024) | Global Consultancy A | Bundles dialysis machines, consumables, and inflation-linked ASP uplift |

| USD 0.41 Billion (2024) | Industry Journal B | Focuses only on implantable prototypes, omits existing portable systems |

The comparison shows that scope breadth and assumption rigor drive large deltas. By anchoring estimates to transparent variables and repeatable checks, Mordor Intelligence delivers the dependable baseline stakeholders require.

Key Questions Answered in the Report

What is the current size of the artificial kidney market?

The market stands at USD 2.98 billion in 2026 and is projected to reach USD 5.64 billion by 2031, reflecting a 13.62% CAGR.

Which device segment grows the fastest?

Bio-artificial kidneys record the highest growth, advancing at 21.58% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

High CKD prevalence, rapid device approvals, and significant private investment drive an 18.05% CAGR for the region.

How do reimbursement reforms affect adoption?

Medicare’s higher payment for home dialysis and expanded telehealth codes lower financial barriers, accelerating home-care uptake.

What are the main challenges facing artificial kidney developers?

High product costs, biocompatibility hurdles, uncertain reimbursement for novel devices, and limited surgical expertise for implantables temper near-term growth.

Page last updated on: