Transplant Box Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

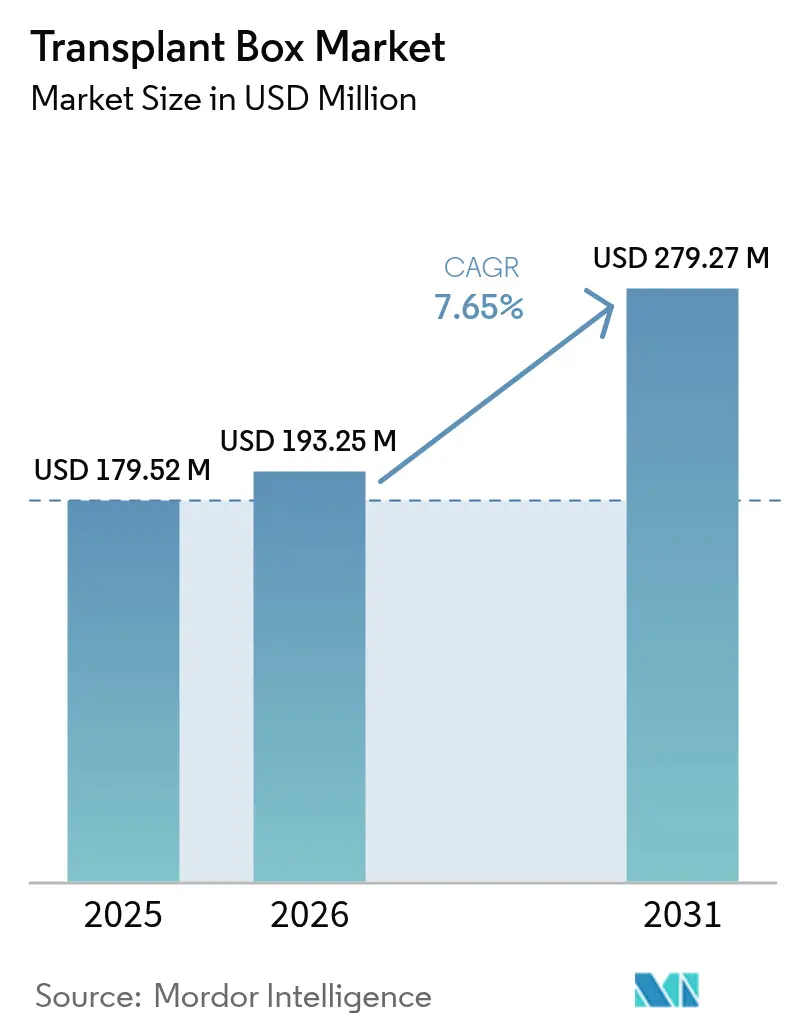

| Market Size (2026) | USD 193.25 Million |

| Market Size (2031) | USD 279.27 Million |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

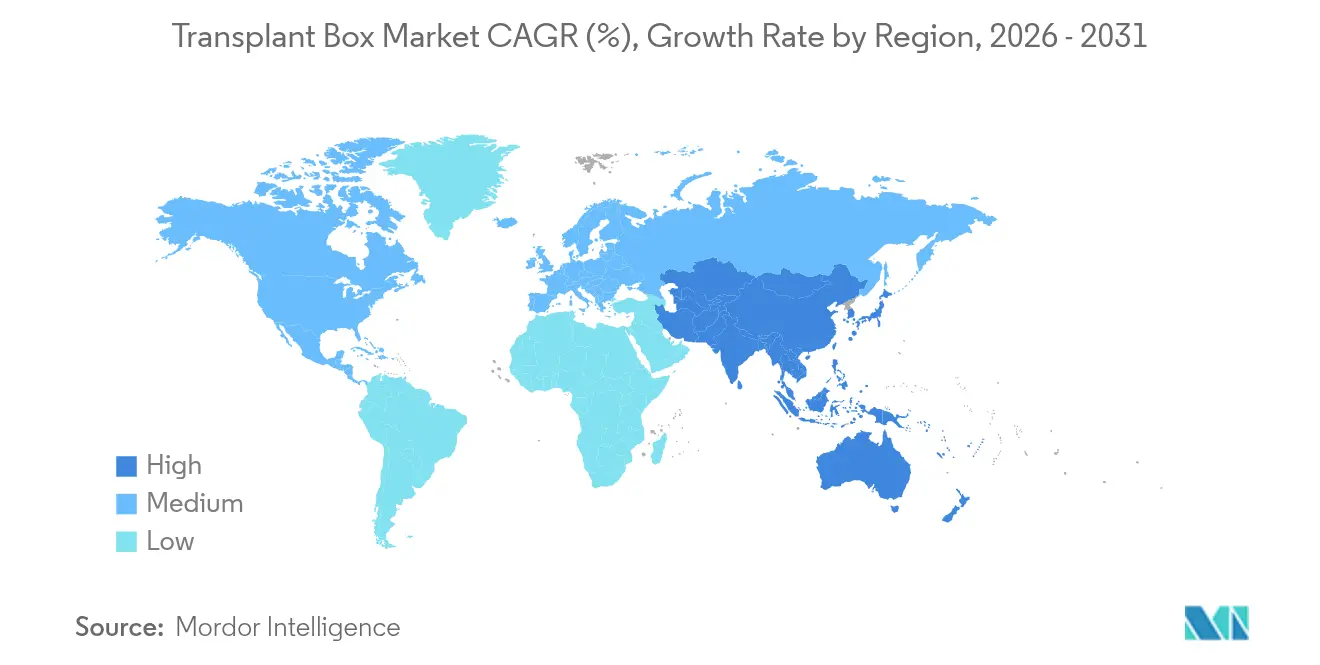

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transplant Box Market Analysis by Mordor Intelligence

Transplant box market size in 2026 is estimated at USD 193.25 million, growing from 2025 value of USD 179.52 million with 2031 projections showing USD 279.27 million, growing at 7.65% CAGR over 2026-2031. Demand scales with global efforts to relieve the persistent organ-shortage gap, where only 10% of transplant requirements are currently met. Rapid substitution of static ice boxes with portable normothermic perfusion devices extends organ viability during transport and allows continuous physiological monitoring, factors that directly underpin volume growth. Military research programs are catalyzing a parallel wave of battlefield-ready solutions with 48-hour resuscitation targets. At the same time, opt-out donor laws, national registry expansions, and rising comorbidities in ageing and diabetic populations create a reliable, long-term demand pipeline. Regulatory multiplicity and shortages of certified cold-chain personnel remain material headwinds, yet ongoing product standardization and automation investments are expected to mitigate these constraints.

Key Report Takeaways

- By geography, North America led with 37.20% of the transplant box market share in 2025 while Asia-Pacific is projected to expand at a 10.42% CAGR through 2031.

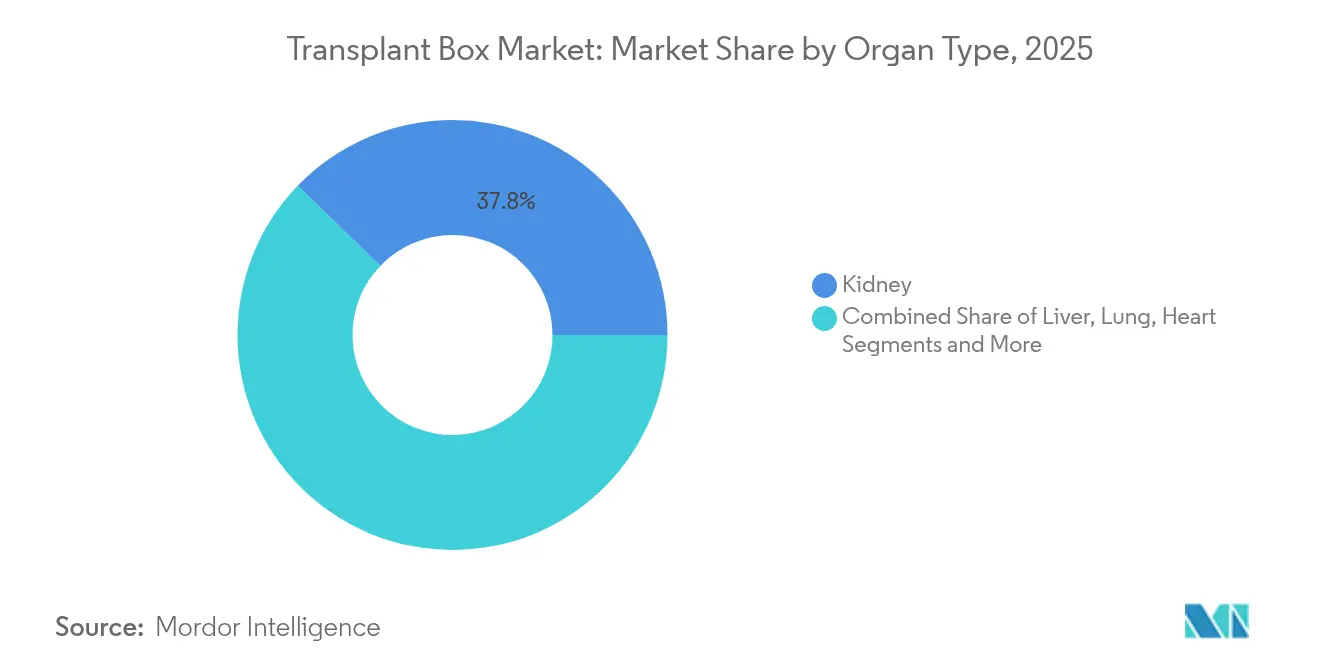

- By organ type, kidney preservation held 37.80% revenue share of the transplant box market in 2025 whereas lung systems are on track for the fastest 11.88% CAGR to 2031.

- By preservation technology, static cold storage retained 53.85% share of the transplant box market in 2025 but normothermic perfusion systems are forecast to register a 16.10% CAGR.

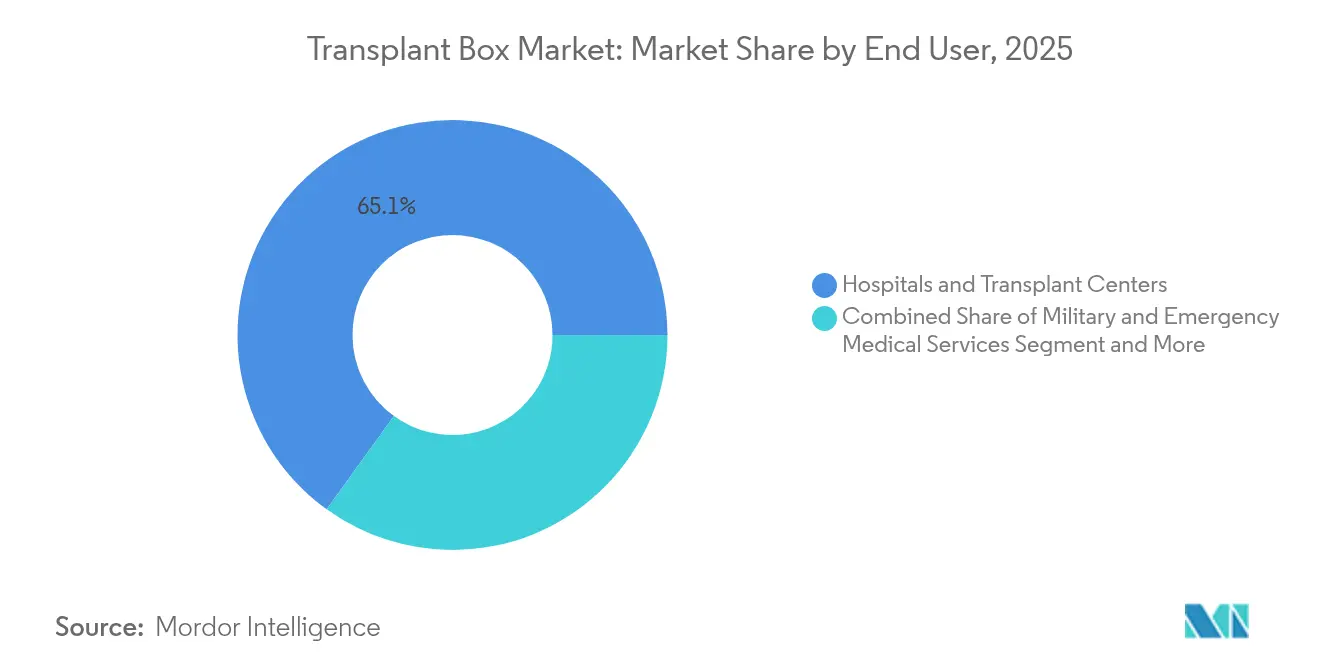

- By end user, hospitals and transplant centers accounted for 65.05% of the transplant box market size in 2025, while military and emergency medical services are poised for a 13.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transplant Box Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing multi-organ transplant volumes in ageing and diabetic populations | +2.1% | North America and Europe anchored, global reach | Long term (≥ 4 years) |

| Government and NGO programs enlarging donor registries | +1.8% | Asia-Pacific and Europe early gains, global scope | Medium term (2-4 years) |

| Shift to portable normothermic perfusion systems | +2.3% | North America and European Union, ripple to Asia-Pacific | Short term (≤ 2 years) |

| Hospital demand for real-time organ analytics | +1.4% | Developed markets worldwide | Medium term (2-4 years) |

| Military-funded R&D for battlefield organ transport | +0.9% | United States primary, NATO allies secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Volume of Multi-Organ Transplants in Ageing and Diabetic Populations

Record organ recovery volumes in 2024 confirm that older and diabetic cohorts are driving sustained procedure growth[3]Association of Organ Procurement Organizations, “U.S. Organ Procurement Organizations Achieve Record Organs Recovered and Transplanted in 2024 Amid Policy Challenges,” aopo.org. Higher prevalence of end-stage renal disease and cardiometabolic complications requires longer preservation windows that static cold storage cannot guarantee. Emerging economies mirrored this rise, highlighting untapped regional demand. Allocation systems now prioritize sicker patients, which often adds inter-state or cross-border travel to procurement logistics. These factors collectively elevate the clinical necessity for advanced devices across the transplant box market.

Government & NGO Programs Expanding Donor Registries

Legislative changes such as Ireland’s opt-out Human Tissue Act 2024, in effect from June 2025, instantly enlarge donor pools. Japan’s coordinator certification framework and India’s expanded brain-death criteria similarly shorten consent cycles and raise utilization rates. The WHO strategy that calls for every member state to meet transplant demand by 2035 institutionalizes this momentum. Expanding donor availability directly lifts shipment volumes and places fresh emphasis on reliable, data-rich preservation hardware.

Shift from Static Cold Storage to Portable Normothermic Perfusion Systems

Clinical evidence proves that normothermic perfusion lowers primary graft dysfunction from 28% to 11% in heart cases, enabling longer journey times without outcome penalties. TransMedics’ Organ Care System illustrated this demand by more than doubling quarterly revenue in 2024. Innovations such as HOPE for lungs allow 20-hour ex-vivo windows, opening donation from distant locations. Early adoption confers measurable competitive advantages and reshapes purchasing criteria across the transplant box market.

Hospital Demand for Real-Time Organ-Condition Analytics

Hospitals increasingly integrate sensor-equipped boxes that deliver continuous pH, lactate, and impedance data, aligning with quality-improvement mandates and malpractice-risk mitigation. The FDA’s qualification plan for the iBox predictive scoring system signals regulatory support for data-driven evaluation. Institutions justify premium pricing when analytics translate into lower readmission and graft-loss rates, reinforcing a technology-led differentiation cycle in the transplant box industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and per-use cost of advanced transplant boxes | -1.7% | Most acute in emerging markets | Short term (≤ 2 years) |

| Complex multi-jurisdictional regulatory clearances | -1.2% | EU–US–Asia corridors | Medium term (2-4 years) |

| Global shortage of qualified cold-chain logistics personnel | -0.8% | Rural and remote regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Per-Use Cost of Advanced Transplant Boxes

Liver transplant expenses rose 10.9% after allocation policy revisions, underscoring the sensitivity of overall costs to logistics inputs. Incremental cost-effectiveness analyses frequently exceed USD 100,000 per quality-adjusted life year, stretching reimbursement thresholds. Consumable kits and single-use cartridges add recurring cost layers that impede broad deployment in mid-tier centers.

Complex Multi-Jurisdictional Regulatory Clearances

The EU SoHO Regulation 2024/1938 introduces new standards while the United States maintains FDA pathways that can span 5,000-plus review days for innovative systems[1]Federal Register, “Determination of Regulatory Review Period for Purposes of Patent Extension; ORGAN CARE SYSTEM HEART,” federalregister.gov. Parallel compliance workstreams inflate development budgets and delay time-to-market, especially for small and mid-size vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organ Type: Kidney Dominance Coupled with Lung-Segment Momentum

Kidney devices contributed 37.80% of the transplant box market in 2025, benefiting from both deceased and living donor programs. Wider acceptance of ABO-incompatible procedures and record 8,200 kidney transplants performed by a single network in 2024 demonstrate deep installed demand. Conversely, lung preservation shows the fastest 11.88% CAGR as ex-vivo perfusion revives marginal grafts, a development that could lift the transplant box market size for pulmonary applications by mid-decade. Heart, liver, and pancreas boxes continue steady uptake, and early-stage work in intestinal and vascular-composite preservation hints at future expansion vectors.

The second growth driver is the widening perimeter of acceptable donor-recipient travel times. Normothermic lung and heart solutions allow 6-20 hour windows without raising ischemia-reperfusion risks, letting clinicians consider intercontinental matches and thereby stimulating regional volume. As transplant registries diversify, organ-specific demand patterns will continue to recalibrate production and R&D allocations across vendors operating in the transplant box market.

By Preservation Technology: Dynamic Platforms Lead Performance Shift

Static cold storage still dominates with 53.85% share owing to simplicity and low price. Nonetheless, clinical data showing a 54% relative decline in four-year cardiac mortality with SherpaPak versus ice drives a decisive perception shift toward dynamic systems. Normothermic platforms post a 16.10% CAGR, propelled by hospital demand for real-time metabolic data and by reimbursement pilots rewarding improved outcomes. Hypothermic perfusion occupies a viable mid-price niche, particularly in liver and kidney procedures where oxygenated perfusion has shown 20-hour preservation capability.

Future technologies such as cryopreservation and vitrification remain at proof-of-concept stage due to toxicity challenges yet represent plausible long-term disruptors. Over the forecast window, however, iterative upgrades that blend closed-loop temperature control, IoT connectivity, and cloud analytics are expected to set the competitive standard in the transplant box market.

By End User: Military Applications Drive Fastest Growth

Hospitals and transplant centers commanded 65.05% of the transplant box market share in 2025, benefiting from mature surgical infrastructure and established reimbursement pathways. More than 20% of U.S. liver transplant centers have adopted advanced containers such as Paragonix’s LIVERguard, underscoring rising clinical confidence in dynamic preservation technology. The spread of donor-care units illustrates a parallel strategy shift; these specialized wards cut organ‐recovery costs by 51% while lifting yields 27.5%. Together, these developments reinforce hospitals as the core customer group even as budgets tighten.

Military and emergency medical services form the fastest-growing end-user category, set to expand at a 13.05% CAGR through 2031. Defense projects prioritize rugged, portable systems capable of sustaining organs alongside blood substitutes, exemplified by DARPA’s USD 46 million ErythroMer program. Field trials with TRV-150 drones show how autonomous delivery can integrate preservation hardware into forward logistics chains. Organ-procurement organizations and research institutes round out demand by validating new platforms and protocols, creating a feedback loop that migrates battlefield innovations into civilian practice and keeps procurement momentum high for the transplant box market.

Geography Analysis

North America retains leadership with 37.20% of global revenue in 2025 owing to robust healthcare infrastructure and rigorous yet navigable regulatory pathways. The United States accounts for the majority of regional sales, supported by sustained double-digit revenue growth reported by leading vendors. Cross-border agreements with Canada and Mexico facilitate broader organ sharing and strengthen procurement logistics, thereby maintaining high device utilization.

Europe follows with sophisticated transplant networks and progressive regulations. The new SoHO rules harmonize technical standards, positioning the bloc for accelerated adoption of dynamic perfusion devices. Countries such as Germany, France, and Spain show notable investment in donor-care units, which increase yields and reduce total costs, thus enhancing device ROI.

Asia-Pacific is the fastest-growing territory, recording a 10.42% CAGR through to 2031. China’s voluntary donation system, Japan’s coordinator certifications, and India’s record transplant volumes collectively generate an expanding customer base. Governments are also funding new transplant centers and procurement hubs, prerequisites for large-scale device deployment. South America, the Middle East, and Africa hold significant latent demand, but limited reimbursement and logistical challenges constrain immediate scale. Gradual infrastructure improvements are likely to unlock incremental opportunities over the second half of the forecast period, incrementally lifting overall transplant box market growth.

Competitive Landscape

The transplant box market is moderately concentrated. TransMedics leads normothermic perfusion with the Organ Care System, more than doubling revenue year-on-year in 2024 and targeting 10,000 annual procedures by 2028 transmedics.com. Getinge’s USD 477 million acquisition of Paragonix adds a diversified portfolio and global distribution muscle getinge.com. Bridge to Life builds a differentiated liver franchise through HOPE perfusion, while XVIVO guards its IP position with an expanding patent estate xvivogroup.com.

Emerging players focus on low-cost, sensor-rich devices tailored to developing markets and on AI-based allocation platforms that integrate seamlessly with perfusion boxes. Military partnerships introduce a parallel commercialization track, moving battlefield-ready prototypes toward civilian trauma and emergency deployment. Early-stage xenotransplantation trials may eventually recast demand fundamentals, yet over the current horizon they primarily reinforce the premium on preservation versatility.

Transplant Box Industry Leaders

Transmedics, Inc

Organ Recovery Systems Inc.

Institut Georges Lopez (IGL)

OrganOx Ltd.

Getinge (Paragonix Technologies, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: OrganOx signs a partnership with ProCure On-Demand to broaden U.S. organ recovery services.

- February 2025: The Northwestern Medicine Canning Thoracic Institute starts routine repair and refrigeration of damaged donor lungs, extending transplant readiness windows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the transplant box market as the global sales of specialized, purpose-built containers, whether passive cold-storage chests or active perfusion devices, that maintain physiologic temperature, sterility, and monitoring of hearts, livers, lungs, kidneys, pancreata, and other solid organs during retrieval to implant transport.

Scope Exclusion: Generic picnic coolers, stand-alone preservation solutions, and third-party courier or air-ambulance services fall outside this market's boundary.

Segmentation Overview

- By Organ Type

- Heart

- Liver

- Lung

- Kidney

- Pancreas

- Others

- By Preservation Technology

- Static Cold Storage Boxes

- Normothermic Machine Perfusion Devices

- Hypothermic Machine Perfusion Devices

- Others

- By End User

- Hospitals & Transplant Centers

- Organ Procurement Organisations (OPOs)

- Military & Emergency Medical Services

- Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

We began by mapping the transplant workflow through open-access sources such as the Global Observatory on Donation & Transplantation, Eurotransplant annual statistics, UNOS/OPTN datasets, national customs codes for HS 901890, peer-reviewed journals in transplantation, and healthcare equipment import alerts. Company 10-Ks and device 510(k) summaries then clarified average selling prices, installed base, and regulatory milestones. Supplementary insight was pulled from D&B Hoovers and Dow Jones Factiva for revenue splits and competitive actions. Trade association releases, hospital procurement tenders, and patent families in Questel helped us benchmark technology diffusion and upcoming product classes. The sources listed above are illustrative; many additional references supported data cross-checks.

Primary Research

Mordor analysts conducted semi-structured interviews with transplant surgeons, procurement organization managers, biomedical engineers, and regional distributors across North America, Europe, and Asia-Pacific to validate utilization rates, failure modes, and price dispersion. These interactions filled data gaps from desk work and confirmed regional weighting before final triangulation.

Market-Sizing & Forecasting

A top-down reconstruction anchored on 2024 transplant volumes, average ischemic time limits, and replacement cycles produced the initial demand pool, which was then stress tested with sampled ASP × unit roll-ups from supplier disclosures. Key variables include annual deceased donor growth, split between cold storage and normothermic devices, regulatory approvals, hospital capital budget trends, and currency movements. Multivariate regression linked these drivers to historical revenue to shape the 2025-2030 forecast; scenario analysis adjusted for policy shocks such as presumed consent legislation. Bottom-up gaps, especially in emerging markets, were patched through shipment-level patterns in Volza and distributor channel checks.

Data Validation & Update Cycle

Outputs pass an anomaly screen, peer review, and senior analyst sign-off. Models refresh yearly, with mid-cycle revisions triggered by device approval bans, reimbursement shifts, or >10% variance in transplant counts; a final sense check precedes every client delivery.

Why Mordor's Transplant Box Baseline Inspires Confidence

Published estimates diverge because firms choose dissimilar organ sets, mix device classes, apply varied ASP curves, or model from different base years.

Key gap drivers include scope, as some add connected IoT logistics or multi-organ carts, currency conversion timing, and refresh cadence; Mordor's page isolates physical boxes only, uses 2024 transplant data as baseline, and updates annually before inflation erodes comparability.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 179.52 M (2025) | Mordor Intelligence | - |

| USD 181.20 M (2025) | Global Consultancy A | Includes smart box telematics and bundled service fees |

| USD 171.50 M (2024) | Regional Consultancy B | Uses earlier base year and blends organ transport accessories |

| USD 168.26 M (2024) | Trade Journal C | Excludes perfusion devices, limiting scope to passive coolers |

Taken together, the comparison shows that while other publishers lean conservative or expansive depending on scope, Mordor's disciplined variable selection and annual refresh provide a balanced, transparent baseline that decision makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the transplant box market in 2026?

The transplant box market stands at USD 193.25 million in 2026.

How fast will the transplant box market grow by 2031?

Revenue is projected to reach USD 279.27 million by 2031, reflecting a 7.65% CAGR.

Which organ segment leads demand for transplant boxes?

Kidney preservation systems hold the largest 37.80% share because kidneys remain the most transplanted solid organ.

What technology trend is reshaping the transplant box industry?

Portable normothermic perfusion devices are displacing static ice boxes, registering a 16.10% CAGR on superior clinical outcomes.

Which region offers the highest growth opportunity?

Asia-Pacific is forecast to grow at a 10.42% CAGR, propelled by expanding donor programs and new transplant centers.

Page last updated on: