Apple Cider Vinegar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

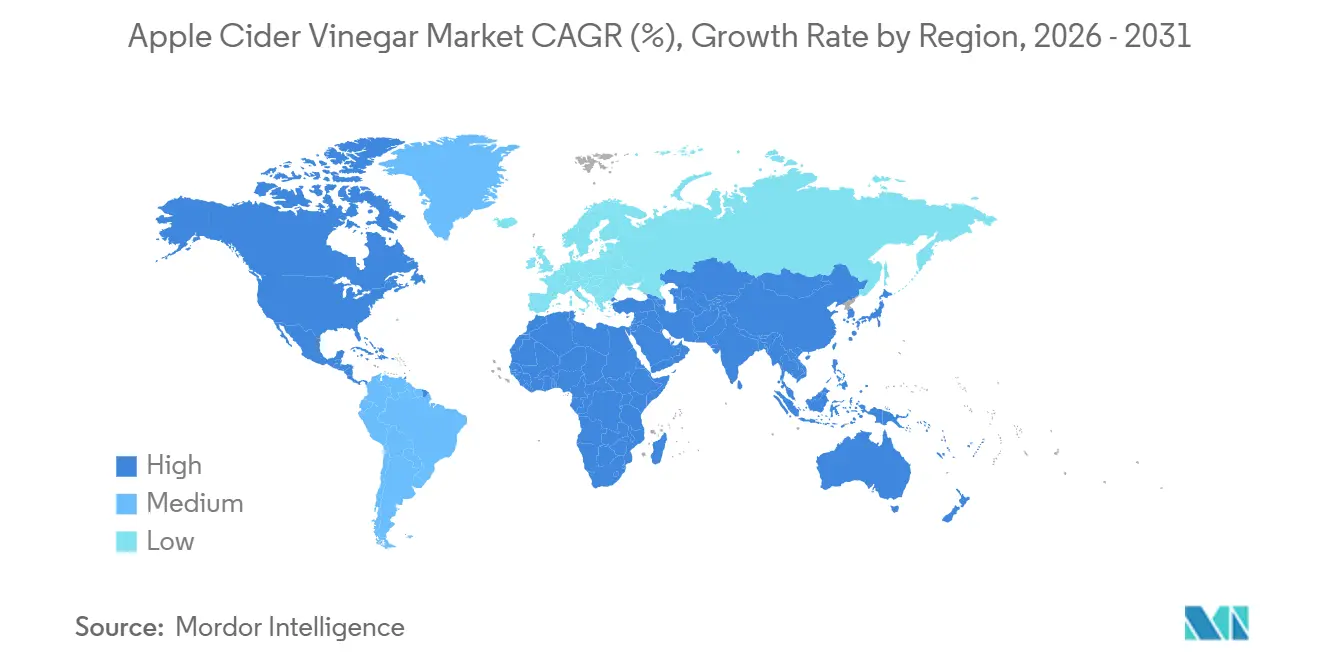

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

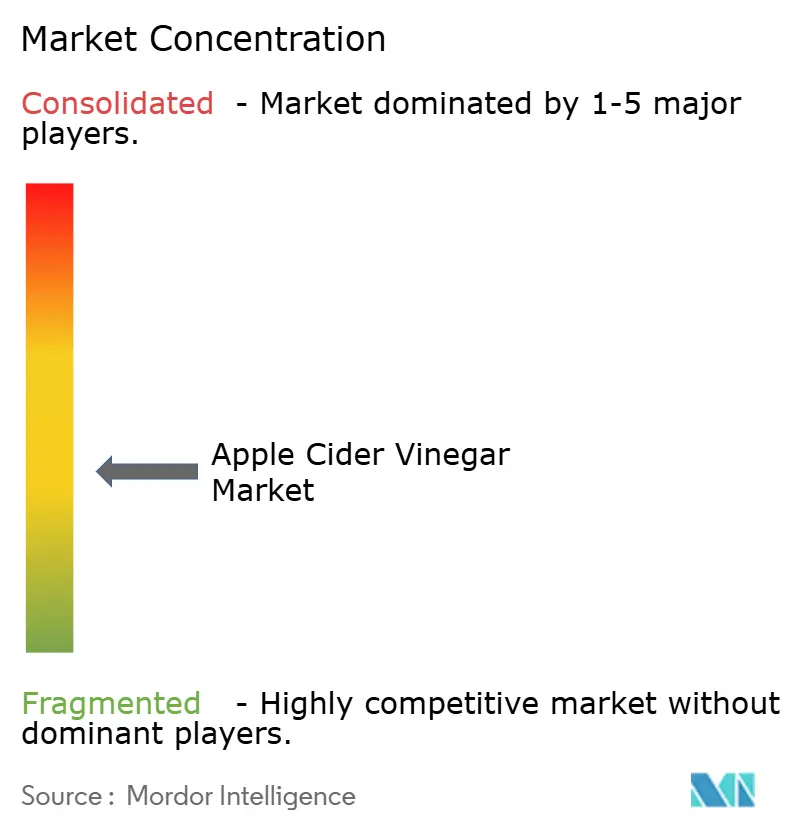

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Apple Cider Vinegar Market Analysis by Mordor Intelligence

The apple cider vinegar market size is expected to grow from USD 1.36 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 2.27 billion by 2031 at 8.78% CAGR over 2026-2031. Continued consumer focus on preventive health, expanding format choices, and rising demand for clean-label products are shifting spending away from reactive pharmaceuticals toward functional pantry items. Liquid products still dominate shelves, yet capsules, tablets, and gummies are expanding the addressable audience by removing taste barriers and aligning with busy lifestyles. Certified-organic SKUs are winning shelf space as the United States Department of Agriculture’s incentives stabilize certified acreage and narrow retail price gaps. Geographic expansion in Asia-Pacific and product diversification into beauty, personal care, and household cleaners cushion growth against a maturing North American segment.

Key Report Takeaways

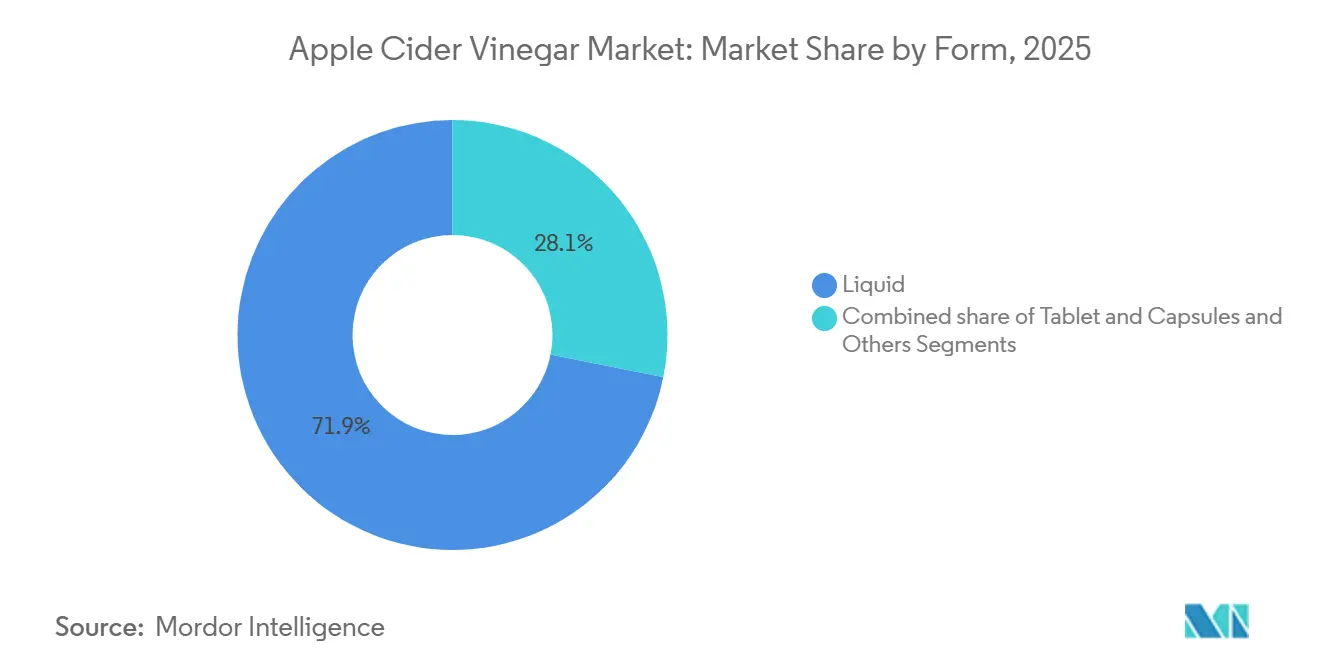

- By form, liquid accounted for 71.87% of revenue in 2025, while capsules and tablets are projected to advance at a 9.61% CAGR through 2031, the highest among all formats.

- By category, conventional products held 67.81% apple cider vinegar market share in 2025, whereas the certified-organic tier is forecast to expand at 9.96% CAGR by 2031.

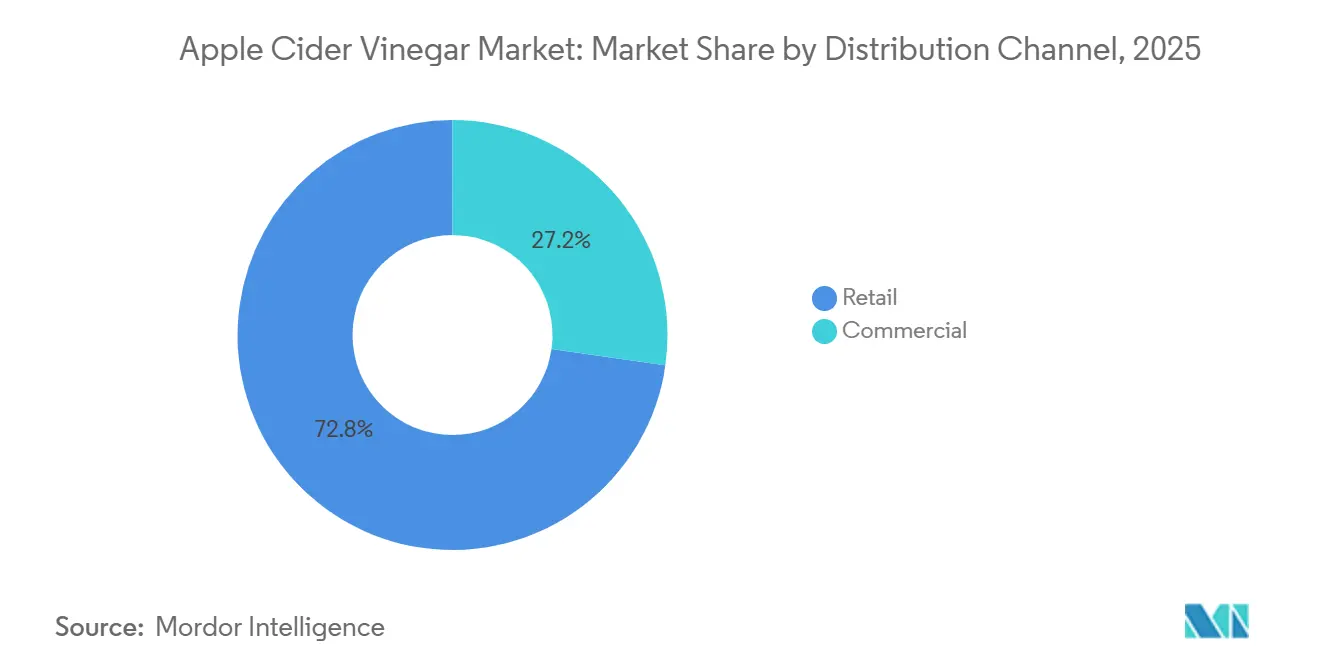

- By distribution channel, retail contributed 72.76% of sales in 2025, but commercial uses, including foodservice and beauty, are growing at a 9.33% CAGR through 2031.

- By geography, North America led with 33.38% of global revenue in 2025, while Asia-Pacific is poised for the fastest CAGR of 10.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Apple Cider Vinegar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on preventive healthcare and functional foods | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expansion of ACV-based product formats | +1.5% | Global, led by North America | Short term (≤ 2 years) |

| Increasing popularity of gut health and microbiome-supporting ingredients | +1.3% | Global, notably North America and Australia | Medium term (2-4 years) |

| Rising demand for natural, organic, and minimally processed products | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Rising incorporation of ACV in beauty, personal care, and household products | +0.9% | North America and Japan | Medium term (2-4 years) |

| Influence of social media wellness trends | +0.8% | Global, highest in digitally connected markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Focus on Preventive Healthcare and Functional Foods

Preventive healthcare spending is reshaping demand for functional ingredients as consumers allocate discretionary income toward products that promise long-term wellness rather than acute symptom relief. The FDA's updated "healthy" nutrient content claim rule, finalized in 2024, now permits manufacturers to highlight specific bioactive compounds, such as acetic acid, on labels, provided they meet revised thresholds for added sugars and sodium, thereby legitimizing ACV's positioning as a functional food rather than a folk remedy[1]Source: U.S. Food and Drug Administration, “Food Labeling: Nutrient Content Claims; Definition of Term ‘Healthy,’” Federal Register, fda.gov. This regulatory clarity has emboldened brands to invest in clinical substantiation, with several filing for qualified health claims related to glycemic response and satiety. The shift is particularly pronounced among consumers aged 25-45 who prioritize ingredient transparency and view ACV as a hedge against metabolic syndrome, a condition affecting over 1 in 3 U.S. adults according to CDC surveillance data. Functional food penetration in emerging markets remains constrained by price sensitivity, but the proliferation of single-serve sachets and diluted ready-to-drink formats is lowering trial barriers in India, Indonesia, and Brazil.

Expansion of ACV-Based Product Formats

Format diversification is decoupling growth from the liquid segment's inherent limitations, taste aversion, portability challenges, and concerns about enamel erosion. Bragg's January 2025 launch of 750-milligram acetic acid capsules at Sprouts Farmers Market exemplifies this pivot, targeting consumers who reject the pungency of liquid while preserving the brand's organic positioning. Gummy formulations, though less prevalent, are gaining traction among younger demographics who associate chewable supplements with lifestyle brands rather than clinical interventions. Tablet and capsule formats are projected to expand at a 9.61% CAGR through 2031, outpacing liquid's 8.5% growth as manufacturers leverage contract encapsulation facilities to scale production without capital-intensive fermentation infrastructure. The format shift also enables premium pricing: per-serving costs for capsules exceed those for liquids by 40-60%, yet conversion rates remain robust due to perceived convenience. This dynamic suggests that brands prioritizing margin over volume will continue fragmenting the category into specialized delivery systems, each optimized for distinct consumption occasions.

Increasing Popularity of Gut Health and Microbiome-Supporting Ingredients

Gut microbiome research has elevated ACV from a niche tonic to a scientifically plausible intervention, even as clinical evidence remains inconclusive for many claims. The ingredient's acetic acid content is hypothesized to modulate gastric pH and short-chain fatty acid production, mechanisms that resonate with consumers familiar with probiotic and prebiotic narratives. While ACV itself does not contain live cultures after pasteurization, brands marketing "with the mother" unpasteurized variants containing acetobacter capitalize on this perception, despite limited peer-reviewed support for efficacy. The FDA has not issued warning letters specifically targeting ACV gut health claims in 2024-2026, suggesting a regulatory gray zone that brands exploit through careful language like "supports digestive wellness" rather than "treats dysbiosis." This ambiguity has attracted both established supplement manufacturers and wellness influencers launching direct-to-consumer brands, intensifying competition for shelf space in the digestive health aisle. The trend is self-reinforcing: as more products enter the market, consumer familiarity grows, which in turn validates further investment in gut-centric positioning.

Influence of Social Media Wellness Trends

Social media platforms, particularly TikTok and Instagram, have amplified ACV's visibility through user-generated content that blurs the line between testimonial and advertising. Influencers promote morning ACV rituals, often pairing the ingredient with lemon juice or honey, generating millions of views and driving search traffic to e-commerce platforms. The Federal Trade Commission has intensified scrutiny of endorsement disclosures in 2024-2025, issuing guidance that requires influencers to clearly label paid partnerships, yet enforcement remains inconsistent across platforms[2]Source: Federal Trade Commission, “Disclosures 101 for Social Media Influencers,” ftc.gov. This regulatory ambiguity allows brands to seed products with micro-influencers at lower cost than traditional advertising, effectively outsourcing customer acquisition to creators with niche followings. The impact is most pronounced among Gen Z and millennial cohorts, who trust peer recommendations over brand messaging. However, the trend's sustainability is uncertain: as ACV content saturates feeds, engagement rates may decline, forcing brands to identify the next ingredient narrative or risk commoditization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and certification costs | -1.2% | Global, with acute impact on small producers in North America and Europe | Medium term (2-4 years) |

| Regulatory scrutiny on health claims | -0.9% | North America, Europe, with emerging enforcement in Asia-Pacific | Short term (≤ 2 years) |

| Fluctuating raw material prices | -0.7% | Global, with highest volatility in regions dependent on apple imports | Medium term (2-4 years) |

| Quality control and consistency issues | -0.6% | Global, particularly affecting smaller producers and contract manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production and Certification Costs

Organic certification and fermentation infrastructure impose fixed costs that disproportionately burden smaller producers, constraining supply growth and limiting competitive intensity. USDA organic certification requires annual fees, third-party audits, and traceability documentation, with compliance costs ranging from USD 1,500 to USD 5,000 for small operations[3]Source: U.S. Department of Agriculture, “Organic Transition Initiative,” Agricultural Marketing Service, usda.gov. Fermentation itself demands temperature-controlled facilities and acetobacter cultures, which smaller brands often outsource to contract manufacturers, sacrificing margin and control over production timelines. These barriers favor vertically integrated players like Bragg and Kraft Heinz, who amortize certification and capital expenses across diversified product lines, effectively raising the floor for new entrants. The dynamic is self-perpetuating: as incumbents capture organic shelf space, retailers allocate limited slots to proven brands, leaving challengers to compete on price in the conventional tier where margins are thinner. This cost structure suggests that market fragmentation will remain limited, with the top 5 players maintaining disproportionate market share absent disruptive business models such as co-fermentation cooperatives or blockchain-enabled traceability that reduce compliance overhead.

Regulatory Scrutiny on Health Claims

The FDA and FTC have intensified enforcement of health claims and advertising disclosures in 2024-2026, creating compliance risks for brands that overstate ACV's benefits. The FDA's structure-function claim framework permits manufacturers to describe effects on normal body processes, such as "supports digestive wellness", without pre-market approval, but prohibits disease claims like "treats diabetes" unless substantiated through the qualified health claim petition process. The FTC has issued warning letters to supplement brands for deceptive advertising, particularly those leveraging influencer endorsements without clear disclosure of material connections. This dual oversight creates a compliance minefield: brands must balance persuasive marketing with legal defensibility, often erring toward vague language that sacrifices differentiation. The scrutiny is most acute in North America and Europe, where regulatory agencies have dedicated resources for digital monitoring, whereas enforcement in Asia-Pacific and Latin America remains inconsistent. For multinational brands, this patchwork necessitates region-specific labeling and promotional strategies, inflating go-to-market costs and slowing product rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Capsules Gain Ground on Convenience

Liquid ACV held 71.87% of market share in 2025, reflecting entrenched consumer familiarity and retail dominance, yet tablet and capsule formats are projected to expand at 9.61% CAGR through 2031, outpacing liquid's growth as brands address taste aversion and portability constraints. Bragg's January 2025 launch of 750-milligram acetic acid capsules at Sprouts Farmers Market signals a strategic pivot toward consumers who prioritize convenience over the ritualistic aspects of liquid consumption. Capsules also enable precise dosing and eliminate the enamel-erosion concerns dentists associate with undiluted liquid, positioning the format as a safer daily supplement. Tablets, though less prevalent, appeal to cost-conscious buyers seeking lower per-serving prices than capsules, while gummies target younger demographics through flavor masking and lifestyle branding. Other forms, including powders and single-serve sachets, remain niche but are gaining traction in Asia-Pacific, where on-the-go consumption aligns with urbanization trends.

The format shift is reshaping value chains, as capsule production requires contract encapsulation facilities rather than fermentation infrastructure, lowering barriers for brands without manufacturing assets. This outsourcing model enables rapid SKU proliferation but sacrifices margin, as contract manufacturers capture 30-40% of wholesale prices. Liquid producers, conversely, benefit from vertical integration, controlling fermentation, bottling, and distribution, which preserves margin but limits format experimentation. The divergence suggests that the market will bifurcate into liquid specialists who compete on authenticity and organic certification, and format innovators who prioritize convenience and premium pricing. Regulatory influence remains minimal in this segmentation, as the FDA treats capsules and liquids identically under dietary supplement or food condiment classifications, depending on label claims.

By Category: Organic Premiums Compress Yet Growth Persists

Conventional ACV commanded 67.81% of 2025 revenues, anchored by price-sensitive retail buyers and foodservice operators who prioritize cost over certification, yet organic variants are expanding at 9.96% CAGR through 2031, driven by USDA-certified supply stabilization and retail buyers' clean-label mandates. The organic segment's growth reflects a broader shift in consumer spending toward products perceived as safer and more sustainable, even as retail premiums compress from 40-50% in 2020 to 20-30% in 2025 due to increased competition and supply normalization, according to the USDA. Conventional products retain dominance in commercial channels, spanning foodservice, industrial food processing, and household cleaning, where organic certification offers limited functional advantage, and buyers resist premium pricing.

The USDA's Organic Transition Initiative, which allocated funding to support farmers converting to organic practices, has begun stabilizing domestic apple supply chains, reducing dependence on imported organic concentrate from Europe and South America. However, certification costs remain a barrier for smaller producers, favoring vertically integrated players like Bragg and Eden Foods, who amortize compliance expenses across diversified portfolios. This dynamic suggests that organic market share gains will accrue disproportionately to incumbents with established certification infrastructure, leaving smaller entrants to compete on price in the conventional tier. The category segmentation also intersects with distribution channels: organic products dominate natural food retailers and e-commerce, while conventional variants hold share in mass merchandisers and dollar stores, reflecting distinct customer demographics and purchasing behaviors.

By Distribution Channel: Retail Dominance Masks Commercial Momentum

Retail channels accounted for 72.76% of 2025 distribution, driven by supermarkets, hypermarkets, and online platforms that offer broad assortments and promotional visibility. Commercial applications are expanding at a 9.33% CAGR through 2031, reflecting ACV's migration into foodservice, beauty formulations, and household cleaning products. Supermarkets and hypermarkets remain the largest retail sub-segment, leveraging high foot traffic and impulse purchase opportunities, though their share is eroding as online retail grows at double-digit rates, propelled by subscription models and influencer-driven discovery. Convenience stores capture incremental demand from consumers seeking single-serve formats, while other retail channels, including natural food stores and pharmacies, serve niche audiences prioritizing organic certification or therapeutic positioning.

Commercial channels, though smaller in absolute terms, offer superior margins and reduced promotional intensity, as buyers in foodservice and industrial applications prioritize consistency and bulk pricing over brand equity. Beauty and personal care manufacturers incorporate ACV into hair rinses and skincare toners, positioning the ingredient as a natural pH balancer, while household cleaning brands market ACV-based sprays as eco-friendly alternatives to synthetic disinfectants. This diversification reduces the market's dependence on dietary supplement cycles and exposes ACV to retail channels with different promotional calendars and margin structures. The shift is particularly pronounced in North America and Europe, where clean beauty and eco-friendly cleaning movements have achieved mainstream penetration, whereas Asia-Pacific adoption remains nascent outside Japan and South Korea.

Geography Analysis

North America held 33.38% of global market share in 2025, anchored by mature wellness infrastructure, established retail penetration, and high per-capita consumption of functional foods, yet the region's growth is moderating as the market saturates and promotional intensity compresses margins. The United States dominates regional demand, driven by widespread availability in supermarkets, natural food stores, and e-commerce platforms, while Canada and Mexico contribute incremental volume through cross-border retail chains and rising health consciousness. The FDA's updated "healthy" nutrient content claim rule, finalized in 2024, has legitimized ACV's positioning as a functional food, emboldening brands to invest in clinical substantiation and qualified health claim petitions. However, the region faces headwinds from regulatory scrutiny on influencer marketing and health claims, with the FTC intensifying enforcement of endorsement disclosures in 2024-2025. North American brands are responding by diversifying into non-ingestible applications across beauty, personal care, and household cleaning to capture demand beyond the dietary supplement category.

Asia-Pacific is expanding at a 10.22% CAGR through 2031, the fastest among all regions, propelled by rising disposable incomes, urbanization, and the integration of fermented foods into modern dietary patterns. India and China lead regional growth, with domestic brands like Dabur, Patanjali, and Kapiva leveraging Ayurvedic positioning and e-commerce distribution to capture middle-class consumers. Japan and South Korea exhibit higher per-capita consumption, driven by established wellness cultures and retail infrastructure that supports premium organic products. Australia's market mirrors North America in maturity, with strong penetration of natural food retailers and online subscription models. The region's growth is tempered by fragmented regulatory frameworks: India's FSSAI and China's CFDA enforce distinct labeling and health claim standards, complicating multinational rollouts and inflating compliance costs. Southeast Asian markets, including Indonesia, Thailand, and Singapore, remain nascent but are attracting investment from regional distributors seeking first-mover advantage in functional foods.

Europe accounted for a significant share in 2025, driven by Germany, the United Kingdom, France, and Italy, where organic food movements and clean-label preferences have achieved mainstream penetration. The European Union's organic regulations, which mandate traceability and third-party certification, create a high-compliance environment that favors established brands with robust supply chain documentation. Germany leads regional consumption, supported by a dense network of natural food retailers and consumer willingness to pay premiums for certified products. The United Kingdom's market has grown despite Brexit-related supply chain disruptions, as e-commerce platforms enable direct-to-consumer distribution that bypasses traditional retail gatekeepers. Southern European markets, including Spain and Italy, exhibit lower per-capita consumption but are expanding as wellness trends diffuse from urban centers. The region's growth is constrained by economic headwinds and consumer price sensitivity, which have compressed organic premiums and intensified promotional activity. Eastern European markets, including Poland and the Czech Republic, remain underpenetrated but are attracting investment from regional distributors seeking growth beyond saturated Western markets.

South America and Middle East and Africa represent emerging opportunities, with Brazil, Argentina, and South Africa leading regional adoption driven by rising health consciousness and retail modernization. Brazil's market benefits from a large population and growing middle class, though economic volatility and currency fluctuations create demand uncertainty. Argentina and Chile exhibit higher per-capita consumption, supported by wellness cultures and retail infrastructure that accommodates premium products. The Middle East's market is concentrated in the United Arab Emirates and Saudi Arabia, where expatriate populations and high disposable incomes drive demand for imported organic products. Africa's market remains nascent, with South Africa and Nigeria accounting for the majority of regional volume, though distribution challenges and price sensitivity limit penetration. These regions face common challenges: fragmented retail infrastructure, limited organic certification frameworks, and regulatory inconsistency that complicates multinational market entry. However, the proliferation of e-commerce platforms and mobile payment systems is lowering barriers, enabling brands to bypass traditional distribution and reach consumers directly.

Competitive Landscape

The apple cider vinegar market operates with moderate concentration, with established multinational players coexisting alongside regional specialists and direct-to-consumer disruptors. Kraft Heinz, Bragg, and Molson Coors (Aspall) leverage vertically integrated supply chains, organic certification infrastructure, and retail distribution agreements to defend share, while regional brands like Dabur and Patanjali in India capitalize on Ayurvedic positioning and e-commerce penetration to capture middle-class consumers. Competition centers on format innovation, organic certification, and direct-to-consumer e-commerce rather than on price wars, as evidenced by Bragg's January 2025 launch of 750-milligram acetic acid capsules at Sprouts Farmers Market, targeting consumers who reject the taste profile of liquids.

The proliferation of gummy, tablet, and powder formats suggests incumbents are defending share by fragmenting the category into micro-segments, each with distinct margin structures and customer acquisition costs. White-space opportunities exist in commercial applications, spanning foodservice, beauty formulations, and household cleaning, where ACV's functional properties offer differentiation beyond dietary supplements. Emerging disruptors include celebrity-backed wellness brands and influencer-led direct-to-consumer labels that leverage social media for customer acquisition, bypassing traditional retail gatekeepers and capturing margin that incumbents sacrifice to distributors. These entrants often outsource fermentation and encapsulation to contract manufacturers, enabling rapid SKU proliferation without capital-intensive infrastructure, though this model sacrifices margin and control over quality.

Technology adoption remains limited, with few brands investing in blockchain traceability or real-time fermentation monitoring, suggesting that operational excellence rather than digital innovation differentiates leaders. The FDA's Current Good Manufacturing Practice regulations apply to dietary supplements but not to vinegar sold as a food condiment, creating a regulatory gap that some brands exploit by avoiding supplement registration. This inconsistency becomes a competitive liability as consumers share negative experiences on social media, eroding the category's credibility and rewarding brands that invest in vertical integration and quality assurance.

Apple Cider Vinegar Industry Leaders

The Kraft Heinz Company

Bragg Live Food Products LLC

Hive and Wellness Australia Pty Ltd

Carl Kuhne KG

Molson Coors Beverage Company (Aspall)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bragg Live Food Products, Inc. has unveiled its latest wellness-promoting blend: Pineapple Turmeric Apple Cider Vinegar. This new offering combines the zesty wellness staple with organic pineapple and turmeric, both known for their digestive support properties. The product is designed to cater to health-conscious consumers seeking natural solutions to enhance digestion and overall well-being.

- March 2025: PepsiCo acquired the prebiotic soda brand Poppi for USD 1.95 billion, a figure that notably includes an anticipated cash tax benefit of USD 300 million. This acquisition marks the largest transaction in the functional beverage sector to date, underscoring the surging market appetite for products rooted in apple cider vinegar. By bringing Poppi into its fold, PepsiCo not only gains the brand's unique formulation but also its established customer base.

- February 2025: Bragg launched its Apple Cider Vinegar supplement capsules across the United States at all Sprouts Farmers Market stores, expanding its retail footprint. The move aligns with its mission to make daily wellness more accessible through convenient, on-the-go formats.

- March 2024: RTD sparkling apple cider vinegar brand Apeal World introduced its third flavor variant, Organic Lemon and Mint. The beverage combines sparkling water, organic apple cider vinegar, organic extracts, and sustainably sourced spices. The product mentioned its each serving contains potassium, calcium, and magnesium.

Global Apple Cider Vinegar Market Report Scope

Apple cider vinegar (ACV) is a type of vinegar made from fermented apple juice. It has a tangy, slightly sweet flavor and is widely used in cooking, food preservation, and natural health remedies. The apple cider vinegar market is segmented by form, category, distribution channel, and geography. The market is segmented by form into liquid, tablets, capsules, and other formats. Based on the category, it is segmented into organic and conventional. Based on distribution channels, the market studied is segmented into off-trade and on-trade. The off-trade segment is further segmented into supermarkets/hypermarkets, drugstores/pharmacies, convenience stores, online retail stores, and other distribution channels. By geography, the study provides key insights into the major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD and volume in units for all the above-mentioned segments.

| Liquid |

| Tablet and Capsule |

| Other Forms |

| Organic |

| Conventional |

| Commercial | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Liquid | |

| Tablet and Capsule | ||

| Other Forms | ||

| By Category | Organic | |

| Conventional | ||

| By Distribution Channel | Commercial | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the apple cider vinegar market by 2031?

The market is expected to reach USD 2.27 billion by 2031.

Which region will post the fastest growth through 2031?

Asia-Pacific is forecast to expand at 10.22% CAGR, the quickest among all regions.

Why are capsules gaining popularity over liquid apple cider vinegar?

Capsules remove vinegar’s strong taste, travel well, and provide precise dosing, leading to a 9.61% CAGR forecast for the format.

How large is the organic segment compared with conventional products?

Organic products held 32.19% of 2025 revenue and are growing faster at 9.96% CAGR as certification costs fall.

Which companies lead the competitive landscape?

Kraft Heinz, Bragg, and Molson Coors (Aspall) are among the top players, collectively controlling close to 28% of global sales.

Page last updated on: