Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.5 Billion |

| Market Size (2026) | USD 2.60 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Vinegar Market Analysis by Mordor Intelligence

The Asia-Pacific vinegar market size is expected to grow from USD 2.50 billion in 2025 to USD 2.6 billion in 2026 and is forecast to reach USD 3.18 billion by 2031 at 4.13% CAGR over 2026-2031. Heightened health awareness, swift adoption of e-commerce, and ongoing investments by major manufacturers bolster the industry's trajectory. Vinegar's dual role as a traditional staple and a functional ingredient used for food preservation, promoting digestive health, and in organic agriculture fuels its demand. Its versatility as a preservative and health-enhancing product makes it a preferred choice among consumers seeking natural and functional food options. The expanding middle class, with its increasing purchasing power, and government initiatives promoting fermented foods, further boost consumption in both retail and industrial sectors. These initiatives often include awareness campaigns and subsidies that encourage the adoption of fermented products. Upgrades in production, such as automated fermentation monitoring and streamlined supply chains, not only ensure consistent quality and cost control but also facilitate scaling. These advancements allow manufacturers to meet growing demand efficiently while maintaining product standards. In China and the Philippines, clearer regulations on additive use dispel uncertainties and foster product innovation, enabling companies to explore new formulations and cater to evolving consumer preferences.

Key Report Takeaways

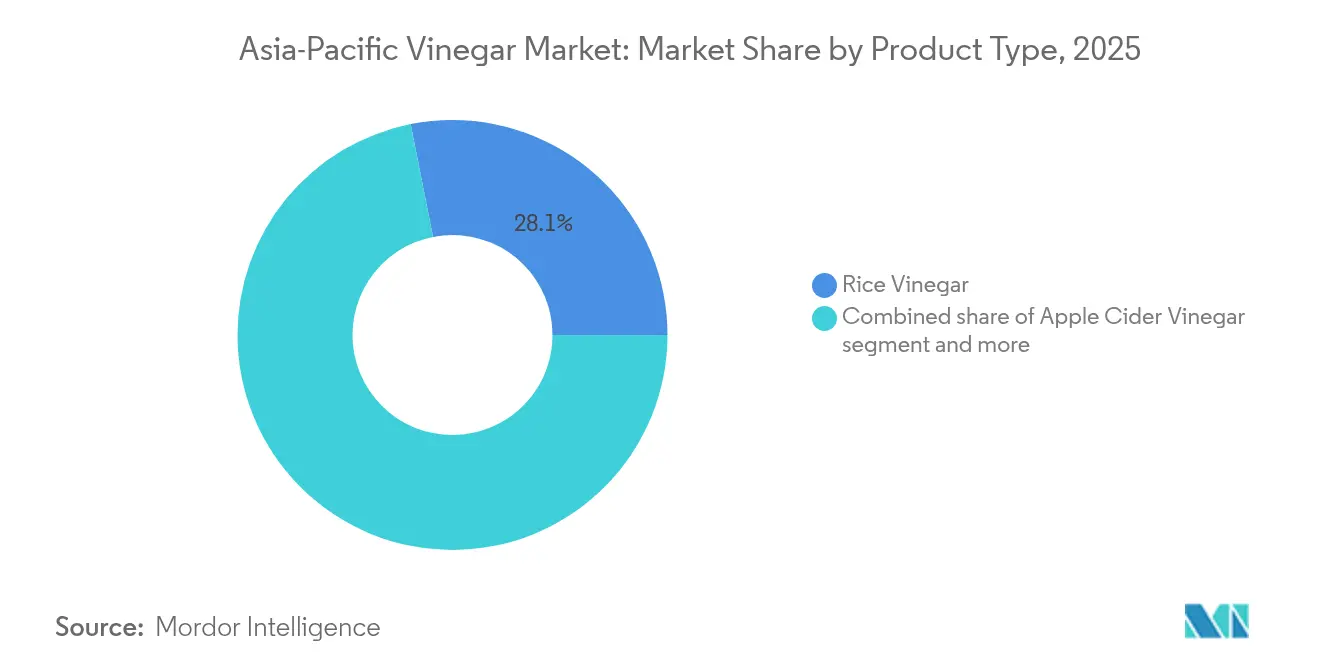

- By product type, rice vinegar led with 28.12% revenue share in 2025, while apple cider vinegar is projected to post the fastest 5.78% CAGR between 2026 and 2031.

- By source, conventional variants accounted for 72.55% of the 2025 base, whereas certified-organic vinegar production is expected to expand at a 4.76% CAGR through 2031.

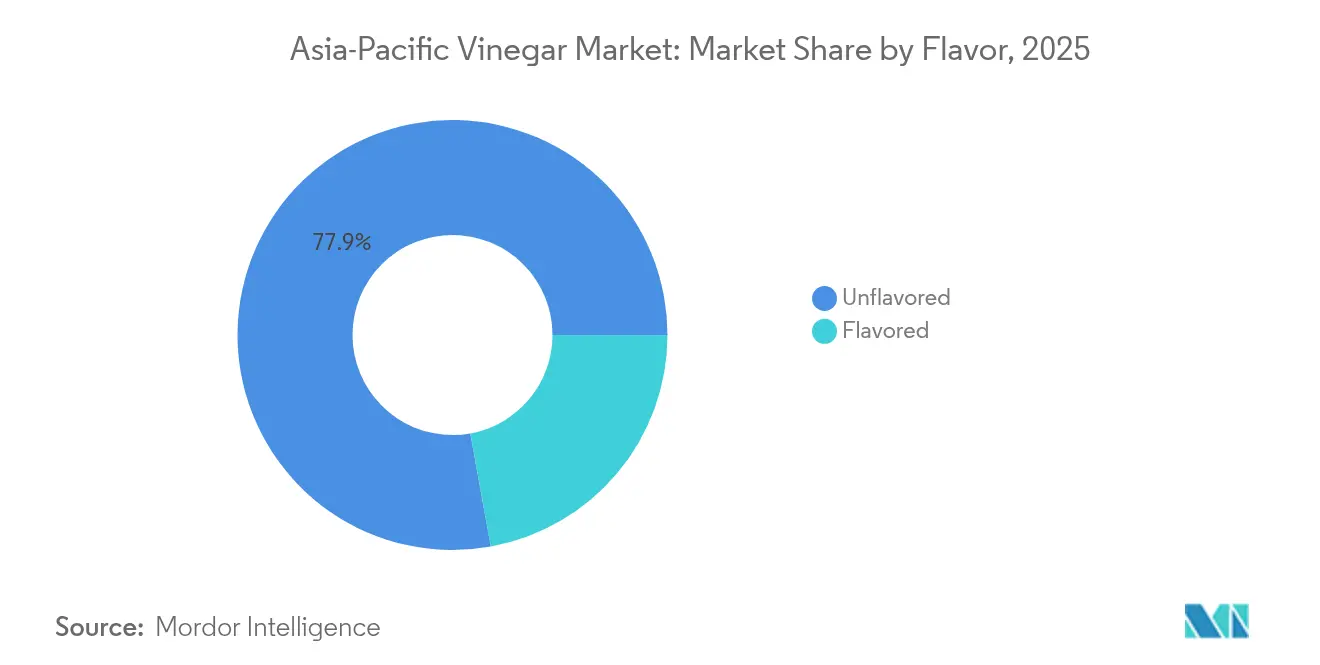

- By flavor profile, unflavored variants held a 77.85% share of the Asia-Pacific vinegar market size in 2025; flavored formulations are set to grow at a 4.83% CAGR from 2026 to 2031.

- By distribution channel, retail commanded 54.21% of revenue in 2025; industrial usage is forecast to record the highest 5.72% CAGR to 2031.

- By geography, China captured 36.78% of 2025 sales; India is poised for the quickest 5.53% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Vinegar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer health-and-wellness focus | +1.2% | Urban China, Japan, Australia | Medium term (2-4 years) |

| Expansion of quick service restaurants and food-delivery platforms | +0.8% | Core Asia-Pacific, spill-over to Southeast Asia | Short term (≤ 2 years) |

| E-commerce penetration | +0.7% | China, India, Thailand metropolitan areas | Short term (≤ 2 years) |

| Government promotion of fermented condiments | +0.6% | China, India, Philippines, Vietnam | Long term (≥ 4 years) |

| Wood-vinegar use in regenerative agriculture | +0.4% | Malaysia, Thailand, Indonesia, Australia | Long term (≥ 4 years) |

| Probiotic drinking-vinegar innovation | +0.5% | Japan, South Korea, urban China, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer health-and-wellness focus drives demand for functional vinegars

Shoppers increasingly adopt apple cider vinegar, associating its acetic content with improved blood-glucose control, though rice vinegar still commands the largest market share. Clinical studies highlighting a 20% reduction in post-prandial glucose have spurred the launch of raw variants, especially those containing the "mother," and marketed for weight management. These studies have also driven consumer interest in functional beverages, encouraging manufacturers to innovate and diversify their product offerings. Manufacturers are now promoting single-serve drinking shots and sparkling vinegar beverages, emphasizing their digestive health benefits and appealing to health-conscious consumers. In the Asia-Pacific vinegar market, younger consumers are willing to pay a premium for transparent ingredient lists, boosting average unit prices and profit margins. This broader vinegar market trend reflects a growing demand for clean-label products that align with wellness-focused lifestyles. Additionally, online direct-to-consumer platforms enhance their reach by targeting niche wellness communities through tailored advertising and subscription bundles, further strengthening brand loyalty and market penetration.

Expansion of QSR and Food-Delivery Platforms Boosts horeca Vinegar Usage

Quick-service restaurants are opening at a rapid pace, and app-based delivery orders are becoming the norm. This shift is significantly boosting industrial demand, challenging the long-standing dominance of retail in the market. Operators are increasingly turning to vinegar, not just to enhance flavors in plant-based dishes, but also to ensure sauces remain stable and maintain quality in takeaway packs. Central kitchens, with their stringent requirements for specific acidity levels and color tolerances, are driving suppliers to adopt advanced automated process controls to meet these demands efficiently. Chains operating across multiple regions are prioritizing uniform formulations to ensure consistent menu offerings, leading them to partner with producers that have vertically integrated facilities capable of handling high-volume contract manufacturing while maintaining quality and consistency.

E-commerce penetration enables long-tail specialty vinegar distribution

In the Asia-Pacific vinegar market, digital marketplaces are breaking the constraints of physical shelves. This shift enables smaller brands to prominently feature their artisanal, fruit-infused, and botanically enriched vinegars, which might otherwise struggle to gain visibility in traditional retail settings. Live-stream promotions not only educate consumers about product benefits and usage but also establish real-time feedback loops, facilitating swift flavor adjustments to meet evolving preferences. Meanwhile, cross-border logistics services are paving the way for overseas opportunities, sidestepping hefty distributor mark-ups and enabling brands to reach international markets more efficiently. Additionally, detailed shopper data empowers producers to fine-tune their inventory based on city tiers, ensuring better alignment with local demand patterns. Subscription programs are further solidifying this landscape, ensuring repeat demand, reducing dependence on promotional discounts, and bolstering stable cash flows for these emerging labels, thereby supporting their long-term growth and market presence.

Government promotion of traditional fermented condiments fuels local output

Governments across the Asia-Pacific are weaving fermented foods into their national nutrition agendas. China's GB 2719 standard upholds traditional quality benchmarks while aligning with contemporary safety norms, ensuring that heritage techniques are preserved without compromising on modern food safety requirements. The Philippines' Food and Drug Administration has introduced a revamped vinegar code, modernizing 1970s regulations and simplifying compliance for small rural producers, thereby fostering inclusivity in the market[1]Source: IRE Journals," Exploring the Practices in the Traditional Nipa Vinegar Production in Lingayen, Pangasinan", irejournals.com . Vietnam's Circular /2019 establishes comprehensive food additive regulations specific to vinegar categories, creating regulatory clarity that supports industry investment and export development[2]Source: Ministry of Health, Vietnam, " Circular No. 24/2019/TT-BYT regulating the management and use of food additives", vfa.gov.vn. With access to technical training and low-interest loans, these producers are upgrading their plants, adopting advanced technologies, boosting throughput, and enhancing export readiness to compete in global markets. Additionally, government-sponsored marketing initiatives at trade fairs are not only amplifying the cultural significance of vinegar but also driving up domestic consumption by creating awareness and promoting its diverse applications in daily diets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acetic-acid feedstock price volatility | -0.9% | Import-dependent Southeast Asian facilities | Short term (≤ 2 years) |

| Substitution pressure from other condiments | -0.6% | Core Asia-Pacific, price-sensitive households | Medium term (2-4 years) |

| Divergent labeling and health-claim rules | -0.4% | Exporters navigating multiple Asia-Pacific jurisdictions | Long term (≥ 4 years) |

| Sensory-quality variance in bulk supply | -0.3% | Large quick service restaurants and central kitchens requiring tight specification bands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acetic-acid feedstock price volatility inflates production costs

In 2024, imported glacial acetic acid prices mirrored the fluctuations of petrochemical markets, significantly impacting the operational costs of smaller plants in Thailand and Indonesia. These plants, particularly those without hedging programs, face heightened financial strain as they are unable to mitigate price volatility effectively. Organic production lines encounter additional challenges due to their reliance on a narrower range of feedstock options and the burden of fixed certification fees, which further constrain their flexibility. On the other hand, integrated brewers with on-site fermentation tanks are better positioned to manage these pressures by diluting their exposure to market swings. This advantage highlights the importance of scale economies, which continue to widen competitive disparities within the industry. Furthermore, currency depreciation in certain ASEAN nations exacerbates the situation by increasing costs for processors heavily dependent on imports, adding another layer of financial pressure.

Substitution pressure from other condiments limits premium pricing

In local cuisines, soy sauce, citrus dressings, and synthetic acidulants vie for dominance, both in terms of pricing and consumer familiarity. These alternatives are widely used due to their adaptability to various flavor profiles and cost-effectiveness. Food processors, aiming for extended shelf-lives, often turn to more affordable lactic or citric acids, which are readily available and efficient, inadvertently capping the potential mark-ups on vinegar. To protect their profit margins, leading brands in the category are not only emphasizing the distinctiveness of their flavors but also intertwining them with health narratives and a commitment to transparent sourcing. This approach helps them appeal to health-conscious consumers and those seeking authenticity in product origins. However, this compelling messaging comes with a hefty price tag in advertising, a cost that smaller firms find challenging to shoulder, limiting their ability to compete effectively in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rice Vinegar Dominance Meets Apple Cider Acceleration

In 2025, rice vinegar commanded a dominant 28.12% share of the Asia-Pacific vinegar market. This stronghold is bolstered by the region's rich culinary traditions, especially in countries like China, Japan, and South Korea, and the availability of abundant rice feedstocks. Automated manufacturing plants in these nations not only ensure low unit costs but also maintain a consistently high product quality. Furthermore, government backing for fermentation innovations is modernizing production methods and broadening product offerings. Traditional applications of rice vinegar in sushi, marinades, and dressings further cement its high-volume demand. Its dominance is a testament to its versatility, affordability, and the deep-rooted food culture in the Asia-Pacific. Notably, barrel-aged variants are now being marketed for gifting and gourmet occasions.

While apple cider vinegar holds a smaller market share, it's emerging as the fastest-growing segment, projected to achieve a 5.78% CAGR through 2031. This surge is largely driven by health-conscious consumers gravitating towards metabolic support and natural wellness solutions. The rising popularity of apple cider vinegar is also attributed to Western lifestyle influences and heightened product endorsements by influencers on social media. Brands are capitalizing on this trend, emphasizing attributes like 'raw' and 'unfiltered' on labels to command premium prices. Additionally, formats like single-serve functional shots are gaining traction, especially among fitness enthusiasts. Specialty vinegars, such as balsamic and coconut, though primarily found in gourmet channels, are leveraging premium packaging and storytelling. The competitive landscape is increasingly focusing on functional claims, like microbiome enrichment and reduced sugar, while government food institutes are aiding smaller players in refining fermentation processes through technology transfer programs.

By Source: Conventional Leadership Faces Organic Momentum

In 2025, conventional vinegar production in the Asia-Pacific region dominated the market, accounting for a substantial 72.55% of total revenue. This stronghold is largely attributed to cost-effective supply chains and a deep-rooted culinary familiarity, especially with staple white and rice vinegars. These vinegars cater not only to price-sensitive households but also to industrial buyers. Manufacturers have bolstered the strength of these conventional formats by scaling operations, optimizing logistics, and ensuring stable output through established supply networks. The versatility of conventional vinegar applications, spanning both household and foodservice uses, solidifies its status as a staple in both local and export markets. In response to growing eco-awareness, conventional producers are modernizing their processes, such as adopting wastewater recycling and renewable energy, to maintain consumer trust, even without fully transitioning to certified-organic status.

Looking ahead, organic vinegar production is set to witness a robust growth trajectory, with projections indicating a 4.76% CAGR by 2031. This surge is fueled by environmentally-conscious and ESG-minded consumers who prioritize authenticity, ingredient transparency, and clean-label products. The expanding market share for organic varieties is bolstered by incentives for farm-gate conversions, especially in regions like Australia and South Korea. Furthermore, North American and European markets offer export premiums, rewarding those with traceable supply chains and sustainable practices. However, the path to entry isn't easy; third-party audits, including organic certifications, create significant barriers. This landscape favors larger, well-capitalized processors who can absorb these costs and consistently meet quality benchmarks. To further enhance their operations, integrated players are leveraging distributed ledger (blockchain) systems, ensuring traceability and mitigating regulatory risks. Additionally, many organic processors are diversifying their offerings, venturing into wood-vinegar bio-stimulants for agriculture. This not only broadens their market reach but also cushions them against retail volatility. Such strategic moves are propelling the momentum of the eco-segment, especially among urban consumers and in export markets where regulatory oversight and consumer scrutiny are paramount.

By Flavor: Unflavored Foundation Supports Flavored Innovation

In 2025, unflavored vinegar formats commanded a dominant 77.85% share of the Asia-Pacific market, primarily catering to multipurpose cooking and food processing applications. Here, consistency, cost-effectiveness, and broad utility reign supreme. This robust demand not only secures high production volumes but also allows manufacturers to harness economies of scale, ensuring they lead in pricing within mass retail channels. Unflavored varieties, particularly white and rice vinegar, are deeply embedded in both industrial and household applications, underscoring the region's entrenched culinary habits and well-established supply chains.

Flavored vinegar innovations, such as citrus, berry, and herb infusions, are set to grow at a 4.83% CAGR through 2031. This growth is fueled by an increasing appetite for convenience, novel taste experiences, and functional nutrition. These flavored products are riding the global wave towards ready-to-drink solutions, striking a balance between refreshing acidity and reduced sugar. They've carved out a premium market position, thanks to techniques like high-pressure processing and cold-brew methods, which safeguard their delicate aromatics and unique flavors. Marketing strategies for these SKUs lean heavily on social media sampling, collaborations with culinary influencers for recipes, and a nimble approach to rolling out seasonal limited editions, all informed by insights from online marketplaces. In this burgeoning market, regulatory teams play a pivotal role. Given the vast differences in flavoring and additive compliance across jurisdictions, established multi-country players find themselves with a pronounced edge.

By Distribution Channel: Retail Dominance Meets Industrial Acceleration

In 2025, retail outlets, encompassing supermarkets and convenience stores, accounted for 54.21% of the revenue in the Asia-Pacific vinegar market. This underscores their pivotal role in household consumption and routine vinegar purchases. Supermarkets, commanding a 38.5% share, engage consumers through a diverse range, prominent shelf visibility, and in-store sampling, ensuring robust repeat sales in both urban and semi-urban locales. Convenience stores play a complementary role, catering to impulse buys and refills for daily meals and food prep. Brands are amplifying shopper engagement through omnichannel strategies, merging in-store tastings with e-commerce flash sales. This approach resonates with buyers who often research online before purchasing in-store. Additionally, direct-to-consumer subscription models are gaining momentum in specialty vinegar segments, capitalizing on the perishability and health appeal of live-culture products, leading to impressive retention rates.

Industrial shipments are emerging as the fastest-growing segment, with projections indicating a climb at a 5.72% CAGR through 2031. This growth is driven by processed food manufacturers increasingly turning to clean-label natural preservatives for sauces, ready meals, snacks, and baked goods. To enhance logistics efficiency, processors are transitioning from 20-liter drums to intermediate bulk containers, optimizing freight and reducing product loss during scaling. A surge in demand from foodservice sectors, notably quick-service restaurants (QSRs) and large-scale caterers, is leading to multi-year purchase agreements. These contracts, often tied to benchmark commodity prices, ensure stable revenue streams and incentivize suppliers to boost fermentation capacities. Suppliers are also delving into new formulations, aligning with the evolving demands for clean labels, health benefits, and extended shelf life. The intertwining of retail and industrial demands, bolstered by innovative omnichannel strategies and procurement methods, paints a promising picture for the vinegar market in the Asia-Pacific region.

Geography Analysis

In 2025, China dominated the market, accounting for 36.78% of both volume and value. This dominance is rooted in China's rich fermentation heritage, with production hubs concentrated in Shanxi and Jiangsu. The country benefits from national standards that bolster quality benchmarks, ensuring consistent product quality across the market. Additionally, state-level grants fund equipment upgrades, which not only enhance production efficiency but also significantly reduce effluent discharge, addressing environmental concerns. E-commerce flash sales festivals have become a key driver of consumption, with vinegar often bundled alongside soy sauce and cooking wine to attract buyers. Meanwhile, exporters leverage the One Belt One Road logistics corridors to deliver competitively priced private-label shipments to retailers in Southeast Asia, capitalizing on the region's growing demand for affordable, high-quality products.

India is set to lead with a robust 5.53% CAGR, driven by rising disposable incomes and urban millennials' growing affinity for Western-style salad dressings and detox trends. Organized retail chains are dedicating more shelf space to premium apple cider and coconut vinegars, reflecting the increasing consumer preference for health-oriented products. At the same time, home-based micro-sellers are making inroads into tier-3 cities through social-commerce platforms, expanding the reach of these niche products. Recognizing the nutritional value of fermented foods, government programs are promoting technical training in small cooperatives. These initiatives aim to minimize hygienic oversights, improve production standards, and ultimately boost consumer trust in locally produced vinegars.

Japan, while mature, offers a lucrative market characterized by its stringent quality demands and a readiness to invest in authenticity. Artisanal black vinegar, aged in traditional earthenware crocks, not only commands a premium but also serves as a sought-after souvenir for domestic tourists. This high-value segment reflects Japanese consumers' willingness to pay for products that emphasize tradition and craftsmanship. Australia's robust organic certification framework is driving a swift adoption of raw, unfiltered products among its health-conscious consumers, who prioritize natural and minimally processed options. In Southeast Asia, Thailand and Vietnam are at the forefront of flavor innovation, skillfully blending local fruits with vinegar to craft vibrant condiments that resonate with the region's street-food culture. Harmonized ASEAN standards for food additives ease cross-border trade, fostering regional collaboration. However, distinct country-specific labeling regulations necessitate tailored packaging solutions, adding complexity to market entry strategies for exporters.

Competitive Landscape

The vinegar market in the Asia-Pacific region exhibits moderate fragmentation. Major players like Mizkan Holdings, CJ CheilJedang, and Daesang boast diverse portfolios and extensive distribution networks, bolstered by their capacity for plant expansions. Meanwhile, regional specialists carve out niches by highlighting their unique fruit bases, organic certifications, and authentic provenance. Through vertical integration, these players manage everything from grain procurement to bottling, ensuring cost control and traceability that appeal to both industrial clients and discerning retail consumers.

Adoption of technology varies across the board. Larger facilities utilize real-time pH and temperature sensors, integrated with cloud analytics, to minimize batch variability. In contrast, mid-sized companies focus on energy-efficient acetators, aiming to cut both operating costs and emissions. Marketing narratives now revolve around the artistry of fermentation and collaborations with local farmers. Mergers and acquisitions remain vibrant, highlighted by Mizkan's 2025 purchase of a cocktail-mixer brand, enhancing its foothold in the premium beverage segment. Firms with an export focus are establishing satellite blending lines close to demand hubs, not only to slash freight expenses but also to cater to the "made in market" labeling trend.

Health-centric start-ups are intensifying competitive pressures, promoting probiotic drinking vinegars through subscription models. These newcomers harness digital platforms and eco-friendly aluminum bottles to attract a younger audience. In response, established companies forge co-branding partnerships with fitness influencers and introduce smaller pack sizes to encourage trial purchases. Companies with robust regulatory compliance, particularly in health claims, gain a competitive edge, thanks to their dedicated scientific teams and multilingual documentation capabilities.

Asia-Pacific Vinegar Industry Leaders

-

The Kraft Heinz Company

-

Autralian Vinegar

-

Mizkan Holdings Co. Ltd.

-

Jiangsu Hengshun

-

Shanxi Shuita

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lee Kum Kee unveiled its new line of premium, health-focused vinegar products. The launch featured culinary demonstrations by top chefs, showcasing the versatility of the products in various cuisines. This initiative highlights the company's dedication to promoting health and driving global culinary innovation.

- February 2025: Kewpie Brewing Company introduced a vinegar aimed at bolstering immune health. Specifically designed for health-conscious Japanese consumers, the product is positioned as a functional beverage for daily wellness. This launch reflects the company's strategic focus on addressing the growing demand for health-oriented products in Japan.

- August 2024: Kong Yen Foods rolled out innovative vinegar varieties for both local and U.S. markets. These products emphasize health claims, such as potential benefits for digestion and overall wellness, and have secured international certifications to appeal to a broader audience. This move aligns with the company's strategy to expand its global footprint while catering to health-conscious consumers.

- July 2024: Thai Dyan Rice Vinegar debuted a new rice vinegar, aligning with wellness trends and the Thai palate's preference for lighter salad and dip condiments. The product launch reflects the company's commitment to promoting healthier eating habits while catering to the evolving preferences of both domestic and international markets.

Asia-Pacific Vinegar Market Report Scope

Vinegar is a sour liquid made by fermenting substances that contain sugar, such as fruit or wine. It is used as a condiment to add flavor or as a preservative for pickling. Vinegar contributes acidic notes to foods, both in aroma and taste. The report on the Asia-Pacific vinegar market is segmented by type into balsamic vinegar, red wine vinegar, apple cider vinegar, rice vinegar, and other types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. The report also involves the analysis of regions such as China, Japan, India, Australia, and Rest of Asia-Pacific. For each segment, the market sizing and forecasting have been done in value terms (USD million).

By Product Type

| Balsamic Vinegar |

| Red Wine Vinegar |

| Apple Cider Vinegar |

| Rice Vinegar |

| Other Types |

By Source

| Organic |

| Conventional |

By Flavor

| Flavored |

| Unflavored |

By Distribution Channel

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| Foodservice | |

| Industrial |

By Geography

| China |

| Japan |

| India |

| Australia |

| New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Philippines |

| Rest of Asia-Pacific |

| By Product Type | Balsamic Vinegar | |

| Red Wine Vinegar | ||

| Apple Cider Vinegar | ||

| Rice Vinegar | ||

| Other Types | ||

| By Source | Organic | |

| Conventional | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| Foodservice | ||

| Industrial | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia Pacific alcoholic vinegar market?

The market stands at USD 2.6 billion in 2026 and is projected to reach USD 3.18 billion by 2031.

Which product type holds the largest share?

Rice vinegar leads with 28.12% of 2025 revenue.

Which geography is growing the fastest?

India is forecast to register the highest 5.53% CAGR between 2026 and 2031.

How big is the industrial channel opportunity?

Rising consumer preference for certified sustainable products is driving a 4.76% CAGR in organic variants.

Page last updated on: