Anti-tuberculosis Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-tuberculosis Drugs Market Analysis by Mordor Intelligence

The anti-tuberculosis drugs market size in 2026 is estimated at USD 1.58 billion, growing from 2025 value of USD 1.49 billion with 2031 projections showing USD 2.13 billion, growing at 6.14% CAGR over 2026-2031. Strengthening public-sector funding, surging multidrug-resistant infections and rapid uptake of shorter all-oral regimens are keeping demand resilient despite lingering supply chain disruptions. North America preserves a dominant revenue position thanks to established stockpiles and reimbursement frameworks, yet expanded procurement in Asia-Pacific – led by India’s National TB Elimination Program and China’s stepped-up screening – is accelerating geographic diversification. Drug-class dynamics are shifting toward novel agents such as bedaquiline and pretomanid as resistance to legacy first-line therapies rises, while digital ordering channels broaden patient access in low-resource environments. Company strategies increasingly revolve around strategic alliances that link innovative molecules with artificial-intelligence diagnostics to secure integrated care offerings, a trend that helps temper fragmentation and lift the overall anti-tuberculosis drugs market trajectory.

Key Report Takeaways

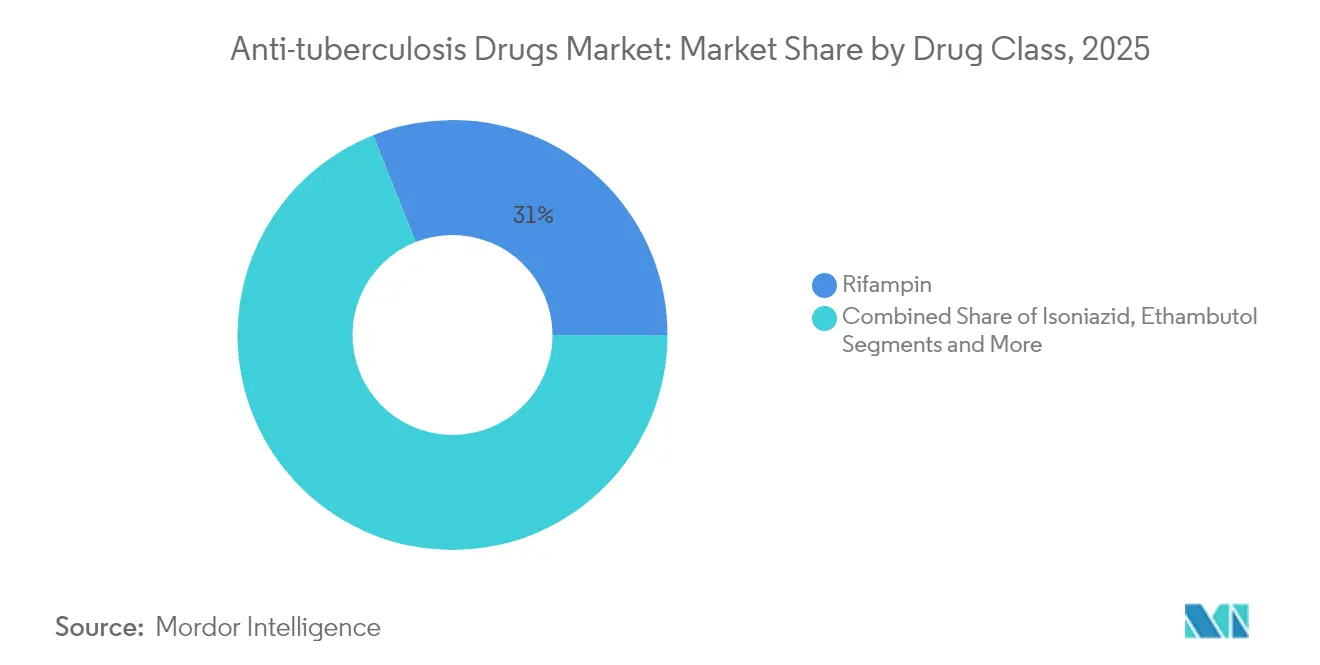

- By drug class, rifampin led with 31.02% revenue share in 2025; bedaquiline is forecast to record a 12.92% CAGR through 2031.

- By end user, hospitals and clinics held 44.87% share of the anti-tuberculosis drugs market size in 2025; non-profit organizations are advancing at a 9.97% CAGR through 2031.

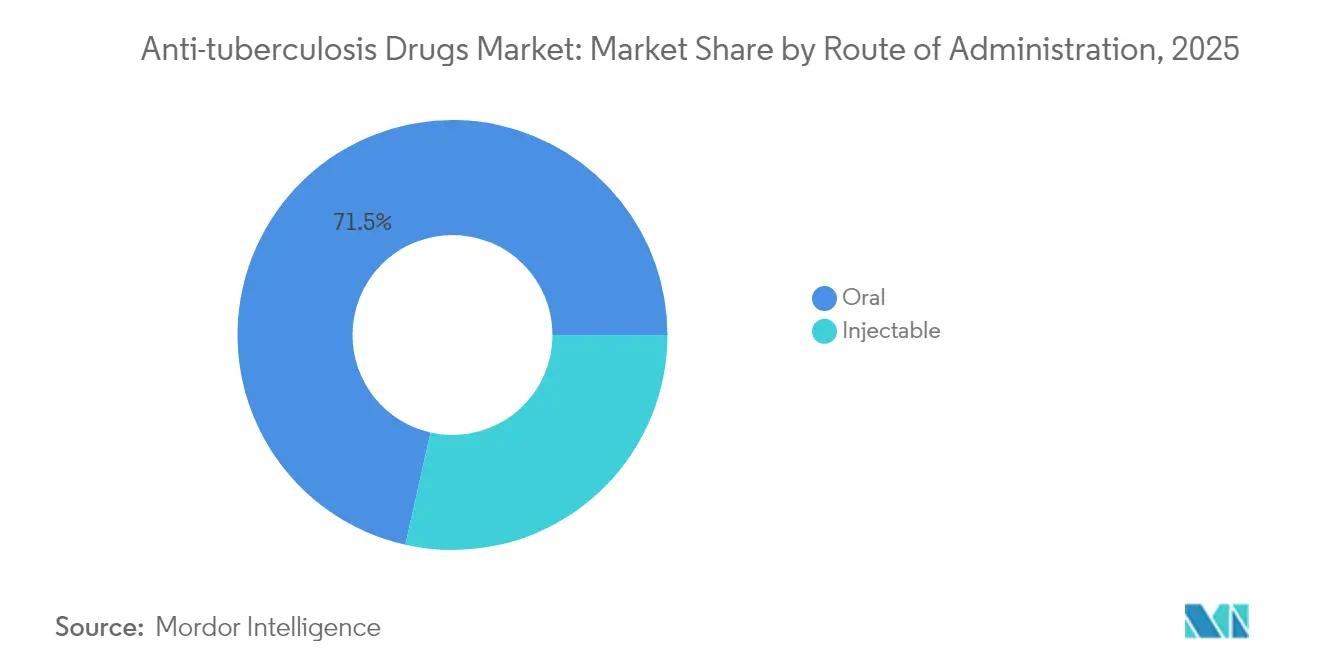

- By route of administration, oral formulations represented 71.48% share in 2025 and continue to register a 7.58% CAGR to 2031.

- By distribution channel, hospital pharmacies captured 51.74% share of the anti-tuberculosis drugs market size in 2025, while online pharmacies are set to expand at an 8.47% CAGR to 2031.

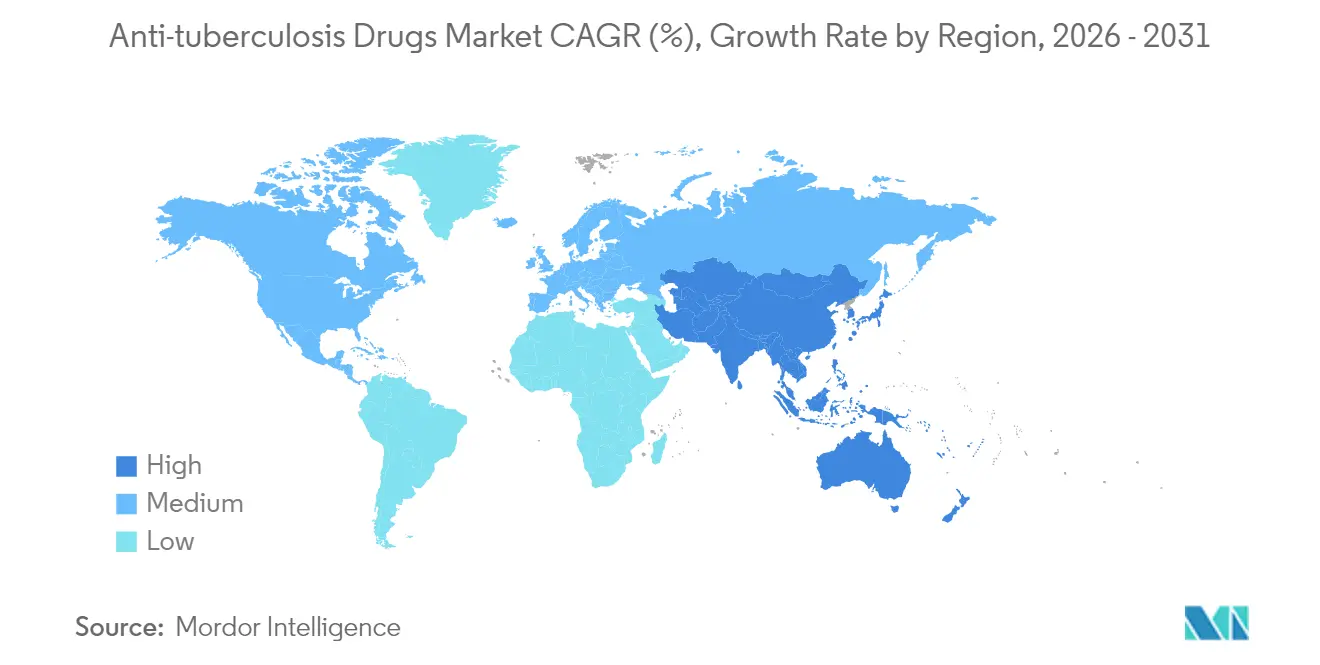

- By geography, North America accounted for 41.96% of the anti-tuberculosis drugs market share in 2025, whereas Asia-Pacific is projected to grow at a 9.49% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-tuberculosis Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of tuberculosis | +1.8% | Asia-Pacific and Africa highest | Medium term (2-4 years) |

| Incidence surge of MDR & XDR strains | +2.1% | Eastern Europe and Asia | Long term (≥ 4 years) |

| WHO End-TB funding momentum | +1.2% | High-burden countries worldwide | Short term (≤ 2 years) |

| Government-led awareness initiatives | +0.9% | Asia-Pacific core; spill-over to Africa and South America | Medium term (2-4 years) |

| Short-course all-oral regimen breakthroughs | +1.5% | Early adoption in developed markets | Short term (≤ 2 years) |

| AI-enabled radiology screening adoption | +0.7% | North America & EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Tuberculosis

Worldwide incidence reached 10.8 million new cases in 2023, the highest since formal monitoring began and outpacing COVID-19 fatalities. India, Indonesia and the Philippines experienced severe notification gaps during pandemic years that now translate into intensified community transmission. Southeast Asia alone carries 46% of global infections, a burden magnified by poverty-related crowding in rapidly urbanizing districts[1]Asian Development Bank, “Pandemic resources and better living conditions are key to tackling tuberculosis,” ADB.ORG. Across such settings, case backlogs elevate demand for first- and second-line medicines, preserving volume growth for the anti-tuberculosis drugs market even where health budgets remain constrained.

Incidence Surge of MDR & XDR Strains

MDR-TB constitutes roughly 5% of all cases yet accounts for up to 20% of TB mortality, and genomic surveillance shows 28% of resistant strains spread person-to-person rather than arising de novo. Eastern Europe and parts of sub-Saharan Africa post the world’s highest MDR and XDR burden, while pre-XDR incidence is rising in Asia. Only 44% of diagnosed MDR-TB patients receive adequate therapy, underscoring the urgent need for pipeline innovation that keeps the anti-tuberculosis drugs market geared toward novel mechanisms of action.

Short-Course All-Oral Regimen Breakthroughs

WHO-endorsed 6-month BPaL/BPaLM protocols trim treatment time by up to 18 months and achieve near-90% success, a leap from historical 52%. India approved nationwide BPaLM use for an estimated 75,000 drug-resistant patients in 2024. Brazil and the Philippines are replicating large-scale rollout via peer-learning hubs coordinated by TB Alliance, signaling a structural tilt toward high-value oral combinations that reposition component suppliers within the anti-tuberculosis drugs market.

AI-Enabled Radiology Screening Adoption

AI-powered lung ultrasound surpasses human interpretation by 9 percentage points, delivering 93% sensitivity and 81% specificity in detection trials. Romania’s field deployment of AI-assisted mobile X-ray units among homeless communities illustrates real-world feasibility. These tools lower diagnostic latency in workforce-scarce regions and feed more confirmed patients into therapeutic channels, effectively lifting the addressable anti-tuberculosis drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse drug-related side-effects | -1.4% | Pediatric and elderly cohorts worldwide | Medium term (2-4 years) |

| High cost of MDR/XDR treatment | -1.8% | Low- and middle-income countries in Africa and Asia | Long term (≥ 4 years) |

| Lengthy treatment & poor adherence | -1.1% | Resource-limited settings globally | Medium term (2-4 years) |

| API supply-chain fragility (rifapentine) | -0.9% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse Drug-Related Side-Effects

First-line regimens trigger hepatotoxicity rates of up to 27% in children, with pyrazinamide and isoniazid most implicated[2]World Journal of Clinical Pediatrics, “Understanding antituberculosis drug-induced hepatotoxicity,” WJGNET.COM. Serious events such as rifampicin-induced acute kidney injury complicate management in chronic kidney disease patients. These safety concerns lead to regimen switches that undermine adherence and press innovators to pursue safer formulations, including early studies on rectal suppositories for severe digestive intolerance. Persistent toxicity risks cap uptake pace and weigh on the anti-tuberculosis drugs market growth potential.

High Cost of MDR/XDR Treatment

Median MDR-TB therapy costs USD 5,047 compared with USD 807 for drug-susceptible cases, pushing 29.9% of Thai households into catastrophic expenditure thresholds. Although bedaquiline prices dropped 55% through the Global Drug Facility, all-oral regimens still strain budgets in resource-constrained countries. High out-of-pocket exposure stalls timely initiation and tempers the anti-tuberculosis drugs market in several high-burden geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Novel Agents Drive Innovation

The anti-tuberculosis drugs market size for rifampin reached USD 462.3 million in 2025, translating into a 31.02% share that confirms its front-line status. Bedaquiline, however, is advancing at a 12.92% CAGR as clinicians pivot toward regimens that withstand resistance. Isoniazid and ethambutol retain therapeutic relevance yet face flat revenue prospects because of saturation and intolerance issues. Pretomanid accelerates through inclusion in WHO-backed BPaL protocols, while fluoroquinolone use decelerates in response to documented resistance patterns. Pipeline candidates such as TBAJ-876 and ganfeborole illustrate how next-generation compounds are shaping competitive hierarchies within the anti-tuberculosis drugs market. The WHO counts 28 active investigational agents, of which 18 are new chemical entities, highlighting a robust but still risk-laden discovery landscape.

Continued clinical progress underscores commercial opportunity. Johnson & Johnson’s JNJ-6640, a PurF inhibitor, demonstrates first-in-class potential. TB Alliance’s five-country Phase 2 evaluation of TBAJ-876 seeks to mitigate emerging bedaquiline resistance. As efficacy data matures, pricing negotiations with procurement facilities could unlock sizeable incremental volumes, especially in price-sensitive Middle-Income settings where anti-tuberculosis drugs market adoption historically trailed need.

By End User: Non-Profits Accelerate Access

Hospitals and clinics generated USD 668.5 million in anti-tuberculosis drugs revenue in 2025, equal to 44.87% share aided by centralised procurement and on-site diagnostics. Non-profit organisations, fuelled by Global Fund disbursements and Gates Foundation grants, are forecast to grow 9.97% annually through 2031, the fastest among end users. Public-private engagement models like Kerala’s STEPS and India’s Ni-kshay Mitras demonstrate how philanthropic partners augment last-mile delivery in underserved districts. Private diagnostic centres maintain mid-single-digit expansion as advanced molecular testing broadens customer mix, while mobile clinics extend service reach into conflict zones and nomadic communities, deepening the overall anti-tuberculosis drugs market penetration.

Strategically, NGOs now wield outsize influence over formulary choices, often insisting on BPaL/BPaLM procurement that favours newer agents. Their funding leverage pressures manufacturers to accept tiered pricing and spurs volume-based agreements through mechanisms such as the Global Drug Facility. For developers, tailored access programmes can yield reputational and market-share gains, but only if supply security is guaranteed amid sporadic active-pharmaceutical-ingredient shortages.

By Route of Administration: Oral Dominance Persists

Oral products booked 71.48% of global revenue in 2025 and are forecast to show the fastest 7.58% CAGR, buoyed by WHO approval of entirely oral six-month courses. Injectable routes serve critical-care niches, particularly for extensively resistant infections or gastrointestinal intolerance, yet their share shrinks as clinical guidelines move away from aminoglycoside-based combinations. Innovative inhalable microparticle systems and dry-powder triple combinations of pretomanid, moxifloxacin and pyrazinamide may create a hybrid administration class that improves pulmonary drug delivery while maintaining adherence simplicity. Such platforms offer differentiation levers for companies seeking to capture incremental slices of the anti-tuberculosis drugs market.

Parenteral therapy remains indispensable in intensive-care scenarios, and Brazil’s development of formal protocols for critically ill TB patients indicates continuing, if limited, demand. Manufacturers able to deliver ready-to-use injectables or long-acting depots can anchor specialised portfolios while diversifying risk away from first-line oral competition.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies held a 51.74% stake in 2025, driven by integrated care delivery and formulary control. Online pharmacies, though currently small, are growing 8.47% annually as pandemic-era behaviour changes endure. The SHOPS Plus pilot in India fulfilled 866 home deliveries during lockdown, proving digital fulfilment viable even where internet penetration is modest. Community drugstores continue to link patients with over-the-counter symptomatic relief, yet standard-of-care TB management at retail level remains uneven; a Pakistani mystery-shopping survey recorded guideline-compliant management in only 37.7% of visits. Governments are therefore drafting accreditation frameworks that could eventually funnel subsidised anti-tuberculosis drugs market volumes through vetted e-commerce portals.

For manufacturers, omni-channel strategies are pivotal. Direct-to-patient shipment programmes reduce leakage and may improve pharmacovigilance via embedded digital-adherence tools. Those capabilities, coupled with scaled procurement from central stockpiles, allow suppliers to counterbalance the volatility stemming from API bottlenecks that periodically impact hospital formularies.

Geography Analysis

North America contributes 41.96% of global revenue, reflecting advanced surveillance infrastructure, insurance reimbursement and the presence of contingency stockpiles to buffer shortages. The region’s elimination push among US-born populations targets incidence below 0.4 per 100,000 by 2025, fuelling uptake of preventive rifapentine regimens and high-specificity diagnostics. Yet supply-chain fragility persists: California’s 2023 stock-out of first-line orals prompted emergency central buffer deployment while Canada grappled with rifampin interruptions that risk underserving Indigenous communities. Mitigation protocols drive steady replenishment contracts that stabilise demand within the anti-tuberculosis drugs market.

Asia-Pacific is the fastest-growing cluster at 9.49% CAGR. India’s introduction of BPaLM for 75,000 patients and community sponsorship via more than 82,000 registered Ni-kshay Mitras illustrate public mobilization at scale. China’s spatio-temporal modelling foresees localised mortality rises by 2030 without intensified intervention. Indonesia participates in Phase 3 trials for the M72/AS01E vaccine candidate, cementing its status as a front-line innovation hub [WHO.INT]. Southeast Asia’s heavy 46% infection share plus uneven health access make the region pivotal to future anti-tuberculosis drugs market expansion.

Europe shows moderate growth but contends with rising paediatric incidence, up 10% to 38,993 cases across 29 EU/EEA countries in 2023. Treatment success remains at 67.9%, far below the 90% target, while MDR completion sits at 56%, sustaining latent demand for new regimens. Romania’s AI-assisted outreach and consortiums such as ERA4TB exemplify regional investment in next-generation regimens. Middle East and Africa markets are shaped by high drug-resistant burden and fragmented funding, yet price cuts for bedaquiline are improving affordability. South America, led by Brazil’s inter-ministerial TB elimination committee, displays rising procurement of oral combinations, creating fresh pull for the anti-tuberculosis drugs market.

Competitive Landscape

The anti-tuberculosis drugs market remains moderately fragmented yet tilts toward consolidation around innovators able to integrate therapy, diagnostics and digital adherence. Johnson & Johnson commands lead status via bedaquiline but relaxed patent enforcement in South Africa has narrowed its exclusivity corridor and lowered prices to USD 130 per course, undercut by Lupin’s USD 90 offering through the Global Drug Facility. TB Alliance curates the largest independent portfolio, leveraging Australian Government funding to operate the PeerLINC knowledge hub that accelerates regimen rollout across Asia.

Supply security emerged as a decisive differentiator after 2023’s isoniazid and rifampin shortages; firms with multi-source API contracts won emergency tenders and strengthened brand reliability. Biotechnology entrants focus on host-directed therapies and PurF- or leuRS-targeting small molecules, banking on orphan-disease incentives to offset development risk. Partnerships linking AI radiology start-ups with drug developers are proliferating: Fujirebio and Heidelberg University Hospital received a USD 6.9 million GHIT Fund grant to co-develop companion diagnostics that could speed treatment initiation.

Competitive intensity will likely sharpen as generic eligibility widens post-patent expiry and as governments exploit pooled procurement to demand deeper price concessions. Players able to back price discipline with robust pharmacovigilance data and digital adherence platforms are primed to defend share when procurement shifts from volume- to outcome-based metrics, extending their influence on the anti-tuberculosis drugs market structure.

Anti-tuberculosis Drugs Industry Leaders

Macleods Pharmaceuticals Ltd

Otsuka Pharmaceutical Co. Ltd

Sequella, Inc.

Lupin Limited

Johnson & Johnson (Janssen)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Australian Government awarded AUD 17 million to TB Alliance to enhance clinical research and establish the PeerLINC Knowledge Hub supporting the BPaL/M regimen rollout.

- February 2025: The Stop TB Partnership’s Global Drug Facility announced a 54% price reduction for bedaquiline supplied by Lupin and Macleods, lowering the cost to USD 90 per treatment course.

Global Anti-tuberculosis Drugs Market Report Scope

As per the scope of the report, Tuberculosis (TB) is a disease affecting the population across the world. Although tuberculosis is a curable disease, it remains one of the most common causes of death among adults, particularly in emerging economies. The Anti-tuberculosis drugs market is segmented by Drug Class (Isoniazid, Rifampin, Ethambutol, Pyrazinamide, Fluoroquinolones, Bedaquiline, Aminoglycosides, Thioamides, Cyclic Peptides, and Other Drug Classes), End User (Hospitals and Clinics, Government Agencies, Non-Profit Organizations, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Isoniazid |

| Rifampin |

| Ethambutol |

| Pyrazinamide |

| Fluoroquinolones |

| Bedaquiline |

| Pretomanid |

| Delamanid |

| Aminoglycosides |

| Thioamides |

| Cyclic Peptides |

| Other Drug Classes |

| Hospitals & Clinics |

| Non-Profit Organizations |

| Private Diagnostic Centers |

| Others |

| Oral |

| Injectable |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others (NGO & Donation Channels, Public Procurement & DOTS Programs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Isoniazid | |

| Rifampin | ||

| Ethambutol | ||

| Pyrazinamide | ||

| Fluoroquinolones | ||

| Bedaquiline | ||

| Pretomanid | ||

| Delamanid | ||

| Aminoglycosides | ||

| Thioamides | ||

| Cyclic Peptides | ||

| Other Drug Classes | ||

| By End User | Hospitals & Clinics | |

| Non-Profit Organizations | ||

| Private Diagnostic Centers | ||

| Others | ||

| By Route of Administration | Oral | |

| Injectable | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others (NGO & Donation Channels, Public Procurement & DOTS Programs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the anti-tuberculosis drugs market?

The anti-tuberculosis drugs market size reached USD 1.58 billion in 2026 and is forecast to grow to USD 2.13 billion by 2031.

Which region leads in revenue terms?

North America held 41.96% of global revenue in 2025, underpinned by strong procurement and strategic drug stockpiles.

Why are novel agents such as bedaquiline gaining traction?

Bedaquiline underpins WHO-endorsed six-month all-oral regimens that deliver near-90% success rates against drug-resistant TB, driving a 12.92% CAGR for that class.

How is digital transformation influencing distribution?

Online pharmacies are expanding at an 8.47% CAGR as e-pharmacy pilots prove effective in maintaining treatment continuity, especially during health-system disruptions.

What factors limit market growth?

Key restraints include high costs of MDR/XDR regimens, adverse drug reactions and periodic active-ingredient shortages that disrupt consistent supply.

Page last updated on: