Primary Biliary Cholangitis Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

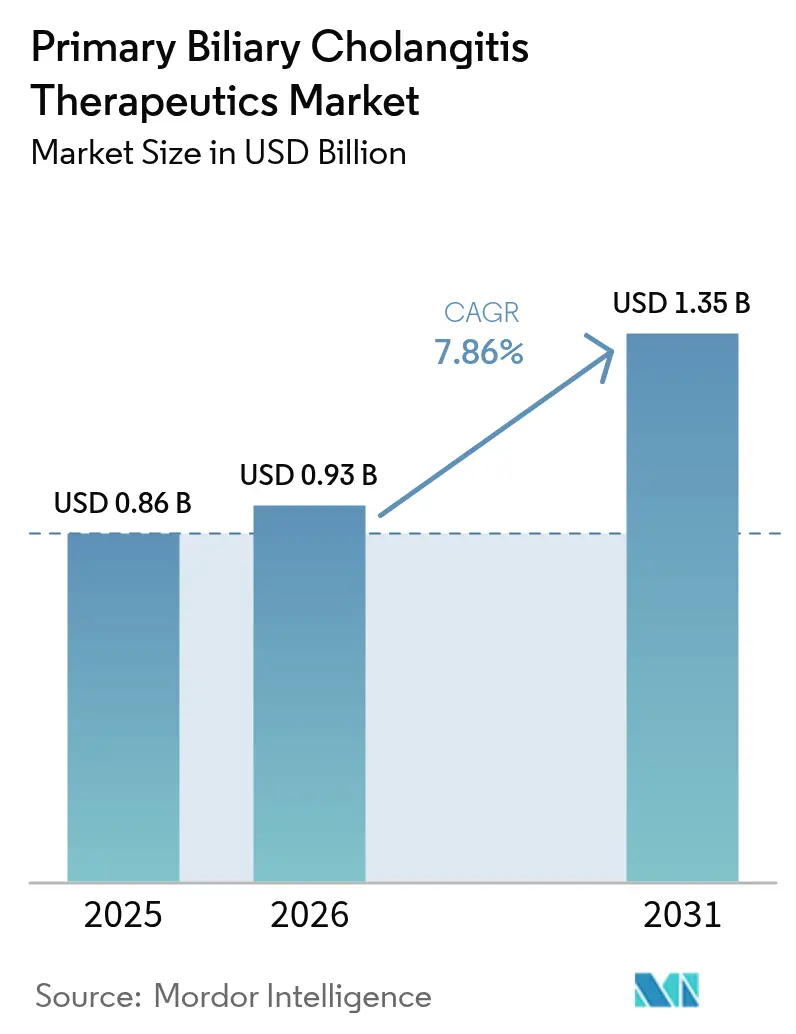

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players_Therapeutics_COmpanies.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Primary Biliary Cholangitis Therapeutics Market Analysis by Mordor Intelligence

The Primary Biliary Cholangitis Therapeutics Market size in 2026 is estimated at USD 0.93 billion, growing from 2025 value of USD 0.86 billion with 2031 projections showing USD 1.35 billion, growing at 7.86% CAGR over 2026-2031.

Robust growth is underpinned by the double approval of the PPAR agonists elafibranor and seladelpar, mounting real-world evidence that links biochemical response to transplant-free survival, and widening payer acceptance of surrogate endpoints in rare liver diseases. Competitive intensity is accelerating as legacy FXR agonists encounter safety-focused label constraints while newer mechanisms compete on pruritus relief and fatigue improvement. Online specialty pharmacy channels are scaling rapidly, diagnostic algorithms powered by artificial intelligence are shortening time to treatment, and combination therapy trials are expanding the eligible patient pool, collectively sustaining demand.

Key Report Takeaways

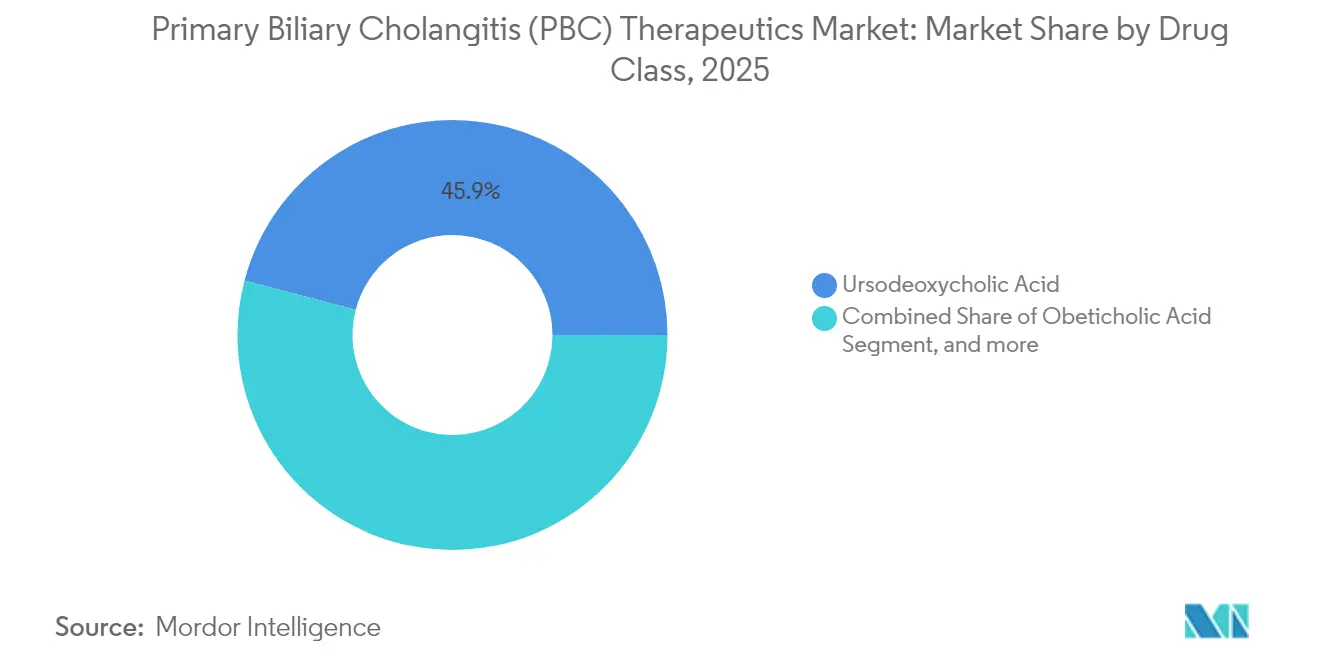

- By drug class, ursodeoxycholic acid led with 45.92% of the primary biliary cholangitis therapeutics market share in 2025; PPAR agonists are projected to advance at a 9.98% CAGR through 2031.

- By mechanism of action, FXR agonists held 38.75% of the primary biliary cholangitis therapeutics market size in 2025, while PPAR α/δ agonists recorded the fastest trajectory at 9.12% CAGR to 2031.

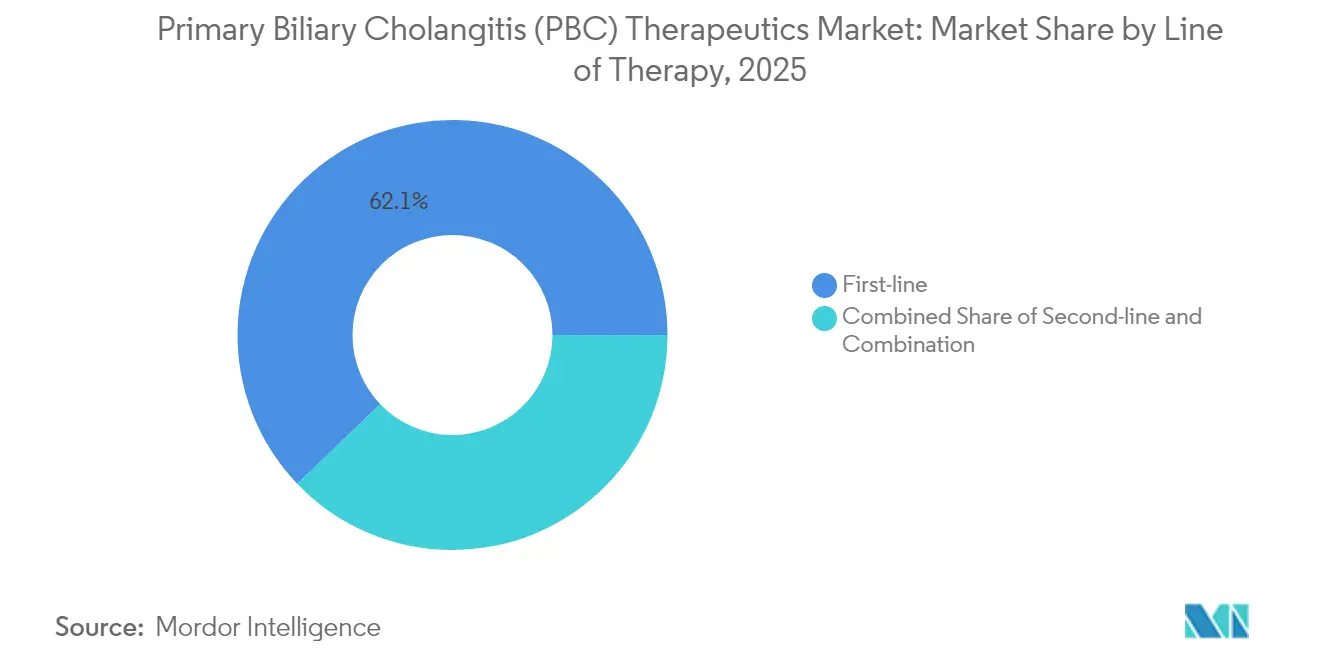

- By line of therapy, first-line treatments accounted for 62.15% of the primary biliary cholangitis therapeutics market size in 2025, whereas second-line options are rising at a 11.85% CAGR over the forecast period.

- By distribution channel, hospital pharmacies retained 53.60% revenue share in 2025; online pharmacies are expanding at 11.05% CAGR to 2031.

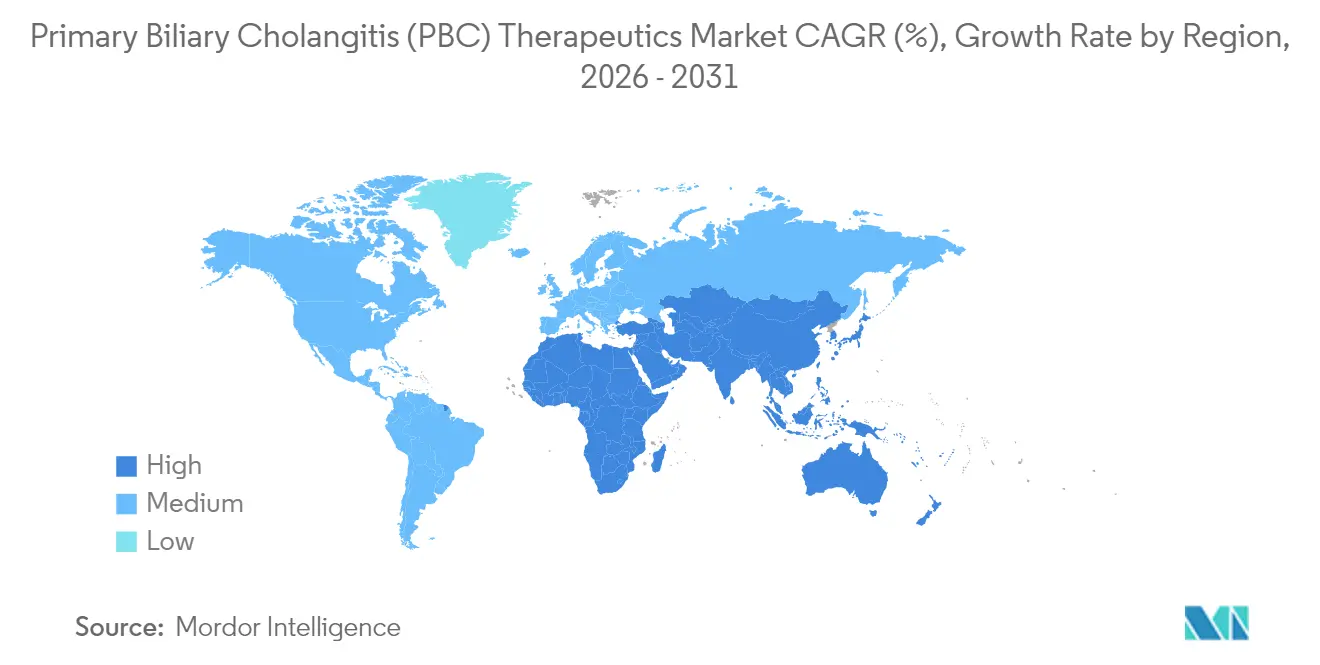

- By geography, North America commanded 37.42% revenue in 2025; Asia Pacific is on course for the highest 10.34% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Primary Biliary Cholangitis Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Label expansion of FXR agonists into compensated cirrhosis | +1.8% | North America, EU, APAC emerging | Medium term (2-4 years) |

| Accelerated approvals for PPAR agonists | +2.1% | Global, early US and EU uptake | Short term (≤2 years) |

| Optimized UDCA generics in cost-sensitive markets | +0.9% | Core APAC, spill-over MEA | Long term (≥4 years) |

| Real-world evidence supporting biochemical responders | +1.2% | Global | Medium term (2-4 years) |

| AI-driven early diagnosis | +1.4% | North America, EU, expanding APAC | Long term (≥4 years) |

| Growing clinical-trial activity in combination therapies | +0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Label Expansion of FXR Agonists into Compensated Cirrhosis

FXR agonists are moving beyond early-stage disease as regulators accept conditional evidence for cirrhotic PBC patients, a cohort representing roughly one-fifth of total cases.[1]U.S. Food & Drug Administration, “Gastrointestinal Drugs Advisory Committee Meeting Briefing Document,” fda.gov Hospitalization costs for compensated cirrhosis average USD 113,567 annually, more than double non-cirrhotic spending, establishing a strong pharmacoeconomic rationale for early FXR use. Real-world datasets indicate that biochemical improvements translate into better transplant-free survival, attracting payer endorsement. Uptake could be tempered by hepatic decompensation risks, necessitating structured monitoring programs and specialist oversight. As tertiary centers refine patient-selection algorithms, the primary biliary cholangitis therapeutics market gains a sizable incremental revenue stream.

Accelerated Approvals for PPAR Agonists

The 2024 FDA clearances for seladelpar and elafibranor shortened development cycles by relying on alkaline phosphatase normalization instead of long-term mortality endpoints.[2]Gilead Sciences, “Completion of Acquisition of CymaBay,” gilead.com Seladelpar’s 25% complete biochemical response and clinically significant itch reduction have redefined treatment goals, differentiating the class from FXR agonists. Premium U.S. pricing USD 12,606 per month for seladelpar and USD 11,500 for elafibranor supports robust revenue despite the orphan-sized patient base. European conditional authorizations mirror U.S. flexibility and establish a global commercial runway. Rapid label updates are expected once confirmatory trials mature, reinforcing the growth trajectory of the primary biliary cholangitis therapeutics market.

Optimized UDCA Generics Penetrating Cost-Sensitive Markets

Second-generation UDCA formulations and vitamin D combinations are proliferating, achieving 80% responder rates compared with 50% for UDCA alone and supporting wider access in health-budget-constrained regions.[3]National Library of Medicine, “Effectiveness of UDCA-Vitamin D Combination,” pubmed.ncbi.nlm.nih.gov Regulators in Asia-Pacific now accept foreign clinical data, cutting launch timelines for generics. Competitive pricing and decades-long safety familiarity make optimized UDCA indispensable within universal-coverage frameworks. Although these entrants compress margins, they expand treated prevalence, indirectly lifting total therapy volume in the Primary Biliary Cholangitis Therapeutics market.

Real-World Evidence Supporting Biochemical Responders

Registries from Canada and Europe show 39% of obeticholic acid recipients achieving composite endpoints by month 12, strengthening confidence in post-marketing effectiveness. Integration of GLOBE and UK-PBC scores into electronic health records enables earlier risk stratification and timely therapy escalation. Payers increasingly reimburse newer agents once real-world biochemical data demonstrate downstream clinical benefit. As datasets grow, evidence-backed treatment algorithms will shorten therapeutic inertia, raising prescription volumes across the Primary Biliary Cholangitis Therapeutics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pruritus risk with high-dose FXR agonists | -1.6% | Global, pronounced in Asian cohorts | Short term (≤2 years) |

| Myopathy-linked discontinuation of fibrates | -0.8% | Global, higher in elderly | Medium term (2-4 years) |

| Lack of transplant-free survival endpoints | -1.2% | Global, prolonging approvals | Medium term (2-4 years) |

| Limited awareness among general practitioners | -0.9% | Emerging markets, rural settings | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Pruritus Risk with High-Dose FXR Agonists

Severe itching affects 41% of obeticholic acid users and drives 17% discontinue. IL-31 overexpression is implicated, and current antipruritic regimens deliver incomplete relief. Asian populations show higher susceptibility, limiting regional uptake. Clinicians consequently weigh symptom burden against biochemical gains, slowing switching from UDCA. Ongoing trials of next-generation FXR agonists claim lower pruritus incidence, but any delay in commercial availability restrains the Primary Biliary Cholangitis Therapeutics market in the near term.

Myopathy-Linked Discontinuation of Fibrates

Bezafibrate improves transplant-free survival metrics yet carries myopathy risk, especially among women over 40 on concurrent statins. Routine creatine kinase monitoring raises caregiver burden, and documented adverse events deter prescribers in community settings. Although cost-effective, fibrates remain under-utilized, ceding share to costlier but better-tolerated PPAR agonists. Safety concerns therefore cap fibrate contribution to the Primary Biliary Cholangitis Therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: UDCA Dominance Faces PPAR Challenge

Ursodeoxycholic acid controlled 45.92% revenue in 2025, reflecting its entrenched first-line status and affordability. However, PPAR agonists are expanding at 9.98% CAGR, buoyed by dual biochemical and symptomatic gains that resonate with prescribers. Obeticholic acid retains a loyal niche for UDCA non-responders but confronts safety-label baggage that limits future momentum. Fibrates, though economical, remain constrained by myopathy vigilance. Other investigational classes, including anti-fibrotic and immunomodulatory agents, are unlikely to influence the Primary Biliary Cholangitis Therapeutics market size materially before 2030, given early-phase maturity.

Continued generic erosion keeps UDCA price points low, securing access across health-economically constrained regions while synergies with vitamin D formulations bolster response rates. In contrast, seladelpar’s USD 12,606 monthly list supports premium positioning among refractory patients with debilitating itch, demonstrating the bifurcation of the Primary Biliary Cholangitis Therapeutics market between cost-sensitive and innovation-premium tiers. Combination therapy trials may ultimately blur drug-class demarcations, yet near-term dynamics remain shaped by UDCA’s volume and PPAR’s value contributions.

By Mechanism of Action: FXR Leadership Challenged by PPAR Innovation

FXR agonists accounted for 38.75% of the primary biliary cholangitis therapeutics market size in 2025, propelled by obeticholic acid’s earlier entry. Nonetheless, pruritus-driven discontinuations expose a vulnerability that PPAR α/δ agonists are exploiting with a forecast 9.12% CAGR. Bile-acid modulators, chiefly UDCA, deliver steady incremental growth, particularly in Asia-Pacific. Investigational pathways such as NADPH oxidase inhibition and IL-31 targeting promise longer-term diversification but lack near-commercial impact.

Mechanistic plurality is reshaping physician algorithms: FXR agonists deliver alkaline phosphatase declines, while PPAR agonists attenuate itch and fatigue. Real-world evidence advocates sequential or concurrent use, intensifying combination-therapy research. As safety-tuned next-generation FXR compounds enter phase 3, incumbents must refine risk-management protocols to defend share in the evolving primary biliary cholangitis therapeutics market.

By Line of Therapy: Second-Line Surge Drives Innovation

First-line regimens captured 62.15% revenue in 2025, fortifying UDCA’s central role at diagnosis. Yet rising recognition of incomplete biochemical response documented in up to 40% of patients catalyzes second-line uptake at a 11.85% CAGR. PPAR and FXR agonists now anchor escalation pathways, aligned with prognostic scores that flag high-risk profiles earlier.

Combination therapy is the fastest-expanding niche, supporting a personalized approach where mechanisms are layered to meet both laboratory and quality-of-life endpoints. This paradigm accelerates revenue diversification within the primary biliary cholangitis therapeutics market.

By Distribution Channel: Hospital Dominance Meets Digital Disruption

Hospital pharmacies commanded 53.60% sales in 2025 owing to complex initiation protocols and hepatology oversight. Specialty-center distribution ensures pharmacovigilance for high-risk profiles, yet shifts in chronic-disease management favor longer-term dispensing through digital channels.

Online pharmacies are gaining 11.05% CAGR as integrated tele-pharmacy platforms coordinate adherence monitoring and side-effect triage. Retail pharmacies remain relevant for generic UDCA but play a minor role for premium agents. As artificial-intelligence-enabled refill reminders and virtual nurse coaching mature, the Primary Biliary Cholangitis Therapeutics market is set to experience channel realignment toward home-delivery models.

Geography Analysis

North America’s 37.42% revenue share in 2025 stems from orphan-drug incentives, comprehensive insurance coverage, and rapid FDA accelerated approvals that expedited seladelpar and elafibranor launches. Widespread adoption of AI-powered diagnostic scoring in tertiary centers enhances early detection, further enlarging the treated cohort. Real-world registries such as the Canadian PBC Network validate effectiveness and inform reimbursement, tightening the evidence loop that fuels regional growth.

Europe follows with harmonized clinical guidelines and conditional marketing pathways that balance early access with post-authorization evidence demands. Approximately 163,000 diagnosed patients across the bloc provide scale for specialty-pharmacy programs. Health-technology-assessment bodies emphasize cost-utility, yet willingness-to-pay thresholds rise when therapies prevent future transplantation costs. Academic-industry collaboration remains prolific, accelerating combination-therapy trials that extend the franchise of approved agents.

Asia-Pacific is the fastest-growing territory, projected at 10.34% CAGR, driven by expanding universal health schemes and demographic aging that heightens autoimmune liver disease prevalence. Japan’s mature reimbursement system enables swift penetration of premium PPAR agonists, while China’s volume-based procurement favors optimized UDCA generics yet increasingly covers high-value orphan drugs. Regional acceptance of foreign pivotal data expedites entry timelines. The deployment of AI-enabled screening tools, especially in urban Chinese hospitals, amplifies patient capture, reinforcing long-term expansion of the Primary Biliary Cholangitis Therapeutics market.

Competitive Landscape

The field remains moderately concentrated as top players leverage differentiated mechanisms, real-world evidence portfolios, and patient-support ecosystems. Gilead’s USD 4.3 billion acquisition of CymaBay in 2024 secured seladelpar and endowed Gilead with a hepatology franchise complementary to its antiviral heritage. Ipsen and Genfit partnered on elafibranor, jointly promoting fatigue-relief data that broaden prescriber appeal. Intercept Pharmaceuticals retains FXR first-mover advantage yet must navigate pruritus mitigation strategies or risk share erosion.

Emergent competitors pursue the combination-therapy space; clinical-stage firms studying anti-fibrotics (e.g., setanaxib) target refractory symptoms, potentially entering add-on regimens. Digital-health alliances between pharmaceutical companies and specialty-pharmacy providers support virtual adherence coaching, a critical differentiator in chronic rare diseases. Patent estates around seladelpar and elafibranor afford exclusivity into the next decade, allowing strategic pricing while patient-access foundations expand.

Strategic imperatives increasingly center on real-world evidence generation and physician-support tools. Registries capturing biochemical and symptom metrics underpin value dossiers in mature markets and facilitate emerging-market payer negotiations. Companies integrating AI diagnostic modules within electronic medical records improve patient identification, forging brand affinity within provider networks. These initiatives collectively reinforce competitive positioning across the primary biliary cholangitis therapeutics market.

Primary Biliary Cholangitis Therapeutics Industry Leaders

Allergan Inc.

Glenmark Pharmaceuticals

Intercept Pharmaceuticals

Teva Pharmaceutical Industries

Viatris (Mylan)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Umecrine Cognition announced it had successfully raised SEK 24.6 million through a convertible loan with attached share options, directed to a consortium of long-term shareholders and investors including Karolinska Development, AB Ility, and Ribbskottet AB. The funding will be used to advance the company’s ongoing Phase 1b/2a clinical study of golexanolone, a novel therapeutic candidate for primary biliary cholangitis (PBC). Golexanolone represents a new class of drugs targeting chronic neuroinflammation, a condition that disrupts normal nerve signaling and contributes to debilitating symptoms such as impaired cognition and severe fatigue.

- May 2025: Ipsen unveiled new clinical data from two late-breaking presentations at the European Association for the Study of the Liver (EASL) congress, further reinforcing the therapeutic value of IQIRVO (elafibranor) in treating Primary Biliary Cholangitis (PBC). The additional analyses from the ELATIVE study (LBP-027) demonstrated that patients treated with IQIRVO experienced significantly greater improvements in fatigue compared to those receiving placebo after 52 weeks of treatment.

Global Primary Biliary Cholangitis Therapeutics Market Report Scope

Primary biliary cholangitis also known as primary biliary cirrhosis is an autoimmune disease of the liver. This results from the slow and progressive destruction of the biliary cells. Currently, a limited number of therapeutics are approved for the treatment of primary biliary cholangitis.

| Ursodeoxycholic Acid |

| Obeticholic Acid |

| PPAR Agonists |

| Fibrates |

| Other Drug Class |

| FXR Agonists |

| PPAR α/δ Agonists |

| Bile-acid Modulators |

| Anti-Fibrotic Agents |

| Immunomodulators |

| First-line |

| Second-line |

| Combination |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Ursodeoxycholic Acid | |

| Obeticholic Acid | ||

| PPAR Agonists | ||

| Fibrates | ||

| Other Drug Class | ||

| By Mechanism of Action | FXR Agonists | |

| PPAR α/δ Agonists | ||

| Bile-acid Modulators | ||

| Anti-Fibrotic Agents | ||

| Immunomodulators | ||

| By Line of Therapy | First-line | |

| Second-line | ||

| Combination | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the primary biliary cholangitis therapeutics market by 2031?

The market is projected to reach USD 1.35 billion by 2031.

Which drug class is growing fastest in primary biliary cholangitis therapeutics therapy?

PPAR agonists are expanding at a 9.98% CAGR through 2031, the highest among all classes.

Why are PPAR agonists significant for treating PBC?

They deliver both biochemical normalization and meaningful pruritus reduction, addressing key unmet needs.

Which region shows the fastest growth for PBC treatments?

Asia-Pacific records a 10.34% CAGR, driven by broader insurance coverage and improved diagnostics.

How is artificial intelligence influencing PBC management?

AI tools shorten diagnostic timelines and help identify high-risk patients, expanding the treated population.

What safety concern limits FXR agonist uptake?

High-dose FXR agonists are linked to severe pruritus, causing notable discontinuation rates.

Page last updated on: