Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.44 Billion |

| Market Size (2026) | USD 16.35 Billion |

| Market Size (2031) | USD 21.79 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Diabetes Drugs Market Analysis by Mordor Intelligence

Europe diabetes drugs market size in 2026 is estimated at USD 16.35 billion, growing from 2025 value of USD 15.44 billion with 2031 projections showing USD 21.79 billion, growing at 5.90% CAGR over 2026-2031. Demand is expanding as obesity and diabetes care converge, especially through the broad uptake of GLP-1 receptor agonists that serve both indications.[1]European Medicines Agency, “EU Actions to Tackle Shortages of GLP-1 Receptor Agonists,” ema.europa.euOral anti-diabetics dominate the treatment mix and are also the fastest-growing class, thanks to SGLT-2 inhibitors and the emergence of oral GLP-1 tablets. Early intervention programs are expanding the addressable patient base, most visibly in the pre-diabetes cohort where screening initiatives are now mainstream across many health systems. Supply security has come under scrutiny as biosimilar insulin erodes prices and GLP-1 shortages expose production bottlenecks, prompting regulatory coordination at EU level. Digital transformation is accelerating distribution shifts toward online channels and is paving the way for hybrid therapy models that pair medicines with approved digital therapeutics.[2]Nature, “Glucose-Sensitive Insulin with Attenuation of Hypoglycaemia,” nature.com

Key Report Takeaways

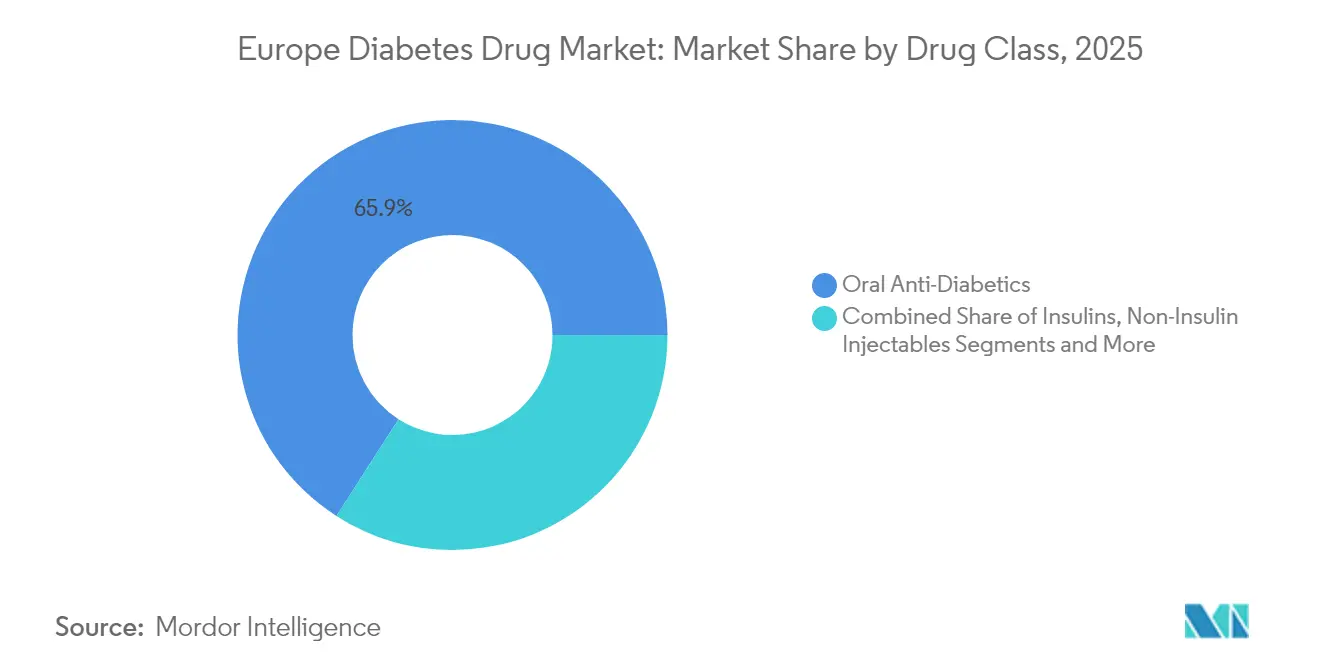

- By drug class, oral anti-diabetics led with 65.92% revenue share in 2025, while also recording the highest projected CAGR at 6.55% to 2031.

- By diabetes type, type 2 diabetes held 89.72% of the Europe diabetes drugs market share in 2025; the pre-diabetes segment is forecast to expand at a 7.05% CAGR through 2031.

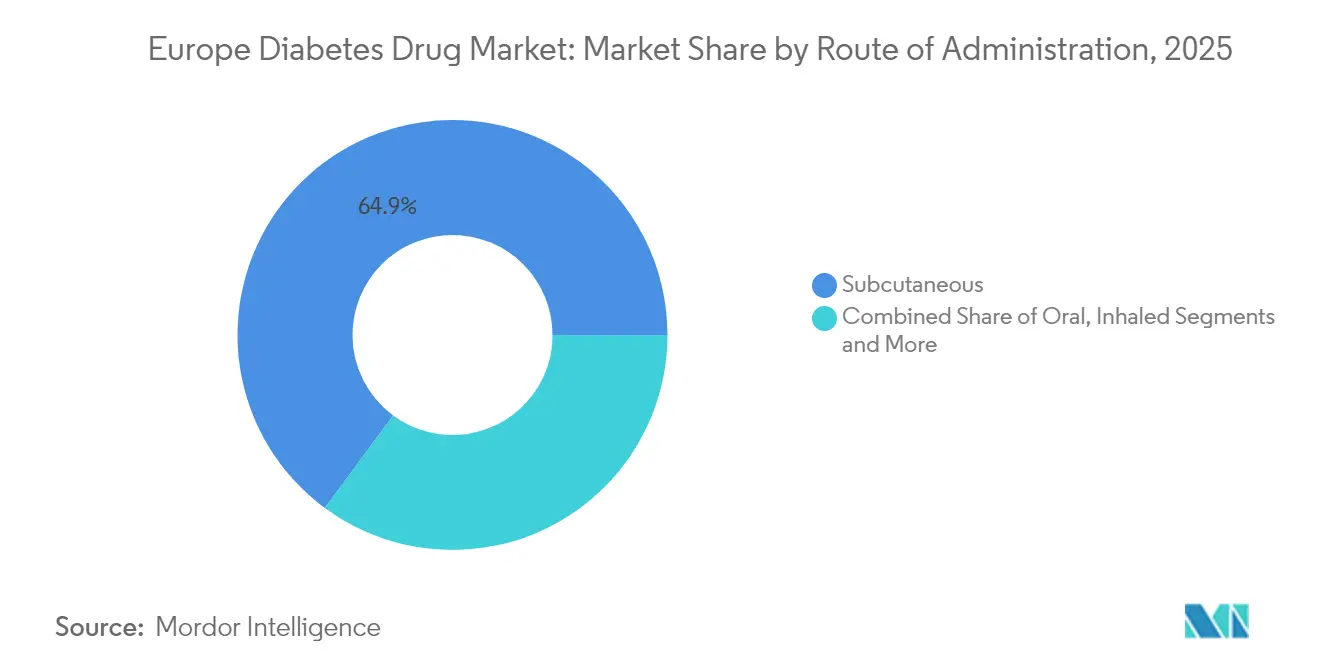

- By route of administration, subcutaneous injections accounted for 64.88% share of the Europe diabetes drugs market size in 2025 and implantable or transdermal systems are advancing at an 8.25% CAGR to 2031.

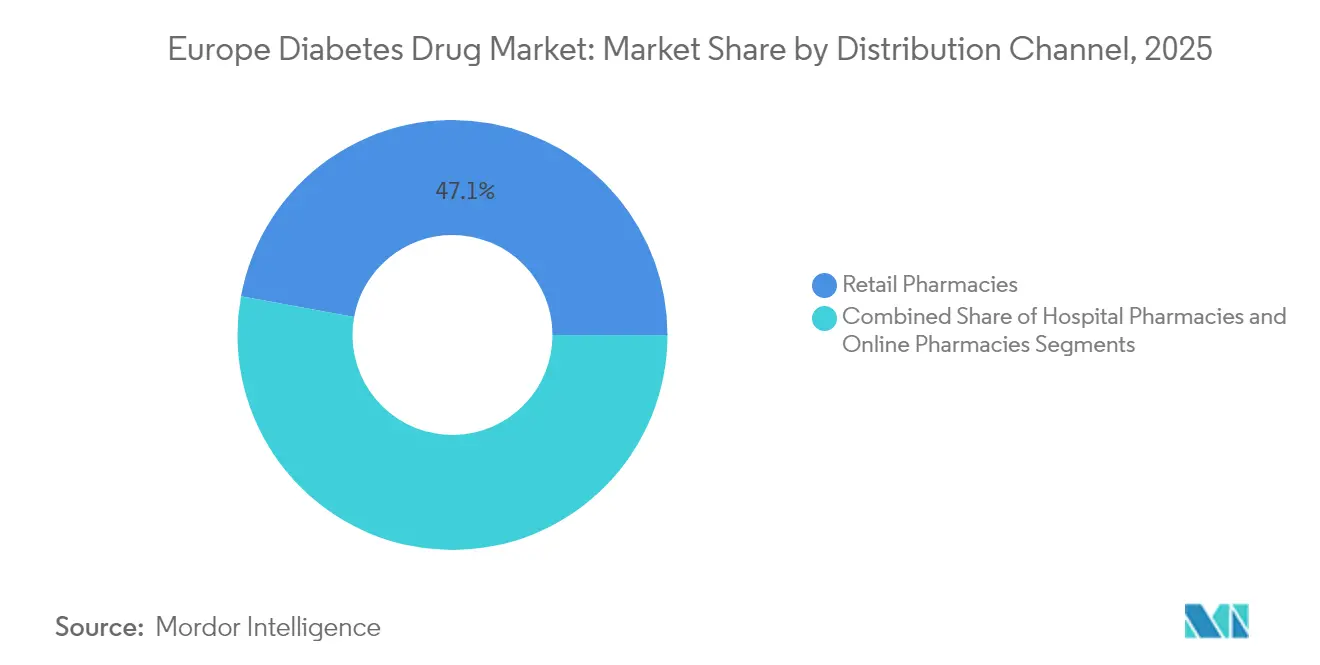

- By distribution channel, retail pharmacies controlled 47.12% of 2025 sales, whereas online pharmacies show the strongest momentum with a 8.60% CAGR to 2031.

- By geography, Germany commanded 22.10% of revenues in 2025, while France leads growth with a 6.45% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Burden of Diabetes and GLP-1 obesity cross-over demand surge | 1.5% | Global Europe, strongest in Germany, UK, France | Medium term (2-4 years) |

| Digital-therapeutic bundling with e-prescriptions | 1.2% | Germany, Nordic countries, expanding to Western Europe | Short term (≤ 2 years) |

| EU-wide early CKD screening guidelines | 0.8% | All EU member states, priority in aging populations | Long term (≥ 4 years) |

| Biosimilar insulin price-competition wave | 0.6% | Pan-European, strongest impact in price-sensitive markets | Medium term (2-4 years) |

| ESG-linked formulary tenders by payers | 0.4% | Western Europe, Nordic countries leading adoption | Long term (≥ 4 years) |

| Oral small-molecule insulin breakthroughs | 0.3% | Research hubs: Denmark, Switzerland, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burden of Diabetes and GLP-1 Obesity Cross-over Demand Surge

Escalating prevalence of both diabetes and obesity is reshaping therapy priorities, and GLP-1 receptor agonists sit at the epicenter of this shift. Italy’s 2024 spending on GLP-1 drugs reached EUR 26 billion, while Greece posted an 82.5% usage spike, reinforcing the medicines’ dual-indication appeal. Surging demand triggered shortages across multiple member states, prompting Belgium to restrict prescriptions temporarily and Germany to weigh export curbs. The European Medicines Agency responded by mandating capacity plans and clarifying off-label use boundaries, demonstrating how one therapeutic class can influence regional policy. Pharma manufacturers are accelerating scale-up projects, yet persistent supply constraints hint at a multiyear balancing act between escalating demand and production capabilities. As treatment algorithms now integrate weight and cardio-renal outcomes, the GLP-1 surge will continue to redirect R&D focus toward multi-agonist and oral delivery formulations.

Digital-Therapeutic Bundling with E-Prescriptions

Germany’s DiGA pathway reimburses 53 digital therapeutics, with diabetes applications making up a substantial share. One-year real-world studies show 89% of type 2 patients reached HbA1c targets below 7% and reduced medication use by 74%, underlining clinical value beyond lifestyle coaching. Performance-based payment models tie reimbursement to measurable outcomes, motivating developers to refine algorithms and user interfaces. Physician interviews, however, highlight onboarding hurdles ranging from time constraints to digital literacy assessments, suggesting that workflow integration will be decisive for broader adoption. Success in Germany is spurring replication across Nordic markets and Western Europe, and pharmaceutical firms increasingly view digital tools as complementary revenue streams that improve persistence on therapy.

EU-wide Early CKD Screening Guidelines

The latest cardio-renal guidelines call for routine chronic kidney disease screening in patients with diabetes; yet registry data reveal that under half of eligible Europeans receive annual tests.[3]BMC Nephrology, “CKD Screening in Patients with Diabetes,” bmcnephrol.biomedcentral.com The screening gap unlocks latent demand for SGLT-2 inhibitors and GLP-1 drugs with proven renal benefits, tilting prescribing toward agents demonstrated to reduce both kidney and cardiovascular events. New reimbursement incentives now link formulary inclusion to cardio-renal outcomes, accelerating uptake of combination therapies. Remote sample collection kits and AI-assisted risk scoring are aligning with screening drives, promising to lift diagnosis rates over the next decade. Long-term gains in quality-adjusted life years strengthen the economic case for earlier pharmacologic intervention.

Biosimilar Insulin Price-Competition Wave

Twenty-eight European countries record a median 21.6% fall in insulin glargine prices after biosimilar entry, creating budget headroom for next-generation therapies. Multi-winner tenders and sustainable procurement designs are now best practice, with Latvia registering the steepest 42.3% price drop. Originator firms are doubling down on weekly insulin icodec and glucose-sensitive formulations to defend margins, pivoting the competitive contest from price to convenience and safety. As insulin becomes less profitable, resource allocation in R&D will skew toward innovative modalities capable of commanding premium pricing and differentiated reimbursement status. Meanwhile, emerging manufacturers capitalize on biosimilar experience to enter higher-value biologics segments, broadening the supplier base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| API supply-chain over-reliance on China | -0.9% | Pan-European, critical for generic manufacturers | Short term (≤ 2 years) |

| GLP-1 capacity bottlenecks & allocation caps | -0.7% | All major European markets, acute in Germany, UK | Short term (≤ 2 years) |

| Rising SGLT-2 DKA safety warnings | -0.5% | EU-wide regulatory impact, clinical practice changes | Medium term (2-4 years) |

| Decentralised healthcare budget austerity | -0.4% | Southern and Eastern Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

API Supply-Chain Over-Reliance on China

The COVID-19 pandemic exposed Europe’s dependence on Chinese active pharmaceutical ingredient plants, a vulnerability that remains unresolved despite public-sector calls for reshoring. High capital costs, specialist talent shortages, and complex regulation hamper local build-out. Novo Nordisk’s USD 2.3 billion expansion in Denmark will add domestic capacity from 2029, yet semaglutide remains excluded from the build. In the interim, any disruption—geopolitical or pandemic-related—can curtail generic metformin or insulin supply, forcing health systems to activate emergency procurement protocols.

GLP-1 Capacity Bottlenecks & Allocation Caps

Manufacturing lead times for peptide therapeutics exceed 18 months, and surging global demand outpaces the scale-up curve, resulting in recurring stock-outs across Europe. Several countries introduced prescription rationing and export bans to protect domestic supply, underscoring systemic fragility. Pharma leaders are investing in additional bioreactors and modular fill-finish lines, yet capacity remains tight, limiting sales growth for GLP-1 products in the short term. Allocation policies may also delay launches of next-generation multi-agonists, tempering topline expansion for the Europe diabetes drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Oral Dominance Drives Innovation

Oral anti-diabetics captured 65.92% of total 2025 sales within the Europe diabetes drugs market, and this segment is forecast to expand at a 6.55% CAGR through 2031, maintaining its leadership as new SGLT-2 and oral GLP-1 agents gain traction. The Europe diabetes drugs market size for oral treatments is set to widen further as convenience, adherence, and superior outcome data drive prescribing. Non-insulin injectables, anchored by GLP-1 analogues, remain the second-largest class; however, their growth is capped by ongoing shortages that national regulators continue to manage through rationing. Insulin revenue is under pressure from biosimilar erosion, but innovation in once-weekly and glucose-sensitive preparations offers a potential rebound by the late 2020s. In addition, dual agonists such as tirzepatide demonstrated HbA1c reductions up to 2.06% and double-digit weight losses in clinical studies, signalling another wave of therapy upgrades.

Emerging multi-agonists and glucose-responsive insulins could redefine the therapeutic hierarchy. Investigational pairing of cagrilintide with semaglutide achieved 14 kg weight loss and 1.8% HbA1c decline over 12 weeks, outperforming most available regimens. Such efficacy encourages payer openness to higher list prices when demonstrable cost offsets in cardiovascular and renal events are evident. Meanwhile, glucose-sensitive candidates like NNC2215 show promise in mitigating hypoglycemia risk, a key determinant of therapy persistence. Overall, R&D pipelines suggest that the Europe diabetes drugs market will remain innovation-intensive, even as biosimilars put legacy molecules under long-term pricing strain.

By Diabetes Type: Type 2 Dominance with Pre-Diabetic Emergence

Type 2 diabetes represents 89.72% of 2025 spending within the Europe diabetes drugs market, reflecting demographic aging and lifestyle patterns across the continent. Yet, the pre-diabetic category is rising faster, at a 7.05% CAGR, as early detection programs enlarge intervention windows and favor lower-dose or lifestyle-linked therapies. Europe diabetes drugs market size projections for prevention indicate significant headroom: guideline adherence to annual HbA1c and kidney screening remains below 50% in several countries, implying growth potential once compliance improves. Type 1 diabetes, while comparatively small, is experiencing technology-driven shifts toward closed-loop insulin delivery, which may curb dose requirements and influence long-term drug volumes.

Prevention economics has become more persuasive to policymakers, with cost-effectiveness analyses favoring funded digital coaching platforms ahead of pharmacologic escalation. Clinical guidelines updated in 2023 recommend GLP-1 and SGLT-2 agents where cardio-renal benefit is proven, reinforcing migration toward class-leading molecules. This shift supports premium pricing for drugs with multi-organ protection attributes, anchoring future revenue diversity for the Europe diabetes drugs market.

By Route of Administration: Injectable Innovation Accelerates

Subcutaneous products dominate with 64.88% share of the Europe diabetes drugs market size in 2025, yet long-acting derivatives such as insulin icodec are improving convenience and could slow patient migration to oral alternatives. Implantable and transdermal systems hold the smallest share today but are expected to achieve the highest CAGR of 8.25% as mini-pumps and microneedle patches commercialize. Oral insulin candidates leveraging nanotechnology passed mid-stage trials in 2025, suggesting that technological hurdles—acid degradation and first-pass metabolism—can be overcome.

Inhaled insulin remains niche, constrained by device complexity and patient selection criteria, yet it continues to demonstrate value for needle-phobic individuals. The introduction of glucose-responsive, implantable depots may further tilt the balance away from multiple daily injections once real-world data secure payer confidence. Overall, administration preferences are converging on less-frequent, physiology-responsive delivery, sustaining high innovation intensity within the Europe diabetes drugs market.

By Distribution Channel: Digital Transformation Accelerates

Retail pharmacies retain 47.12% share of 2025 revenues, but online channels are growing at 8.60% CAGR as e-prescription coverage widens and telemedicine proliferates. Hospital pharmacies remain critical for complex insulin initiations, though outpatient migration continues as community providers acquire the necessary clinical competencies. Europe diabetes drugs market share in digital channels benefits from consumer preference for convenience and competitive pricing, as well as from chronic therapy adherence programs embedded into mobile apps.

Regulatory environments are evolving: Germany’s e-prescription mandate from 2024 embeds online fulfilment into standard care pathways, and Poland’s telemedicine boom shows how smaller markets can leapfrog to digital models. Brick-and-mortar pharmacies are responding with click-and-collect services, medication lockers, and integration of digital coaching. The distribution shift underscores that convenience and data-driven adherence support are now key differentiators in the Europe diabetes drugs industry.

Geography Analysis

Germany continues as the largest single contributor to the Europe diabetes drugs market, owing to structured disease-management programs, nationwide e-prescriptions, and strong diagnostic penetration. GLP-1 demand outstrips reimbursement limits, fostering a sizable private-pay segment, while DiGA-linked outcome contracts may catalyze wider payer adoption of hybrid therapy models. France gains momentum from decisive reimbursement approvals and domestic manufacturing expansion, factors that reduce supply risk and shorten time to market for advanced biologics.

In the United Kingdom, the NHS commitment to finance weight-management injectables underscores alignment between obesity reduction and diabetes complication avoidance, though fiscal impact will require phased implementation. Italy and Spain show growth despite budget pressures, leveraging regional procurement hubs that negotiate competitive biosimilar insulin contracts. Smaller Central and Eastern European markets display delayed access, reflecting variable HTA capacity and localized economic constraints, yet EU centralized approvals ensure eventual availability of novel agents.

Competitive Landscape

Market concentration remains moderate as Novo Nordisk, Sanofi, and Eli Lilly sustain leading positions through portfolio breadth and continuous R&D. Biosimilar insulin entrants have compressed prices rapidly, forcing originators to pivot toward weekly formulations and glucose-sensitive variants that justify premium reimbursement. Strategic alliances are increasing: Roche partnered with Zealand Pharma in a USD 5.3 billion accord to develop petrelintide, illustrating how big pharma taps biotech innovation to enlarge metabolic pipelines.

White-space opportunities center on oral insulin, AI-enabled glucose monitoring, and multi-agonist peptides. CE-marked smart sensors such as Roche’s SmartGuide signal convergence of diagnostics and therapeutics, offering differentiation via predictive analytics. Supply chain resilience is becoming a competitive parameter; firms with in-region API or formulation capabilities can secure preferential contracts when shortages loom. Meanwhile, biosimilar producers leverage tender know-how to pursue higher-margin biologics, adding diversity to the competitive roster and restraining oligopolistic tendencies in the Europe diabetes drugs market.

Europe Diabetes Drugs Industry Leaders

Eli Lilly

Astrazeneca

Novo Nordisk

Sanofi

Boehringer Ingelheim

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Feburary 2025: Biocon launched liraglutide in the United Kingdom under the brands Liraglutide Biocon and Biolide for diabetes and weight management.

- May 2024: Sanofi committed over EUR 1 billion to expand French biomanufacturing, including facilities for TZield and monoclonal antibody capacity.

- April 2024: Eli Lilly secured EU approval for tirzepatide (Mounjaro) across diabetes and weight-management indications.

- March 2024: The European Commission granted marketing authorization for insulin icodec (Awiqli), delivering once-weekly dosing for type 1 and type 2 patients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe diabetes drugs market as prescription-only and reimbursable pharmaceutical preparations that lower blood glucose, including insulins, non-insulin injectables, and oral anti-diabetic agents that have marketing authorization in one or more EU-27, UK, EFTA, or EEA states. Products used exclusively for diagnostics, nutritional supplements, herbal adjuvants, and diabetes-care devices are outside the scope.

Scope exclusion: over-the-counter nutraceuticals and blood-glucose reagents are not sized herein.

Segmentation Overview

- By Drug Class

- Insulins

- Basal/Long-acting

- Bolus/Fast-acting

- Human traditional

- Biosimilar

- Oral Anti-diabetics

- Biguanides

- SGLT-2 inhibitors

- DPP-4 inhibitors

- Sulfonylureas

- Non-Insulin Injectables

- GLP-1 RAs

- Amylin Analogues

- Combination Drugs

- Insulins

- By Diabetes Type

- Type-1

- Type-2

- By Route of Administration

- Oral

- Sub-cutaneous Injection

- Inhaled

- Implantable/Transdermal

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed European endocrinologists, hospital pharmacists, payor advisers, and marketing leaders across Germany, France, Italy, Spain, the Nordics, and CEE. These conversations clarified real-world treatment mix shifts, insulin biosimilar uptake, and anticipated GLP-1 access hurdles, letting us fine-tune channel splits and average selling prices that desktop sources alone could not reveal.

Desk Research

We collated macro and epidemiology baselines from tier-1 public sources such as Eurostat population files, WHO Global Health Observatory, the IDF Diabetes Atlas, and OECD Health Statistics, and then triangulated price and volume anchors using EMA product registries, national tender portals, and quarterly sales disclosures lodged with the European Securities and Markets Authority. Proprietary cues from D&B Hoovers and Dow Jones Factiva helped us profile company footprints, while Questel patent pulls highlighted pipeline read-through for forecast inflections. Additional inputs came from investor decks, annual reports, and trade association releases. The above list is illustrative; many other open datasets informed validation.

Market-Sizing & Forecasting

We reconstructed 2024 volume and value pools through a top-down prevalence-to-treated-patient build, applying diagnosis, treatment, and adherence ratios to adult diabetic cohorts before layering audited ASP brackets by drug class. Supplier roll-ups and sampled pharmacy invoice checks served as bottom-up reasonableness gates. Key variables in our model include adult diabetes prevalence, GLP-1 reimbursement decisions, insulin biosimilar penetration, average daily dose intensity, currency shifts, and obesity incidence trends. A multivariate regression links these drivers to historic sales and then projects through 2030 under a base-case policy scenario, with scenario analysis stress-testing price erosion and cardiovascular-outcome-driven uptake spikes.

Data Validation & Update Cycle

Outputs run through variance checks versus independent import data and payer reimbursement outlays. Senior reviewers sign off after anomaly resolution, and we refresh every twelve months, with mid-cycle updates triggered by EMA approvals or pricing reforms. Clients therefore receive a recently validated snapshot each time.

Why Our Europe Diabetes Drugs Baseline Commands Reliability

Published estimates differ because firms vary scope, base years, and refresh cadence. We acknowledge those gaps and show where they stem from.

Key gap drivers include whether insulins for gestational diabetes are counted, how aggressive GLP-1 ramp-ups are modeled, price-erosion curves for biosimilars, and the length of time series used to smooth COVID-era volatility. Mordor's disciplined inclusion rules, annual re-benchmarking, and dual-path triangulation mitigate these skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.44 B (2025) | Mordor Intelligence | |

| USD 24.86 B (2025) | Global Consultancy A | Bundles weight-management GLP-1s and OTC antihyperglycemics, relies on wholesale shipment data without prevalence checks |

| USD 16.98 B (2023) | Trade Journal B | Captures only Type-2 therapies, excludes insulin biosimilars and uses outdated hospital discharge multipliers |

These contrasts show that when variable selection, scope clarity, and yearly refresh are inconsistent, valuations swing widely. Mordor's method delivers a balanced, transparent baseline that links every dollar to traceable patients, doses, and prices, giving decision-makers a dependable starting point.

Key Questions Answered in the Report

How big is the Europe Diabetes Drugs Market?

The Europe Diabetes Drugs Market size is expected to reach USD 16.35 billion in 2026 and grow at a CAGR of 5.90% to reach USD 21.79 billion by 2031.

What is the current size of the Europe diabetes drugs market?

The market stands at USD 16.35 billion in 2026 and is forecast to reach USD 21.79 billion by 2031 at a 5.90% CAGR.

Which drug class leads sales?

Oral anti-diabetics hold 65.92% of 2025 revenue and are also the fastest-growing class at 6.55% CAGR.

How large is Germany’s share of regional sales?

Germany accounts for 22.10% of the Europe diabetes drugs market in 2025, making it the largest national market.

Why are GLP-1 drugs in short supply?

Unprecedented demand from both diabetes and obesity indications has outpaced peptide manufacturing capacity, leading to periodic shortages and prescription caps across Europe.

What role do digital therapeutics play?

Germany’s DiGA reimbursement pathway has validated digital apps that support glycemic control, driving broader European interest in bundled medicine–software offerings.

How is biosimilar competition affecting prices?

Biosimilar insulin entry has reduced originator glargine prices by a median 21.6% across 28 countries, freeing health-care budgets for next-generation therapies.

Page last updated on: