Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.09 Billion |

| Market Size (2031) | USD 35.95 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

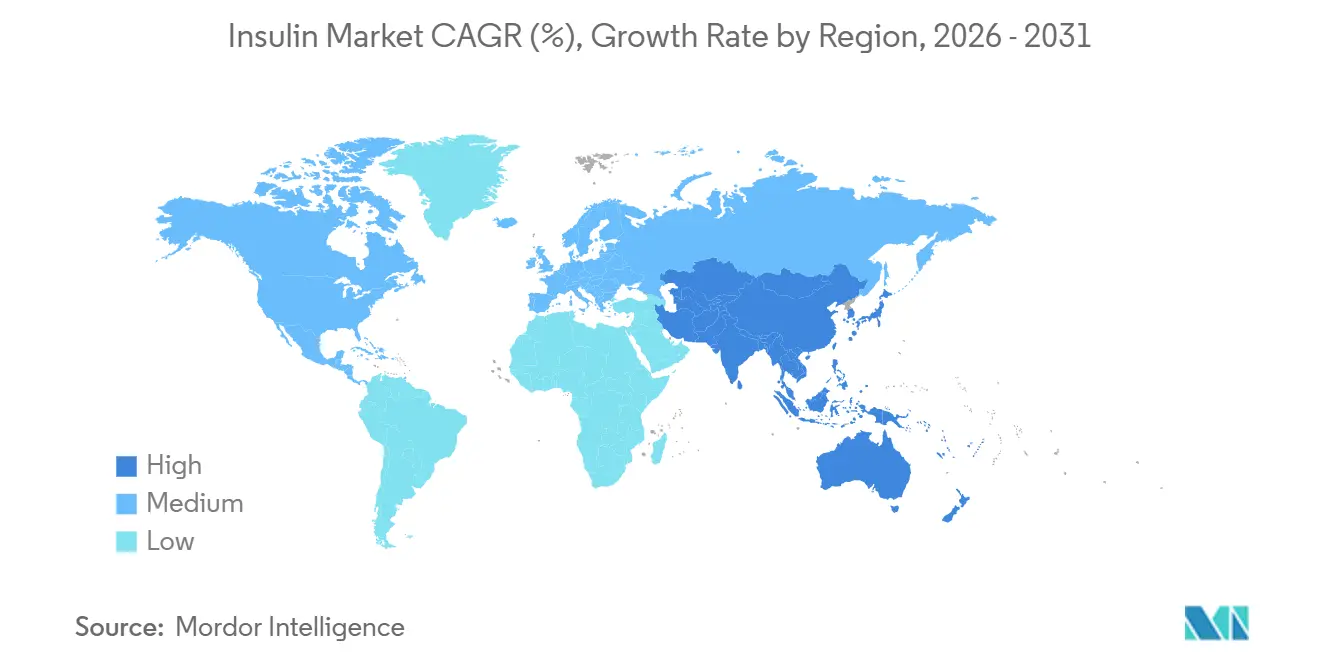

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Market Analysis by Mordor Intelligence

The Insulin Market size is projected to be USD 29.03 billion in 2025, USD 30.09 billion in 2026, and reach USD 35.95 billion by 2031, growing at a CAGR of 3.62% from 2026 to 2031.

Demand expands despite therapeutic substitution from incretin drugs, continued pricing pressure, and cold-chain challenges that undermine dose potency in hot climates. Long-acting analogs such as glargine and degludec remain the revenue backbone, yet once-weekly insulin icodec and biosimilar launches are shifting competitive dynamics. Rapid-acting analog volumes are rising as automated delivery algorithms demand ultra-fast prandial corrections, while sustainability mandates are pushing manufacturers toward reusable pen platforms. Regional procurement programs in China and India compress list prices but simultaneously broaden patient access, keeping the Insulin market on a slow-growth path.

Key Report Takeaways

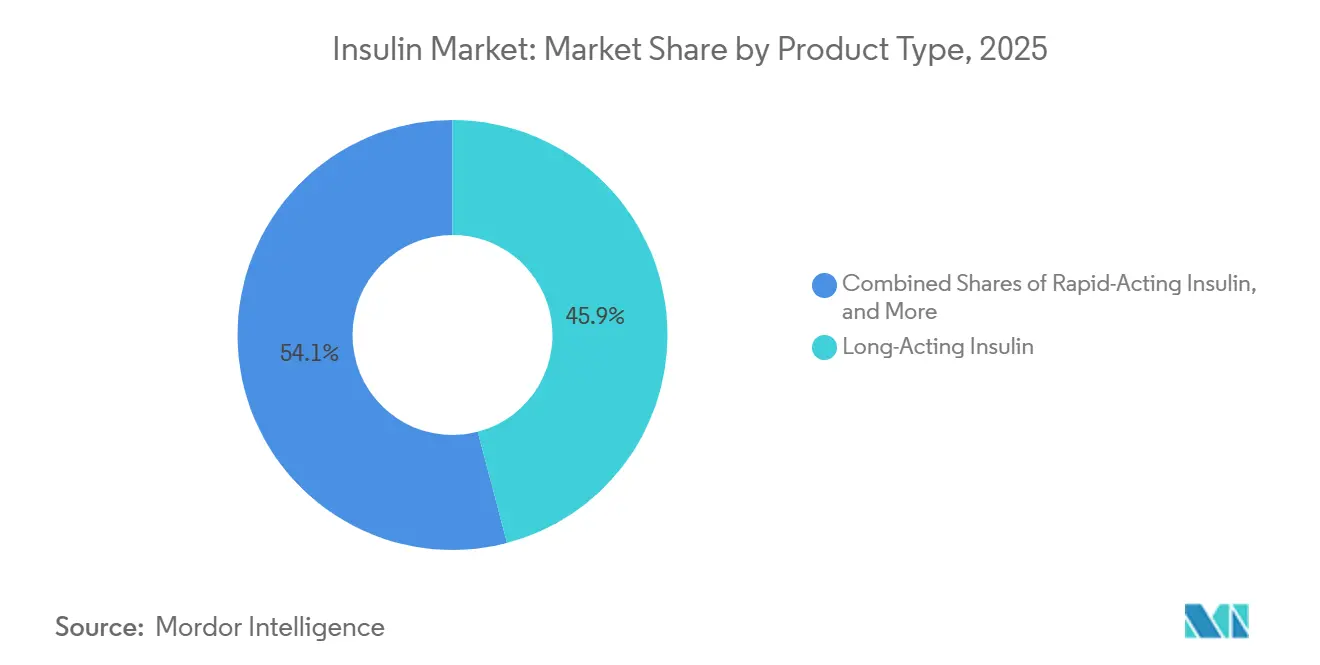

- By product type, long-acting insulin led with 45.92% of the Insulin market share in 2025, while rapid-acting insulin is projected to expand at a 5.28% CAGR to 2031.

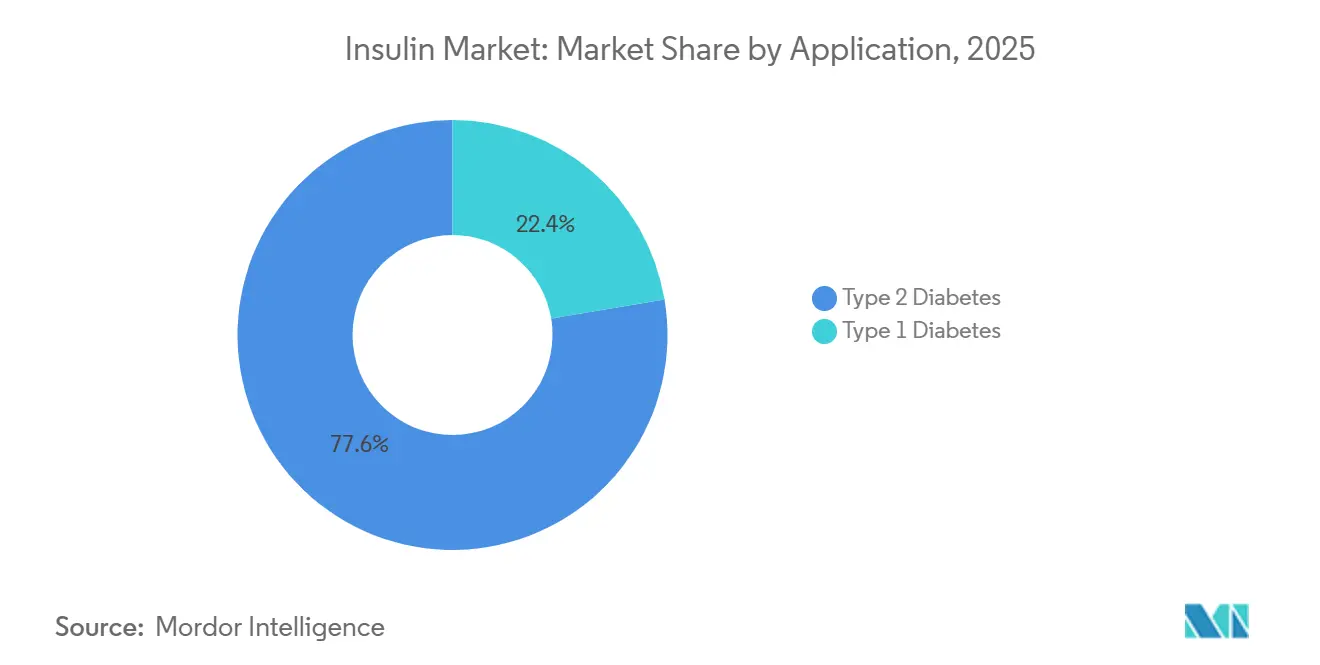

- By application, type 2 diabetes accounted for 77.64% of demand in 2025; type 1 diabetes recorded the fastest growth at a 6.05% CAGR through 2031.

- By delivery device, pens accounted for 64.71% of volume in 2025, whereas jet, patch, and inhaled formats are set to grow at a 5.84% CAGR through 2031.

- North America accounted for 41.78% of 2025 revenue, yet Asia-Pacific is forecast to post the highest regional CAGR at 4.43% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulin Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing diabetes prevalence | +1.8% | Global, highest absolute growth in China and India | Long term (≥ 4 years) |

| Technological advancements in insulin delivery | +0.9% | North America, EU, urban APAC | Medium term (2-4 years) |

| Expansion of reimbursement and affordability initiatives | +0.7% | India, Indonesia, Middle East, Sub-Saharan Africa | Medium term (2-4 years) |

| Rising adoption of biosimilar insulin | +0.5% | EU, North America, South Korea, Australia | Short term (≤ 2 years) |

| Weekly basal-insulin launches enhancing adherence | +0.4% | North America, EU, Japan | Medium term (2-4 years) |

| Volume-based procurement accelerating tier-2 uptake | +0.6% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Diabetes Prevalence

The International Diabetes Federation reported 589 million adults living with diabetes in 2024 and projects 852.5 million by 2050. China and India already account for 238 million diagnosed cases, shifting the Insulin market toward high-volume, lower-margin geographies.[1]International Diabetes Federation, “IDF Diabetes Atlas 11th Edition,” diabetesatlas.org Type 2 Diabetes dominates consumption, but Type 1 prevalence is climbing as newborn screening improves early detection. Automated delivery systems extend basal-bolus therapy to younger cohorts, while real-world data show patients on GLP-1 drugs frequently transition back to insulin within a year. Rising prevalence sustains baseline volume even as alternative injectables gain share.

Technological Advancements in Insulin Delivery

Closed-loop pumps and smart pens integrate continuous glucose monitoring, Bluetooth dosing logs, and algorithmic titration. Medtronic’s MiniMed 780G and Abbott’s FreeStyle Libre 3 pairing boosted time-in-range by 15 percentage points in 2025 cohort studies. BD’s Libertas patch injector bridges the gap between pens and durable pumps, offering up to 200 units over 72 hours. Adoption remains highest in North America and Western Europe, where reimbursement offsets hardware cost, yet APAC urban centers are beginning to pilot payer coverage for closed-loop platforms.

Expansion of Reimbursement & Affordability Initiatives

India’s Jan Aushadhi Kendra network surpassed 10,000 outlets in 2025, supplying insulin vials at prices up to 80% lower than those in private channels.[2]Pharmaceuticals & Medical Devices Bureau of India, “Jan Aushadhi Kendra Expansion,” janaushadhi.gov.in China’s ninth volume-based procurement round in November 2024 cut analog list prices by 42% and extended coverage to 11 additional provinces.[3]China National Healthcare Security Administration, “Ninth Volume-Based Procurement Results,” nhsa.gov.cn Saudi Arabia eliminated prior authorization for analog insulin in 2025, reducing treatment delays. These policies widen access, partially offsetting revenue headwinds from lower unit pricing and sustaining the Insulin market’s patient base.

Rising Adoption of Biosimilar Insulin

FDA-designated interchangeable products, such as Semglee, captured roughly 15% of United States basal prescriptions by 2025. A 2024 BMJ Open Diabetes Research & Care analysis found that European glargine prices fell by 21.6% within 10 years of biosimilar entry. Biocon’s USD 100 million plant expansion in Malaysia aims to produce 50 million vials annually by 2027, signaling confidence in continued biosimilar uptake. Divergent reimbursement policies still shape the pace; Germany mandates biosimilar starting therapy, but United States commercial plans often steer patients toward originators through tiered formularies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price-control policies and competitive tenders | -0.8% | China, India, EU reference-pricing markets, United States | Short term (≤ 2 years) |

| Therapeutic shift toward incretin-based drugs | -1.2% | North America, EU, Japan, South Korea, Australia | Medium term (2-4 years) |

| Cold-chain vulnerabilities in emerging markets | -0.3% | Sub-Saharan Africa, rural South Asia, interior Latin America | Long term (≥ 4 years) |

| Sustainability pressure on disposable-pen waste | -0.2% | EU, selected U.S. states, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Control Policies and Competitive Tenders

The United States Inflation Reduction Act authorized Medicare price negotiation for insulin glargine starting in 2027.[4]Centers for Medicare & Medicaid Services, “Inflation Reduction Act Drug Negotiation Guidance,” cms.gov Europe’s reference pricing, China’s 42% procurement cuts, and India’s state tenders compress average selling prices, encouraging SKU rationalization and biosimilar switching. Sanofi discontinued Lantus vials in several EU markets in 2024, redirecting patients to higher-margin Toujeo pens. Short-term revenue erosion limits top-line growth yet accelerates affordability.

Therapeutic Shift Toward Incretin-Based Drugs

GLP-1 receptor agonists and dual-agonist successors offer compelling weight-loss and cardiometabolic benefits, prompting many clinicians to postpone or bypass insulin initiation for Type 2 patients. In 2025, combined GLP-1 sales by Novo Nordisk and Eli Lilly surpassed USD 15 billion, evidencing rapid uptake in both diabetes and obesity indications. As these agents improve glycemic control alongside body-weight reduction, they reduce progression to basal insulin therapy, creating a substitution effect that softens traditional insulin volume growth. Insulin manufacturers are responding by pursuing combination regimens and investing in advanced delivery systems, yet the fundamental value proposition shift toward weight management remains a headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biosimilars Reshape Analog Economics

Long-acting analogs held 45.92% of the insulin market share in 2025, but rapid-acting analogs are projected to lead growth at a 5.28% CAGR to 2031, fueled by closed-loop pump demand. Biosimilar glargine reached 15% U.S. penetration and drove a 21.6% price decline in Europe, narrowing premium gaps. Insulin degludec sustains differentiation with a 42-hour half-life, whereas detemir’s twice-daily schedule curtailed its footprint and prompted phased withdrawals. Premix formulations remain staples in South Asia and Africa due to cost and dosing simplicity, even as continuous glucose monitoring promotes individualized regimens elsewhere. Ultra-rapid prandial agents and weekly basal formulations together preserve therapeutic relevance and stabilize the overall Insulin market size for this segment.

Second-generation inhaled and oral candidates explore non-invasive delivery to broaden uptake among needle-averse populations. Cipla’s inhaled powder, cleared by India’s CDSCO in December 2025, presents a rapid-acting alternative for post-prandial control. However, widespread adoption will depend on reimbursement parity and real-world pulmonary safety data. Manufacturers continue to balance potency, onset speed, and manufacturing costs as they diversify their portfolios to defend market share.

By Application: Type 1 Gains Share as Automation Expands

Type 2 Diabetes commanded 77.64% of 2025 demand, yet GLP-1 substitution tempers its forward growth. Type 1 Diabetes volume is rising at 6.05% CAGR as pediatric incidence climbs and automated delivery drives tighter glycemic targets. Insulet’s Omnipod 5 and Tandem’s Control-IQ systems broaden pump acceptance. JDRF-supported newborn screening uncovers earlier onset, extending therapy duration per patient, and supporting the Insulin market size for Type 1 care.

Payer policies increasingly reimburse rapid-acting analogs for pediatric and gestational indications, expanding basal-bolus uptake in emerging regions. Conversely, basal-only regimens remain the standard of care for early-stage Type 2 patients in resource-constrained settings. However, volume-based procurement is making full analog coverage feasible in Chinese tier-2 and Indian district hospitals. As treatment algorithms become more differentiated, manufacturers tailor messaging by disease stage rather than a one-size-fits-all approach.

By Delivery Device: Pen Leadership Faces Patch and Smart Pump Upswing

Pen injectors retained 64.71% of the insulin market share in 2025, driven by dose accuracy and user familiarity. Digital add-ons such as Medtronic’s InPen app, now linked to real-time glucose data, are enhancing the category’s usability. Jet and patch injectors are projected to grow at a 5.84% CAGR, offering pain-free, tubeless alternatives that resonate especially with pediatric and Type 2 segments managing multiple comorbidities. Inhaled formats remain niche but are drawing diagnostic-era interest as pulmonary absorption science matures.

Automated insulin delivery (AID) ecosystems represent the next competitive frontier. Insulet’s CE-marked Omnipod 5 pairing with Abbott Libre sensors underscores how open connectivity spurs platform stickiness. Microneedle arrays under investigation could extend painless delivery further, while vial-and-syringe usage is declining in both high- and middle-income settings as training programs normalize pen proficiency. Regulatory frameworks increasingly reward devices that document reductions in dosing errors and hypoglycemia, incentivizing investment in integrated software and sensor interfaces.

Geography Analysis

North America accounted for 41.78% of global revenue in 2025, driven by robust insurance coverage and early adoption of premium analogs. The USD 35 Medicare copay ceiling, however, is narrowing manufacturers’ pricing latitude, compelling them to focus on operational efficiencies and differentiated value propositions. U.S. capacity expansions, Novo Nordisk’s USD 4.1 billion North Carolina plant, and Eli Lilly’s USD 9 billion Indiana complex underscore long-term confidence despite near-term biosimilar and GLP-1 competition. Canada, meanwhile, is phasing out animal-sourced products in favor of modern analogs, underscoring North America’s pivot to high-purity recombinant supply.

Europe remains a mature yet dynamic market where biosimilar penetration and value-based purchasing foster disciplined price trajectories. After biosimilar entry, average insulin glargine prices declined more than 20% across 28 countries, illustrating payers’ negotiation leverage. Weekly basal approvals, such as Awiqli (icodec) and expanded CE markings for AID systems, position the region as an early proving ground for next-generation therapies. Still, supply chain hiccups and Fiasp PumpCart shortages in 2025 expose vulnerabilities in specialized cartridge formats and highlight the need for diversified manufacturing nodes. Prospective regulatory streamlining for biosimilars could shorten development cycles and raise competitive intensity post-2026.

Asia-Pacific is the fastest-growing geography, with a 4.43% CAGR through 2031, driven by rising diabetes incidence, urban lifestyle shifts, and policy-driven affordability gains. China’s Volume-Based Procurement has cut insulin prices by up to 48% in nationwide tenders, expanding access to millions of new users. India is leveraging domestic biosimilar capacity to cover rural districts previously underserved by analog products. Multinational firms are pairing local fill-finish alliances with greenfield builds, as evidenced by Sanofi’s Beijing complex and Novo Nordisk’s Tianjin expansion, to anchor supply close to growth clusters. Cold-chain infrastructure gaps and regional reimbursement disparity remain challenges, yet they also create openings for logistics specialists and telehealth platforms.

Competitive Landscape

The insulin market is an oligopoly: Novo Nordisk, Eli Lilly, and Sanofi collectively supply nearly 90% of global volume. Novo Nordisk leverages integrated upstream capacity and a broad injectable-to-oral pipeline, while pivoting aggressively into GLP-1 domains. Eli Lilly complements deep manufacturing spend of USD 18 billion since 2024 with diversified biologics in obesity and Alzheimer’s, reducing reliance on basal analog revenue. Sanofi’s EUR 1.3 billion (USD 1.54 billion) expansion of its Frankfurt plant signals continued commitment to basal insulin demand, even as its pipeline focuses on autoimmune and oncology assets.

Biosimilar developers such as Biocon are scaling output under WHO pre-qualification, using cost positions to win public tenders across Asia and Latin America. Hikma’s 2024 liraglutide generic approval hints at broader entry ambitions in combination with endocrine therapies. Device innovators are likewise reshaping competition: Abbott’s open-innovation CGM strategy now spans Medtronic and Tandem AID partners, establishing an ecosystem model that encourages multilateral integration. Insulet’s acquisition of Bigfoot Biomedical's IP consolidates patent coverage for tubeless pumps, fortifying defenses against emerging rivals. Overall, success hinges on pairing molecular innovation with connected delivery, an imperative pushing incumbents and entrants alike toward software-enabled care models.

Strategic moves in 2025 highlight this evolution. Novo Nordisk resubmitted icodec to the FDA with a Type 2-only label, aiming for a mid-2026 launch. Biocon expanded its Civica partnership to supply affordable glargine in the United States. Abbott received expanded interoperability clearance for Libre 3 with leading pump brands, reinforcing its sensor franchise.

Insulin Industry Leaders

Novo Nordisk A/S

Eli Lilly and Company

Pfizer Inc.

Sanofi

Biocon Biologics Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Novo Nordisk announced that the US Food and Drug Administration (FDA) had approved Awiqli (insulin icodec-abae) injection, 700 units/mL. This approval established Awiqli as the first and only once-weekly, long-acting basal insulin, designed to support diet and exercise in improving blood sugar control for adults with type 2 diabetes.

- October 2025: Novo Nordisk resubmitted its the United States NDA for once-weekly insulin icodec targeting a mid-2026 launch.

- October 2025: Biocon Biologics expanded its Civica collaboration to include the United States supply of biosimilar insulin glargine.

- July 2025: Health Canada approved Kirsty (insulin aspart-xjhz), the first interchangeable biosimilar to NovoLog, expanding affordable options for insulin-dependent patients.

- June 2025: Tandem Diabetes Care partnered with Abbott to link AID systems with future glucose-ketone sensors for early ketoacidosis detection.

- May 2025: Brazil launched tirzepatide (Mounjaro) in retail pharmacies following Anvisa authorization as an Ozempic competitor.

Global Insulin Market Report Scope

As per the scope of the report, insulin is defined as a hormone that regulates the body's blood sugar level. It treats chronic diseases such as type 1 and type 2 diabetes.

The insulin market is segmented by product type, application, delivery device, and geography. By product type, the market is segmented into rapid-acting insulin, combination insulin, long-acting insulin, and other product types. By application, the market is segmented by type 1 diabetes and type 2 diabetes. By delivery device, the market is segmented into pens, infusion pumps, syringes, and other delivery devices. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.

By Product Type

| Rapid-Acting Insulin | Insulin Lispro |

| Insulin Aspart | |

| Insulin Glulisine | |

| Technosphere Insulin | |

| Long-Acting Insulin | Insulin Detemir |

| Insulin Glargine (Originator) | |

| Insulin Glargine-Yfgn (Biosimilar) | |

| Insulin Degludec | |

| Combination / Premix Insulin | NPH/Regular |

| Protamine/Lispro | |

| Protamine/Aspart | |

| Biosimilar Insulin (cross-cutting) | |

| Other Product Types |

By Application

| Type 1 Diabetes |

| Type 2 Diabetes |

By Delivery Device

| Pens |

| Pump Reservoirs |

| Vials & Syringes |

| Jet / Patch / Inhalers |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Rapid-Acting Insulin | Insulin Lispro |

| Insulin Aspart | ||

| Insulin Glulisine | ||

| Technosphere Insulin | ||

| Long-Acting Insulin | Insulin Detemir | |

| Insulin Glargine (Originator) | ||

| Insulin Glargine-Yfgn (Biosimilar) | ||

| Insulin Degludec | ||

| Combination / Premix Insulin | NPH/Regular | |

| Protamine/Lispro | ||

| Protamine/Aspart | ||

| Biosimilar Insulin (cross-cutting) | ||

| Other Product Types | ||

| By Application | Type 1 Diabetes | |

| Type 2 Diabetes | ||

| By Delivery Device | Pens | |

| Pump Reservoirs | ||

| Vials & Syringes | ||

| Jet / Patch / Inhalers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the global Insulin market be by 2031?

The Insulin market size is projected to reach USD 35.95 billion by 2031, expanding at a 3.62% CAGR from 2026.

What segment will grow fastest through 2031?

Rapid-acting insulin is forecast to record the quickest expansion at a 5.28% CAGR, driven by its role in closed-loop delivery systems.

Which region offers the highest growth opportunity?

Asia-Pacific shows the strongest outlook with a 4.43% CAGR, helped by large diagnosed populations in China and India and expanding procurement coverage.

How are biosimilars influencing pricing?

Biosimilar glargine lowered European list prices by 21.6% over ten years and holds about 15% of U.S. basal prescriptions, intensifying price competition.

What is the impact of weekly basal insulin?

Once-weekly formulations like insulin icodec improve adherence by reducing injection frequency and are expected to enhance patient convenience without sacrificing glycemic control.

How is sustainability shaping device decisions?

EU take-back mandates and U.S. state fees on disposable pens push manufacturers toward reusable and recyclable delivery platforms, influencing procurement choices.

Page last updated on: