China Feed Minerals Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

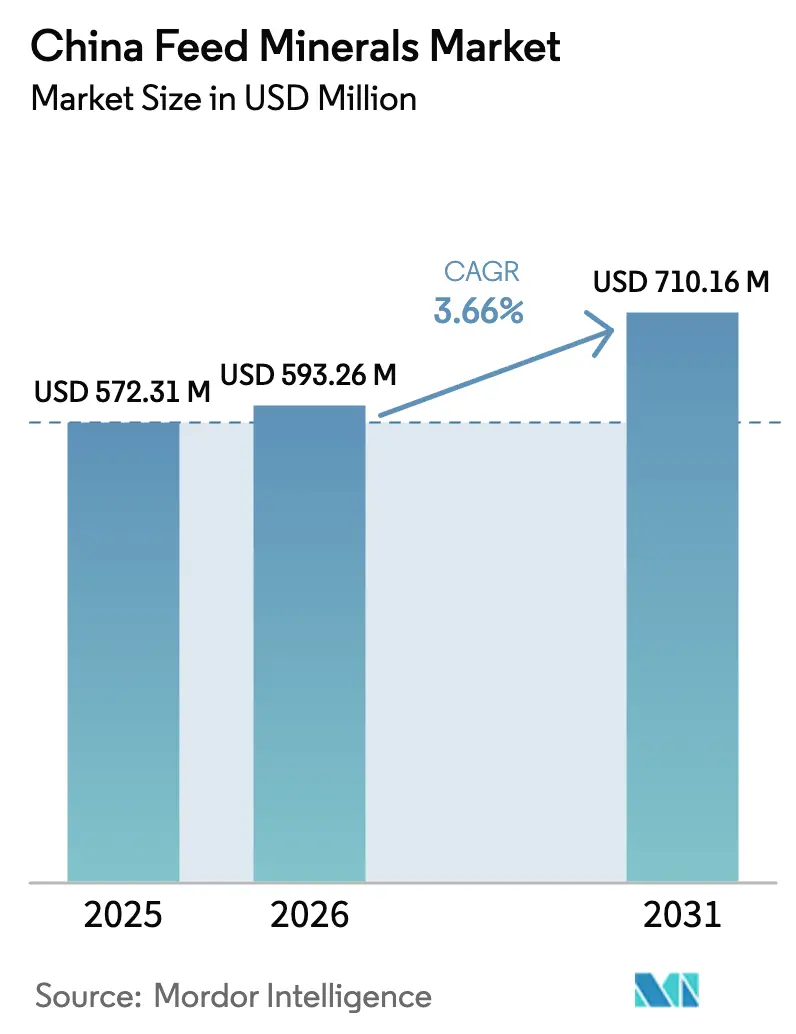

| Base Year Market Size (2025) | USD 572.31 Million |

| Market Size (2026) | USD 593.26 Million |

| Market Size (2031) | USD 710.16 Million |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

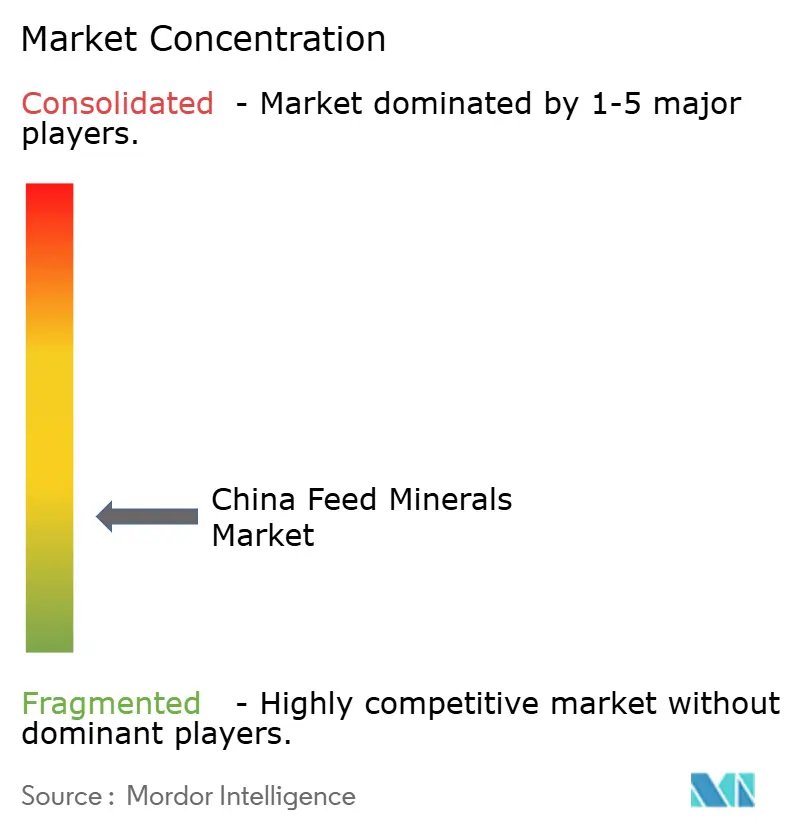

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Feed Minerals Market Analysis by Mordor Intelligence

The China feed minerals market size was valued at USD 572.31 million in 2025 and estimated to grow from USD 593.26 million in 2026 to reach USD 710.16 million by 2031, at a CAGR of 3.66% during the forecast period (2026-2031). This growth path reflects tightening copper and zinc limits, surging aquaculture feed demand, and ongoing feed-mill consolidation that together reshape mineral procurement, formulation, and pricing patterns within the China feed minerals market. Evolving sustainability mandates favor chelated and organic minerals that deliver comparable bioavailability at lower inclusion rates, while carbon-neutral livestock pilots reward solutions that curb nutrient excretion. Meanwhile, hog-sector overcapacity suppresses short-term volume growth, and volatile phosphate prices compress margins for smaller mills that lack hedging power. Large integrated producers are responding by locking in long-term mineral contracts, building local production, and co-developing precision formulations with global suppliers to safeguard supply security and regulatory compliance across the China feed minerals market.

Key Report Takeaways

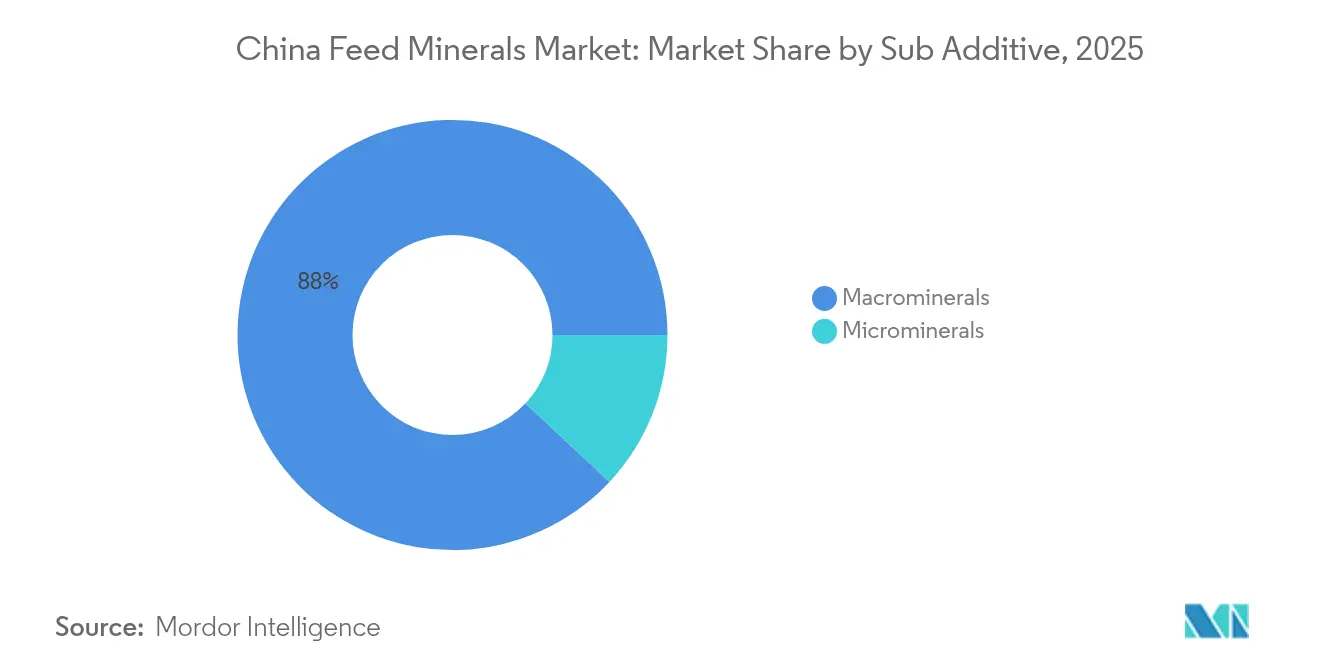

- By sub-additive, macrominerals led with 88.02% of China feed minerals market share in 2025, and are expanding at a 3.72% CAGR through 2031.

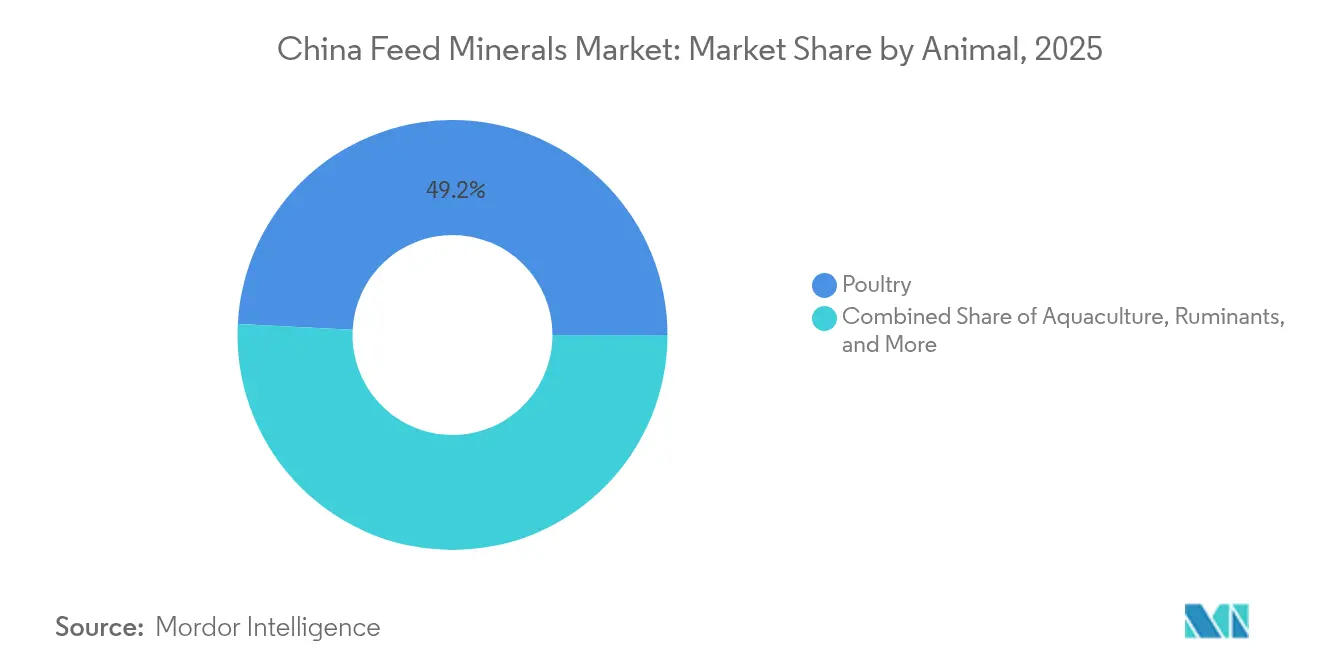

- By animal, poultry commanded 49.18% of the China feed minerals market size in 2025, whereas ruminants exhibited the fastest 4.24% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Feed Minerals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory cap on high-dose inorganic Cu/Zn pushing shift to chelated/organic minerals | +1.2% | National, with early adoption in eastern provinces | Medium term (2-4 years) |

| Soy-meal-reduction policy raises demand for mineral-balanced synthetic amino-acid premixes | +0.8% | National, concentrated in major feed production hubs | Medium term (2-4 years) |

| Growth of the aquaculture and pet-food sectors demanding species-specific mineral blends | +0.9% | Coastal provinces, expanding inland | Long term (≥ 4 years) |

| Consolidation of feed mills accelerating adoption of fully-fortified premixes | +0.7% | National, led by eastern industrial zones | Short term (≤ 2 years) |

| Carbon-neutral livestock pilots favor low-excretion mineral technologies | +0.4% | Pilot regions in Shandong, Henan, Inner Mongolia | Long term (≥ 4 years) |

| Provincial feed-testing subsidies promoting higher-grade mineral inclusion | +0.5% | Provincial implementation varies, strongest in developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory cap on high-dose inorganic Cu/Zn pushing shift to chelated/organic minerals

China’s 2017 decision to cut copper and zinc inclusion limits by 20-30% transformed supplementation strategies, driving sustained uptake of chelated minerals that deliver equal nutrition at 30-40% lower inclusion[1]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Grain and Feed Update (CH2024-0075),” FAS.USDA.GOV. Research shows iron-nanoparticle feed additives can cut bioavailable copper in manure by 66.8%, easing soil contamination concerns[2]Source: University of South Australia, “Iron nanoparticles offer a solution,” PHYS.ORG. Large integrators quickly embraced these premium minerals to comply with tightening discharge rules and to capture feed-conversion gains. Provincial authorities now spotlight mineral utilization metrics during environmental audits, reinforcing the shift away from high-dose inorganic products. Consolidated producers use their scale to negotiate bulk contracts for organic minerals, ensuring a steady supply and traceability.

Soy-meal-reduction policy raises demand for mineral-balanced synthetic amino-acid premixes

Beijing’s program to curb imported soybean meal reshapes feed formulations and heightens the need for precision mineral balancing. Cottonseed, rapeseed, and single-cell proteins alter calcium-phosphorus ratios, compelling nutritionists to deploy tailored mineral-amino premixes. Adisseo’s new 150,000 metric tons methionine plant in Fujian underpins this transition by pairing amino acids with complementary minerals for low-protein diets. The National Development and Reform Commission subsidizes low-protein rations at RMB 300 per metric ton (USD 42.9), spurring adoption across industrial feed mills.

Growth of aquaculture and pet-food sectors demanding species-specific mineral blends

Producing more than 70% of global aquafeed, China demands species-specific trace-mineral blends that remain stable in water and support immunity. The Chongqing FeedKind plant supplies 20,000 metric tons of single-cell protein requiring selenium, iodine, and manganese optimization, illustrating the growing niche for marine-grade minerals. Pet-food processors mirror this trend, formulating chelated zinc and copper premixes that improve coat quality and palatability in premium brands.

Consolidation of feed mills accelerating adoption of fully-fortified premixes

Large operators now supply 65% of compound feed, compared with 38% in 2022, enabling uniform mineral programs across multi-site networks. Integrated players such as New Hope and Haid negotiate multi-year contracts for fully fortified premixes, reducing handling errors and ensuring batch consistency. Their enterprise-plus-farmer model transmits standardized mineral specifications to thousands of contract growers, reinforcing nationwide demand for certified chelated products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile phosphate and trace-metal prices are squeezing feed-mill margins | -1.1% | Global supply chain affecting all regions | Short term (≤ 2 years) |

| Stringent MARA import registration delays new formulations | -0.8% | National regulatory framework | Medium term (2-4 years) |

| Over-capacity in hog sector dampening near-term mineral demand | -1.3% | National, concentrated in major pig-producing provinces | Short term (≤ 2 years) |

| Environmental limits on mining of domestic mineral ores | -0.6% | Western provinces with mining operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile phosphate and trace-metal prices are squeezing feed-mill margins

Phosphate costs have swung widely on export curbs, while a 2024 plant fire in Germany tightened vitamin A and E supply, cascading into mineral premix price spikes. Corn at RMB 2,320 per metric ton (USD 331) offered feed mills temporary relief, yet mineral price hikes erased many savings. Smaller mills lack hedging tools, exposing them to margin erosion and prompting closures or mergers. Chinese vitamin producers, who dominate global supply for vitamin C and several B-complex vitamins, have faced extended shutdowns and are quoting limited volumes, adding unpredictability to mineral premix costs that rely on vitamin-mineral combinations for optimal efficacy.

Stringent MARA import registration delays new formulations

Securing approval for novel chelated minerals can take up to two years, with dossiers requiring exhaustive molecular and residue data. International suppliers often partner with domestic firms that already hold registrations, but this adds cost layers and reduces pricing flexibility. Delays particularly constrain specialty products aimed at carbon-neutral pilots, slowing market diffusion of cutting-edge solutions. The regulatory framework particularly impacts smaller specialty mineral suppliers who lack the resources to navigate lengthy approval processes, effectively consolidating market share among larger international and domestic players with established regulatory capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Macrominerals Underpin Core Demand

Macrominerals accounted for an 88.02% China feed minerals market share in 2025, anchored by essential calcium and phosphorus needs in all livestock species. This category is forecast to expand at a 3.72% CAGR through 2031, underlining its foundational role. High-energy corn diets increase the calcium-phosphorus balancing requirement, especially for layers and lactating sows. Mills also elevates magnesium and sodium inclusions when alternative protein meals alter electrolyte profiles. Robust demand from dairy modernization programs ensures sustained volume growth, while chelated calcium salts gain traction for ruminant close-up diets aiming to prevent hypocalcemia.

Microminerals represent only a minimal share of the value, but their premium pricing drives revenue. Copper, zinc, manganese, and iron chelates command up to 3-times the price of inorganics, yet formulators accept higher costs because improved bioavailability trims inclusion rates by one-third. Selenium yeast enjoys rapid adoption in aquaculture, enhancing antioxidant capacity and reducing juvenile mortality. Trace-mineral premixes increasingly bundle vitamins and organic acids to simplify dosing for integrated customers, reinforcing micromineral segment expansion.

By Animal: Poultry Leads While Ruminants Accelerate

Poultry held 49.18% of the China feed minerals market size in 2025, backed by broiler feed output and sustained layer expansion. Shell strength demands 4–4.5 g daily calcium intake, supporting large calcium-carbonate volumes. Chelated manganese improves eggshell microstructure and has become a standard in commercial layer diets. Broiler integrators employ lower copper levels to meet environmental rules, substituting organic copper for performance retention.

Ruminants post the fastest 4.24% CAGR as beef feedlots scale and dairy farms modernize. Precision mineral packs adjust calcium and phosphorus to the lactation stage, while protected zinc supports hoof health in high-yield cows. Swine demand remains subdued due to sow herd cuts, but sow mineral tubs incorporating organic selenium and chromium aim to boost litter viability. Aquaculture consumption outpaces the overall market, with shrimp diets requiring water-stable chelated trace minerals, and seabass farms demanding iodine for thyroid regulation. Pet-food formulators chase human-grade mineral purity, creating a niche opportunity for pharmaceutical-grade calcium and zinc sources.

Geography Analysis

Eastern provinces, Shandong, Henan, and Hebei, controlled half of the China feed minerals market demand in 2025 due to dense livestock populations and proximity to coastal ports. Emission-control campaigns forced many legacy pig and layer farms to adopt chelated minerals that reduce manure excretion and comply with discharge caps. Henan cut livestock-related emissions through precision feeding and manure utilization technologies, setting a benchmark for mineral-efficiency gains.

Western regions such as Inner Mongolia, Xinjiang, and Qinghai are experiencing double-digit herd growth and consequently rising mineral requirements. Inner Mongolia posted an increase in livestock activity, moving from traditional grazing toward semi-intensive feedlots that necessitate formulated mineral packs. Supply chains in these land-locked areas increasingly rely on rail shipments of premixes produced in eastern hubs, spurring investment in regional blending plants to shorten lead times and cut freight costs.

Southern coastal provinces, including Guangdong and Fujian, serve as aquaculture powerhouses, driving specialized mineral demand for shrimp and marine fish. The Fujian methionine facility anchors a local ecosystem of amino and mineral suppliers geared toward aquatic species. Government grants for recirculating aquaculture systems encourage the adoption of encapsulated trace-mineral technologies that resist leaching and maintain feed integrity in water.

Competitive Landscape

The market shows low concentration: the top five players balance global technology leaders and price-competitive domestic firms. International companies such as Alltech, Inc., Archer Daniels Midland Co., Solvay S.A., BASF SE, and Cargill Inc., leverage advanced chelation patents and existing Migration Agents Registration Authority (MARA) registrations to defend their share in high-value segments. Adisseo’s 150,000 metric tons methionine project in Fujian exemplifies the push for local production that lowers logistics costs and improves service responsiveness.

Domestic challengers focus on commodity macrominerals and regional distribution strength, but several are upgrading to organic mineral lines to satisfy integrated customers’ quality audits. Guangdong Haid integrates premix manufacturing with its feed and farming units, capturing internal demand and offering external contract services. Hebei Chengxin scales chelated copper output, bundling technical services to differentiate from smaller blenders.

Technology adoption pivots around precision formulation software that models real-time nutrient requirements and environmental limits. Suppliers co-develop digital dosing systems with integrators, embedding proprietary algorithms that lock in long-term mineral business. White-space areas include carbon-footprint labeled minerals and nanoparticle-based detox solutions that could redefine competitive dynamics once MARA approvals are secured.

China Feed Minerals Industry Leaders

Alltech, Inc.

BASF SE

Cargill Inc.

Solvay S.A.

Archer Daniels Midland Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The United States Department of Agriculture (USDA) trimmed China’s 2024/25 corn-import estimate by 3 million metric tons to 10 million metric tons, reflecting weaker feed demand and policy interventions that reshape mineral balancing.

- July 2024: Calysseo's FeedKind aquafeed plant became operational in Chongqing with 20,000 metric tons annual capacity, representing a major investment in premium aquaculture feed ingredients that require specialized mineral supplementation for optimal performance.

- August 2023: Adisseo announced the construction of a new powder methionine plant in Fujian Province with a planned annual production capacity of 150,000 metric tons, consolidating the company's leadership in amino acid production and supporting integrated mineral-amino acid supplementation strategies.

China Feed Minerals Market Report Scope

Macrominerals, Microminerals are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal.| Macrominerals |

| Microminerals |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Sub Additive | Macrominerals | |

| Microminerals | ||

| Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms