Animal Disinfectant Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

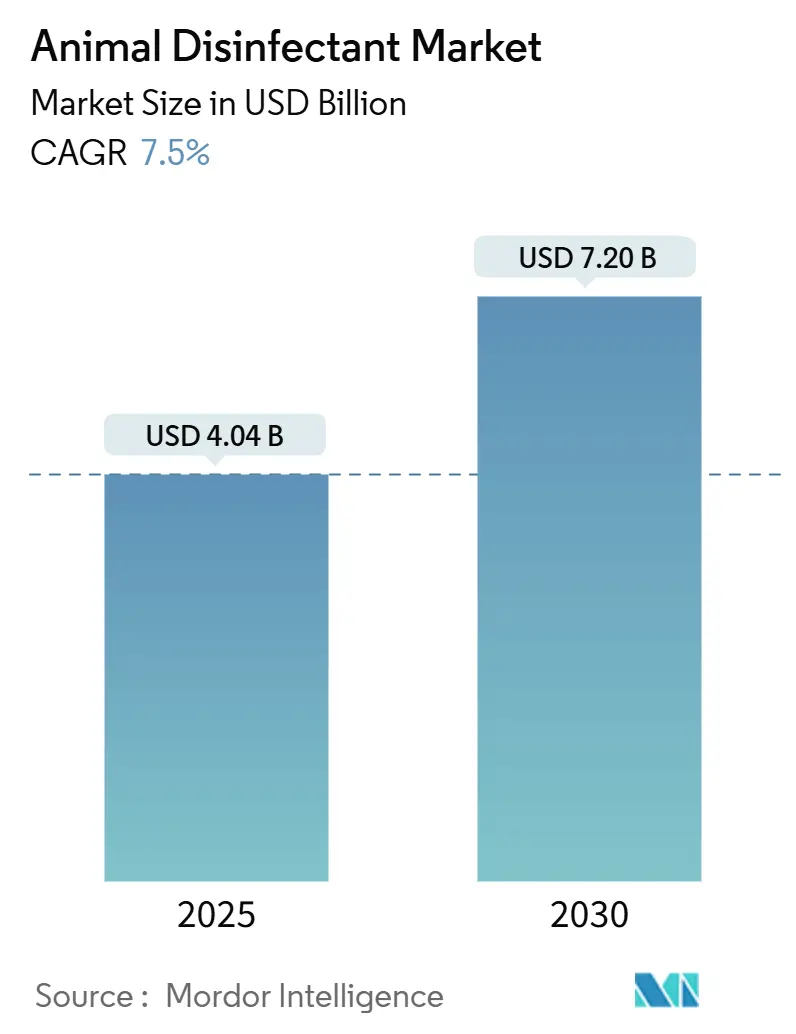

| Market Size (2025) | USD 4.04 Billion |

| Market Size (2030) | USD 7.20 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Disinfectant Market Analysis by Mordor Intelligence

The Animal Disinfectant Market size is estimated at USD 4.04 billion in 2025, and is expected to reach USD 7.20 billion by 2030, at a CAGR of 7.5% during the forecast period (2025-2030).

Animal Disinfectant Market Overview

The animal disinfectants market is undergoing substantial changes, driven by evolving biosecurity protocols and stringent regulatory frameworks within the global agricultural sector. According to the European Center for Disease Control's November 2024 report, 75 cases of highly pathogenic avian influenza (HPAI) subtypes A(H5) and A(H7) were detected between June 15 and September 20, 2024. These included 16 cases in domestic birds and 59 cases in wild birds across 11 European countries, underscoring the necessity of robust disinfection protocols. Farms and veterinary facilities are prioritizing investments in advanced biosecurity measures and comprehensive sanitation programs. Industry participants are increasingly integrating traditional disinfection techniques with modern monitoring systems to enhance efficiency and ensure adherence to regulatory standards.

The market is increasingly shifting towards sustainable and environmentally friendly solutions, aligning with broader sustainability objectives across industries. Leading companies focusing on eco-friendly formulations, including a biodegradable product line that significantly reduces plastic waste compared to conventional packaging. This trend is particularly evident in the veterinary clinic segment, where adopting sustainable practices has become a competitive advantage. Furthermore, the market is witnessing a rise in investments in plant-based and biodegradable disinfectant solutions, which provide high efficacy while minimizing environmental impact.

Strategic consolidation and technological advancements are reshaping the competitive dynamics of the market. In November 2024, Byotrol Ltd entered into a 5-year strategic partnership with Duggan Veterinary Group, granting Duggan exclusive distribution rights for Byotrol's innovative product portfolio. These products, including ANIGENE veterinary surface disinfectant, PROCESSUS hand sanitizer, and INVIRTU for instrument decontamination, will be distributed exclusively across Northern Ireland and the Republic of Ireland. The partnership targets veterinary clinics, animal welfare organizations, zoos, and other animal health entities. Additionally, manufacturers are incorporating digital technologies into disinfection protocols, such as smart dosing systems and IoT-enabled monitoring solutions, to optimize product usage and improve the tracking of disinfection processes.

The industry is advancing rapidly in product formulation and application technologies to meet changing customer demands and operational requirements. For example, in January 2023, Planet Pets launched Zap Kennel Wash, India's first disinfectant designed specifically for pet owners. This product addresses persistent odor issues and combats the spread of harmful viruses among pets. It is intended for use in veterinary clinics, hospitals, and pet-owning households, offering effective virus neutralization on contact. The focus on specialized solutions has led to the development of formulations tailored to specific animal species and facility types. Market leaders are heavily investing in research and development to create next-generation disinfectants that provide enhanced efficacy against emerging pathogens while ensuring user safety and ease of application.

Global Animal Disinfectant Market Trends and Insights

Growing Incidence of Livestock Diseases

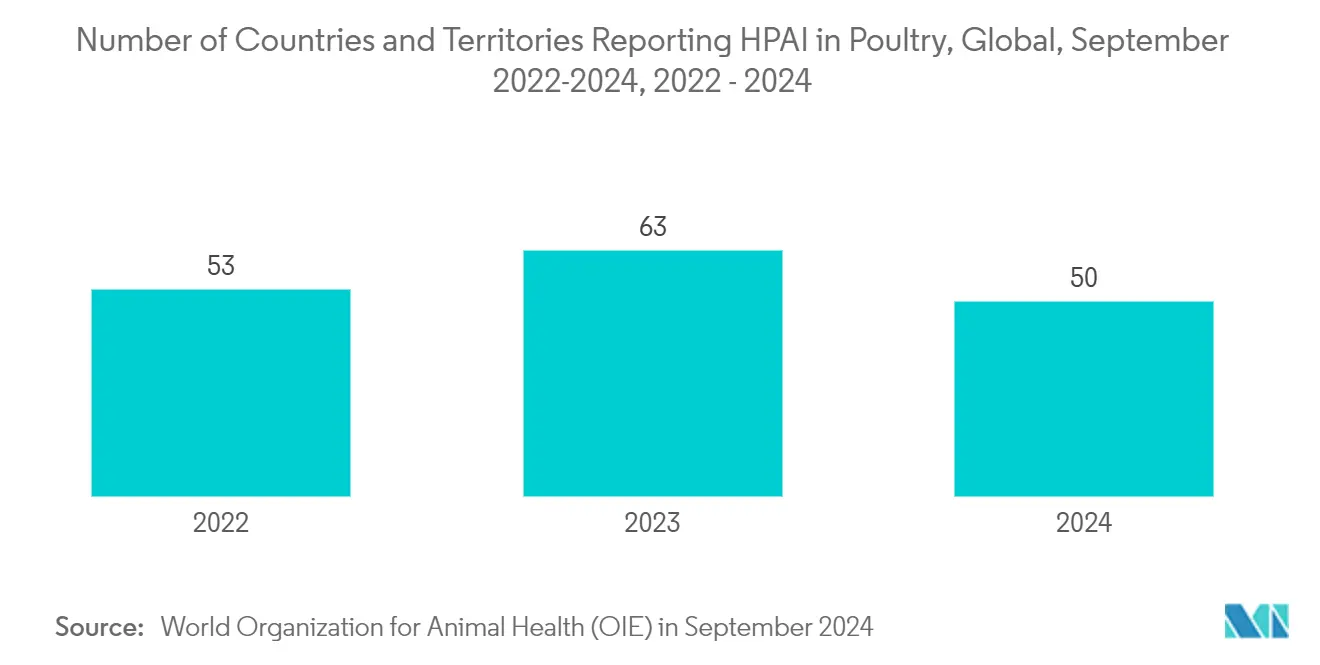

The global demand for animal disinfectants is experiencing significant growth, primarily due to the increasing prevalence of livestock diseases. A report published by the World Organization for Animal Health (OIE) in September 2024 revealed a sharp rise in avian influenza outbreaks across various countries, resulting in considerable losses in domestic poultry and wild bird populations. Between October 2023 and September 2024, 39 countries and territories reported high pathogenic avian influenza (HPAI) in poultry, while 50 countries and territories reported HPAI in wild birds. During this period, there were 771 HPAI outbreaks in poultry and 1,023 HPAI outbreaks in wild birds. These developments have compelled agricultural authorities to enforce stricter biosecurity measures and implement enhanced disinfection protocols.

The growing incidence of zoonotic diseases, such as salmonellosis, brucellosis, and tuberculosis, further highlights the critical need for effective animal disinfection solutions. These diseases pose substantial risks to both animal health and human populations, particularly through direct contact with animals or the consumption of animal-derived products. In response, organizations like the United States Department of Agriculture's Animal and Plant Health Inspection Service have introduced comprehensive protocols and Standard Operating Procedures (SOPs) to assist farmers in managing these diseases effectively. This has led to increased awareness of the importance of routine disinfection practices and a rising demand for high-quality animal disinfectants within the farming industry.

Rising Demand for Eco-friendly and Cost-Effective Disinfectants

The market is undergoing a notable transition toward eco-friendly and sustainable disinfectant solutions, driven by growing environmental awareness and stringent regulatory requirements. This shift is particularly evident in the increasing adoption of biological disinfectants, which deliver broad-spectrum efficacy while reducing environmental impact. For instance, in April 2023, Virox Technologies launched Rescue Refill Wipe pouches, incorporating eco-friendly disinfectant formulations. These pouches use 90% less plastic compared to traditional canisters, highlighting the industry's focus on sustainability without compromising performance.

The identification of traditional chemical compounds, such as formaldehyde, as potential carcinogens has accelerated the development and acceptance of safer, biological alternatives. These eco-friendly solutions are gaining traction as they combine the benefits of chemical disinfectants, such as broad-spectrum antimicrobial activity, with a significantly lower environmental footprint. Manufacturers are prioritizing the development of cost-efficient green formulations that effectively control pathogens while addressing environmental concerns. This market evolution is supported by increased research into natural compounds and sustainable production processes. However, challenges remain in balancing cost efficiency and ensuring these solutions are accessible across all market segments.

Animal Disinfectant Market Product Type Segment Analysis

Quaternary Ammonium Compounds (QAC) Segment in Animal Disinfectant Market

In 2024, the quaternary ammonium compounds (QAC) segment holds a leading position in the animal disinfectant market, accounting for approximately 22% of the market share. This dominance is primarily driven by QAC's broad-spectrum antimicrobial effectiveness and relatively lower toxicity compared to other disinfectant categories. The segment's strong market presence is further reinforced by its extensive use in veterinary clinics, dairy farms, and poultry facilities, where its residual antimicrobial activity ensures prolonged protection. QAC disinfectants have witnessed significant adoption in developed markets due to their stability, effectiveness at room temperature, and compatibility with diverse surfaces. The segment's growth trajectory is further supported by increasing awareness of biosecurity practices in livestock farming and the rising focus on preventive healthcare in animal husbandry. Moreover, the development of advanced QAC formulations with improved efficacy and reduced environmental impact continues to sustain its market leadership.

Alcohol-based Disinfectants Segment in Animal Disinfectant Market

The alcohol-based disinfectants segment is positioned as the fastest-growing category within the animal disinfectant market, with a projected CAGR of 7.8% from 2025 to 2030. This significant growth is attributed to the increasing adoption of efficient, rapid-acting disinfection solutions in veterinary clinics and animal farming operations. The segment's expansion is further supported by the rising preference for volatile disinfectants that leave minimal residue, making them particularly suitable for sensitive equipment and surfaces. Innovations in alcohol-based formulations have addressed earlier limitations related to effectiveness against specific pathogens while maintaining their quick-drying and broad-spectrum antimicrobial characteristics. Additionally, the segment benefits from the growing demand for ready-to-use disinfectant solutions, which minimize preparation time and deliver consistent performance. The heightened awareness of effective disinfection practices, amplified by the COVID-19 pandemic, has also played a pivotal role in sustaining the growth of this segment.

Remaining Segments in Animal Disinfectant Market

The segments, including iodine-containing, aldehyde, peroxide, lactic acid, and other disinfectants, represent significant growth potential within the animal disinfectant market. These segments cater to distinct requirements across various animal farming industries and veterinary applications. Iodine-containing disinfectants maintain a consistent market presence due to their proven efficacy in dairy farming operations. Aldehyde-based products are preferred in applications requiring high-level disinfection. Peroxide disinfectants are gaining traction for their environmentally friendly characteristics and minimal residual effects. Lactic acid-based solutions have secured a niche in organic farming, where natural and sustainable alternatives are prioritized. The diversification of these segments reflects the market's responsiveness to changing regulatory frameworks, environmental concerns, and application-specific needs across different regions and farming practices. Recent innovations within these segments aim to enhance effectiveness, minimize environmental impact, and address specific pathogen-related challenges.

Animal Disinfectant Market Form Segment Analysis

Liquid Segment in Animal Disinfectant Market

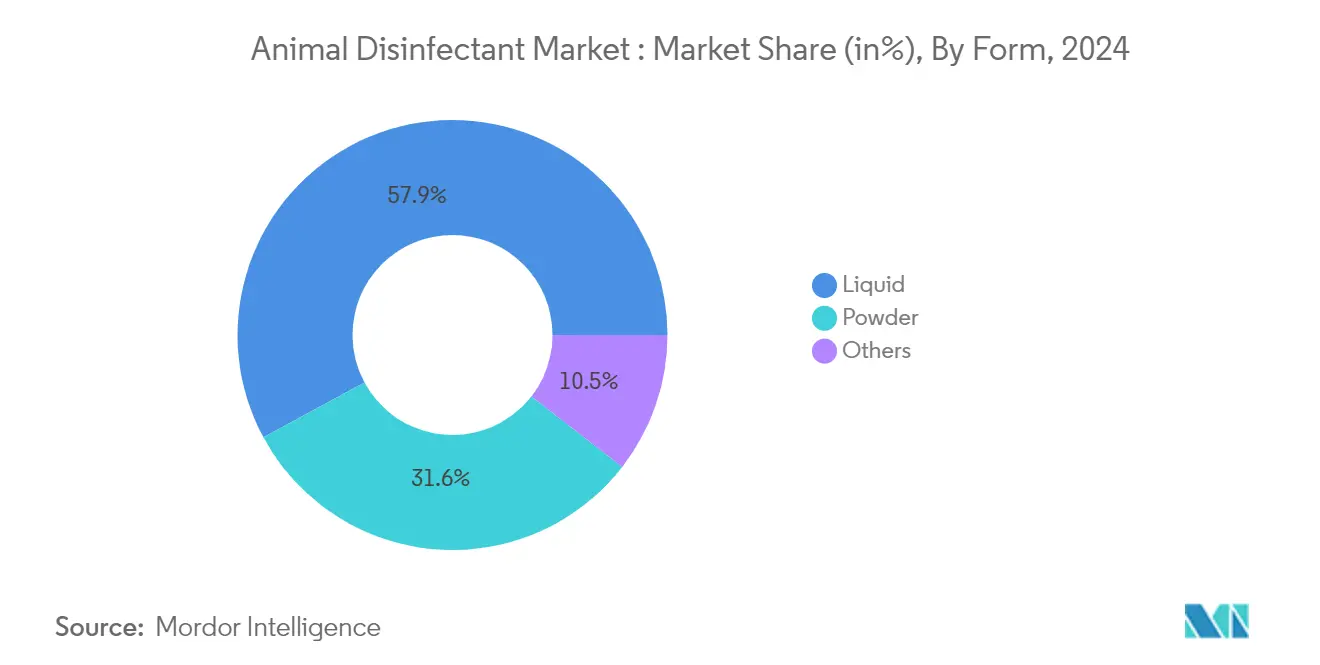

In 2024, the liquid segment holds a commanding 55% share of the animal disinfectant market. This significant market position is driven by the superior coverage and penetration capabilities of liquid disinfectants, which are well-suited for diverse animal farming environments. The segment's prominence is further enhanced by the convenience of application through spraying systems and fogging equipment, making it particularly advantageous for large-scale livestock operations. Liquid disinfectants are extensively utilized in dairy farming and poultry sectors due to their ability to access hard-to-reach areas such as corners and crevices. Additionally, advancements in concentrated formulations, offering cost-efficient dilution options, have contributed to the segment's growth. The adoption of automated dispensing systems in modern farming facilities has further propelled demand. Furthermore, the increasing preference for ready-to-use solutions among small and medium-sized farm operators continues to support the segment's expansion.

Powder Segment in Animal Disinfectant Market

The powder segment is anticipated to witness the fastest growth in the animal disinfectant market, with a projected CAGR of 7.9% from 2025 to 2030. This robust growth is attributed to key factors such as the segment's enhanced stability and lower transportation expenses compared to liquid alternatives. Powder disinfectants are increasingly preferred due to their longer shelf life and reduced storage requirements, making them a practical choice for distributors and end-users. Advancements in water-soluble packaging and improved dissolution properties are further driving the segment's expansion by addressing previous challenges associated with powder formulations. Manufacturers are also focusing on introducing eco-friendly powder variants to align with sustainable farming practices. Furthermore, the segment is gaining traction in regions with limited cold chain infrastructure, where powder formulations offer significant logistical and operational advantages over liquid options.

Remaining Segments in Animal Disinfectant Market

The gel, foam, and aerosol segments within the animal disinfectant market, though smaller in size, represent a noteworthy share of the market. These alternative formulations are increasingly being adopted in specialized use cases where traditional liquid or powder options may not deliver optimal results. Gel-based disinfectants are gaining traction in veterinary clinics due to their extended contact time and reduced dripping, enhancing their practicality. Foam formulations are becoming more prevalent in small animal care facilities and research laboratories, offering visible coverage and better adherence to vertical surfaces. The aerosol segment is witnessing growth in applications requiring disinfection of hard-to-reach areas within animal housing facilities. These alternative formulations are benefiting from continuous research and development aimed at improving their effectiveness and ease of use.

Animal Disinfectant Market Application Segment Analysis

Poultry Segment in Animal Disinfectant Market

In 2024, the poultry segment retains its leadership in the animal disinfectant market, accounting for approximately 25% of the market share. This dominance is primarily driven by the extensive scale of global poultry operations and the enforcement of stringent biosecurity measures in commercial poultry farming. The segment's growth is further supported by the increasing adoption of intensive farming methods and heightened awareness regarding zoonotic diseases. Regular disinfection of housing facilities, feeding equipment, and transportation vehicles in modern poultry operations sustains a consistent demand for disinfectant products. The recent outbreaks of avian influenza have necessitated stricter hygiene protocols, further boosting disinfectant usage in poultry farming. Additionally, the rising consumer demand for poultry products in emerging markets has led to the expansion of poultry farming activities, thereby driving the demand for animal disinfectants within this segment.

Aquaculture Segment in Animal Disinfectant Market

The aquaculture segment is positioned as the fastest-growing category within the animal disinfectant market, forecasted to achieve a CAGR of 7.7% during the period from 2025 to 2030. This significant growth is attributed to the global expansion of commercial aquaculture operations and the increasing emphasis on aquatic animal health management. The Asia-Pacific region, in particular, is experiencing substantial growth due to the rising adoption of intensive aquaculture practices. Heightened concerns regarding waterborne diseases in fish farming have driven the implementation of specialized disinfection protocols. Regulatory mandates emphasizing aquaculture product quality and safety have also necessitated the adoption of more rigorous disinfection measures. Additionally, advancements in water treatment technologies and the integration of automated disinfection systems in modern aquaculture facilities are further supporting the segment's expansion.

Remaining Segments in Animal Disinfectant Market

The animal disinfectant market's remaining segment, which includes dairy farming, swine, equine, veterinary clinics, and research laboratories, presents significant business opportunities, each with distinct growth trajectories. The dairy farming segment continues to grow steadily, driven by rising standards in milk production and hygiene practices. The swine segment is experiencing significant expansion, fueled by the increasing emphasis on preventing disease outbreaks in commercial pig farming. Veterinary clinics remain key end-users, particularly in developed markets where high pet care standards prevail. The research laboratories segment is gaining prominence due to growing investments in animal health research and development initiatives. Although smaller in scale, the equine segment exhibits stable growth, supported by the professional horse racing and breeding industries. Each of these segments is defined by specific disinfection protocols and requirements, collectively influencing the overall market dynamics through their distinct demand patterns and applications.

Animal Disinfectant Market Geography Segment Analysis

Animal Disinfectant Market in North America

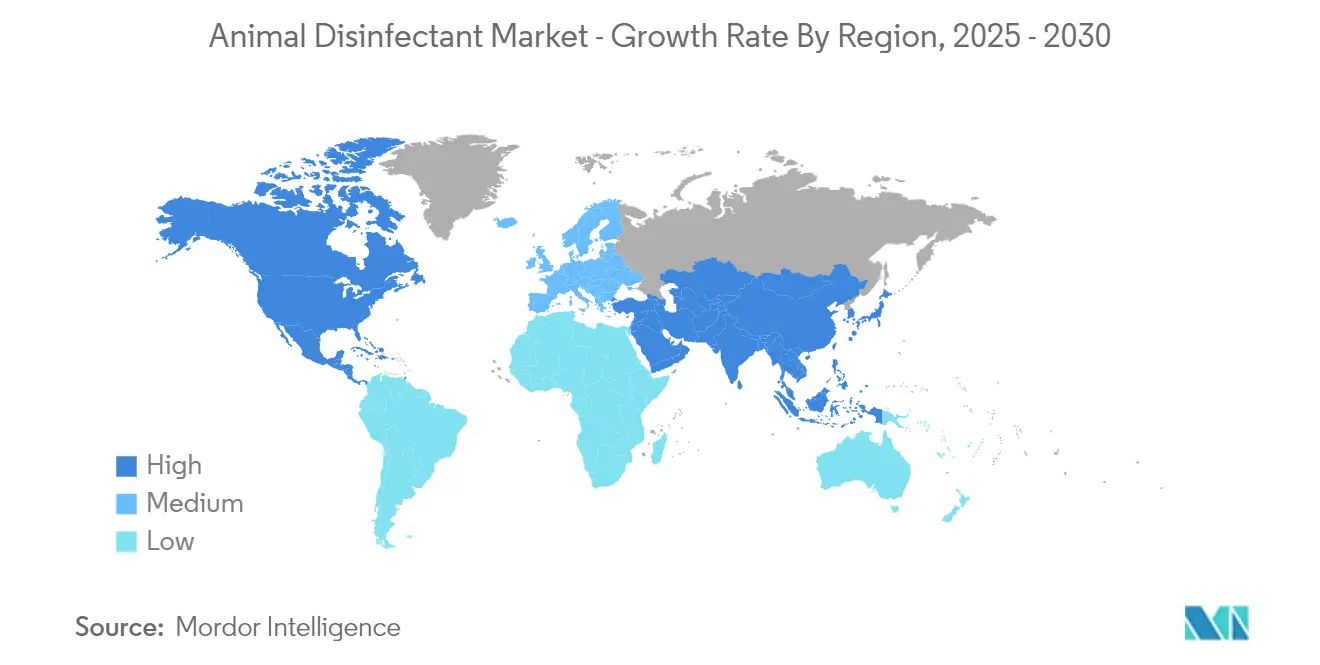

In 2024, North America holds a leading 42% share of the global animal disinfectants market. This dominance is attributed to the region's well-established agricultural infrastructure and advanced livestock management systems. The significant presence of large-scale commercial farming operations, particularly in the United States and Canada, drives robust demand for high-quality disinfection products. Additionally, the region's strict regulatory environment concerning animal health and biosecurity standards supports market growth. The increasing emphasis on preventive healthcare practices in veterinary clinics and research institutions further accelerates market expansion. Furthermore, the presence of key industry players investing in research and development to deliver innovative disinfectant solutions strengthens the region's position. Growing awareness among farmers about the critical role of hygiene in animal facilities has also led to a higher adoption rate of premium disinfectant products.

Animal Disinfectant Market in Europe

Europe is poised for significant growth in its already sophisticated animal disinfectant market from 2025-2030. Stringent regulations on animal welfare and biosecurity, especially in nations like Germany, France, and the UK, shape the region's market landscape. Established livestock farming and a robust veterinary healthcare system bolster this market's expansion. With European farmers placing a premium on preventive healthcare, the demand for effective disinfection solutions surges. Moreover, Europe's commitment to organic farming amplifies the call for eco-friendly and sustainable disinfectants. The market is further buoyed by a strong presence of research institutions and ongoing technological advancements in disinfection. Heightened awareness of zoonotic diseases and their prevention has spurred the adoption of professional-grade disinfectants in various animal care facilities across the continent.

Animal Disinfectant Market in Asia-Pacific

The Asia Pacific animal disinfectants market is anticipated to experience significant growth, with a projected CAGR of approximately 7.9% during the forecast period from 2025 to 2030. This growth is primarily attributed to the rapid expansion of the livestock industry in the region and increasing awareness regarding animal health and hygiene. Key markets such as China, India, and Japan are undergoing substantial modernization in animal farming practices, which is driving the demand for advanced disinfection solutions. The adoption of intensive farming methods and a stronger focus on disease prevention in livestock management are further propelling market growth. Moreover, rising investments in veterinary healthcare infrastructure and higher disposable income levels are contributing to the increased demand for high-quality animal care products. Government initiatives aimed at improving animal health practices and mitigating disease outbreaks in livestock populations are also playing a pivotal role in supporting market development.

Animal Disinfectant Market in the Middle East and Africa

The animal disinfectants market in the Middle East and Africa is poised for growth, driven by increasing investments in livestock farming and a rising focus on animal health. The region is gradually transitioning to modern farming practices, particularly in key markets such as Saudi Arabia and South Africa. Efforts to enhance food security and achieve self-sufficiency in meat production are accelerating the adoption of advanced animal health management solutions. Government initiatives aimed at improving livestock productivity and mitigating disease outbreaks are fostering a supportive environment for market expansion. Additionally, the growing dairy sector and heightened investments in poultry farming are fueling the demand for effective disinfection products. The development of veterinary healthcare infrastructure and increased awareness of hygiene standards in animal facilities further contribute to the market's growth trajectory.

Animal Disinfectant Market in South America

The animal disinfectants market in South America exhibits strong growth potential, driven by the region's extensive livestock industry and an increasing emphasis on animal health management. The market is witnessing advancements in farming practices, particularly in Brazil and Argentina, where modernization efforts are gaining momentum. Rising awareness of biosecurity measures in animal farming is fostering the adoption of specialized disinfection solutions. Additionally, stricter government regulations on animal health and safety are further accelerating market expansion. The growing dairy and poultry industries are generating significant demand for effective disinfection products. Furthermore, the region's focus on producing export-quality meat has led to the implementation of higher hygiene and sanitation standards in animal facilities. Increased investments in veterinary infrastructure and heightened awareness of zoonotic diseases are also key factors driving market growth.

Competitive Landscape

Top Companies in Animal Disinfectant Market

The leading companies in the animal disinfectant market include Neogen Corporation., GEA Group, Lanxess, Zoetis, Solvay, Kersia Group, Stockmeier Group, Ecolab, Albert Kerbl Gmbh, PCC Group, Sanosil Ag, and Delaval Inc. These industry leaders demonstrate consistent focus on research and development to introduce innovative formulations and expand their product portfolios. Companies are increasingly investing in eco-friendly and sustainable disinfectant solutions while strengthening their distribution networks across regions. Strategic partnerships with veterinary clinics, livestock farms, and research laboratories have become crucial for market expansion. The industry witnesses regular product launches incorporating advanced antimicrobial technologies and improved application methods. Companies also emphasizing digital integration for better customer service and supply chain optimization.

Market Structure Shows Balanced Competition Dynamics

The animal disinfectant market is moderately consolidated, with global conglomerates and specialized regional players maintaining a notable presence. Global companies leverage their robust research capabilities and extensive distribution networks to sustain market leadership. Meanwhile, regional players excel by delivering customized solutions tailored to local demands. The market comprises a mix of established manufacturers offering comprehensive product portfolios and niche players focusing on specific application areas or geographic regions. The competitive dynamics of the industry are influenced by the necessity to uphold stringent quality standards while addressing diverse end-user needs across various animal sectors.

Strategic mergers and acquisitions have played a pivotal role in the market, enabling companies to expand their geographic reach and enhance technological expertise. Many firms are prioritizing vertical integration to strengthen their market position and improve operational efficiency. Collaborations between manufacturers and research institutions are increasingly common, fostering the development of innovative formulations. Regional players are scaling their presence through strategic partnerships with established distribution networks, while global companies are acquiring local firms to penetrate emerging markets and access well-established customer bases.

Innovation and Sustainability Drive Future Success

Success in the animal disinfectant market increasingly depends on developing environmentally sustainable products while maintaining high efficacy standards. Companies need to invest in research and development to create innovative formulations that address emerging pathogen challenges while meeting stringent regulatory requirements. Building strong relationships with key stakeholders, including veterinary professionals and livestock farmers, is crucial for market expansion. Manufacturers must focus on developing integrated solutions that combine effective disinfection with ease of application and cost efficiency. Companies should also strengthen their digital presence and implement smart manufacturing processes to improve operational efficiency and market responsiveness.

Market players must address the growing demand for organic and natural disinfectant solutions while maintaining competitive pricing strategies. Success factors include developing robust supply chain networks to ensure product availability and maintaining consistent quality standards across different markets. Companies need to focus on educational initiatives to raise awareness about biosecurity measures and proper disinfection protocols among end-users. Regulatory compliance and obtaining necessary certifications remain critical for market success, particularly in highly regulated markets. Future growth opportunities lie in developing specialized solutions for different animal sectors while maintaining flexibility to adapt to changing market requirements and emerging disease challenges.

Animal Disinfectant Industry Leaders

Neogen Corporation.

Lanxess

Zoetis

Ecolab

Solvay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Byotrol has unveiled Anigene Professional Surface Disinfectant Wipes, marking the debut of the industry's first and only plastic-free surface wipe, fully compliant with all biocidal regulations for feline and other animals. While polypropylene and other plastic-based wipes have long been the industry standard for their reliability and compatibility with biocidal active materials, the UK is set to ban them due to their century-long breakdown period.

- April 2024: Neogen Corporation has introduced Neogen Farm Fluid MAX in Great Britain, with plans to expand its availability to additional European markets, contingent on obtaining global registrations and notifications. This dual-action disinfectant is specifically developed to address the demands of challenging farm environments and is a key element of Neogen's Pathogen Programme.

- October 2023: Oil-Dri Corporation of America has introduced Cat's Pride Antibacterial Clumping Litter, a significant innovation in the United States market. This product is the first antibacterial litter in the country, designed to eliminate 99.9% of odor-causing bacteria. It aims to provide a cleaner litter box environment and promote a more sanitary home for consumers.

- August 2023: Virox Technologies has rolled out updates to its flagship product line, Prevail Ready-to-Use (RTU) and Wipes. With the introduction of a superior Accelerated Hydrogen Peroxide (AHP) formula, the revamped Prevail RTU and Wipes are setting a new benchmark for disinfection in Canada's veterinary practices, animal shelters, and pet boarding facilities.

Global Animal Disinfectant Market Report Scope

According to the scope, animal disinfectants are used to minimize the risk of infection and pathogen transmission in the animals. They support the health and safety of livestock from various diseases and are employed for cleaning the equipment and bedding for sanitization purposes.

The disinfection process leads to the protection and enhancement of a safe environment for livestock farming. The Animal Disinfectants Market is segmented by product type, form, application and geography. By product type, the market is segmented as alcohol‑based disinfectants, iodine‑containing disinfectants, peroxide disinfectants, quaternary ammonium compounds disinfectants, lactic acid disinfectants, and other disinfectants. By form, the market is segmented as liquid. powder, and others. By applications, the market is segmented as dairy farming, poultry, swine, equine, aquaculture, and others. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East, and Africa. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers a value of USD for the above segments.

| Alcohol-based Disinfectants |

| Iodine-containing Disinfectants |

| Peroxide Disinfectants |

| Quaternary Ammonium Compounds Disinfectants |

| Lactic Acid Disinfectants |

| Other Disinfectants |

| Liquid |

| Powder |

| Others |

| Dairy Farming |

| Poultry |

| Swine |

| Equine |

| Aquaculture |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Alcohol-based Disinfectants | |

| Iodine-containing Disinfectants | ||

| Peroxide Disinfectants | ||

| Quaternary Ammonium Compounds Disinfectants | ||

| Lactic Acid Disinfectants | ||

| Other Disinfectants | ||

| By Form | Liquid | |

| Powder | ||

| Others | ||

| By Application | Dairy Farming | |

| Poultry | ||

| Swine | ||

| Equine | ||

| Aquaculture | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Animal Disinfectant Market?

The Animal Disinfectant Market size is expected to reach USD 4.04 billion in 2025 and grow at a CAGR of 7.5% to reach USD 7.20 billion by 2030.

What is the current Animal Disinfectant Market size?

In 2025, the Animal Disinfectant Market size is expected to reach USD 4.04 billion.

Which is the fastest growing region in Animal Disinfectant Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Animal Disinfectant Market?

In 2025, the North America accounts for the largest market share in Animal Disinfectant Market.

What years does this Animal Disinfectant Market cover, and what was the market size in 2024?

In 2024, the Animal Disinfectant Market size was estimated at USD 3.74 billion. The report covers the Animal Disinfectant Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Animal Disinfectant Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: