GCC Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

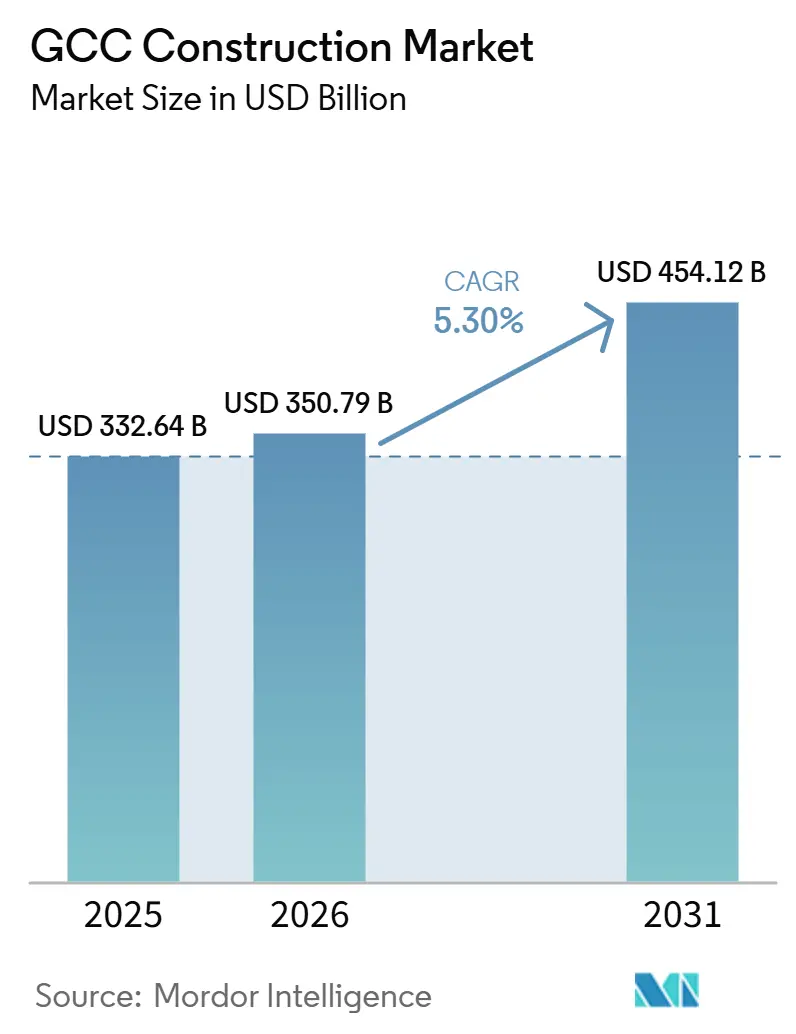

| Base Year Market Size (2025) | USD 332.64 Billion |

| Market Size (2026) | USD 350.79 Billion |

| Market Size (2031) | USD 454.12 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Construction Market Analysis by Mordor Intelligence

The GCC Construction Market size is expected to grow from USD 332.64 billion in 2025 to USD 350.79 billion in 2026 and is forecast to reach USD 454.12 billion by 2031 at 5.30% CAGR over 2026-2031.

This solid trajectory mirrors policymakers’ resolve to diversify economies away from hydrocarbons by fast-tracking infrastructure programs under Saudi Vision 2030 and Dubai’s 2040 Urban Master Plan. Robust public spending insulates the GCC construction market from oil-price swings, while international contractors help transfer advanced technology and finance to regional mega-projects. Across the GCC construction market, modular building systems, 3D concrete printing, and other industrialized methods are speeding project timelines and shrinking labor needs. Private capital is rising through public–private partnership (PPP) structures, and green-building codes now shape bidding criteria, materials choices, and life-cycle cost calculations.

Key Report Takeaways

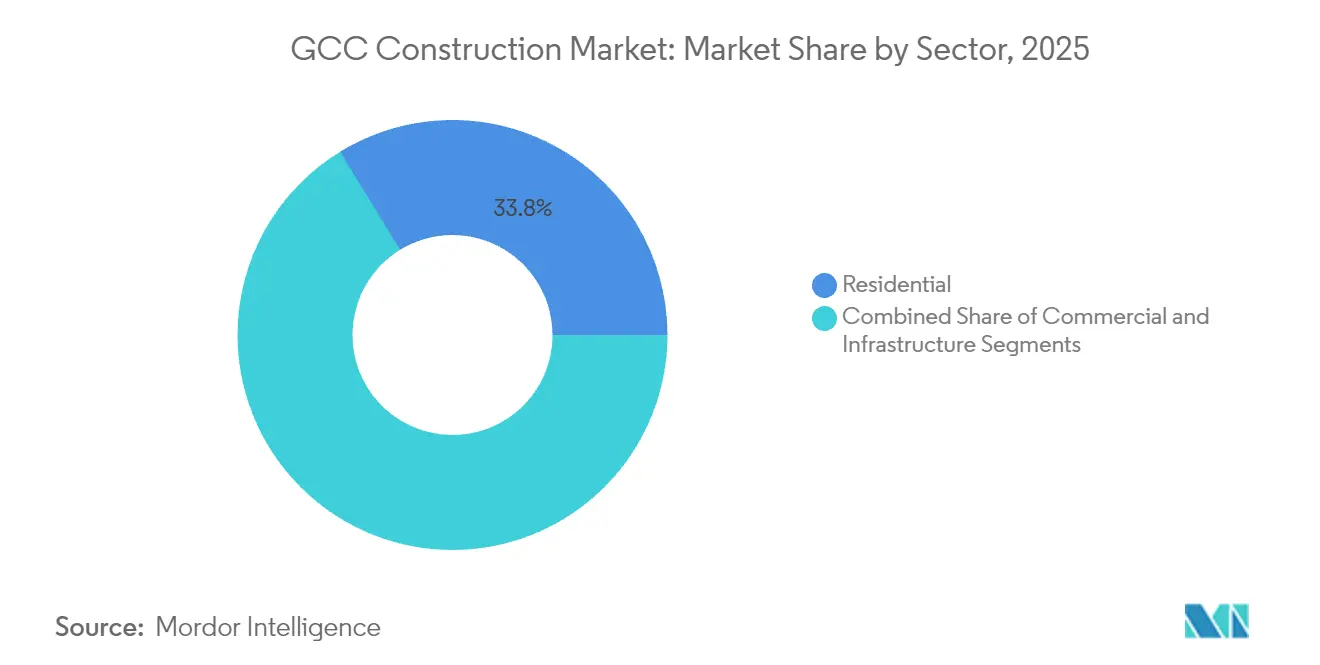

- By sector, infrastructure registered the fastest 5.63% CAGR to 2031, whereas residential construction retained the largest 33.76% portion of the GCC construction market size in 2025.

- By construction type, new construction led with 73.84% of 2025 revenue, while renovation activities are on track to post a 5.18% CAGR through 2031.

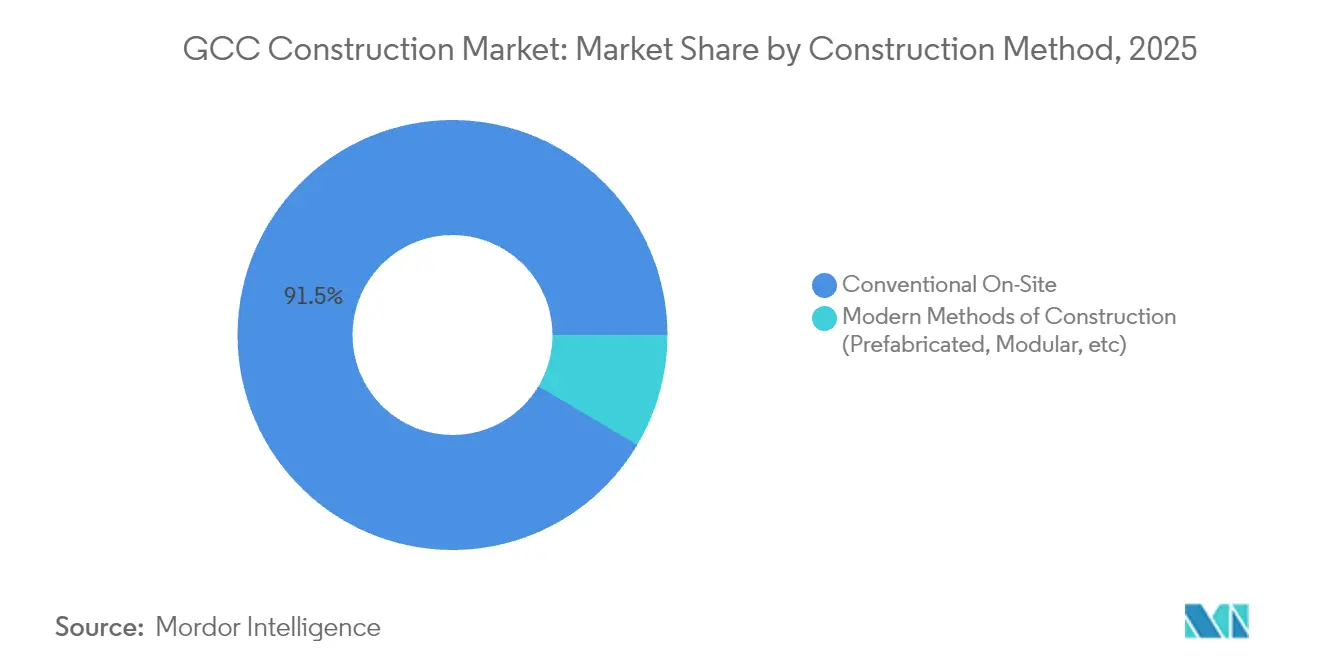

- By construction method, conventional on-site techniques held 91.45% of GCC construction market share in 2025, yet modular approaches are forecast to advance at 9.14% CAGR to 2031.

- By investment source, public entities accounted for 54.92% of the GCC construction market size in 2025, but private funding is growing at a 6.71% CAGR on the back of PPP pipelines.

- By geography, Saudi Arabia commanded 40.60% of the GCC construction market share in 2025 and is expanding at a 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC giga-projects pipeline (Vision 2030, Dubai 2040 Urban Master Plan, etc.) | +1.8% | Saudi Arabia, UAE core with spillover to Qatar, Bahrain | Long term (≥ 4 years) |

| Shift to modular/off-site construction | +0.9% | Global, with early adoption in UAE, Saudi Arabia | Medium term (2-4 years) |

| Mandatory green-building codes (e.g., Estidama, SBC 801) | +0.7% | UAE, Saudi Arabia, with gradual adoption across GCC | Medium term (2-4 years) |

| Revival of religious tourism infrastructure | +0.6% | Saudi Arabia concentrated, with minor spillover to regional connectivity projects | Short term (≤ 2 years) |

| Adoption of project-finance PPP models | +0.5% | UAE, Saudi Arabia leading, expanding to Kuwait, Oman | Long term (≥ 4 years) |

| 3-D-printed concrete pilots scaling to mid-rise assets | +0.3% | UAE, Qatar early adoption, Saudi Arabia scaling initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Giga-Project Pipeline Drives Sustained Construction Demand

Saudi Vision 2030, Dubai’s 2040 Urban Master Plan, and linked mega-initiatives together underpin more than USD 1.8 trillion of schemes that anchor the GCC construction market. The USD 1.554 billion railway contract inside NEOM and USD 810 million financing for Sindalah Island underscore global investor confidence in the region’s execution capacity. Dubai’s 64-kilometer green spine, a USD 8.1 billion renewal of Sheikh Mohammed Bin Zayed Road, blends transit, solar-power generation, and public realm upgrades. Such schemes fuse smart-city digital layers into concrete and steel, creating procurement niches for specialist contractors and driving the GCC construction market toward higher-margin technology-led workstreams[1]Abdulrahman Al-Fadley, “Vision 2030 Projects Update,” Ministry of Economy and Planning, mep.gov.sa.

Modular Construction Methods Transform Project Delivery

Prefabrication is moving from niche pilot to mainstream in the GCC construction market. The SAR 177.7 million (USD 177.7 million) contract for modular worker camps at Trojena proves factory-built units can meet stringent quality and schedule targets. Modular guest-room pods for religious-tourism hotels offer scale benefits while easing urban congestion around holy sites. Regional governments support off-site manufacturing because it seeds new industrial clusters and absorbs local labor, thereby reinforcing economic-diversification targets.

Green-Building Codes Accelerate Sustainable Construction Adoption

The Gulf Organisation for Research and Development (GORD) issued the first regional Sustainable Construction Code, while Saudi Building Code 801 and Abu Dhabi’s Estidama ratings now set minimum performance thresholds on energy, water, and embodied carbon. Compliance pushes demand for high-efficiency façades, solar-ready rooftops, and building-management systems that cut operating costs, aligning climate goals with fiscal prudence. Contractors that integrate environmental modelling and supply-chain traceability into bids stand out in pre-qualification. Local cement and steel makers able to document lower-carbon processes also gain an advantage in the GCC construction market.

3D Concrete Printing Scales Beyond Pilot Projects

Dubai aims for 25% of new buildings to use on-site robotic printing by 2030. Qatar’s 40,000-square-meter printed-school program demonstrates the technology’s leap from decorative pavilions to education infrastructure. Regulatory clarity from Trakhees fast-tracks permit issuance and lowers risk perceptions among financiers. Printed geopolymer mixes can shrink material waste by 30% and cut labor hours 80%, crucial in a region tightening migrant-labor quotas. These performance gains catalyze further uptake, locking 3D printing into the innovation roadmap of the GCC construction market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil fiscal revenues | -1.2% | Saudi Arabia, Kuwait, UAE core impact with regional spillover | Short term (≤ 2 years) |

| Tightened migrant-labour quotas & wage-protection reforms | -0.8% | UAE, Saudi Arabia, Oman with gradual GCC-wide implementation | Medium term (2-4 years) |

| Building-materials price spikes (cement, rebar) | -0.6% | Global impact with acute effects in import-dependent GCC markets | Short term (≤ 2 years) |

| Slow permitting cycles for foreign contractors in GCC region | -0.4% | Kuwait, Saudi Arabia concentrated with moderate UAE, Qatar impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil-Revenue Volatility Constrains Government Infrastructure Spending

The International Monetary Fund warns that combined GCC budget deficits could reach USD 54.2 billion in 2025 if oil averages USD 60 per barrel. Fiscal tightening forces ministries to sequence projects more selectively, stretching payment schedules for contractors. Governments hedge by packaging projects into PPP concessions so that private lenders share cash-flow risk. Firms with strong balance sheets, diversified order books, and robust working-capital lines weather delays better than narrowly focused peers, resulting in gradual industry consolidation within the GCC construction market.

Labor-Market Reforms Increase Construction Operating Costs

All GCC states are rolling out Wage Protection Systems that mandate electronic salary transfers and equalized social-security charges, raising total labor costs by an estimated 15–20% for expatriate-heavy work. Saudi policy now also ties contractor classification to national worker ratios, pushing companies to invest in upskilling citizens or adopt automation to stay competitive. Robotics for rebar tying, drywall finishing, and facade cleaning are gaining traction because payback periods have shortened under the new cost structure. The labor transition favors technology-literate contractors and accelerates digitalization across the GCC construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Acceleration Outpaces Residential Dominance

Infrastructure held 28.31% of the GCC construction market size in 2025, just behind residential’s leading 33.76%. Yet infrastructure is advancing at a 5.63% CAGR to 2031, the fastest among sectors. Dubai’s USD 1.431 billion Al Khaleej Street Tunnel and Abu Dhabi’s USD 8.1 billion Tasreef drainage upgrade illustrate how transport and utilities spending now eclipses private real estate cycles. Contractors capable of heavy civil works, traffic modeling, and micro-tunneling capture larger work packages.

The residential segment remains volume king, propelled by young demographics and mortgage reforms, but growth moderates at 3.31% CAGR. Developers increasingly bundle smart-home systems and district-cooling links to meet green-code thresholds and reduce life-cycle costs. Infrastructure’s momentum is therefore set to dilute residential’s share, reinforcing a shift in the GCC construction market toward public-service assets over pure housing stock.

By Construction Type: Renovation Gains Momentum Despite New-Build Leadership

New-build projects represented 73.84% of GCC construction market share in 2025 and still dominate pipelines. However, renovation and retrofit activities are growing at a 5.18% CAGR as asset owners chase energy savings and code compliance in existing towers. The Gulf construction industry now values certified energy-use intensity metrics, prompting widespread façade re-cladding and HVAC replacement drives.

Renovation also draws on heritage-preservation budgets in Saudi Arabia’s Diriyah and Jeddah Historic Districts. Specialists in laser scanning, BIM-to-field workflows, and lime-based mortars secure premium margins. Investors perceive renovation as less cyclical than ground-up work, thereby smoothing revenue streams across the GCC construction market.

By Construction Method: Modern Approaches Disrupt Traditional Techniques

Conventional on-site operations still comprise 91.45% of GCC construction market share in 2025. Yet modern methods of construction (MMC) post a robust 9.14% CAGR through 2031, gradually biting into traditional dominance. Time-saving prefab bathroom pods and precast façade panels are standard on high-rise hospitality builds in Riyadh and Doha.

Clients now stipulate MMC ratios in tender documents to guarantee timeline certainty and safety performance, triggering supply-chain investments in regional component factories. Digital twins merge with MMC to pre-validate tolerances, further reducing rework and waste. This twin adoption curve confirms MMC as a strategic pillar in the evolution of the GCC construction market.

By Investment Source: Private Funding Accelerates on PPP Tailwinds

Public agencies financed 54.92% of the GCC construction market size in 2025, yet private capital is expanding faster at a 6.71% CAGR thanks to PPP frameworks codified in Saudi, UAE, and Omani law. The USD 628 million Khalifa University housing concession shows how availability-payment models attract pension funds seeking predictable returns.

Private investors favor social-infrastructure and renewable-energy clusters where operational cash flows mitigate traffic-risk volatility common in pure transport PPPs. Local banks syndicate with export-credit agencies to diversify exposure, creating deeper liquidity pools. As a result, private finance will represent a growing slice of the GCC construction market by 2031.

Geography Analysis

Saudi Arabia captured 40.6% of the GCC construction market share in 2025 and is advancing at a 5.52% CAGR through 2031, powered by Vision 2030’s USD-scale mega-projects such as NEOM, Qiddiya, and the Red Sea destination. Cost competitiveness is improving: Q1 2024 iron-ore input prices slid 10% and ready-mix concrete eased 2.5%, giving contractors headroom to absorb wage-policy increases. The Saudi Building Code’s holistic scope, covering seismic, energy, and accessibility standards, sets a compliance baseline now echoed region-wide.

The UAE remains the region’s innovation front-runner. Dubai mandates 25% 3D-printed buildings by 2030 and backs the policy with expedited permitting via Trakhees. Abu Dhabi pours capital into cultural flagships like the USD 1 billion Guggenheim museum, tying construction demand to creative-economy expansion. These moves enhance the UAE’s reputation for integrating smart-city layers and sustainability targets earlier in asset-life cycles, thereby shaping client expectations across the GCC construction market.

Qatar, Oman, Kuwait, and Bahrain together contribute a modest but rising share of activity. Qatar’s establishment of a national 3D-print hub and its 68.5% spike in Q1 2024 project awards confirm its shift toward innovation-led spending. Oman leads on wage-protection enforcement, indirectly pushing mechanical automation uptake. Kuwait’s large budget deficit tempers short-term award volumes yet sets the stage for PPP adoption to reboot stalled schemes. Collectively, these smaller states diversify the opportunity landscape and ease competitive intensity in the broader GCC construction market.

Competitive Landscape

The GCC construction market is moderately fragmented. Regional champions such as ALEC Engineering, Saudi Binladin Group, and Consolidated Contractors Company defend positions by forging technology partnerships exemplified by ALEC’s robotics alliance to automate high-rise floor construction. Chinese majors, notably China State Construction, leverage larger balance sheets and EPC financing packages to clinch signature towers and infrastructure corridors.

Joint ventures proliferate on gigaproject lots because local content rules and global know-how must converge to satisfy developer requirements. Bechtel’s program-management role at NEOM demonstrates the premium on integrated schedule governance spanning hundreds of subcontractors. Meanwhile, disruptors like Printstone3D capture media attention by completing a fully printed gatehouse in under three weeks with a three-person crew, illustrating how agility and novel delivery processes can unlock smaller yet high-margin assignments.

Sustainability credentials now equal price in tender rankings. Firms embed environmental-product declarations and digital-carbon models to meet code-compliance checkpoints. nVent Electric’s USD 1.7 billion thermal-management divestiture signals strategic refocusing on high-growth electrification niches serving the GCC construction market’s green-transition agenda. Collectively, these dynamics underpin a competitive environment where technology adoption and financial structuring skills outweigh simple workforce scale.

GCC Construction Industry Leaders

Nesma & Partners Contracting

Albawani Group

ALEC Engineering and Contracting

Arabian Construction Company

ASGC Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NEOM signed USD 1.554 billion railway contracts and closed USD 810 million Sindalah Island financing; the port opened with USD 2.025 billion first-phase outlay; the green-hydrogen plant reached USD 8.4 billion financial close.

- May 2025: The USD 7 billion Thakher Makkah project hit 62.2% completion, targeting 42,000 hotel rooms for 1.6 million annual visitors.

- April 2025: Diriyah Company awarded a USD 1.4 billion opera-house build to a consortium including CSCEC.

- April 2025: Dubai’s RTA let the USD 1.431 billion Al Khaleej Street Tunnel package.

- March 2025: TC MENA offered USD 39.9 million to buy Gulf Cement Company outright.

GCC Construction Market Report Scope

The construction market is defined as companies that are engaged in the construction of buildings or engineering projects, such as bridges and roads. Construction work also takes place when renovating existing buildings.

The construction market in GCC countries is segmented by sector into commercial construction, residential construction, industrial construction, infrastructure (transportation) construction, and energy and utility construction, and by country into Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates.

The report offers market size and forecasts in value (USD) for all the above segments.

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| United Arab Emirates |

| Saudi Arabia |

| Oman |

| Qatar |

| Kuwait |

| Bahrain |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | United Arab Emirates | |

| Saudi Arabia | ||

| Oman | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

Key Questions Answered in the Report

What is the current value of the GCC construction market?

The GCC construction market size is USD 350.79 billion in 2026.

How fast is the sector expected to grow?

The market is forecast to rise to USD 454.12 billion by 2031, translating into a 5.30% CAGR.

Which country holds the biggest share in regional spending?

Saudi Arabia leads with 40.60% of total activity and posts the fastest 5.52% CAGR through 2031.

What segment is expanding the quickest?

Infrastructure construction is the fastest-growing sector at 5.63% CAGR on large transport and utility programs.

How are green-building rules affecting contractors?

Mandatory codes now require energy-efficient materials and digital carbon tracking, favoring firms with advanced sustainability workflows.

Why are modular methods gaining traction?

Prefabrication shortens schedules, cuts labor dependence and aligns with wage-policy reforms, driving a 9.14% CAGR for modern methods.

Page last updated on: