Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 166.36 Billion |

| Market Size (2026) | USD 173.18 Billion |

| Market Size (2031) | USD 211.71 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Construction Market Analysis by Mordor Intelligence

Australia Construction Market size in 2026 is estimated at USD 173.18 billion, growing from 2025 value of USD 166.36 billion with 2031 projections showing USD 211.71 billion, growing at 4.1% CAGR over 2026-2031.

Large-scale fiscal stimulus, record migration-driven housing demand, and rising public investment in transport and clean-energy assets underpin this outlook. Tier-1 contractors continue to win bigger civil packages while smaller firms struggle with price volatility, pushing consolidation. Prefabrication, modular methods, and digital engineering adoption are increasing as contractors seek productivity gains and compliance with tougher sustainability codes. At the same time, material-cost pressures and labor shortages temper margins, keeping risk management central to project delivery across the Australia construction market.

Key Report Takeaways

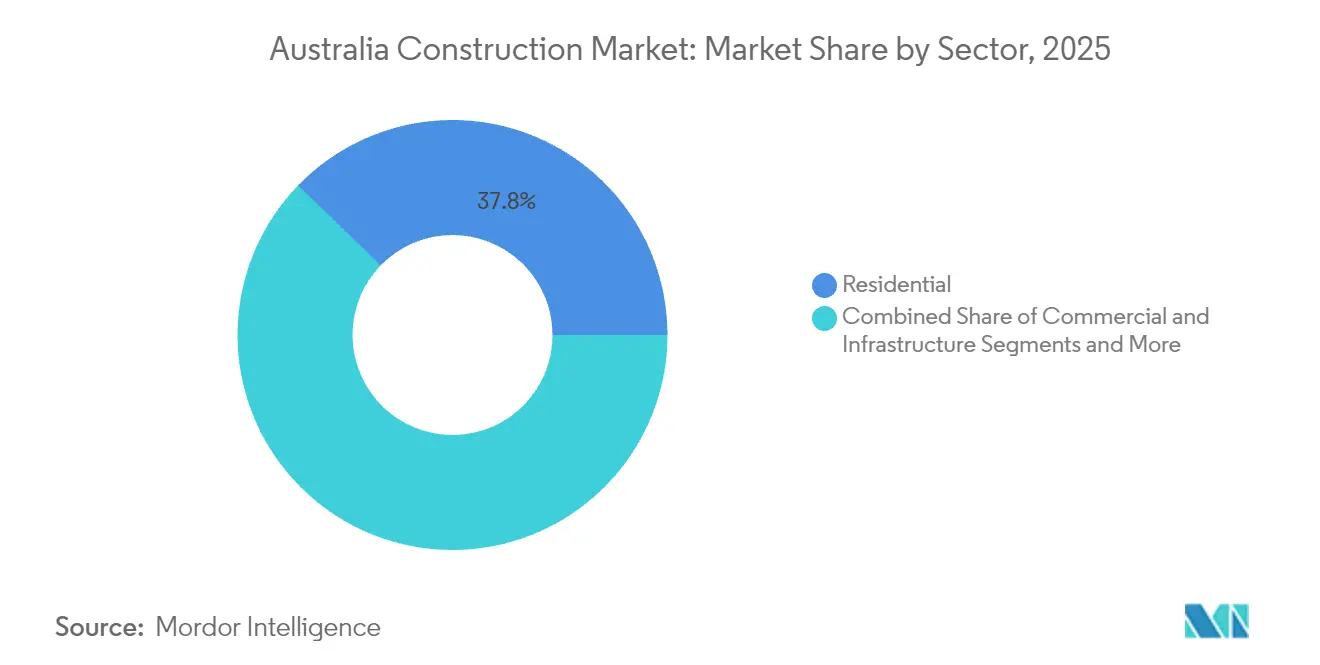

- By sector, the residential segment led with 37.75% of Australia construction market share in 2025, while infrastructure is set to grow fastest at a 6.18% CAGR through 2031.

- By construction type, new construction accounted for 78.45% of the Australia construction market size in 2025; repair & maintenance is projected to expand at a 4.34% CAGR to 2031.

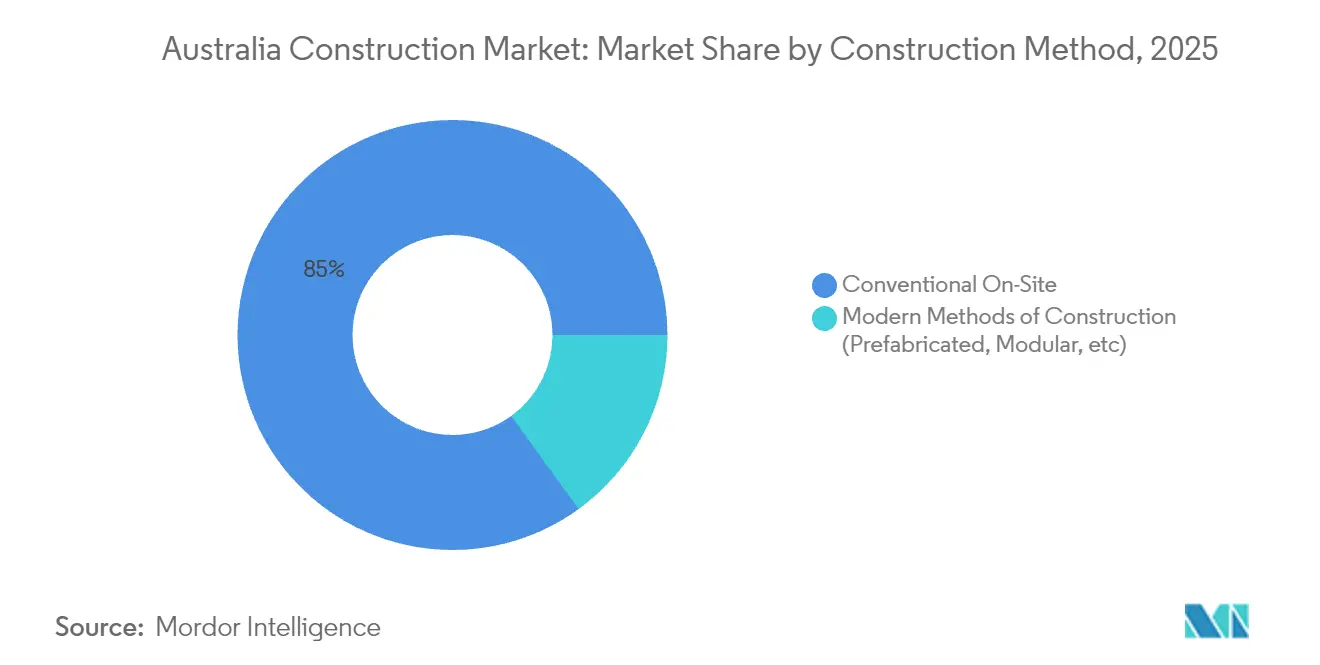

- By construction method, conventional on-site work commanded an 84.98% share of the Australia construction market size in 2025, and modern methods are advancing at a 7.12% CAGR through 2031.

- By investment source, private funding held 90.70% of the Australia construction market share in 2025; public investment records the highest projected CAGR at 6.42% through 2031.

- By Geography, New South Wales contributed 32.10% share of the Australia construction market size in 2025, and Western Australia is on track for the quickest growth at a 4.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-funded fiscal stimulus pipeline | +1.8% | National, with concentration in NSW, Queensland, Victoria | Medium term (2-4 years) |

| Migration-led housing demand rebound | +1.2% | National, with early gains in Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Decarbonisation mandates for public works | +0.9% | National, led by NSW and Victoria regulatory frameworks | Long term (≥ 4 years) |

| Rapid uptake of digital engineering & BIM | +0.7% | National, with higher adoption in tier-1 contractors | Medium term (2-4 years) |

| Expansion of renewable-energy megaprojects | +0.6% | Western Australia, Queensland, with spillover to Victoria | Long term (≥ 4 years) |

| Government first-nations procurement quotas | +0.3% | National, with emphasis on regional and remote areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-funded Fiscal Stimulus Pipeline

Record federal and state allocations are reshaping project pipelines by prioritizing roads, rail, and energy assets. The 2025-26 federal budget earmarks USD 17.1 billion for transport corridors, while Queensland’s USD 5.75 billion Logan & Gold Coast Faster Rail scheme connects Olympic venues with commuter hubs. Victoria sustains momentum via a USD 208 billion rolling capital program that averages USD 19.3 billion annually despite a tight labor supply. These commitments draw private co-investment, deepen subcontractor pipelines, and amplify materials demand across the Australian construction market. The medium-term effect is a reliable baseline of civil workloads that shields contractors from cyclical downturns.

Migration-led Housing Demand Rebound

Net overseas migration of 518,100 people in 2024 has widened the dwelling shortfall, lifting residential approvals after a brief interest-rate dip. The federal target of 1.2 million new homes by 2029 requires completions to jump from 176,000 to 240,000 annually, creating visibility for developers and volume homebuilders. Investor sentiment is improving as rental yields rise in major cities, supporting multi-family projects. Skills gaps persist, however, with the sector needing 90,000 extra workers, thereby inflating wages and stretching schedules. Short-term growth in the Australia construction market, therefore, rests on bridging labor shortages and fast-tracking approvals to match high-density demand hotspots[1]Victorian Government, “State Capital Program 2025,” vic.gov.au.

Decarbonization Mandates for Public Works

The National Construction Code 2025 tightens commercial energy-efficiency thresholds, while NSW’s Sustainable Buildings SEPP aims to cut 2.6 million tCO₂e by 2033. Queensland now requires 7-star residential energy ratings, pushing architects and contractors toward low-carbon materials and on-site renewables. These rules shift bid evaluation toward carbon credentials and life-cycle performance, giving early adopters of green-cement, recycled steel, and mass-timber systems a competitive edge. Over the long term, the mandates funnel additional value into specialized consultancies and green-tech suppliers across the Australia construction market.

Rapid Uptake of Digital Engineering & BIM

Technology diffusion is accelerating: 37% of firms now deploy AI-enabled design coordination, up from 26% in 2023. Infrastructure Victoria estimates AI could shave 23% off education projects ' overruns, saving USD 516.1 million by 2055. Contractors are layering drones, robotics, and GPR into asset inspection workflows, lowering rework and safety costs. Each additional technology adopted is linked to a 1.14% revenue uplift, reinforcing ROI arguments. Wider digital adoption increases transparency for financiers and regulators, accelerating payment cycles and improving cash-flow stability across the Australia construction market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Material-price volatility & supply chain bottlenecks | -1.4% | National, with acute impact on Queensland and Western Australia | Short term (≤ 2 years) |

| Skilled-labour shortages & wage inflation | -1.1% | National, with critical shortages in NSW and Victoria | Medium term (2-4 years) |

| Tightening credit & high mortgage rates | -0.8% | National, with greater impact on residential construction | Short term (≤ 2 years) |

| Rising insurance premiums on combustible cladding | -0.4% | National, with particular focus on high-rise developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Material-price Volatility & Supply-chain Bottlenecks

Building construction prices rose 31.1% between September 2020 and June 2024, while house construction costs climbed 40.8% in the same span. Steel, concrete, and gypsum continue to see double-digit quarterly rises, with suppliers warning bathroom fixtures could add another 7% in 2025. Contractors locked into fixed-price contracts face margin erosion, fuelling a 28% jump in insolvencies to 2,832 firms in FY 2024 AFR.COM. Although global freight rates have eased, domestic logistics and specialized component shortages still generate scheduling risk that subtracts momentum from the Australia construction market.

Skilled-labor Shortages & Wage Inflation

Construction unemployment fell to a record low of 3.2% in early 2025, leaving projects in Sydney and Melbourne short of carpenters, electricians, and project managers. BuildSkills Australia warns the sector needs 90,000 extra workers to meet housing targets, yet only 2.8% of recent migrants hold construction roles. Firms are offering premiums and flexible rosters to attract talent, but higher wage bills raise tender prices and stall marginal projects. Over the medium term, limited training capacity and slow skills-recognition processes threaten delivery schedules, shaving 1.1 percentage points off the potential CAGR for the Australia construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Leads Growth Momentum

Infrastructure spending has reset the competitive mix, yet residential remains the largest contributor with a 37.75% Australia construction market share in 2025. Civil contractors are ramping up resources to deliver the USD 7.1 billion Brisbane 2032 venues and the USD 17.1 billion federal road-rail slate, driving order books beyond 2027. Renewable-energy assets such as Western Australia’s USD 584 million Clean Energy Link North and the USD 2.8 billion Alkimos Desalination Plant illustrate the pivot toward climate-resilient infrastructure.

Infrastructure exhibits the fastest 6.18% CAGR through 2031 as governments front-load capital programs for productivity and decarbonization aims. The Australia construction market size for transport corridors alone is projected to reach USD 63.4 billion by 2031, propelled by corridor duplications and intermodal hubs. Residential activity benefits from the USD 1.5 billion Housing Support Program, yet approvals remain below the 240,000 annual threshold required to rebalance supply. Commercial construction is muted, but pockets such as data centers show 57% year-over-year growth driven by AI workloads, offering diversification to contractors.

By Construction Type: Renovation Gains Traction

New construction held a commanding 78.45% of % Australian construction market share in 2025, underscoring the scale of greenfield housing estates and mega-infrastructure builds. However, repair & maintenance logs a 4.34% fastest CAGR to 2031 as asset owners extend lifecycles under fiscal and carbon constraints. Regulatory tightening through the National Construction Code 2025 mandates retrofits for energy efficiency, compelling commercial portfolios to upgrade HVAC, façades, and onsite renewables.

High-profile refurbishments, such as the Reserve Bank headquarters escalation from USD 260 million to USD 1.1 billion after asbestos discoveries, highlight the complexity premiums embedded in retrofit work. Asset management strategies increasingly prioritize predictive maintenance, leveraging IoT sensors to schedule interventions before failures. For contractors, the renovation wave offers counter-cyclical revenue, helping stabilize earnings when greenfield pipelines pause, thereby supporting balanced growth in the Australia construction market.

By Construction Method: Modern Methods Accelerate

Conventional on-site activity still dominated with an 84.98% Australia construction market size share in 2025, reflecting entrenched procurement models and supply chains. Yet, prefabricated and modular solutions are accelerating at a 7.12% CAGR through 2031 on government backing and demonstrable time savings. The federal USD 54 million modular-housing fund and NSW’s 24-unit South Grafton project, finished in six months, show proof-of-concept for speed-to-market.

Imports of prefabricated homes reached USD 500 million over five years, with Chinese suppliers holding a 70% share. The Australian Building Codes Board has issued a dedicated handbook to streamline compliance, mitigating approval-risk perceptions. Scale, workforce upskilling, and localized manufacturing remain barriers, but accelerating adoption is expected to compress delivery times by up to 40%, supporting higher turnover in the Australia construction market.

By Investment Source: Public Sector Momentum

Private capital retained a 90.70% Australia construction market share in 2025, driven by housing and commercial pipelines. Public investment, however, is forecast for a 6.42% CAGR through 2031 as governments fund strategic transport, social, and renewable-energy projects. Victoria’s USD 208 billion capital program and the USD 1.5 billion Housing Support Program illustrate a shift to mission-oriented spending that crowds in private partners via PPP frameworks.

Budget allocations prioritize productivity and emissions outcomes, positioning public funding as a counter-cyclical anchor for the Australia construction market. Contractors with demonstrated ESG-compliant delivery and digital transparency strike the best bid-win ratios on these packages. Elevated interest rates and cost inflation constrain private speculative builds, yet institutional investors continue to back logistics and data-center assets, hedging inflation through indexed leases.

Geography Analysis

New South Wales maintains its leadership position with 32.10% of the Australia construction market share, supported by major transport and urban renewal projects that stimulate housing and commercial spinoffs. The completion of the USD 786 million Bridgewater Bridge enhances freight efficiency, while the state’s Sustainable Buildings SEPP creates a pipeline for low-carbon retrofits. Insolvencies among Canberra builders underscore financial strains, yet large civil contracts continue to draw tier-1 participation.

Victoria’s market reflects an ambitious USD 208 billion capital program, spanning hospital expansions, schools, and the Suburban Rail Loop. Infrastructure investment peaked at USD 24 billion in FY 2024 before normalizing, but workforce constraints persist, prompting project-sequencing adjustments. A gradual policy shift toward prefabrication and modular classrooms is emerging to meet delivery deadlines and NCC 2025 energy targets.

Western Australia is forecast for the fastest 4.48% CAGR, driven by resource megaprojects, population inflows, and clean-energy infrastructure. Projects such as Northern Star’s USD 1.3 billion gold mine and the Clean Energy Link North upgrade keep engineering demand high. Renewable schemes align with the state’s coal-exit timeline by 2030, ensuring sustained grid and storage procurement. Together, these dynamics sustain balanced growth across regions, reinforcing nationwide activity in the Australia construction market.

Competitive Landscape

Tier-1 contractors have expanded their share of public infrastructure work from 49% to 59% since 2016, with average contract values approaching USD 600 million. CIMIC Group leverages global data-center expertise to secure hyperscale builds, while Lendlease is refocusing domestically after USD 2.8 billion of offshore divestments to simplify its balance sheet. Smaller firms contend with razor-thin margins and higher insolvency risk, intensifying the bar for surety bonding and digital compliance.

Strategic differentiation is pivoting toward technology enablement and ESG credentials. CPB Contractors integrates drone surveying and AI scheduling on the Main South Road Duplication to cut rework and carbon footprint. ACCIONA and SUEZ have secured a USD 322 million water-plant build through design-build-operate models that transfer performance risk while optimizing lifecycle revenue. Foreign entrants are active: UAE-based Arada acquired Roberts Co NSW, signaling international appetite for mid-tier Australian assets.

Market whitespace centers on prefabrication, carbon-neutral materials, and AI-driven project controls. The federal USD 54 million modular-housing fund lowers entry barriers for specialist manufacturers, and early adopters already report 25% schedule savings. Contractors are able to combine off-site manufacturing with integrated digital twins to capture procurement advantages in upcoming PPP bids. Overall, competitive intensity is shifting from raw capacity toward innovation and sustainability leadership inside the Australia construction market.

Australia Construction Industry Leaders

CPB Contractors

Lendlease Corporation Ltd

John Holland Group

Laing O’Rourke

Multiplex (Brookfield)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Western Australia fast-tracked the USD 584 million Clean Energy Link North project, targeting completion by 2027 to enable coal retirement by 2030.

- July 2025: New South Wales opened a 24-unit modular social-housing estate in South Grafton after a six-month build under a USD 9 million contract.

- June 2025: Tasmania’s USD 786 million Bridgewater Bridge commenced traffic, improving freight travel times.

- May 2025: Gold Fields raised its bid for Gold Road Resources to USD 3.7 billion, while Northern Star launched a USD 1.3 billion mine build creating 900 construction jobs.

Australia Construction Market Report Scope

Civil construction is a subset of civil engineering, which is concerned with the design, construction, and maintenance of the physical and naturally built environment. The art of building bridges, dams, roads, airports, canals, and buildings is known as civil construction.

A complete background analysis of the Australia Construction Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report. The Australia Construction Market is segmented by Sector (Residential, Commercial, Industrial, Infrastructure (Transportation), Energy, and Utilities). The report offers market size and forecasts for the Australia Construction market in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| Rest of Australia |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| Rest of Australia | ||

Key Questions Answered in the Report

How big is the Australia construction market in 2026?

The Australia construction market size stands at USD 173.18 billion in 2026 and is forecast to reach USD 211.71 billion by 2031.

What CAGR is expected for Australian construction to 2031?

The sector is projected to expand at a 4.1% CAGR during the 2026-2031 period.

Which segment grows fastest within Australian construction?

Infrastructure is the fastest-growing segment with a 6.18% CAGR, driven by transport and clean-energy spending.

Which state is set for the highest growth?

Western Australia shows the quickest trajectory with a 4.48% CAGR through 2031, supported by resource and renewable projects.

What is the main challenge facing builders?

Material-price volatility and acute labor shortages are pressuring margins and timelines for contractors nationwide.

How are modern construction methods evolving?

Prefabricated and modular techniques are rising at a 7.12% CAGR thanks to federal funding and faster delivery times, though they still form a small share of total activity.

Page last updated on: