Amlodipine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

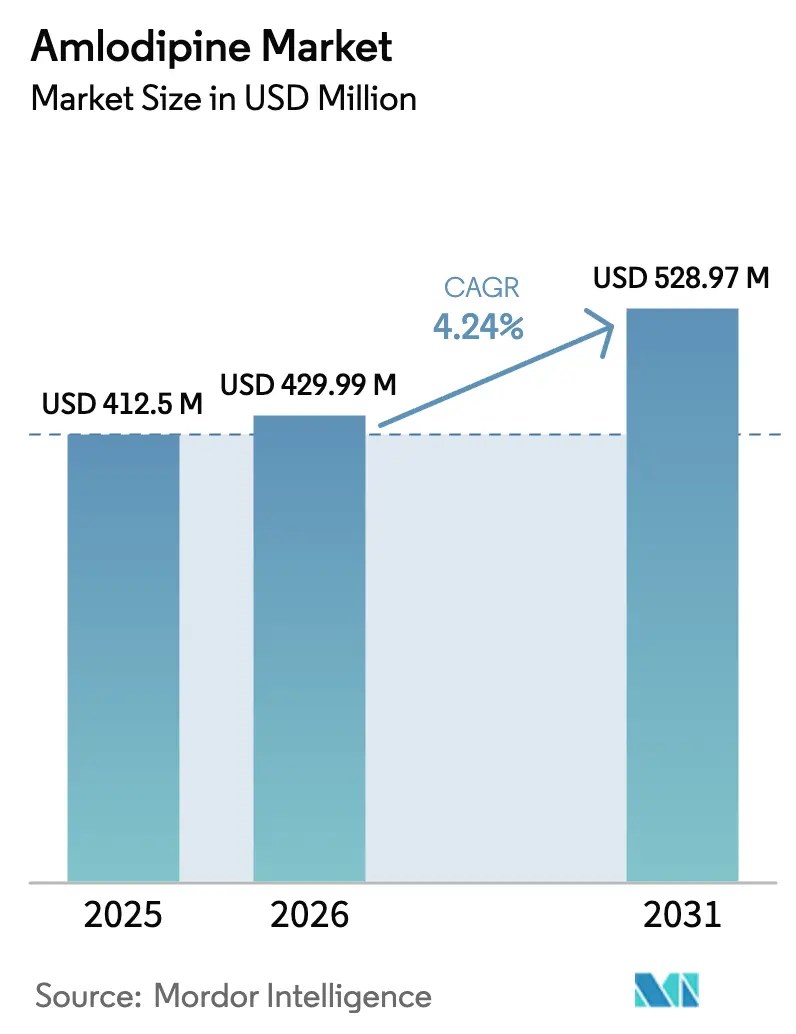

| Market Size (2026) | USD 429.99 Million |

| Market Size (2031) | USD 528.97 Million |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

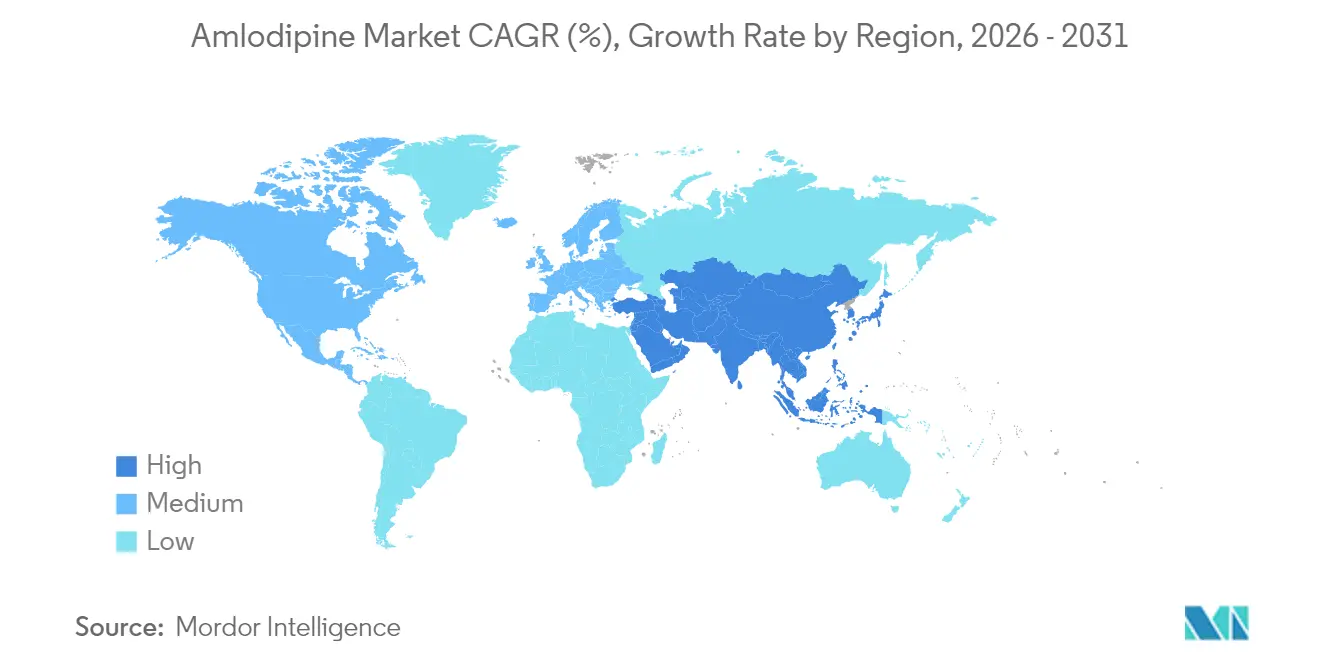

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amlodipine Market Analysis by Mordor Intelligence

The Amlodipine market size is expected to grow from USD 412.50 million in 2025 to USD 429.99 million in 2026 and is forecast to reach USD 528.97 million by 2031 at 4.24% CAGR over 2026-2031. Sustained demand stems from the drug’s status as a first-line calcium-channel blocker for hypertension, even as patent expirations intensify generic rivalry. Generic penetration is reshaping pricing and access; procurement frameworks in China and reference-pricing policies in Europe increase volumes yet cap margins. Fixed-dose combinations and digital adherence tools widen therapeutic uptake, while ageing populations in Asia-Pacific and North America enlarge the addressable patient base. Manufacturing scale, regulatory experience, and formulation innovation remain the core competitive levers in the evolving Amlodipine market.

Key Report Takeaways

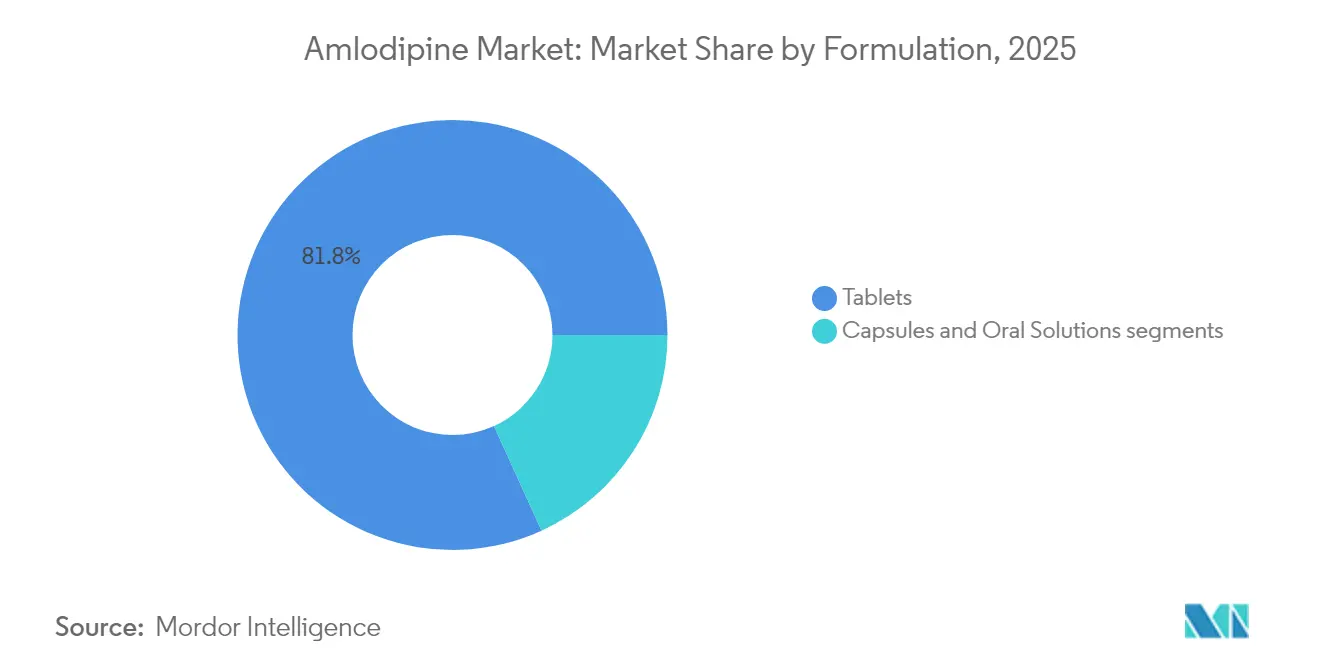

- By formulation, tablets led with 81.80% revenue share in 2025, whereas oral solutions are projected to expand at a 5.16% CAGR to 2031.

- By dosage strength, the 5 mg tier held 47.05% of the Amlodipine market share in 2025, while 2.5 mg is on track for a 5.28% CAGR through 2031.

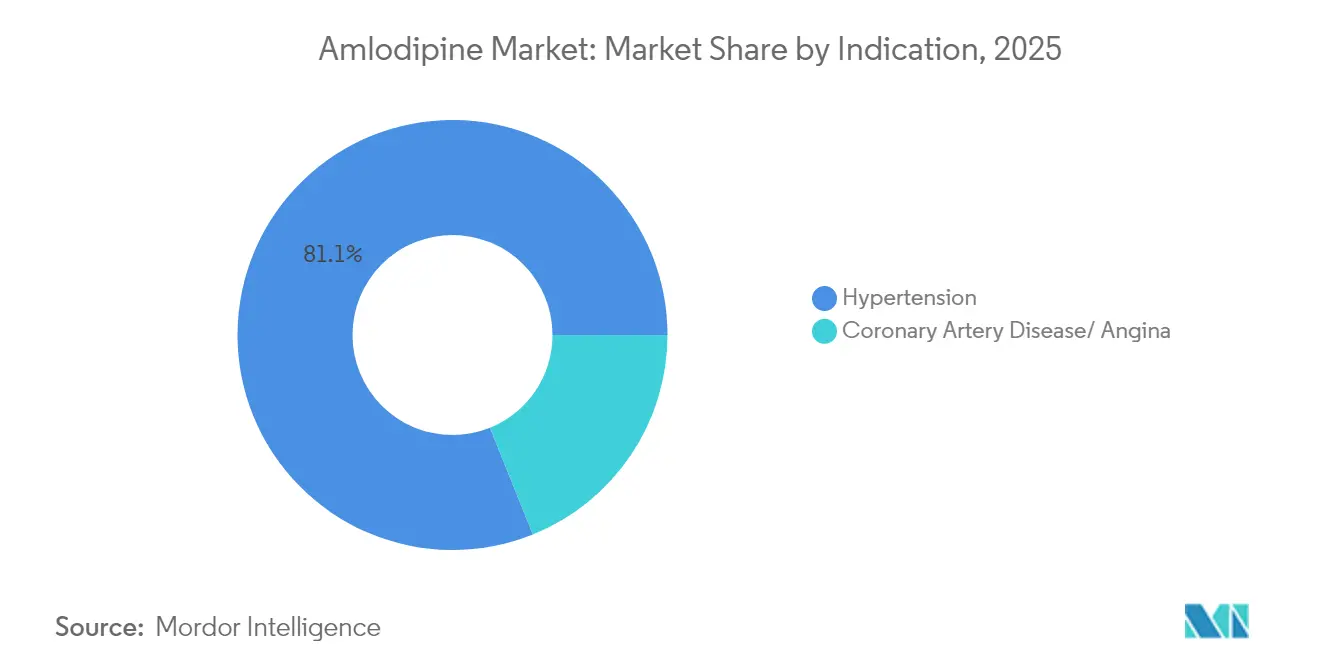

- By indication, hypertension accounted for 81.10% of use in 2025; coronary artery disease is poised for a 5.43% CAGR.

- By distribution channel, retail pharmacies captured 55.95% share in 2025, with online pharmacies progressing at a 5.58% CAGR.

- By geography, North America commanded 33.20% of revenue in 2025; Asia-Pacific is forecast to grow at a 5.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Amlodipine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Loss-of-exclusivity generic penetration | +1.2% | Global; strongest in US and Europe | Short term (≤ 2 years) |

| Hypertension prevalence in ageing populations | +0.8% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Fixed-dose combination approvals | +0.6% | Early uptake in developed markets; expanding worldwide | Medium term (2-4 years) |

| China bulk-buy procurement | +0.4% | Core influence in China; spill-over to emerging economies | Medium term (2-4 years) |

| AI-guided dose titration | +0.3% | North America and EU; adoption in Asia-Pacific | Medium term (2-4 years) |

| S-amlodipine development | +0.2% | Premium patient segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Loss-of-Exclusivity–Driven Generic Penetration

Accelerated generic approvals follow streamlined FDA guidance, enabling rapid entry for firms with proven quality systems[1]Source: Federal Register, “Product-specific guidances; revised draft guidances for industry; availability,” federalregister.gov. Indian manufacturers leverage cost efficiencies and a USD 63.7 billion global patent-cliff to gain share . Therapeutic equivalence studies confirm no added cardiovascular risk, validating substitution in value-constrained health systems. Competitive dynamics bifurcate into premium formulations and high-volume commodity generics, each supported by tailored pricing strategies. The driver raises short-term volumes yet compresses price points, reshaping the Amlodipine market within two years.

Hypertension Prevalence in Ageing Populations

WHO data show 1.28 billion adults living with hypertension and only 21% achieving control, with prevalence hitting 47% among older Chinese adults. Age-linked risk escalates demand for established therapies, underpinning long-term growth in the Amlodipine market. National initiatives such as India’s Hypertension Control Initiative report 70-76% control rates using standardized 5 mg protocols. As emerging markets expand coverage, demand for affordable generics rises. This structural demographic driver sustains the forecast CAGR through 2030.

Fixed-Dose Combination (FDC) Approvals Accelerating Uptake

Regulatory bodies increasingly endorse amlodipine-based FDCs to improve adherence. FDA clearance of Widaplik, a triple-combination polypill, demonstrated superior blood-pressure reduction over monotherapy. WHO inclusion of two-drug FDCs in the Essential Medicines List validates economic benefits. Manufacturers with diversified FDC portfolios gain competitive advantage, driving medium-term uptake across developed and emerging regions.

China’s Bulk-Buy Procurement Expanding Volume Demand

Centralized purchasing cut outpatient hypertension spend 15.61% while lifting volumes 49% for selected Amlodipine formulations. Domestic generics dominate tenders, pressuring international players yet broadening access. The transparent volume-price mechanism influences procurement models in other large markets, signaling medium-term volume growth but persistent margin compression.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-ceiling policies | -0.7% | Developed markets with public reimbursement | Short term (≤ 2 years) |

| API supply volatility | -0.5% | Global, concentrated in Asia-Pacific supply chains | Medium term (2-4 years) |

| Pharmacovigilance alerts | -0.3% | Regulatory focus in US and EU | Medium term (2-4 years) |

| Device-based hypertension therapies | -0.2% | Premium segments in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Ceiling Policies in Key Markets

US Medicare price negotiations may drive discounts of up to 70% versus current list prices [2]Source: Commonwealth Fund, “How prices for first 10 drugs compare internationally,” commonwealthfund.org . Europe enforces reference pricing that ties reimbursement to the lowest-priced therapeutic equivalent, squeezing branded margins. Manufacturers shift toward outcome-based pricing yet face limited acceptance, reinforcing near-term pressure on the Amlodipine market.

API Supply Volatility from India–China Trade Tensions

India imports 70% of its Amlodipine API from China; new Chinese regulations and shipping delays raised besylate prices in early 2025. India’s Production Linked Incentive Scheme funds domestic API plants, but capacity ramps take years. Tariff threats in the US add further cost uncertainty. Supply diversification programs mitigate risk yet entail higher working-capital demands, restraining medium-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Tablets Maintain Predominance Amid Oral Solution Growth

Tablets retained 81.80% revenue in 2025, reflecting established manufacturing lines and broad prescriber familiarity. Oral solutions, though only a small slice of the Amlodipine market, exhibit the swiftest rise at a 5.16% CAGR due to pediatric demand and swallowing-difficulty accommodations. Capsule formats cater to niche modified-release needs. The 2022 FDA approval of Norliqva illustrates regulatory openness to patient-centric oral solutions.

Continuous melt-milling and other advanced processes allow sub-micron particles that boost dissolution, supporting novel oral dispersible formats. These innovations strengthen adherence without altering therapeutic equivalence. Manufacturers that optimize production economics for both high-volume tablets and specialty liquids position themselves for incremental Amlodipine market share gains through 2031.

By Dosage Strength: 5 mg Leadership Under Precision-Dosing Spotlight

The 5 mg strength commanded 47.05% of the Amlodipine market share in 2025, in line with global guidelines that recommend it as the initial dose. The 2.5 mg tier is expanding fastest, at a 5.28% CAGR, as AI-enabled titration favors tailored regimens that reduce edema risk. Remote monitoring during the COVID-19 period pushed 80% control rates with app-guided dose adjustments. Pharmacogenomic findings linking CACNA1C variants to enhanced response further reinforce precision-dosing interest. The 10 mg segment serves severe hypertension yet grows modestly because of higher adverse-event vigilance. Precision-dosing tools will likely moderate 5 mg dominance yet support overall Amlodipine market size expansion by optimizing outcomes for diverse patient cohorts.

By Indication: Hypertension Core with CAD Momentum

Hypertension drove 81.10% of 2025 prescriptions, underscoring Amlodipine’s role in first-line therapy. Coronary artery disease prescriptions are increasing at a 5.43% CAGR, buoyed by evidence linking amlodipine to a 26% reduction in major adverse cardiovascular events when bundled into integrated protocols. Longer-term observational studies also hint at cognitive-benefit potential after multiyear exposure. The widening clinical footprint fortifies the Amlodipine market through indication diversity while facilitating combination-therapy adoption.

By Distribution Channel: Retail Pharmacy Strength Meets Digital Upsurge

Retail outlets captured 55.95% of revenue in 2025 by pairing prescription fulfillment with in-store blood-pressure services. Online pharmacies, however, are advancing at a 5.58% CAGR as consumers migrate to e-commerce for chronic-care refills. Telemedicine and e-prescription integration reduce friction, making door-step delivery attractive for elderly and rural populations. Hospital pharmacies focus on complex cases but face growth headwinds as outpatient hypertension management rises. An omnichannel strategy that blends telehealth, automated refills, and community counseling is becoming critical for sustained Amlodipine market penetration.

Geography Analysis

North America generated 33.20% of global revenue in 2025 on the back of approximately 116 million hypertensive adults and well-funded insurance systems. Market expansion centers on adherence technologies and combination pills since basic access is largely assured. Medicare price negotiations create immediate price pressure yet may raise filled-prescription volumes by trimming out-of-pocket costs. Canada’s province-run formularies achieve utilization efficiency through automatic generic substitution, reinforcing stable demand for cost-effective Amlodipine market options.

Asia-Pacific represents the fastest-growing territory, advancing at a 5.74% CAGR to 2031. China’s bulk-buy model increased amlodipine unit volumes 49% in early procurement waves, offsetting 42% price cuts. India’s Hypertension Control Initiative recorded 70-76% control rates with standardized amlodipine-first protocols across two populous states. Rapid urbanization and ageing heighten prevalence, while government health-insurance expansions widen drug access. Southeast Asian nations adopt WHO essential-medicine frameworks that favor low-cost generics, reinforcing the region’s long-term contribution to overall Amlodipine market size.

Europe exhibits mature yet opportunity-rich characteristics. Reference pricing and HTA reviews ensure cost-effectiveness scrutiny, but stable cardiovascular guidelines uphold steady usage. Eastern Europe displays higher unmet need, where income growth and EU accession funds modernize health infrastructure. Manufacturers tailor market-access files to national cost-utility thresholds, keeping the Amlodipine market relevant across divergent reimbursement climates.

Competitive Landscape

The Amlodipine market shows moderate concentration. Leading generic producers such as Teva, Viatris, and Indian firms Cipla, Dr. Reddy’s, and Lupin combine vertical integration with global regulatory dossiers to secure tenders and retail contracts. Cipla’s One-India division crossed INR 10,000 crore revenue in 2024, reflecting a 10% rise in chronic therapy sales. Scale economies in API production, dossier maintenance, and pharmacovigilance underpin sustainable cost advantages, especially in large public-procurement settings.

Formulation innovation provides white-space differentiation. George Medicines gained FDA approval for Widaplik, a triple-combination pill that simplifies multidrug regimens and supports premium pricing in targeted segments. Development of S-amlodipine offers edema-reduction benefits, with trials noting a 15.1% absolute reduction in peripheral edema versus the racemate. Continuous manufacturing methods introduced by several Indian CDMOs deliver tighter quality control and lower per-tablet conversion costs, enhancing supply reliability for global buyers.

Future rivalry will hinge on omnichannel distribution, supply-chain resilience, and the ability to furnish integrated cardiovascular portfolios. Manufacturers that combine competitive unit costs with differentiated polypills, digital adherence platforms, and diversified API sourcing will likely outpace commodity-only players in the expanding Amlodipine market.

Amlodipine Industry Leaders

Cipla Limited

Lupin Pharmaceuticals, Inc.

Mylan Inc (Viatris Inc.)

Pfizer

Zydus Cadila

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: George Medicines received FDA approval for Widaplik, a triple-combination polypill containing telmisartan, amlodipine, and indapamide, with commercial launch planned for Q4 2025.

- May 2025: Mineralys Therapeutics announced pivotal Launch-HTN trial data for lorundrostat, showing 16.9 mmHg systolic reduction at Week 6 and 19.0 mmHg at Week 12 in uncontrolled hypertension.

- January 2025: Global amlodipine besylate prices spiked after Chinese production delays, exposing supply-chain vulnerabilities

Global Amlodipine Market Report Scope

As per the report’s scope, amlodipine besylate is a calcium channel blocker class member that effectively reduces blood pressure. It achieves this by relaxing blood vessels and easing the heart's workload. Beyond blood pressure management, Amlodipine addresses specific angina types (chest pain) and conditions stemming from coronary artery disease, characterized by narrowed blood vessels supplying the heart.

The amlodipine market is segmented by form, concentration, application, and end-user. The market has been segmented by form into tablets, oral suspensions, and others. Based on concentration, the market is segmented into 2.5 mg, 5 mg, 10 mg, and others. By application, the market is segmented into chest pain, coronary artery disease (CAD), and hypertension. By end-user, the market covers hospital pharmacies, retail pharmacies, online pharmacies, and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report details market size and forecasts for 17 countries across these regions, with valuations presented in USD.

| Tablets |

| Capsules |

| Oral Solutions |

| 2.5 mg |

| 5 mg |

| 10 mg |

| Hypertension |

| Coronary Artery Disease / Angina |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Europe | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Formulation (Value) | Tablets | |

| Capsules | ||

| Oral Solutions | ||

| By Dosage Strength (Value) | 2.5 mg | |

| 5 mg | ||

| 10 mg | ||

| By Indication (Value) | Hypertension | |

| Coronary Artery Disease / Angina | ||

| By Distribution Channel (Value) | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Europe | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Amlodipine Market?

The Amlodipine Market size is expected to reach USD 429.99 million in 2026 and grow at a CAGR of 4.24% to reach USD 528.97 million by 2031.

What is the current Amlodipine Market size?

In 2026, the Amlodipine Market size is expected to reach USD 429.99 million.

Who are the key players in Amlodipine Market?

Cipla Limited, Lupin Pharmaceuticals, Inc., Mylan Inc (Viatris Inc.), Pfizer and Zydus Cadila are the major companies operating in the Amlodipine Market.

Which is the fastest growing region in Amlodipine Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Amlodipine Market?

In 2025, the North America accounts for the largest market share in Amlodipine Market.

What years does this Amlodipine Market cover, and what was the market size in 2025?

In 2025, the Amlodipine Market size was estimated at USD 429.99 million. The report covers the Amlodipine Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Amlodipine Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: