Croatia Pharmaceutical Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

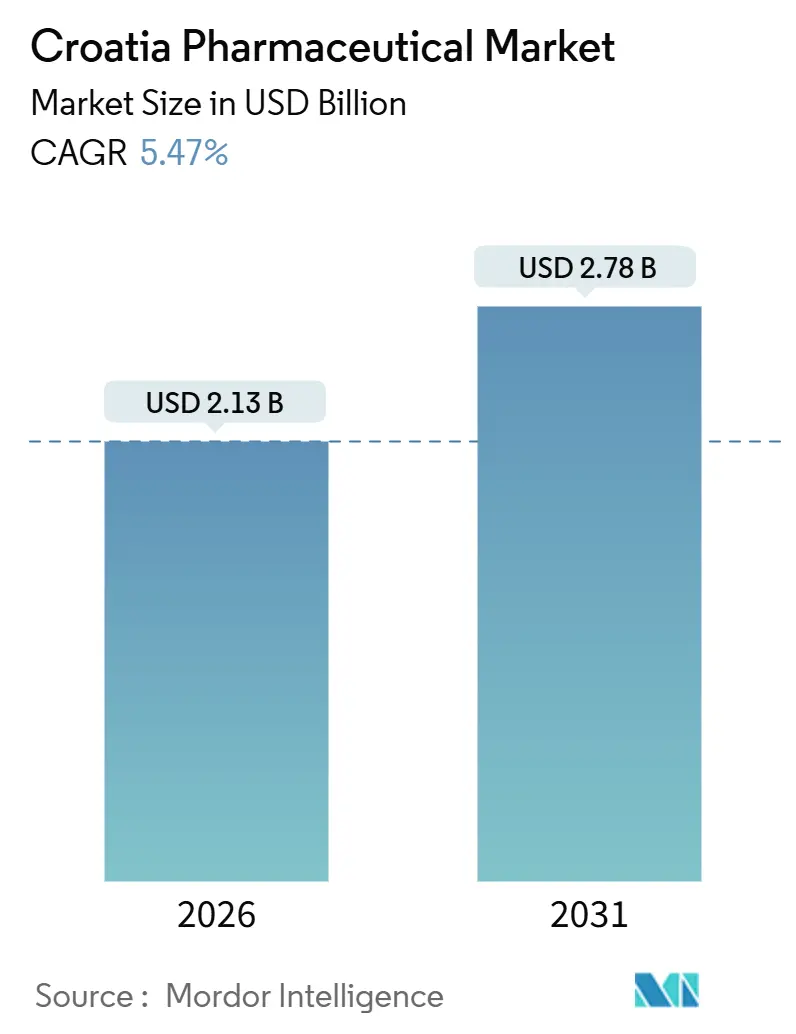

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia Pharmaceutical Market Analysis by Mordor Intelligence

The Croatia Pharmaceutical Market size is estimated at USD 2.13 billion in 2026, and is expected to reach USD 2.78 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031).

The combination of growing public health spending, European Union regulatory alignment, and an entrenched preference for low-cost generics keeps demand resilient even as pricing controls pressure margins. Zagreb, which concentrates one-fifth of the population and most tertiary hospitals, channels a disproportionate share of specialty-drug budgets. At the same time, five additional counties, together accounting for over half of the residents, shape regional access patterns. Hospital tenders deliver double-digit price cuts that help the public payer contain costs, yet they also intensify competition among multinational innovators, regional generic leaders, and niche local manufacturers. Meanwhile, the antimicrobial-resistance crisis amplifies hospital consumption of carbapenems and polymyxins, giving anti-infectives a clear volume tailwind. On the consumer side, the shift toward self-care that began during the COVID-19 pandemic continues to keep pharmacy front-end sales buoyant, despite potential headwinds from the rescheduling of codeine.

Key Report Takeaways

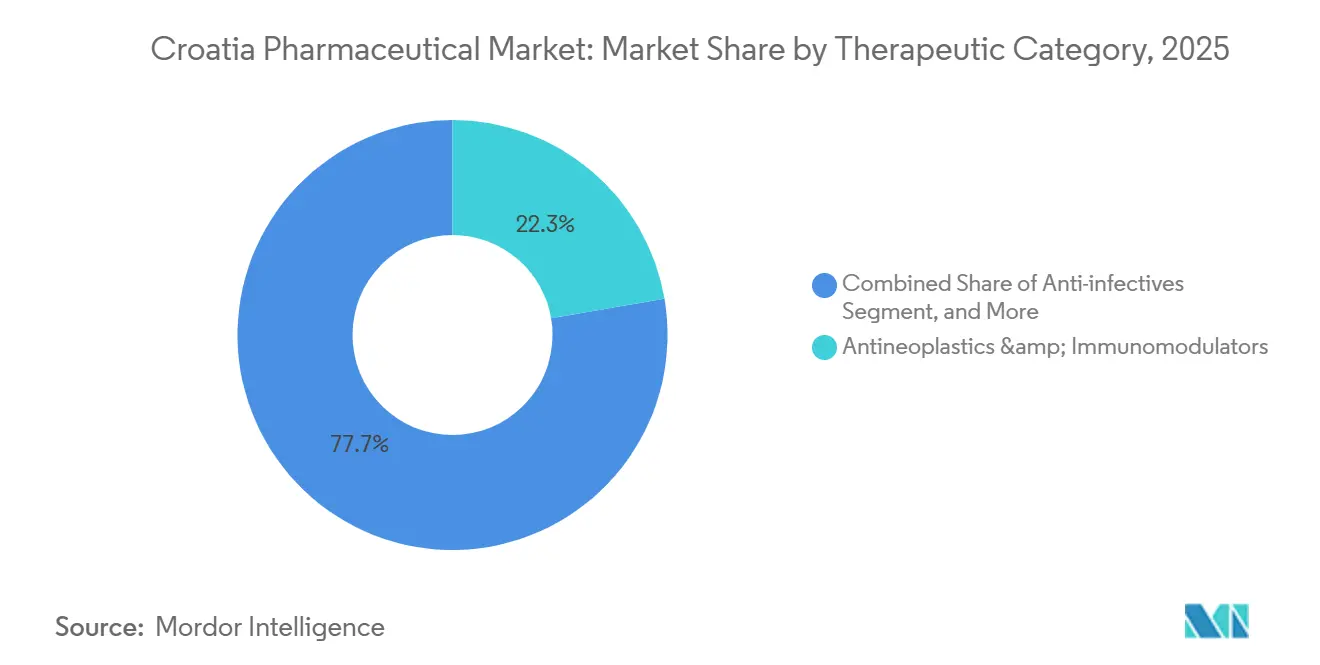

- By therapeutic category, antineoplastics and immunomodulators held 22.31% of Croatia pharmaceutical market share in 2025, while anti-infectives are forecast to grow fastest at an 8.06% CAGR through 2031.

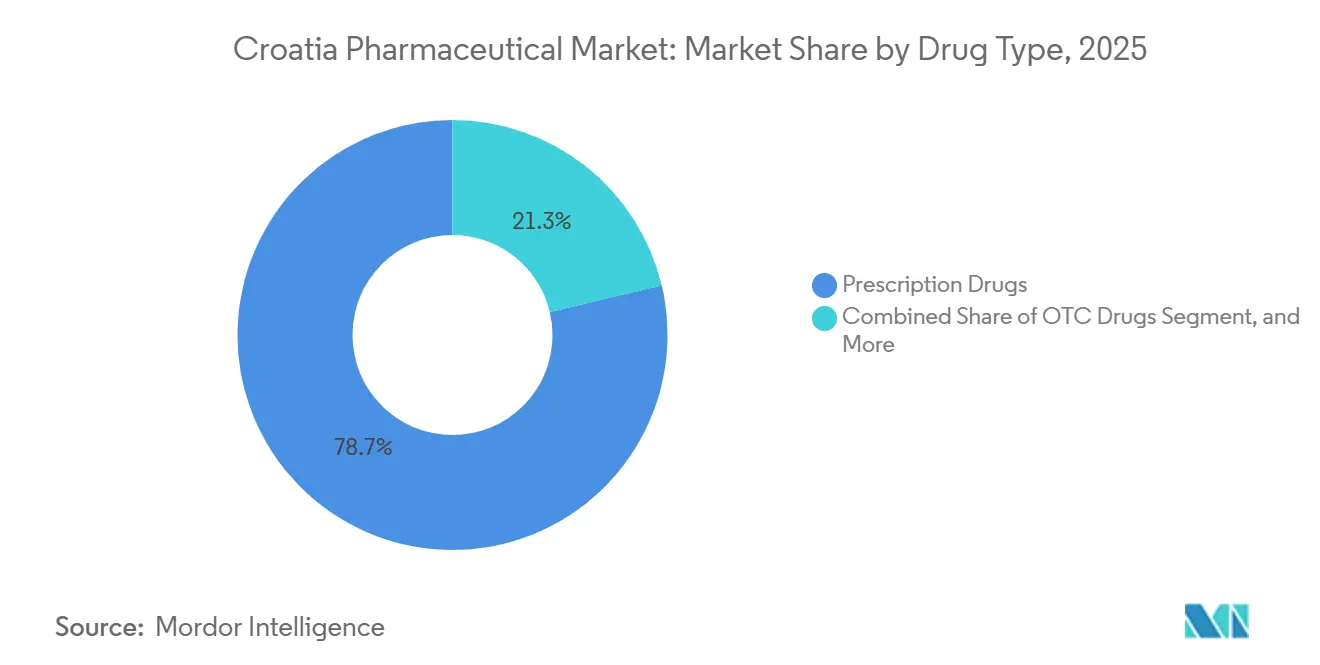

- By drug type, prescription medicines captured 78.73% of the Croatia pharmaceutical market in 2025, whereas over-the-counter products are expected to outpace the total market with a 9.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Croatia Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Healthcare Expenditure | +0.8% | Zagreb and five largest counties | Medium term (2-4 years) |

| Growing Burden of Chronic Diseases | +0.9% | Aging coastal and rural regions | Long term (≥ 4 years) |

| Harmonized EU Regulatory Framework | +0.5% | National | Short term (≤ 2 years) |

| High Generic Penetration Driving Volumes | +0.7% | National | Medium term (2-4 years) |

| CHIF Very Expensive Medicines Fund Expansion | +0.6% | National | Medium term (2-4 years) |

| National Lung-Cancer LDCT Programme & Oncology Database | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare Expenditure

Public sources finance 84.1% of total health expenditures, insulating medicine consumption from fluctuations in household income. HZZO’s three drug budgets, community, hospital, and the costly medicines fund, give planners room to reallocate resources swiftly, even as election cycles introduce political risk. Zagreb’s tertiary centers absorb the bulk of specialty spending, while rural counties still lag in access to oncology and biologics. Since 2015, HZZO’s financial independence has improved budget agility, but also exposed the payer to headline scrutiny when costs spike. The April 2024 registry for expensive medicines now links reimbursement to patient outcomes, a move likely to favor breakthrough therapies with robust real-world data.

Growing Burden of Chronic Diseases

Croatia posted the European Union’s highest crude cancer mortality in 2022 at 346.3 deaths per 100,000.[1]World Bank, “Cost Control-Oriented Provisions in Croatian Pharmaceutical Policy,” worldbank.org Low screening uptake and late presentation drive demand for immuno-oncology agents, which HZZO continues to add to its list, including glofitamab and expanded uses of pembrolizumab. Cardiovascular and metabolic illnesses dominate primary-care prescribing, with 71 million scripts dispensed in 2023. The aging population creates complex polypharmacy scenarios; however, strict prescribing audits prompt physicians to opt for lower-cost generics whenever therapeutic equivalence exists. Real-world registries, rolled out in 2024, are expected to help decision-makers refine reimbursement for high-value therapies for chronic diseases.

Harmonized EU Regulatory Framework

Since joining the EU in 2013, Croatia has aligned its approval processes with those of the EMA, thereby shortening the launch timelines for multinational companies. HALMED’s 2024 update to mirror Regulation 2019/6 enhanced pharmacovigilance and brought veterinary rules in line with human-medicine standards.[2]HALMED, “Regulatory Updates 2024,” halmed.hr The Falsified Medicines Directive and the new HTA Regulation impose compliance costs but standardize quality across member states, easing cross-border distribution. External reference pricing links Croatia to Italy, Slovenia, and the Czech Republic, allowing them to transmit their price cuts locally. Three-year managed-entry agreements mitigate initial budget shocks, but the secrecy surrounding net prices clouds regional benchmarking.

High Generic Penetration Driving Volumes

Generics account for roughly 40% of the market value and more than 70% of prescription volume. First-in generics must list 30% beneath originator prices, with subsequent entrants taking an additional 10% cut, setting off a deflationary spiral. Single-winner hospital tenders slice prices by more than 40% in many classes. Krka’s cardiovascular franchise, featuring Atoris and Roswera, illustrates how regional champions leverage aggressive pricing to secure share. E-prescribing prompts physicians to choose the most cost-effective alternative, and budget caps reinforce adherence, preserving volume growth even as unit values decline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Pricing & Reimbursement Controls | -0.9% | National | Short term (≤ 2 years) |

| Public-Sector Payment Delays | -0.5% | Secondary and tertiary hospitals | Medium term (2-4 years) |

| Potential Upscheduling of OTC Codeine Products | -0.3% | National | Short term (≤ 2 years) |

| Demographic Decline Limiting Long-term Volume Growth | -0.7% | Rural and coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Pricing & Reimbursement Controls

Dual reference pricing and tight internal benchmarking trimmed average pack prices from EUR 7 to EUR 6 within four years of the 2009 reform. Annual recalculations allow only downward movements, while managed-entry contracts stretch discounts further behind closed doors. Hospital tender savings exceeded 40% for many generic lines but sometimes left single suppliers, risking shortages. Confidential net prices obscure accurate market signals, and repeated deflation discourages companies from launching marginal innovations.

Public-Sector Payment Delays

Hospitals owed suppliers EUR 235 million as of September 2024, with some invoices stretching past 180 days. Government bailouts offer episodic relief yet do not fix structural underfunding. Smaller manufacturers tighten their credit or abandon low-margin lines, consolidating supply among well-capitalized multinational companies. The 2024 registry now tracks invoice status, but enforcement gaps remain, perpetuating working-capital strain across the distribution chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Category: Oncology Leads, Infections Surge

Antineoplastics and immunomodulators controlled 22.31% of the Croatia pharmaceutical market in 2025, underscoring the system’s commitment to cancer care despite per-capita oncology outlays of only EUR 130 PPP in 2023. Croatia reimburses a greater portion of new oncology actives than several larger Central European peers. The February 2025 list update added glofitamab and broadened coverage for pembrolizumab and nivolumab. Anti-infectives, driven by soaring resistance rates, are projected to grow at an 8.06% CAGR through 2031, the fastest among all categories. Hospital antibacterial use continues to rise, with the consumption of carbapenems and polymyxins increasing sharply since 2013.

Cardiovascular drugs dominate prescriptions but, given more than 70% generic penetration, deliver limited value growth. Krka’s atorvastatin and rosuvastatin lines exemplify regional dominance in these mature classes. Gastrointestinal and respiratory medicines benefit from self-medication and an aging, smoking-exposed population, yet intense generic competition restrains pricing. Dermatology remains a niche stronghold for local players, such as Belupo, supported by a modern factory in Koprivnica that has increased topical-cream output by 1.5 times.

By Drug Type: Rx Dominance, OTC Momentum

Prescription products captured 78.73% of spending in 2025, reflecting the payer’s tight grip on chronic-disease therapies. Internal referencing forces the first Croatia pharmaceutical market size discount to 30% below the originator, and subsequent entries deepen that cut, keeping generic prices among the lowest in the EU. Hospitals amplify the effect by using single-winner tenders, which deliver 44.7% savings on many interchangeable drugs.

Over-the-counter lines are projected to grow at a rate of 9.72% annually, driven by consumers who prefer pharmacy access for minor ailments and supplements. Pharmacy front-end revenue reached EUR 1.2 billion in 2023, representing an 8% year-over-year increase. Vitamins, dermatological topicals, and cough-and-cold remedies underpin momentum, and digital health platforms now pair teleconsultations with OTC recommendations. However, any move to prescription-only codeine would erase a high-margin subcategory almost overnight. Belupo’s broad OTC range positions it to defend share, while international brands may need to adjust marketing once stricter scheduling takes hold.

Geography Analysis

Croatia’s health-spending footprint is highly centralized. Zagreb accounts for 20% of residents yet absorbs an even larger slice of hospital and specialty-drug budgets thanks to four university hospitals and a dense network of tertiary centers. These facilities anchor most managed-entry agreements, allowing swift introduction of biologics and advanced oncology regimens. In contrast, coastal counties, popular with tourists but home to aging local populations, struggle with limited specialist coverage, leading to referral bottlenecks for oncology, rheumatology, and endocrinology services.

Generic substitution rates run higher in these regions because e-prescribing and budget controls are rigorously enforced. The Croatia pharmaceutical market size for smaller inland counties remains modest, yet suppliers target them with mobile pharmacy programs and telemedicine to offset physician shortages. Hospital payment delays are most acute outside Zagreb, where secondary hospitals rely heavily on central bailouts.

Islands and sparsely populated rural districts face persistent access challenges. Community pharmacies there handle both prescription and OTC demand, and they depend on wholesalers’ willingness to extend credit amid delayed reimbursements. Aging demographics amplify chronic-disease prevalence but do not fully translate into higher volumes because absolute population is contracting. Regional public-health authorities are piloting home-delivery of medicines for immobile seniors, a model that, if scaled, may slightly expand Croatia pharmaceutical market penetration into underserved areas.

Competitive Landscape

The Croatia pharmaceutical market features a mid-tier concentration level: multinationals dominate patented oncology and immunology niches, while regional generic firms and local manufacturers control volume-driven primary-care segments. Confidential managed-entry agreements make list prices poor indicators of actual market share, but Krka, Pliva (Teva), and Zentiva collectively supply a significant portion of high-volume generics. Innovators such as Roche, Pfizer, and Novartis leverage global trial data to negotiate early listings, often tied to budget caps and outcome clauses.

Manufacturing investment underscores strategic intent. Pfizer and Swedish Orphan Biovitrum inaugurated a EUR 100 million biotech plant near Zagreb in 2024, which is expected to reach full commercial output by 2026, thereby expanding the regional supply of monoclonal antibodies and biosimilars. Pliva added 2 billion tablets of annual capacity at its new USD 100 million facility in Zagreb in 2025, positioning itself for exports to the United States once FDA clearance is obtained. JGL’s INTEGRA project boosted sterile output by 60% and expanded R&D labs, enhancing its standing in hospital injectables.

Competitive tactics hinge on pricing finesse and tender agility. Regional firms excel at undercutting larger rivals in single-winner hospital tenders, while multinationals trade discounts for volume commitments within MEAs. Biosimilars now enter tenders alongside reference products, resetting price anchors in oncology and rheumatology. Digital health startups aim to connect physicians, payers, and patients; however, reimbursement hurdles hinder rapid adoption. Overall, the Croatia pharmaceutical industry remains fiercely price-sensitive, rewarding manufacturers that balance cost leadership with reliable supply.

Croatia Pharmaceutical Industry Leaders

Johnson & Johnson

Pfizer Inc.

Bayer AG

Merck & Co., Inc.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Biofrontera Pharma GmbH, the principal commercial subsidiary of Biofrontera AG, has entered into a promotion and distribution agreement with Croatian pharmaceutical company Propharma d.o.o. to commercialise its dermatological prescription product Ameluz in Croatia. Under the agreement, Propharma will take responsibility for promoting and distributing Ameluz within the Croatian market.

- October 2024: ACG, a leading integrated provider of oral dosage solutions, has announced a major expansion of its operations in Europe with significant upgrades to its Croatian facilities. The initiative includes a substantial increase in production capacity at ACG Capsules’ Croatian site, alongside the establishment of new warehousing and slitting facilities by the ACG Packaging Materials division.

- May 2024: Alkaloid AD Skopje initiated a project worth EUR 19.4 million (USD 20.82 million) to construct solid pharmaceutical form manufacturing facilities covering an area of 6,200 square meters. This marked the company's most significant investment in the past two decades.

Croatia Pharmaceutical Market Report Scope

As per the scope of this report, pharmaceuticals are referred to as prescribed and non-prescription drugs. These medicines can be bought by an individual with or without a doctor's prescription and are consumed to treat various diseases. The report also covers the in-depth analysis of qualitative and quantitative data.

The Croatian pharmaceutical market is segmented by therapeutic category and drug type. By therapeutic category, the market is segmented into anti-infectives, cardiovascular, gastrointestinal, anti-diabetic, respiratory, dermatological, musculoskeletal system, nervous system, and other therapeutic categories. By drug type, the market is segmented into prescription drugs and OTC drugs. By prescription drugs, the market is segmented into branded drugs and generic drugs. For each segment, the market size and forecast are provided in terms of value (USD).

| Anti-infectives |

| Cardiovascular |

| Gastro-intestinal |

| Anti-diabetic |

| Respiratory |

| Dermatological |

| Musculoskeletal System |

| Nervous System |

| Antineoplastics & Immunomodulators |

| Other Therapeutic Categories |

| Prescription Drugs | Branded |

| Generic | |

| OTC Drugs |

| By Therapeutic Category | Anti-infectives | |

| Cardiovascular | ||

| Gastro-intestinal | ||

| Anti-diabetic | ||

| Respiratory | ||

| Dermatological | ||

| Musculoskeletal System | ||

| Nervous System | ||

| Antineoplastics & Immunomodulators | ||

| Other Therapeutic Categories | ||

| By Drug Type | Prescription Drugs | Branded |

| Generic | ||

| OTC Drugs | ||

Key Questions Answered in the Report

How large is the Croatia pharmaceutical market today?

The Croatia pharmaceutical market size is USD 2.13 billion in 2026 and is forecast to reach USD 2.78 billion by 2031 at a 5.47% CAGR.

Which therapy area dominates Croatian drug spending?

Oncology leads with 22.31% of total spending in 2025, followed by cardiovascular medicines that top prescription volumes.

What is driving the fastest growth segment?

Anti-infectives are projected to expand at an 8.06% CAGR through 2031 due to escalating antimicrobial resistance and increased hospital use of reserve antibiotics.

Why are over-the-counter medicines growing faster than prescriptions?

Self-medication trends and convenience have driven OTC sales to EUR 1.2 billion in 2023, and they are forecast to grow at a rate of 9.72% annually, despite potential codeine restrictions.

How do pricing controls affect new drug launches?

Dual reference pricing and aggressive internal benchmarking force substantial price cuts, which can delay or discourage launches until confidential managed-entry agreements offset margin loss.

Page last updated on: