Enzyme-Linked Immunosorbent Assay (ELISA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

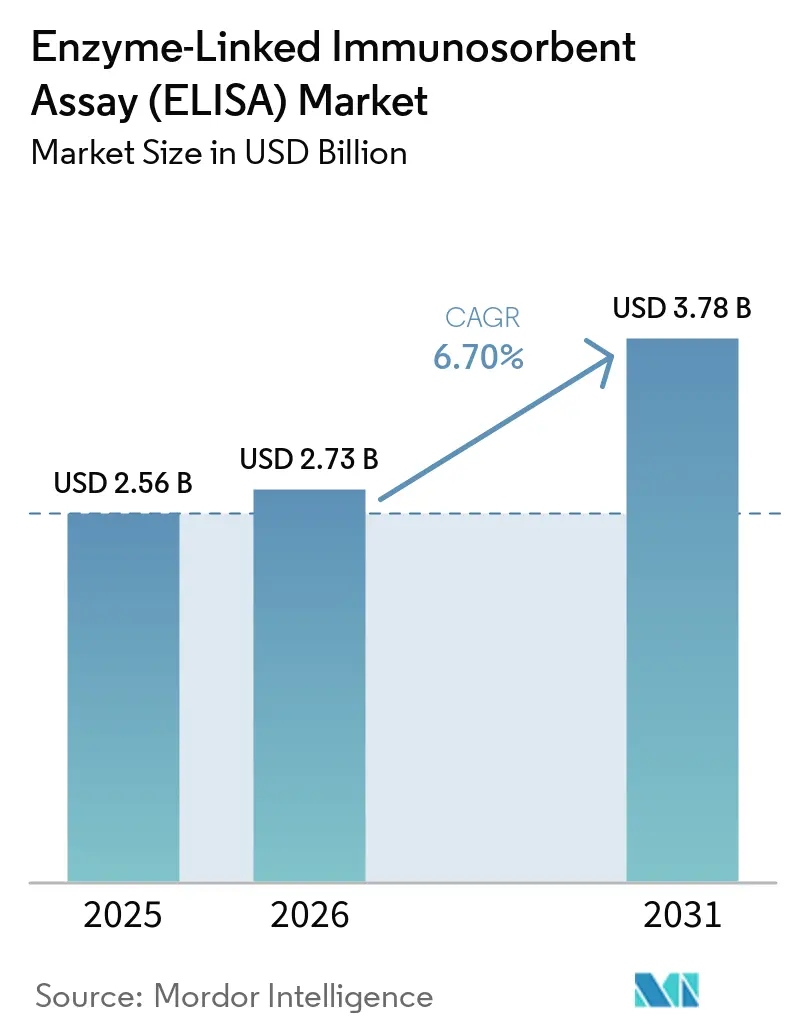

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 3.78 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enzyme-Linked Immunosorbent Assay (ELISA) Market Analysis by Mordor Intelligence

The Enzyme-Linked Immunosorbent Assay (ELISA) Market size was valued at USD 2.56 billion in 2025 and is estimated to grow from USD 2.73 billion in 2026 to reach USD 3.78 billion by 2031, at a CAGR of 6.70% during the forecast period (2026-2031). Rapid automation, widening chronic-disease screening programs, and steady adoption of ELISA in drug‐development workflows underpin this trajectory, even as next-generation immunoassay formats intensify competitive pressure. High-throughput workstations are easing sample-volume bottlenecks, while the expansion of companion diagnostics in immuno-oncology raises assay specialization and average selling prices. North America retains a dominant market share on the back of mature reimbursement systems and streamlined FDA pathways. Asia-Pacific offers the fastest revenue runway, propelled by government-backed diagnostic infrastructure upgrades and the rising burden of non-communicable diseases. Sustainability mandates, particularly in Europe, are starting to reshape consumable design, nudging vendors toward recyclable microplates and reduced plastic content.

Key Report Takeaways

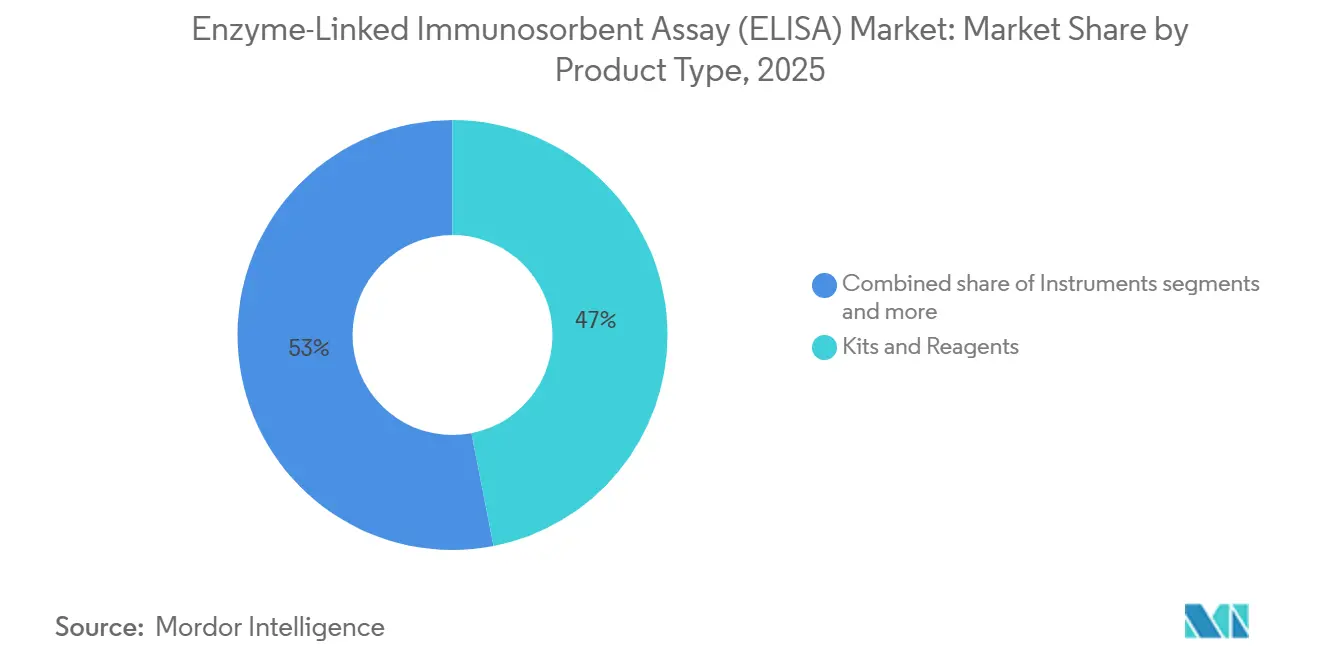

- By product type, kits & reagents held 46.95% of the Enzyme-Linked Immunosorbent Assay (ELISA) market share in 2025, whereas instruments are projected to expand at a 7.05% CAGR to 2031.

- By assay technique, sandwich ELISA led with 35.65% of the Enzyme-Linked Immunosorbent Assay (ELISA) market share in 2025; competitive ELISA registers the fastest 7.28% CAGR through 2031.

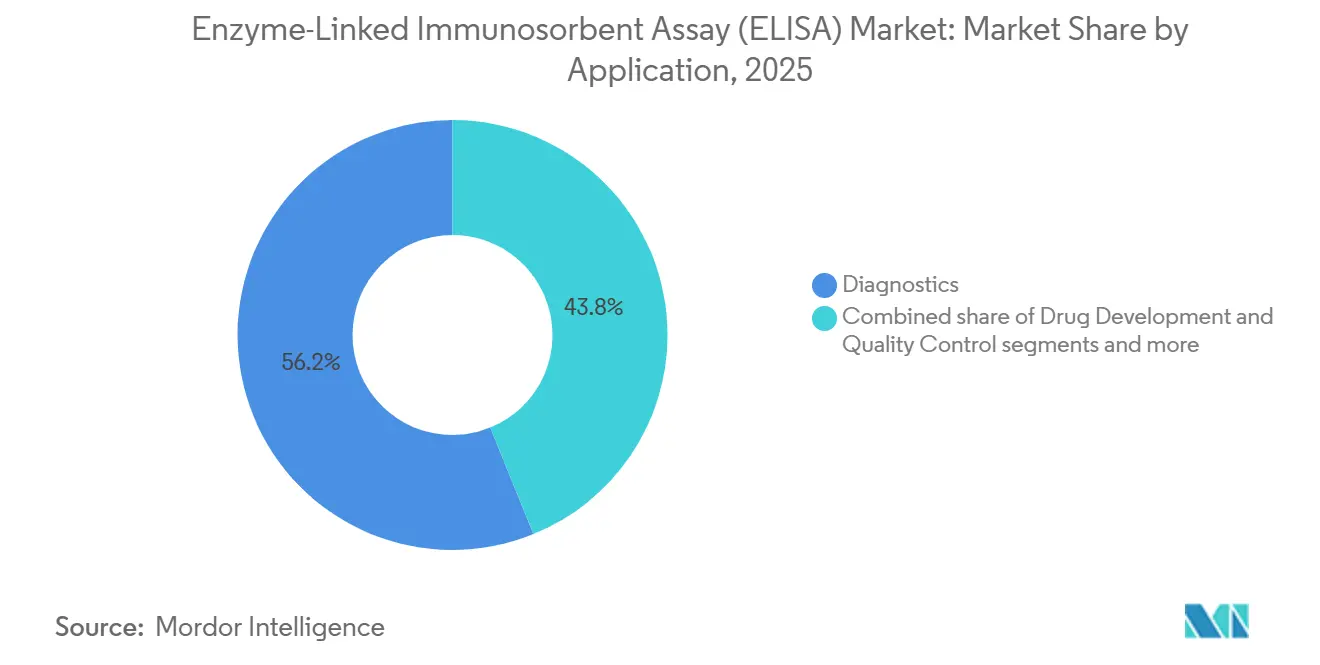

- By application, diagnostics commanded 56.15% of the Enzyme-Linked Immunosorbent Assay (ELISA) market size in 2025, while drug development & quality control is forecast to rise at a 7.55% CAGR.

- By end user, diagnostic laboratories retained 30.05% of the Enzyme-Linked Immunosorbent Assay (ELISA) market share in 2025; pharmaceutical & biotechnology companies are advancing at a 7.82% CAGR to 2031.

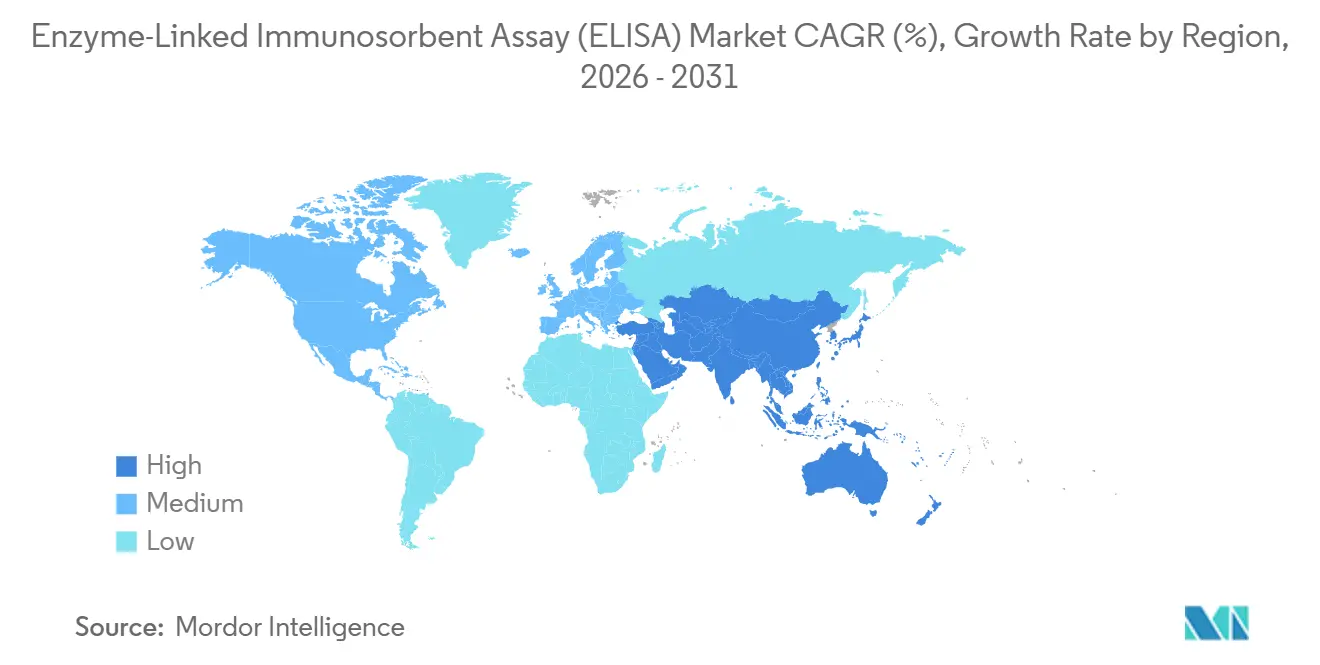

- By geography, North America dominated with 41.85% of the Enzyme-Linked Immunosorbent Assay (ELISA) market share in 2025; Asia-Pacific is poised to post an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enzyme-Linked Immunosorbent Assay (ELISA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic & infectious diseases | 1.2% | Global, with higher impact in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Rapid penetration of high-throughput automated ELISA workstations | 0.8% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Rising demand for companion diagnostics in immuno-oncology | 0.6% | North America & Europe, selective APAC markets | Medium term (2-4 years) |

| Multiplex ELISA panels for immunotherapy monitoring | 0.4% | Global, concentrated in advanced healthcare systems | Long term (≥ 4 years) |

| Cost-efficient recombinant/plant-derived antibodies for ELISA kits | 0.3% | Global, with manufacturing advantages in APAC | Long term (≥ 4 years) |

| Decentralised POC ELISA-on-chip formats for rural settings | 0.2% | Emerging markets, rural healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of chronic & infectious diseases

Rising incidences of diabetes, cardiovascular disorders, and persistent viral infections are pushing healthcare providers to embed ELISA into routine population-health programs. National screening agendas in India and China are scaling up biomarker testing volume, with ELISA favored for its validated protocols and low per-test cost, especially when budgets constrain the uptake of newer chemiluminescent systems. Hospital networks in the Middle East are integrating ELISA panels for hepatitis and HIV monitoring within universal-testing rollouts, lifting reagent consumption. Multilateral donors are also financing ELISA-based tuberculosis surveillance in sub-Saharan Africa, enlarging the installed base. The combined effect is a stable sample-volume pipeline that cushions market revenue against cyclical R&D spending patterns.

High-throughput automated ELISA workstations

Automation addresses the chronic shortage of qualified technicians and reduces error rates linked to manual pipetting. Leading platforms now process up to 960 wells per hour with integrated barcode tracking and AI-led result validation, cutting turnaround time by more than 30% for large reference labs. Cost-benefit analyses in US hospital chains show a two-year payback when daily test load exceeds 1,500 samples. European laboratories are layering middleware that feeds results directly into electronic medical records, improving clinical decision efficiency. Asian contract research organizations are adopting lease models that bundle instrumentation, software, and reagents, lowering upfront capital barriers and accelerating penetration.

Companion diagnostics demand in immuno-oncology

Pharmaceutical pipelines list more than 1,200 active immunotherapy candidates, each requiring validated companion diagnostics. ELISA, with its straightforward regulatory path and established precision, is being selected to quantify PD-L1, CTLA-4, and other immune checkpoints in early-phase trials. As label expansions reach commercial stages, assay volumes grow in parallel with patient stratification protocols, lifting high-margin kit sales. Strategic alliances—such as Abbott’s agreements with mid-cap biotech developers—streamline co-development timelines, while FDA breakthroughs shorten review cycles for integrated drug-test submissions. This synergy secures a durable revenue stream that offsets commoditization pressures in general infectious-disease testing.

Multiplex ELISA panels for immunotherapy monitoring

Oncology centers increasingly demand multiplexed cytokine and chemokine profiling to capture treatment-response dynamics in real time. Multiplex ELISA reduces sample draw by 80% compared with sequential single-analyte tests, an important consideration for frail patients. Technological advances in antibody engineering suppress cross-reactivity, boosting specificity metrics to parity with bead-array systems. Early adopters report 25% lower consumable cost per actionable data point. Pharmaceutical firms are incorporating multiplex panels into adaptive-trial designs to refine dose titration, reinforcing the platform’s clinical relevance and widening its total addressable market.

Restraint Imoact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-reactivity & false-positive concerns | -0.7% | Global, particularly in complex diagnostic applications | Short term (≤ 2 years) |

| Growing adoption of next-gen multiplex bead & CLIA platforms | -0.5% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Sustainability pressure on single-use micro-plates & plastics | -0.3% | Europe & North America, spreading globally | Long term (≥ 4 years) |

| Shortage of skilled immunoassay technicians in emerging markets | -0.2% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cross-reactivity & false positives

Overlap in epitope binding can trigger misleading results, especially when analyte concentration is low or sample matrices are heterogeneous. Clinical laboratories now mandate confirmatory testing for critical biomarkers, adding process steps that inflate operating costs. Regulators responded with tighter validation guidance in 2024, raising the bar for commercial kit launch approvals. Manufacturers counter with high-affinity recombinant antibody pairs and refined blocking buffers, yet performance variability persists among lower-priced kits, complicating procurement decisions for price-sensitive hospitals. The resultant skepticism nudges some institutions toward chemiluminescent formats with broader dynamic range.

Shift to multiplex bead & CLIA platforms

Next-generation bead arrays can quantify up to 50 analytes from 25 μL of sample, attractive to oncology centers where tissue is limited. CLIA systems deliver picogram-level sensitivity, widening diagnostic windows for early disease detection. Major IVD players allocated more than USD 2 billion to CLIA expansion during 2024-25, accelerating catalog breadth. High initial capital outlay and proprietary reagent lock-in deter full migration, yet reference labs with heavy sample volumes find the throughput gains compelling. ELISA vendors face margin pressure as premium accounts diversify assay platforms, prompting investment in hybrid systems that integrate chemiluminescent detection into existing ELISA footprints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instruments gain tempo while consumables retain scale

Kits & reagents generated 46.95% of the ELISA market in 2025, powered by their recurring-revenue profile and broad menu coverage. Instruments, although representing a smaller installed-base value, are forecast to outpace consumables at a 7.05% CAGR as laboratories pursue automation. The ELISA market size for high-capacity analyzers is expected to reach USD 1.69 billion by 2031, reflecting bundled software and service contracts that lift average selling prices. Vendors now embed cloud analytics for remote calibration and predictive maintenance, shrinking downtime to enhance lab productivity.

Large hospital networks pursue multi-plate robotics that unify microplate washing, incubation, and optical detection, trimming technician hours by up to 40%. Subscription models offer predictable cash flow for suppliers and smoother capital budgeting for customers. Emerging Asian labs, where capital budgets remain constrained, are adopting staged-upgrade pathways: entry-level semi-automated readers today, scalable to full robotics upon volume escalation. Reagent manufacturers collaborate with instrument partners to pre-validate kit compatibility, ensuring plug-and-play deployment and shortening verification cycles.

By Assay Technique: Competitive ELISA climbs niche peaks

Sandwich assays still anchor 35.65% of 2025 revenue, preferred for large protein detection owing to dual-antibody specificity. Competitive ELISA, however, expands at 7.28% CAGR as pharmaceutical clients require low-molecular-weight drug quantification during pharmacokinetic studies. Direct ELISA finds traction in rapid toxin screens, while indirect formats remain standard for serological surveillance of emerging pathogens.

Technique selection increasingly hinges on regulatory precedent. Competitive formats enjoy entrenched FDA-cleared protocols for therapeutic drug monitoring, smoothing submission dossiers for new generics. Academic research groups appreciate the technique’s tolerance for small antigen targets, fueling catalog diversification among mid-tier kit suppliers. Detection chemistries also evolve: colorimetric substrates give way to amplified fluorescence, extending detection limits and pulling ELISA closer to CLIA performance without overhaul of legacy plate readers.

By Application: Drug development eclipses traditional diagnostics growth

Diagnostics delivered 56.15% of 2025 sales, yet drug development & quality control is advancing at a 7.55% CAGR thanks to the biologics pipeline and biosimilar comparability requirements. Contract research organizations (CROs) absorb a rising share of this demand, bundling method development, validation, and large-scale sample analysis.

In diagnostics, infectious-disease panels remain volume leaders, while oncology and autoimmune markers carry premium pricing. Food allergen monitoring adopts ELISA to ensure compliance with stricter labeling laws in Europe and North America. Rare-disease laboratories deploy laboratory-developed ELISA tests where commercial kits are unavailable, leveraging validated platforms to navigate the FDA’s evolving LDT framework. Hormone fertility testing continues steady demand in reproductive health clinics, benefiting from ELISA’s recognized reliability.

By End User: Pharma-biotech segments scale fastest

Diagnostic laboratories controlled 30.05% of 2025 revenues, but pharmaceutical & biotechnology entities will post the sector‘s fastest 7.82% CAGR, reflecting escalating biomarker validation and lot-release testing. Companies invest in in-house bioanalytical labs to streamline regulatory submissions and safeguard proprietary data.

Hospitals remain pivotal for routine screening, yet budget ceilings curb capex growth; their focus pivots to integrated analysers that slash reagent waste. Academic institutes contribute consistent baseline demand for exploratory research, often funded by public grants prioritizing infectious-disease preparedness. CROs consolidate regional facilities, using scale to negotiate volume discounts on reagents and lock instrument leases at favorable rates, reinforcing barriers to smaller entrants.

Geography Analysis

North America generated 41.85% of 2025 revenue and retains leadership through 2031, supported by elevated per-capita healthcare spending and the concentration of top IVD manufacturers. Clinical laboratories readily adopt next-generation instruments, and payors reimburse specialized assays, sustaining premium pricing. Government initiatives to fortify pandemic readiness cement ELISA as a backbone technology within national stockpiles.

Asia-Pacific advances at an 8.12% CAGR, the highest regional pace. China’s “Healthy China 2030” blueprint funds hospital immunology labs in secondary cities, lifting capital equipment imports. India’s Ayushman Bharat scheme broadens insurance coverage, unlocking rural diagnostic demand met by decentralized ELISA-on-chip devices distributed via primary health centers. Japan and South Korea emphasize automation upgrades, leveraging domestic robotics expertise to raise throughput while offsetting technician shortages; Australia maintains stable demand through public-private pathology partnerships that prioritize assay standardization.

Europe demonstrates balanced growth under the new IVDR that requires higher clinical-evidence thresholds. Germany’s manufacturing prowess secures supply chain resilience for regional kit production. The United Kingdom channels Life Sciences Vision funding into oncology biomarker research, inflating competitive ELISA kit usage. Southern European nations roll out EU-supported modernization grants, updating public hospital labs with automated workstations. South America and Middle East & Africa contribute incremental gains as economic headwinds stabilize; multinational NGOs deploy ELISA for surveillance of vector-borne diseases, expanding the installed base that vendors can later monetize with consumables.

Competitive Landscape

The ELISA market shows moderate consolidation. Thermo Fisher Scientific broadened its proteomics reach by acquiring Olink for USD 3.1 billion in 2024, integrating proximity extension assays that complement ELISA for orthogonal validation. Danaher’s subsidiary Beckman Coulter rolled out compliance toolkits aligned with 2024 CLIA updates, bolstering its service moat. Roche continues to invest in AI-assisted plate-reader software that flags outliers automatically, enhancing reproducibility for high-value oncology panels.

Horizontal mergers feature prominently. Bruker purchased ELITechGroup for USD 942 million, securing a foothold in specialty infectious-disease ELISA kits and leveraging its own mass-spec installed base for cross-selling. Tecan’s acquisition of Cisbio ELISA assets enriched its neuroendocrine portfolio, indicating appetite for niche biomarkers that hospitals cannot source from mainstream vendors. bioMérieux bought SpinChip Diagnostics to add ten-minute point-of-care capabilities, signalling that rapid, decentralized formats are strategic growth levers.

Disruptors differentiate through materials science. Creative Diagnostics invests in plant-based antibody libraries, promising cost cuts that can defend margin when volume contracts. Start-ups deploy microfluidic ELISA-on-a-cartridge paradigms, trimming reagent volume by 90% and aligning with green-laboratory directives in Europe. Meanwhile, major players intensify sustainability roadmaps, prototyping compostable wells and closed-loop recycling schemes to pre-empt upcoming eco-label regulations. The competitive environment thus balances scale advantages with innovation niches, sustaining healthy price discipline.

Enzyme-Linked Immunosorbent Assay (ELISA) Industry Leaders

Thermo Fisher Scientific

Bio-Rad Laboratories, Inc

Agilient Technologies, Inc

Merck KGaA

Promega Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina completed its USD 425 million acquisition of SomaLogic to expand proteomics coverage for biomarker discovery

- May 2025: Abbott introduced the i-STAT TBI rapid blood test for on-site concussion evaluation in sports settings

- April 2025: Tecan Group acquired ELISA kit assets from Cisbio Bioassays to reinforce specialty diagnostics in neuroendocrine tumors

Global Enzyme-Linked Immunosorbent Assay (ELISA) Market Report Scope

As per the scope of this report, the Enzyme-Linked Immunosorbent Assay (ELISA) is a commonly used solid-phase type enzyme immunoassay to detect the presence of a ligand in a liquid sample using antibodies directed against the protein to be measured. The market is segmented by product (direct ELISA, indirect ELISA, sandwich ELISA, and competitive ELISA), application (disease diagnosis, vaccine development, and other applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in ( in USD million) for the above segments.

| Kits & Reagents |

| Instruments |

| Software & Services |

| Sandwich ELISA |

| Direct ELISA |

| Indirect ELISA |

| Competitive ELISA |

| Diagnostics | Infectious Diseases |

| Cancer | |

| Auto-immune Diseases | |

| Hormone & Fertility | |

| Food Allergy | |

| Drug Development & Quality Control | |

| Research Use |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organisations |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Kits & Reagents | |

| Instruments | ||

| Software & Services | ||

| By Assay Technique (Value) | Sandwich ELISA | |

| Direct ELISA | ||

| Indirect ELISA | ||

| Competitive ELISA | ||

| By Application (Value) | Diagnostics | Infectious Diseases |

| Cancer | ||

| Auto-immune Diseases | ||

| Hormone & Fertility | ||

| Food Allergy | ||

| Drug Development & Quality Control | ||

| Research Use | ||

| By End User (Value) | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Pharmaceutical & Biotechnology Companies | ||

| Contract Research Organisations | ||

| Academic & Research Institutes | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the ELISA market?

The ELISA market size is USD 2.73 billion in 2026 and is projected to reach USD 3.78 billion by 2031

Which region is growing fastest in the ELISA market?

Asia-Pacific is the fastest-growing region, registering an 8.12% CAGR through 2031.

Which product segment is expanding most rapidly?

ELISA instruments lead growth at a 7.05% CAGR as laboratories prioritize automation upgrades.

How are pharmaceutical companies influencing ELISA demand?

Pharma-biotech firms are increasing ELISA use for biomarker validation and immunogenicity testing, driving a 7.82% CAGR in this end-user segment.

Page last updated on: