Biological Sample Collection Kits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

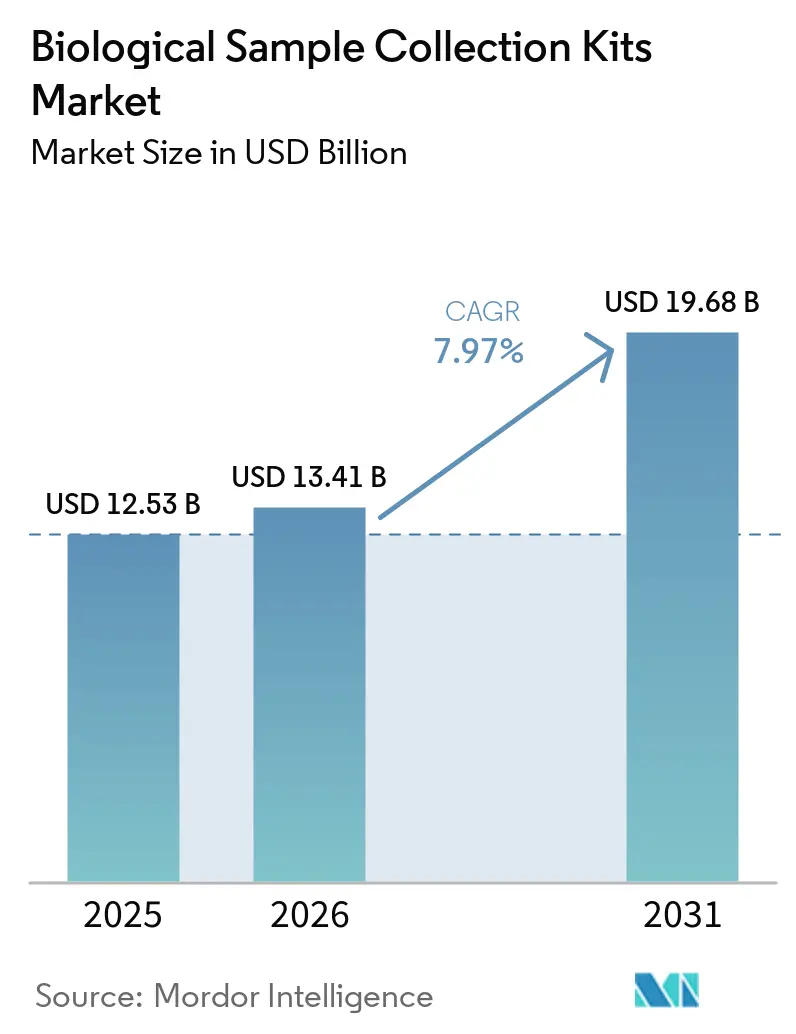

| Market Size (2026) | USD 13.41 Billion |

| Market Size (2031) | USD 19.68 Billion |

| Growth Rate (2026 - 2031) | 7.97% CAGR |

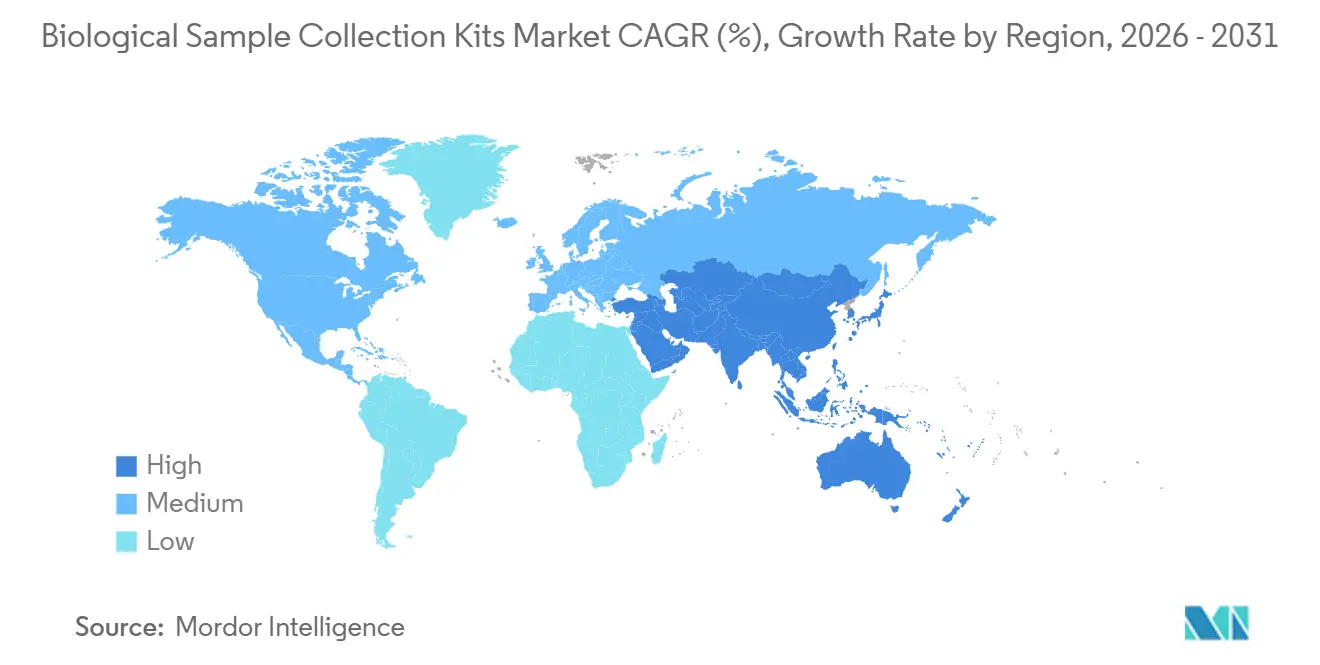

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

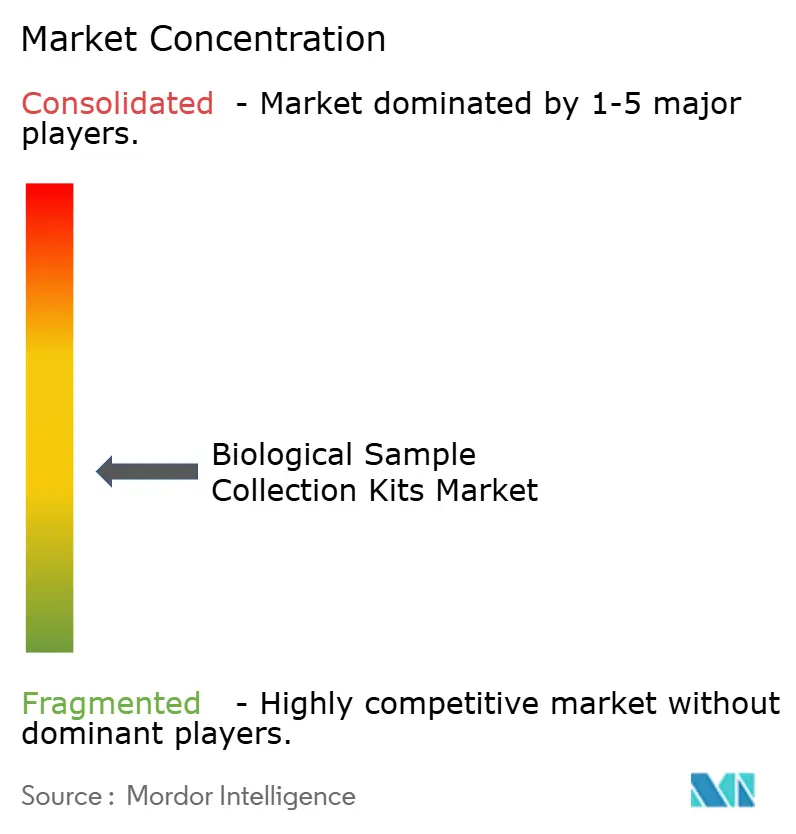

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biological Sample Collection Kits Market Analysis by Mordor Intelligence

The Biological Sample Collection Kits Market size is projected to expand from USD 12.53 billion in 2025 and USD 13.41 billion in 2026 to USD 19.68 billion by 2031, registering a CAGR of 7.97% between 2026 to 2031.

An ongoing blend of infectious-disease surveillance, decentralized clinical research, and at-home diagnostics is keeping volumes high even as inventory cycles settle. Blood-collection formats with closed-system safety features are gaining market share because laboratories want to reduce hemolysis, prevent needlestick injuries, and comply with the OSHA Bloodborne Pathogens Standard [1]Occupational Safety and Health Administration, “Bloodborne Pathogens Standard,” osha.gov. Diagnostics applications dominate demand thanks to widespread respiratory and STI testing, while genetic screening and liquid biopsy programs are adding incremental kit volumes. Regulatory clarity around decentralized trials in the United States and Europe is opening fresh opportunities for self-collection devices, and ambient-stable chemistries that remove frozen-shipment costs are tilting purchasing criteria toward total cost of ownership.

Key Report Takeaways

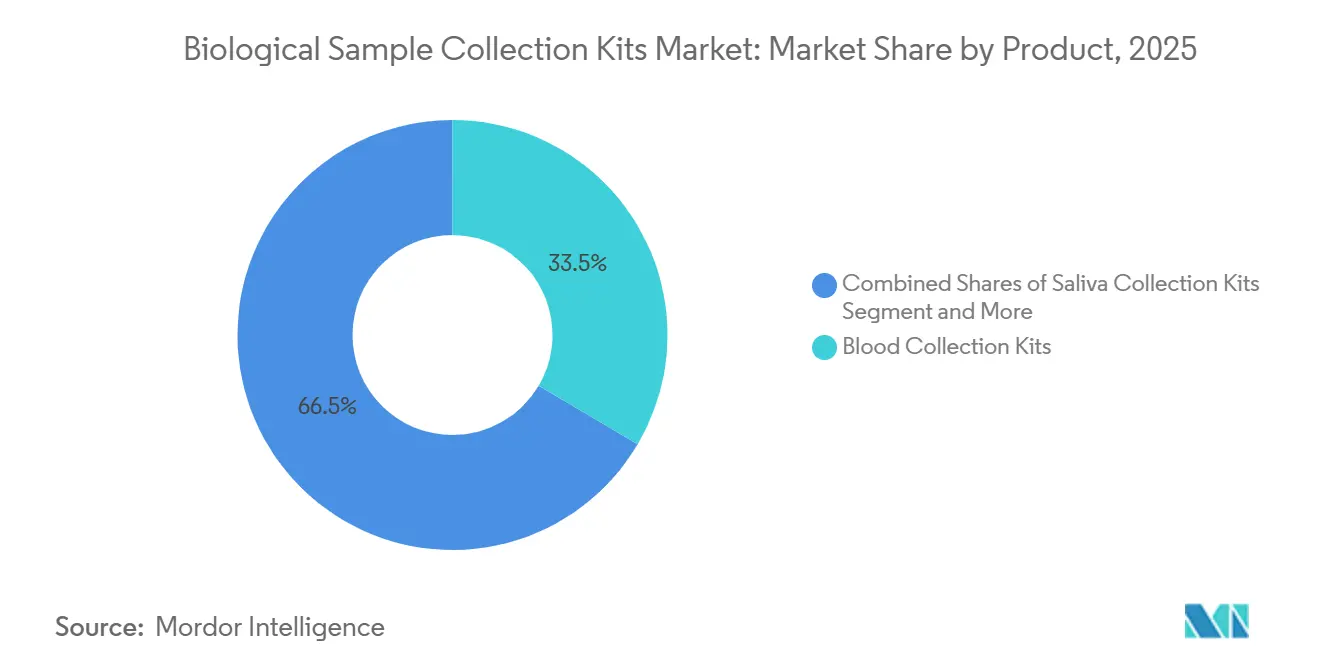

- By product, blood-collection kits led with 33.48% of the biological sample collection kits market share in 2025 and are projected to advance at an 8.34% CAGR through 2031.

- By application, diagnostics accounted for 45.84% of revenue in 2025 and is expanding at a 8.12% CAGR through 2031.

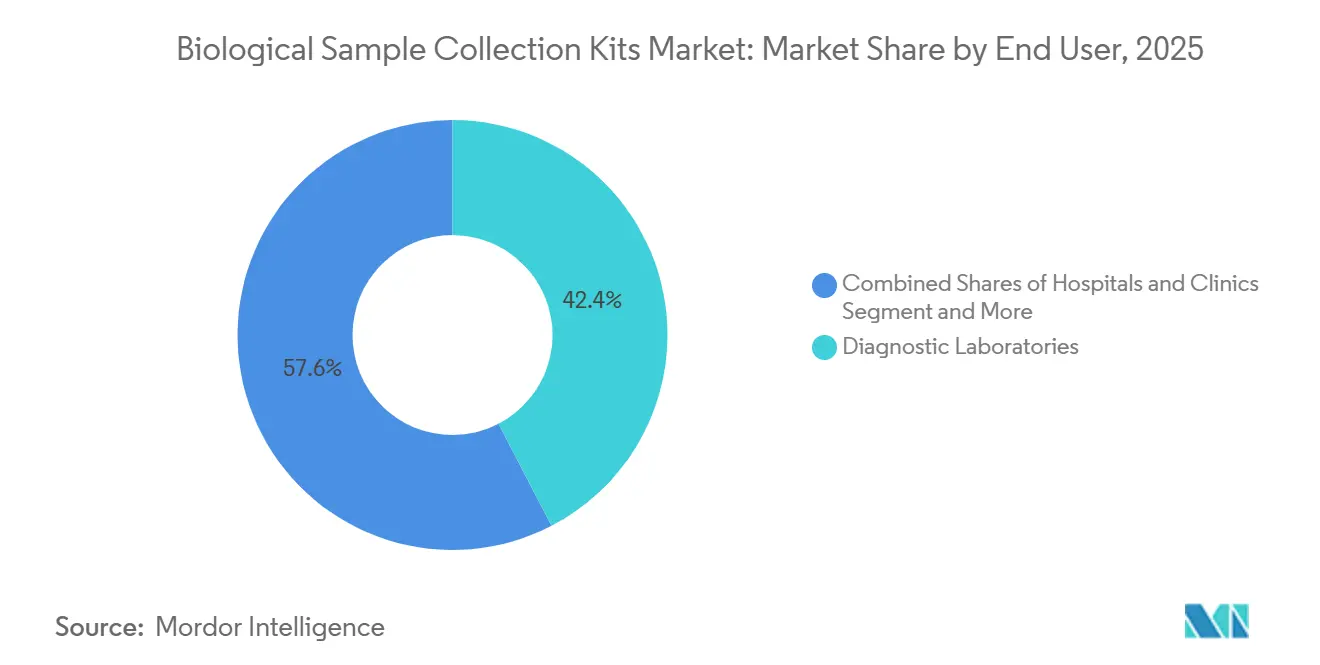

- By end user, diagnostic laboratories accounted for 42.38% of revenue in 2025, and the segment is progressing at an 8.53% CAGR over the same period.

- By geography, North America accounted for 44.25% of revenue in 2025; Asia-Pacific is expected to be the fastest-growing region at a 8.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biological Sample Collection Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to at-home/remote collection for diagnostics and decentralized trials | +1.8% | North America and Europe are leading, and Asia-Pacific adoption is accelerating | Short term (≤ 2 years) |

| Expansion of genetic testing (NIPT, PGx, oncology) requiring validated collection kits | +1.5% | Global, concentrated in high-income markets with reimbursement frameworks | Long term (≥ 4 years) |

| Ambient-stable nucleic-acid chemistries reducing cold-chain dependence | +1.3% | Global, with early adoption in decentralized-trial sponsors and telehealth networks | Medium term (2-4 years) |

| Persistent infectious-disease testing volumes (respiratory, STI) sustaining kit demand | +1.2% | Global, with elevated volumes in North America and Europe | Medium term (2-4 years) |

| Government procurement for surveillance and preparedness (stockpiles, sentinel networks) | +1.1% | North America, Europe, and the Asia-Pacific government health agencies | Short term (≤ 2 years) |

| Biobanking and precision-medicine programs standardizing preanalytics | +0.9% | North America, Europe, and select Asia-Pacific hubs (Singapore, Australia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Infectious-Disease Testing Volumes Sustaining Baseline Demand

Respiratory and sexually transmitted infection programs are still anchoring kit orders even after COVID-19 normalization. The CDC logged 2.2 million combined chlamydia, gonorrhea, and syphilis cases in 2024, a number higher than pre-pandemic levels despite a 9% yearly drop [2]Centers for Disease Control and Prevention, “Sexually Transmitted Disease Surveillance 2024,” cdc.gov. Influenza H3N2 subclade K and the SARS-CoV-2 BA.3.2 lineage triggered regional testing surges in early 2025, boosting demand for swabs and viral-transport kits. WHO influenza networks rely on standardized swab protocols, and multiplex respiratory panels detecting influenza A/B, RSV, and SARS-CoV-2 require validated kits that protect nucleic acids across multiple targets. Sentinel laboratories feeding national databases are therefore expected to maintain mid-single-digit growth in swab kit volume through 2028. Manufacturers are balancing this steady demand with lean inventory practices to avoid the overstock cycles seen in 2021-2022.

Rapid Shift to At-Home and Remote Collection

Self-collection devices are reshaping diagnostic workflows. The FDA approved Teal Health’s Wand for at-home HPV screening in May 2025, with 96% concordance with clinician samples, and the majority of users said home testing would keep them up to date with screening [3]U.S. Food and Drug Administration, “FDA Authorizes First Home Collection Kit for HPV Screening,” fda.gov. The agency’s September 2024 guidance formally permits fully decentralized trials for selected products, thereby reducing patient travel burdens and shortening enrollment timelines. European regulators endorse hybrid designs that mix site visits with remote sampling. Sponsors must still train participants to ensure specimen quality, yet cost savings from reduced site overhead and the ability to reach geographically dispersed patients outweigh the added complexity. Telehealth platforms now bundle collection kits with video guidance and prepaid returns, linking directly to CLIA laboratories for analysis.

Expansion of Genetic Testing

Non-invasive prenatal testing is growing rapidly, and sensitivity for trisomy 21 exceeds 99.3% when maternal blood is collected in stabilization tubes that prevent cell-free DNA degradation. Direct-to-consumer pharmacogenomics panels cleared by the FDA depend on saliva kits that maintain DNA integrity during ambient shipping, whereas oncology liquid biopsies require additives to preserve circulating tumor DNA for several days before processing. The BLOODPAC consortium published minimal technical data elements that many trial sponsors now adopt as de facto standards. Kit suppliers that furnish certificates of analysis and prove lot-to-lot consistency are becoming preferred vendors for decentralized oncology studies and precision-medicine clinics.

Ambient-Stable Nucleic-Acid Chemistries Reducing Cold-Chain Dependence

Ambient preservation is altering cost structures in the biological sample collection kits market. Merck’s RNAstable matrix keeps RNA viable for 29 months at room temperature, and Imagene’s DNAshell platform records 15-year stability with an estimated 38 000-year half-life. Eliminating dry-ice shipments can slash total logistics costs surged significantly, appealing to small telehealth providers and decentralized-trial sponsors operating on tight budgets. Faster transit and lower breakage also improve patient experience because kits no longer arrive with melted ice packs or condensation. Procurement teams are beginning to compare lifetime ownership costs rather than unit price alone, giving early-moving chemistries a strategic edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IVDR/FDA compliance costs and documentation complexity for self-collection devices | -1.4% | Europe (IVDR), North America (FDA 510(k)), with spillover to exporters in Asia | Short term (≤ 2 years) |

| Price pressure and tender-driven commoditization in swabs/VTM | -0.8% | Global, most acute in government tenders and hospital group-purchasing organizations | Medium term (2-4 years) |

| Raw-material volatility (medical-grade polymers, flocking fibers) impacting margins | -0.6% | Global, with supply-chain concentration in Asia-Pacific polymer producers | Short term (≤ 2 years) |

| Post-pandemic inventory normalization and destocking cycles | -0.9% | Global, concentrated in North America and Europe where stockpiles peaked in 2021-2022 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IVDR and FDA Compliance Costs Creating Consolidation Pressure

Europe’s In Vitro Diagnostic Regulation expanded notified-body oversight from roughly 10% of assays to 80%-90%, and certification now takes 13-18 months, with total fees often exceeding EUR 50, 000 (USD 58,800). The EUDAMED database becomes mandatory on 28 May 2026, compelling firms to upload labeling and surveillance data. A high number of manufacturers have already dropped some product lines after weighing the costs, leading to spot shortages of legacy kits.

Similar pressure exists in the United States, where 510(k) submissions for self-collection devices require human-factors data and post-market plans. Smaller vendors without dedicated regulatory teams are therefore pursuing mergers or exiting altogether, nudging industry concentration higher.

Raw-Material Volatility Compressing Margins

Medical-grade polypropylene and polyethylene prices still fluctuate with feedstock movements, and specialty flocking fibers experienced severe shortages during the 2020-2021 surge. Although capacity has normalized, lead times for high-grade fibers remain long, and commodity swab makers face aggressive price ceilings in hospital and government tenders. Suppliers are trimming low-volume SKUs and emphasizing higher-margin dried blood-spot cards and ambient-stable tubes where proprietary chemistries justify premium pricing. The shift is visible in product roadmaps that favor integrated barcodes, tamper-evident seals, and pre-filled buffers aimed at precision-medicine cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Blood Collection Dominance with Specialty Formats Gaining Share

Blood-collection kits accounted for 33.48% of 2025 revenue, and this segment of the biological sample collection market is growing at an 8.34% CAGR through 2031. The biological sample collection kits market for blood-collection devices is expanding as hospitals mandate safety needles that reduce injuries by 71% compared with legacy designs. Swab and viral-transport kits remain core to respiratory and STI surveillance, yet face tender-driven price compression. Saliva kits are capitalizing on direct-to-consumer genomics and hormone assays; 23andMe relies on proprietary tubes for its FDA-cleared pharmacogenetics panel.

Specialty formats are moving up the value chain. Dried blood-spot cards, once confined to newborn screening, now support decentralized pharmacokinetic studies following the FDA's 2024 bioanalytical guidance. Buccal swab DNA kits continue to underpin forensics and paternity testing, while urine collectors support drug screening. Stool and fecal microbiome kits are emerging for colorectal cancer screening and inflammatory bowel disease monitoring, yet most offerings still target research use. Vendors that can obtain CLIA validation for these kits hold significant white-space potential.

By Application: Diagnostics Leadership with Decentralized Trials Accelerating

Diagnostics captured 45.84% of 2025 revenue and is expanding at an 8.12% CAGR, keeping the biological sample collection kits market at the center of infectious-disease and genetic screening programs. The FDA’s HPV home-collection clearance highlighted patient willingness to use self-collection, and multiplex respiratory panels are embedding kit specifications in tender documents. Research and academia run standardized protocols anchored in ISO 20070:2025 container requirements.

Clinical and decentralized trials form the fastest-growing subsegment. Analysis of 1,370 U.S. decentralized trials found the majority used digital tools and 21% involved device endpoints between 2000 and 2023. Remote specimen collection lowers dropout rates in oncology and rare-disease studies where travel costs deter participation. Sponsors must, however, audit local laboratories or arrange validated shipping to central sites to ensure data integrity. Direct-to-consumer genomics and wellness players continue to rely on saliva and buccal swab kits, although reimbursement for wellness tests is patchy.

By End User: Laboratory Consolidation with Telehealth Operators Emerging

Diagnostic laboratories accounted for 42.38% of revenue in 2025 and are expected to grow at a 8.53% CAGR through 2031, driven by regional reference labs merging and expanding their molecular testing menus. Closed-system blood-collection tubes with hemolysis-reduction features are now standard requisites in tenders. Academic institutes and biobanks follow ISBER best practices that demand barcoded kits and certificates of analysis, raising the entry bar for small suppliers.

Pharmaceutical sponsors are procuring more kits for remote trials, and at-home self-collection platforms rank as the fastest-growing end users. Telehealth companies bundle kits with mobile apps that walk patients through collection and track return rates. Partnerships with CLIA laboratories ensure compliance while keeping shipping distances short, a model expected to spread beyond the United States as regulatory frameworks mature.

Geography Analysis

North America accounted for 44.25% of global revenue in 2025, reflecting entrenched diagnostic infrastructure and high per capita healthcare spending. The U.S. Department of Health and Human Services earmarked USD 306 million for H5N1 preparedness in 2025, including USD 8 million for kit manufacturing. The CDC’s Epidemiology and Laboratory Capacity program supplied USD 364 million in 2024 to upgrade specimen logistics across state labs. Regulatory approvals for at-home HPV screening and pharmacogenomics tests are further normalizing self-collection, while decentralized-trial sponsors lean heavily on ambient-stable tubes to sidestep frozen shipping.

Asia-Pacific is the fastest-growing region, with a 8.48% CAGR, accounting for a significant share of the biological sample collection kits market in 2025. India’s PM-ABHIM allocated INR 4,770 crore (USD 570 million) in FY 2025 to build district laboratories, a major year-on-year rise. The Union Budget 2026 pledged INR 10,000 crore for Bio SHAKTI to seed 1,000 trial sites, while the Production Linked Incentive scheme steers INR 34.2 billion toward in-vitro diagnostic devices. China is rolling out regional genomics centers, and Japan’s multiplex genetic point-of-care devices, launched in late 2023, are stimulating demand for saliva and blood kits across oncology and prenatal testing.

Europe remains sizable, but growth is tempered by IVDR-related overheads, which have driven significant number of firms to discontinue some products. Certification queues and limited notified-body capacity prolong market entry, tilting the share toward large incumbents. The Middle East and Africa, plus South America, are early in the adoption curve; government procurements for surveillance and donor-funded disease programs keep baseline volumes stable, with private diagnostic chains gradually adding molecular panels that require higher-grade collection kits.

Competitive Landscape

The biological sample collection kits market is moderately fragmented. Top players maintain scale advantages in regulatory compliance, distribution, and vertically integrated production. At the same time, regional specialists thrive in niches such as dried blood spot cards and ambient-stable nucleic acid tubes. Merck’s RNAstable and Imagene’s DNAshell are reframing value propositions around room-temperature longevity. These chemistries shrink logistics costs and turnaround times, a benefit that resonates with decentralized-trial sponsors and telehealth operators who ship single-patient kits nationwide.

Strategic moves center on vertical integration. Several large manufacturers now own CLIA laboratories, allowing them to offer turnkey solutions from kit supply to test reporting. Smaller firms chase ISO 13485 certification and notified-body approvals ahead of the EUDAMED deadline. BD’s passive-retraction needle, cleared in November 2025, exemplifies incremental innovation that meets hospital safety committees' requirements. Direct-to-consumer genomics brands such as 23andMe are backward-integrating into kit design to secure supply and protect proprietary chemistries.

Ambient-stable technologies are also fostering collaboration. Exact Sciences partnered with a telehealth platform in September 2025 to provide at-home stool collection for colorectal cancer screening, integrating digital instructions to lift return rates. Thermo Fisher’s February 2026 capacity expansion targets the same decentralized-trial and telehealth customer base, underscoring how incumbents are positioning for sustained growth in remote sampling.

Biological Sample Collection Kits Industry Leaders

Becton, Dickinson and Company

F. Hoffmann-La Roche

QIAGEN

Thermo Fisher Scientific

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Thermo Fisher Scientific will expand North American kit manufacturing with new ambient-stable tube and microsampling lines, shipping by Q4 2026.

- December 2026: F. Hoffmann-La Roche secured a multi-year contract to supply ISO 20070-compliant blood and saliva kits to a European biobank consortium handling 500 000 samples a year.

- November 2025: Becton, Dickinson and Company (BD) obtained FDA 510(k) clearance for a passive-retraction safety blood-collection needle aimed at further lowering needlestick injury rates.

Global Biological Sample Collection Kits Market Report Scope

As per the scope of the report, biological sample collection kits are specialized medical and research tools designed to collect, stabilize, and transport various types of specimens such as blood, saliva, urine, stool, and tissue from donors to laboratories for analysis. These kits are essential for ensuring the integrity of collected biomolecules, such as DNA and RNA, which can degrade rapidly if not handled according to standardized protocols.

The biological sample collection kits market is segmented by product, application, end user, and geography. Based on product, the market is segmented into blood collection kits, swab and viral transport kits, saliva collection kits, dried blood spot (DBS) collection cards/kits, buccal swab DNA collection kits, urine collection kits, and stool/fecal microbiome collection kits. By application, the market is segmented into diagnostics, research & academia, biobanking & biorepositories, clinical trials & decentralized trials, forensics & law enforcement, and direct-to-consumer genomics & wellness testing. By end users, the market is segmented into hospitals & clinics, diagnostic laboratories, academic & research institutes, biobanks & biorepositories, pharmaceutical & biotechnology companies, and at-home self-collection / telehealth program operators.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Blood Collection Kits |

| Swab And Viral Transport Kits |

| Saliva Collection Kits |

| Dried Blood Spot (DBS) Collection Cards/Kits |

| Buccal Swab DNA Collection Kits |

| Urine Collection Kits |

| Stool/Fecal Microbiome Collection Kits |

| Diagnostics |

| Research & Academia |

| Biobanking & Biorepositories |

| Clinical Trials & Decentralized Trials |

| Forensics & Law Enforcement |

| Direct-To-Consumer Genomics & Wellness Testing |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Biobanks & Biorepositories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Blood Collection Kits | |

| Swab And Viral Transport Kits | ||

| Saliva Collection Kits | ||

| Dried Blood Spot (DBS) Collection Cards/Kits | ||

| Buccal Swab DNA Collection Kits | ||

| Urine Collection Kits | ||

| Stool/Fecal Microbiome Collection Kits | ||

| By Application | Diagnostics | |

| Research & Academia | ||

| Biobanking & Biorepositories | ||

| Clinical Trials & Decentralized Trials | ||

| Forensics & Law Enforcement | ||

| Direct-To-Consumer Genomics & Wellness Testing | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Biobanks & Biorepositories | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the market size of biological sample collection kits market in 2025?

The Biological Sample Collection Kits Market size is projected to expand from USD 12.53 billion in 2025 and USD 13.41 billion in 2026 to USD 19.68 billion by 2031, registering a CAGR of 7.97% between 2026 to 2031.

Which product type leads revenue within this field?

Blood-collection kits held 33.48% of 2025 revenue and remain the leading product thanks to hospital safety mandates and closed-system workflows.

How fast is Asia-Pacific expanding in this space?

Asia-Pacific is projected to grow at an 8.48% CAGR to 2031, supported by large public-health laboratory investments in India and diagnostic infrastructure expansion in China and Japan.

Why is IVDR impacting European suppliers?

The regulation now requires notified-body review for up to 90% of devices, adding fees above EUR 50 000 and stretching certification timelines to 18 months, prompting smaller firms to discontinue products.

Page last updated on: