Ambulance Stretchers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

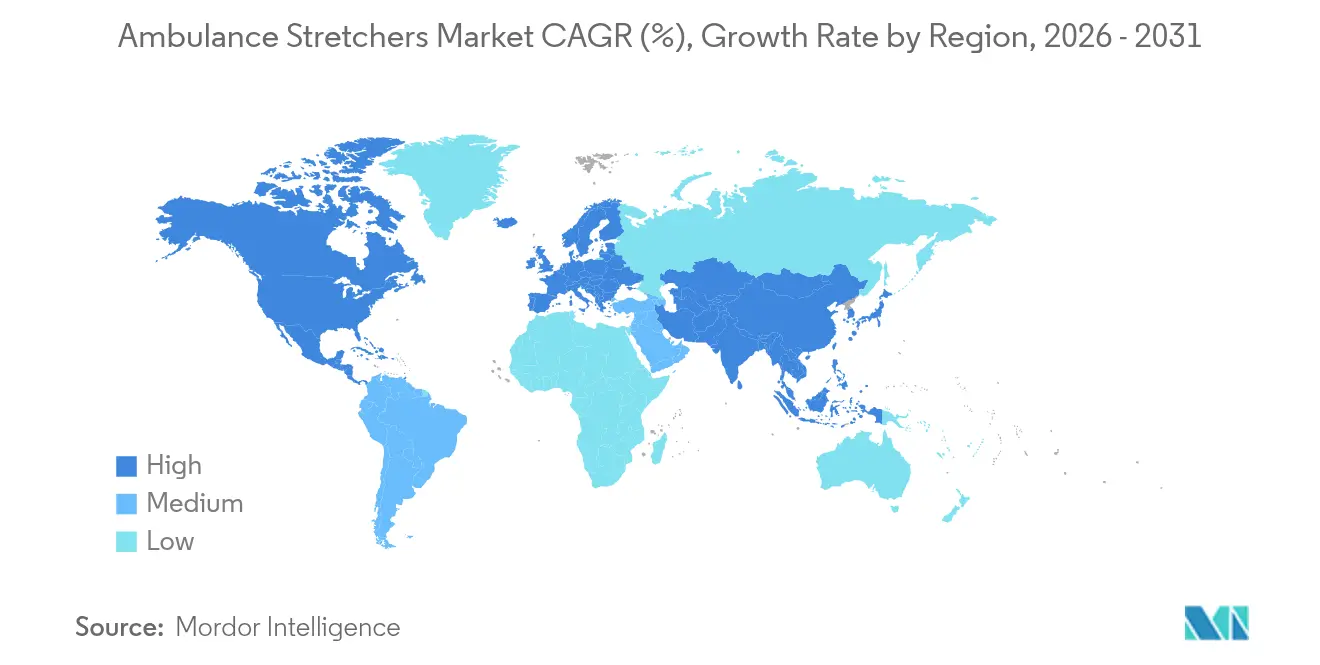

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambulance Stretchers Market Analysis by Mordor Intelligence

ambulance stretchers market size in 2026 is estimated at USD 2.38 billion, growing from 2025 value of USD 2.30 billion with 2031 projections showing USD 2.79 billion, growing at 3.27% CAGR over 2026-2031. Demand is rising as aging populations require equipment that accommodates multiple chronic conditions and as low- and middle-income countries expand trauma-care capacity. Workforce-safety regulations in developed economies are accelerating the shift from manual to electric-powered models, while road-traffic injuries in emerging regions sustain baseline volume growth. The dual focus on bariatric capability and rapid patient transfers is reshaping procurement priorities, opening white-space for platform-based products compatible across ambulance types. Supply-chain disruption during the pandemic has also lowered the entry barrier for regional suppliers willing to address cost-sensitive buyers with compliant yet affordable designs.

Key Report Takeaways

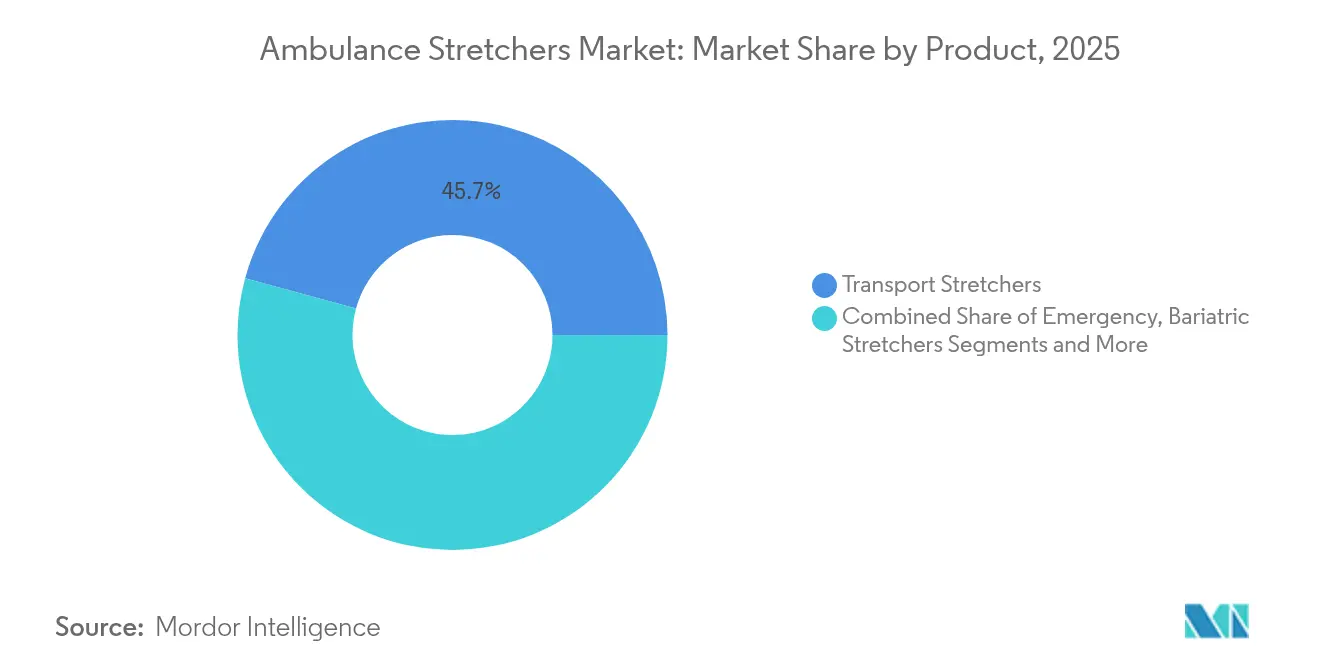

- By product type, transport stretchers held 45.74% of the ambulance stretcher market share in 2025, whereas bariatric stretchers are forecast to expand at a 9.1% CAGR through 2031.

- By technology, the manual segment retained 60.62% of ambulance stretcher market share in 2025, while electric systems are advancing at a 10.02% CAGR to 2031.

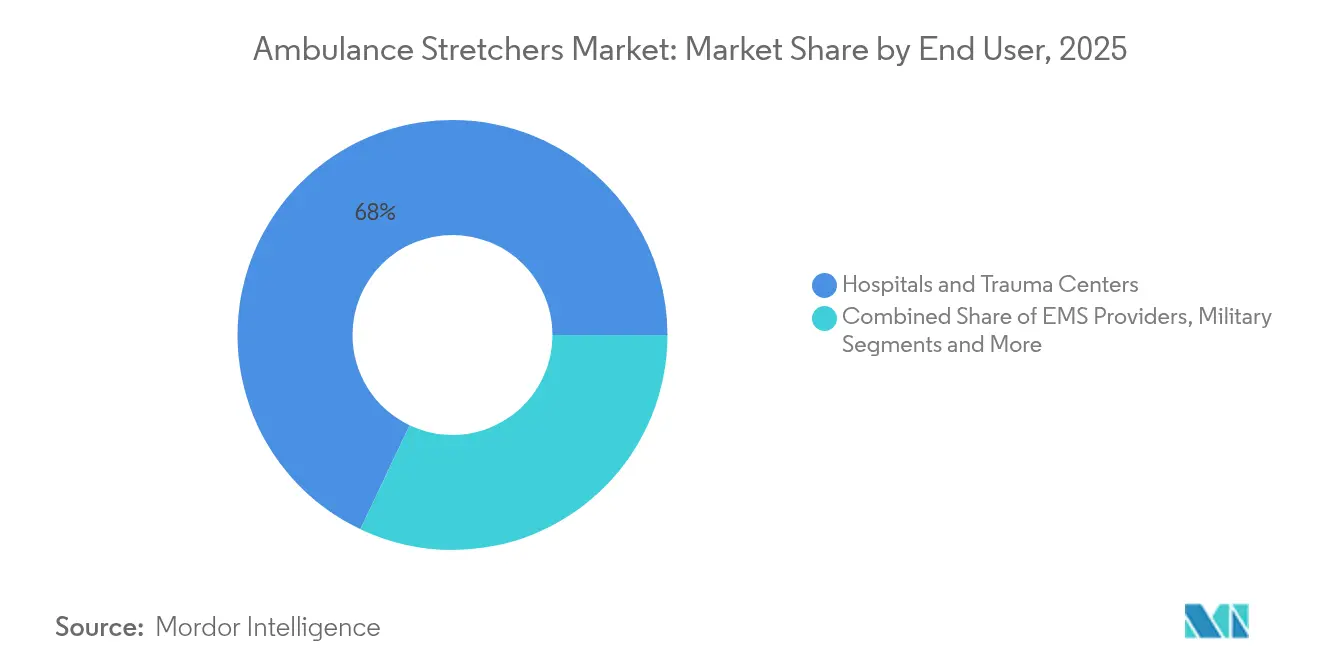

- By end user, hospitals and trauma centers captured 67.95% of the ambulance stretcher market size in 2025; military and disaster-relief agencies are projected to grow at an 8.18% CAGR.

- By geography, North America led with 35.34% revenue share in 2025, whereas the Middle East and Africa region is growing fastest at 7.33% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ambulance Stretchers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-Linked Chronic Disease Burden | +0.80% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Road-Traffic Trauma Growth In EMs & LMICs | +0.60% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Worldwide Upgrade To Type III & Modular Ambulances | +0.40% | North America, Europe, developed APAC markets | Medium term (2-4 years) |

| EMS Reimbursement Expansion In APAC | +0.30% | APAC core markets | Short term (≤ 2 years) |

| Extreme-Temperature Response-Ready Composite Stretchers | +0.20% | Global, with emphasis on extreme climate regions | Long term (≥ 4 years) |

| OEM-Agnostic IoT Sensor Retrofits Driving Aftermarket | +0.20% | Developed markets globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-Linked Chronic Disease Burden

One in five U.S. residents will be at least 65 years old by 2030, intensifying demand for stretchers with multi-position functions, wider frames, and enhanced pressure-relief surfaces.[1]D. Jones, “The Aging U.S. Population and Health Infrastructure,” Nature, nature.com Healthcare providers facing physician shortages are adopting ergonomic equipment to transfer complex cases safely with fewer staff, making stretcher design a workforce-retention lever rather than a routine purchase. Bariatric devices now double as mobility platforms inside emergency departments, shortening handoff times and lowering fall risk. Procurement teams increasingly specify weight ratings above 300 kg and integrated monitoring rails as baseline requirements. These shifts collectively amplify premium-segment revenue and expand the addressable pool for electric power-lift models.

Road-Traffic Trauma Growth in EMs & LMICs

Road accidents account for 37.3% of trauma cases in Addis Ababa and similar shares across sub-Saharan hubs, yet only 13.6% of victims receive adequate stabilization before hospital transfer in countries like Tanzania. This mismatch drives demand for durable stretchers able to perform both extraction and transport functions under resource constraints. International donor programs now bundle stretcher purchases with ambulance grants, accelerating first-generation upgrades in provincial fleets. Manufacturers responding with cost-down versions that still meet EN1789 and FDA class I requirements widen their reach without compromising safety. As governments adopt WHO trauma-system guidelines, spending on transport and scoop stretchers is shifting from sporadic tenders to multiyear budgets, lifting baseline volumes across Africa and South Asia.

Worldwide Upgrade to Type III & Modular Ambulances

Advanced chassis allow caregivers to reconfigure interiors between trauma, cardiac, and neonatal loads, raising the importance of stretchers that dock to multiple floor tracks. Composite frames that resist biofluid corrosion and contain RFID tags for preventive maintenance are moving from premium to mainstream. OEM-agnostic stretcher mounts shorten vehicle build cycles and lower whole-life costs, a key selling point for fleet operators under fixed-payment EMS contracts. Integration of multi-point restraint systems improves crash survivability and supports national road-safety targets. The net effect is sustained replacement demand across mature markets even as fleet counts plateau.

EMS Reimbursement Expansion in APAC

Japan’s increase in ambulance transport payments improved hospital acceptance rates and prompted regional neighbors to trial similar policies.[2]H. Tekle, “Urban Trauma Burden in Addis Ababa,” QScience, qscience.com Higher tariffs free up working capital for devices that cut unloading times, such as powered cots with one-button lift functions. Singapore’s prototype motorized stretcher, designed for single-operator use, illustrates how fee reforms spur local R&D tailored to dense urban environments.[3]P. Tan, “Motorised Stretcher for SCDF,” HTX Press Room, htx.gov.sg Private hospital chains in Southeast Asia are replicating this approach to differentiate service quality and attract medical tourists. As reimbursement ceilings rise, procurement decisions shift from the lowest up-front price to total cost of ownership, encouraging the adoption of telematics-ready stretchers that flag maintenance needs automatically.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-Related Musculoskeletal Injuries To EMS Staff | -0.40% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Capital-Intensive Power-Lift Systems For Low-Income Fleets | -0.30% | LMICs, rural healthcare systems globally | Medium term (2-4 years) |

| Stricter Biocontamination Norms Lengthen Approval Cycles | -0.20% | Global, with emphasis on FDA and EU regulated markets | Medium term (2-4 years) |

| Raw-Material Price Volatility | -0.20% | Global, with highest impact on cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-Related Musculoskeletal Injuries to EMS Staff

EMS personnel register injury rates surpassing construction workers, with manual cot lifting singled out as a primary cause. University of Waterloo research found a 78% drop in paramedic injuries after powered stretcher deployment. Despite clear ROI from reduced compensation claims, some municipal services defer upgrades due to procurement cycles and union negotiations. Worker-safety advocacy groups now lobby regulators to set mandatory force-exertion thresholds, potentially accelerating electric adoption but raising near-term compliance costs. Persistent staffing shortages magnify the operational impact of each injury, incentivizing fleets to accelerate replacement timetables once financing aligns.

Capital-Intensive Power-Lift Systems for Low-Income Fleets

A powered cot and compatible loading rail can exceed USD 40,000, a sum greater than annual equipment budgets for many district hospitals. Maintenance complexity and patchy electricity supply add hidden costs that deter rural buyers even when grant funding offsets the purchase price. As a result, the ambulance stretchers market bifurcates into premium, automation-rich offerings for developed settings and rugged manual designs for cash-strapped operators. Non-governmental aid organisations often procure refurbished stretchers to stretch limited funds, but upcoming FDA regulations on remanufacturing could constrain this workaround by imposing stricter traceability requirements. Unless financing models evolve, penetration of power-lift systems will stall in underserved regions, capping upside for global volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Transport Dominance Masks Bariatric Opportunity

Transport stretchers generated the most significant revenue slice, accounting for 45.74% of the ambulance stretchers market size in 2025. Their ubiquity across emergency fleets ensures predictable replacement cycles, but commoditization pressures margins as specifications standardize. Bariatric models, by contrast, are climbing at 9.1% CAGR as obesity prevalence rises in developed economies. Scoop and basket stretchers continue to serve confined-space rescues, yet remain niche. Neonatal variants see steady demand tied to hospital birthing volumes, while trauma-specific designs face moderate growth as modular ambulance interiors assume more tasks.

Demand for bariatric equipment is reinforced by regulations that stipulate minimum safe-working loads above 300 kg and require four-point harnesses for larger patients. These standards drive the procurement of stretchers with more expansive decks and motorized height adjustment. In turn, manufacturers integrate antimicrobial coatings and quick-swap mattress systems to minimize turnaround time in high-occupancy departments. As a result, the bariatric line is transitioning from optional inventory to essential stock in tertiary-care facilities, expanding its revenue contribution in the broader ambulance stretchers market.

By Technology: Electric Transition Accelerates Despite Manual Dominance

Manual designs will still command 60.62% of the ambulance stretcher market in 2025, supported by lower up-front cost and minimal maintenance. Yet, electric units exhibit 10.02% CAGR as care providers quantify lifetime savings from injury avoidance and faster turnaround. Pneumatic and hydraulic platforms serve rural or military users where battery reliability is uncertain, but their share is shrinking as lithium-iron-phosphate cells improve cold-weather performance.

Adopters of electric coats often bundle automated loading rails, cutting patient loading time by up to 30 seconds and lowering exertion forces below occupational-safety thresholds. Real-time diagnostics embedded in motor controllers trigger service alerts before faults immobilize vehicles, enhancing fleet uptime. Coupled with IoT telemetry, these features position electric stretchers as data-generating assets, aligning with hospital digital twin initiatives. Consequently, the technology shift is poised to reshape the ambulance stretchers market as mature purchasers replace legacy rigs on five- to seven-year cycles.

By End User: Military Growth Outpaces Traditional Healthcare

Hospitals and trauma centers contribute 67.95% of the ambulance stretcher market share, reflecting their central role in patient stabilization and intra-facility transfers. Procurement volumes mirror admission rates and regulatory mandates for worker safety. Military and disaster-relief agencies, however, are growing at 8.18% CAGR, buoyed by modernization programs that prioritize rapid casualty evacuation. The trend spans NATO and non-aligned nations alike, spurred by heightened geopolitical risk and climate-driven natural disasters.

Defense buyers specify stretchers compatible with rotary-wing platforms and CBRN-resistant materials, pushing suppliers into niche engineering. Disaster agencies need collapsible, lightweight frames deployable in austere conditions, often with thermal blankets integrated for hypothermia management. These divergent requirements spur product-line extensions that subsequently filter into civilian ambulance fleets seeking multipurpose capability, creating spillovers that benefit the entire ambulance stretchers industry.

Geography Analysis

North America holds a 35.34% revenue share and sets the pace for regulatory and technology trends. Occupational-safety statutes and high labor costs favor powered systems, sustaining premium pricing. The U.S. CARES Act capital allocations enabled county EMS agencies to refresh fleets post-pandemic, while Canadian provinces adopted similar stimulus frameworks. The ongoing alignment of the FDA Quality System Regulation with ISO 13485 raises compliance costs while stabilizing product quality, reinforcing the market position of well-capitalized incumbents.

The Middle East and Africa region delivers the fastest CAGR at 7.33% by 2031. Governments channel oil revenues into tertiary hospitals and trauma centers, with Saudi Arabia alone budgeting USD 50.4 billion for health-sector development in 2023. Private operators building medical-tourism hubs in the Gulf import U.S. and European stretcher brands to meet Joint Commission International accreditation. Simultaneously, African Union programs subsidize basic EMS fleets, opening doors for value-engineered models. This two-tier demand landscape encourages multinational vendors to localize assembly to sidestep import duties and qualify for public tenders.

Asia Pacific is the most diverse territory. Japan and Singapore mandate advanced safety features, fostering early adoption of motorized stretchers and telematics. Conversely, populous nations such as Indonesia focus on scaling fleet numbers with robust manual units. Domestic manufacturing incentives under schemes like India’s Production-Linked Incentive encourage joint ventures, facilitating technology transfer while containing costs. As digital health funding rises, hospitals in South Korea and Australia pilot stretchers with integrated RFID to streamline asset tracking, setting precedents that the wider region may emulate.

Competitive Landscape

The ambulance stretchers market features a moderately consolidated structure anchored by Stryker, Ferno-Washington, and Hill-Rom. Collectively, these players leverage global distribution, broad product portfolios, and certification expertise to defend share against price-focused entrants. Their innovation pipelines center on injury-reduction technology, IoT integration, and modular component platforms that shorten new-product cycles. Stryker’s MedSurg division posted 10.6% growth in 2024 on the back of powered cot demand, reinforcing the profitability of premium positioning.

Regional manufacturers in China, Turkey, and Poland exploit supply-chain resiliency concerns by touting localized sourcing and faster lead times. Some collaborate with ambulance OEMs to supply private-label stretchers bundled in turnkey vehicles, eroding incumbents' brand visibility in cost-sensitive markets. Regulatory convergence around ISO 13485 eases cross-border expansion for compliant mid-tier firms, intensifying competition in Latin America and Eastern Europe.

Strategic moves increasingly revolve around data services. Leading vendors embed sensor suits that track load cycles, battery health, and cleaning compliance, offering subscription analytics that create recurring revenue. Partnerships with fleet-management software providers integrate stretcher status into dispatch dashboards, enhancing value propositions beyond hardware. Meanwhile, aftermarket refurbishment gains traction as hospitals seek circular-economy credentials, although forthcoming FDA remanufacturing guidance will likely thin the field to operators with robust quality systems.

Ambulance Stretchers Industry Leaders

Stryker Corporation

Ferno-Washington Inc.

Narang Medical Limited

Fu Shun Hsing Technology Co. Ltd

Hill-Rom Services Inc. (Baxter)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Road Rescue debuted the RediMedic Type I and Type III ambulance platform with composite body panels and Per4Max restraint integration.

- June 2024: Singapore’s HTX unveiled a single-operator motorized stretcher prototype for the Civil Defence Force’s high-rise rescue missions.

- February 2024: FDA amended its Quality System Regulation, effective Feb 2026, harmonizing U.S. medical-device GMP with ISO 13485 requirements.

Global Ambulance Stretchers Market Report Scope

As per the scope of this report, ambulatory stretchers are collapsible wheeled stretches that are used for moving patients. Moreover, emergency medical services use these stretchers for mobilizing out-of-hospital patients. Therefore, stretchers used in ambulances need to be light, strong, and compatible to assist personnel in carefully handling patients. The ambulance stretchers market is segmented by product (transport stretchers and emergency stretchers), technology (manual stretchers, electric powered stretchers, pneumatic stretchers, and other technologies), end user (clinics and hospitals, ambulatory surgical centers, and other end users), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments. The report offers the value (in USD billion) for the above segments.

| Transport Stretchers |

| Emergency Stretchers |

| Bariatric Stretchers |

| Neonatal & Paediatric Stretchers |

| Scoop & Basket Stretchers |

| Manual |

| Electric-Powered |

| Hydraulic/Pneumatic |

| Automated Loading Systems |

| Hospitals & Trauma Centers |

| EMS Providers |

| Military & Disaster-Relief Agencies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Transport Stretchers | |

| Emergency Stretchers | ||

| Bariatric Stretchers | ||

| Neonatal & Paediatric Stretchers | ||

| Scoop & Basket Stretchers | ||

| By Technology | Manual | |

| Electric-Powered | ||

| Hydraulic/Pneumatic | ||

| Automated Loading Systems | ||

| By End-User | Hospitals & Trauma Centers | |

| EMS Providers | ||

| Military & Disaster-Relief Agencies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the ambulance stretchers market?

The ambulance stretchers market stands at USD 2.38 billion in 2026.

How fast is the ambulance stretchers market expected to grow?

It is projected to expand at a 3.27% CAGR, reaching USD 2.79 billion by 2031.

Which product segment is growing quickest?

Bariatric stretchers are advancing at 9.1% CAGR due to rising obesity rates and updated safe-handling regulations.

Why are electric ambulance stretchers gaining traction?

They reduce caregiver injuries and speed patient loading, leading to a 10.02% CAGR despite higher initial cost.

Which region offers the highest growth potential?

The Middle East and Africa region leads in growth at 7.33% CAGR thanks to large-scale health-infrastructure spending.

Page last updated on: