Fatty Methyl Ester Sulfonate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

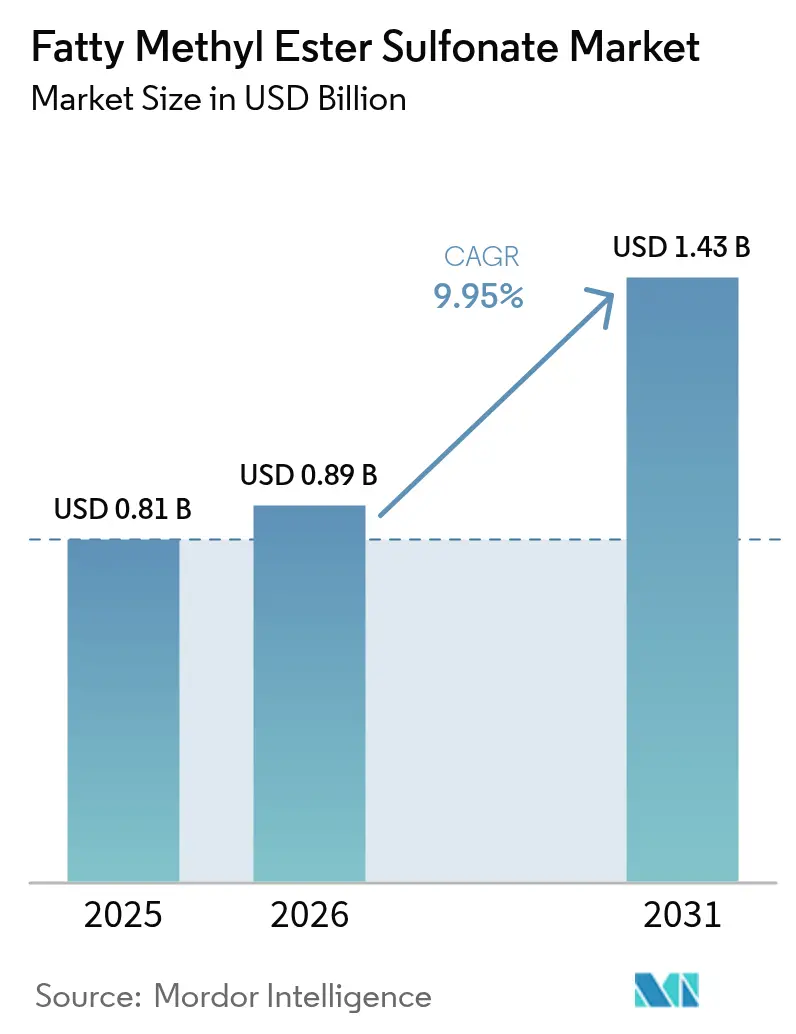

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

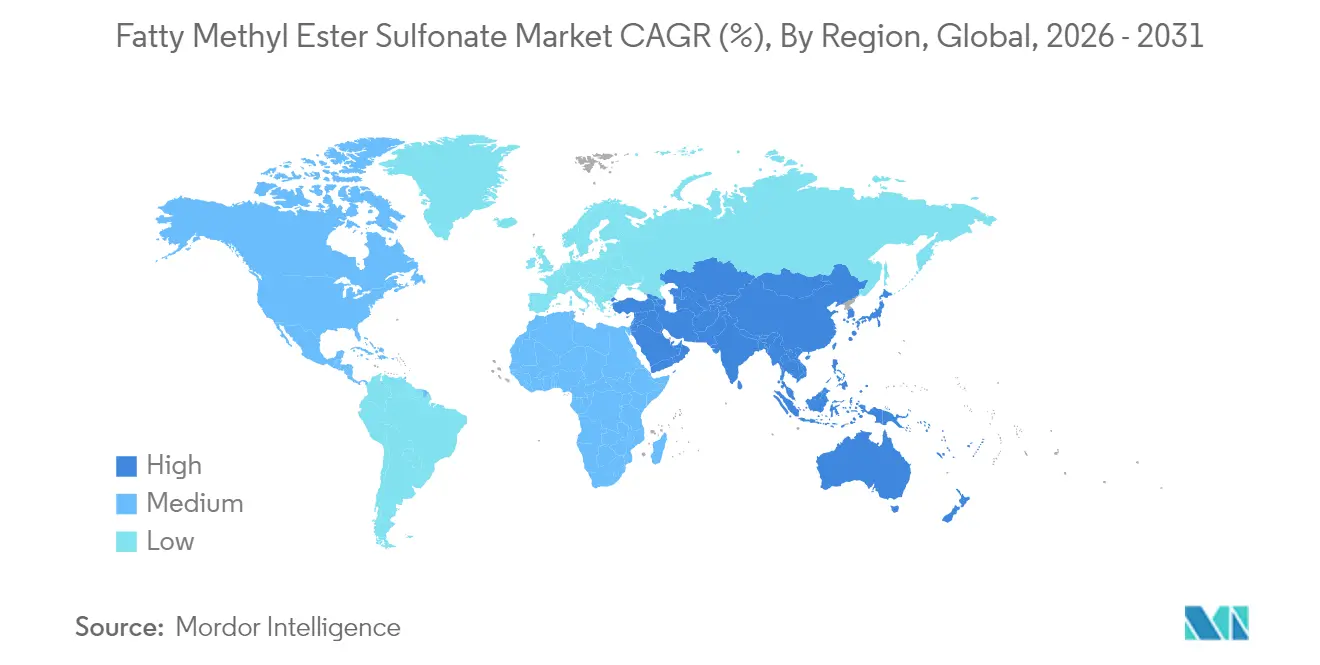

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fatty Methyl Ester Sulfonate Market Analysis by Mordor Intelligence

The fatty methyl ester sulfonate market size is expected to grow from USD 0.81 billion in 2025 to USD 0.89 billion in 2026 and is forecast to reach USD 1.43 billion by 2031 at 9.95% CAGR over 2026-2031. This solid growth trajectory mirrors the global pivot toward bio-based surfactants, tighter environmental regulations, and the cost gains delivered by modern oleochemical processes. Ample palm kernel and coconut oil supplies in Southeast Asia, sustained capital expenditure in sulfonation capacity, and the preference for compact detergent formats continue to widen commercial acceptance. The fatty methyl ester sulfonate market now benefits from corporate decarbonization commitments that favor renewable feedstocks, rising premiums for mild and non-irritating ingredients, and certification programs that reward traceable supply chains. Despite feedstock price swings and high entry costs for specialized equipment, sustained demand from both detergents and premium personal-care lines keeps overall sentiment positive

Key Report Takeaways

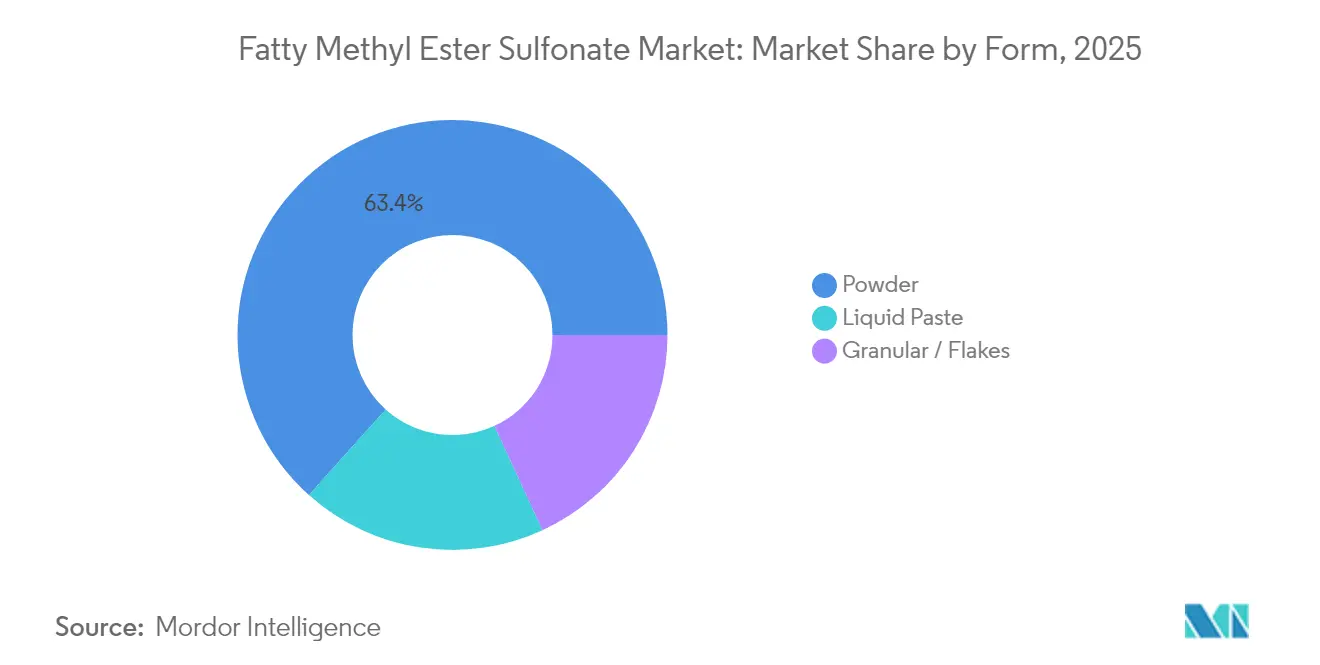

- By form, powder products held 63.36% of the fatty methyl ester sulfonate market share in 2025; liquid paste variants are forecast to register an 10.86% CAGR through 2031.

- By feedstock source, palm-kernel oil commanded 81.68% share of the fatty methyl ester sulfonate market size in 2025; coconut oil is the fastest-growing feedstock at an 11.31% CAGR.

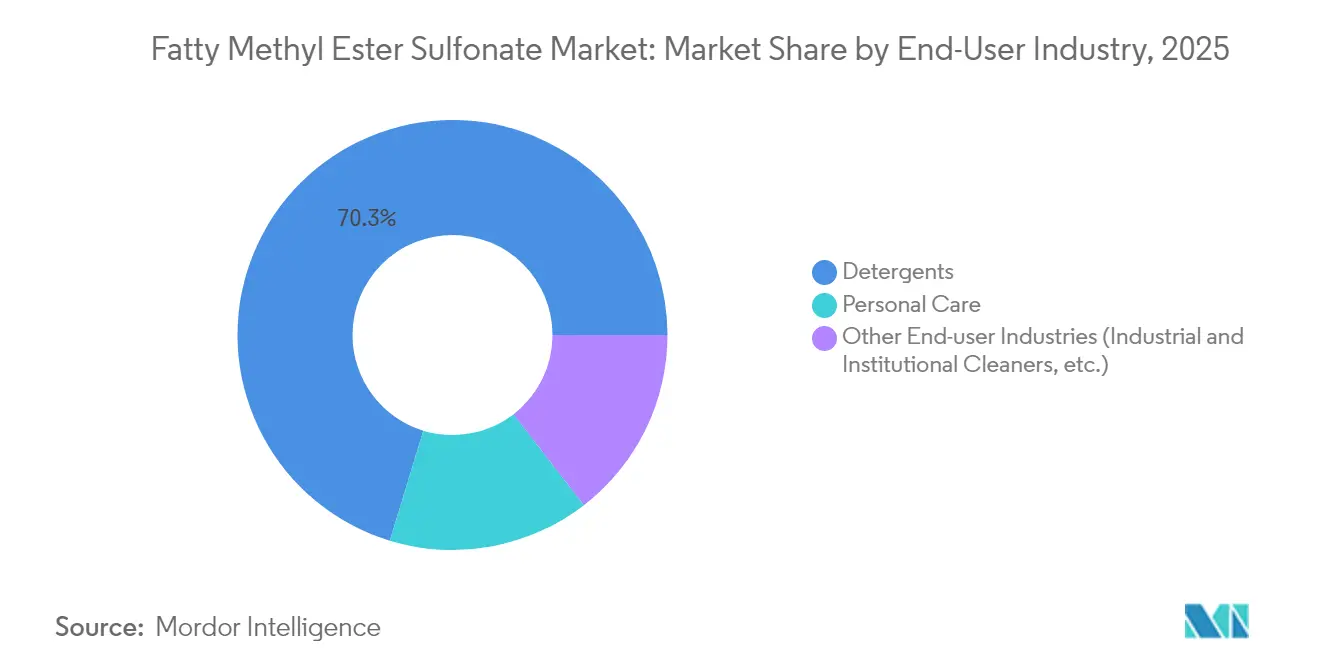

- By end-user industry, detergents led with 70.29% revenue share in 2025, while personal care is projected to expand at an 11.02% CAGR to 2031.

- By geography, Asia-Pacific accounted for 57.26% of 2025 revenues, and the region is set to grow at a 10.82% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fatty Methyl Ester Sulfonate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for bio-based surfactants | +2.8% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Rapid penetration of premium compact powders | +1.9% | North America & Europe core, expanding to APAC | Short term (≤ 2 years) |

| Growing demand from personal care industry | +2.1% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Increasing demand for mild and non-irritating surfactants | +1.6% | Global, with premium markets in developed regions | Medium term (2-4 years) |

| Expansion of the cleaning products market | +1.4% | APAC manufacturing hubs, global distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Bio-Based Surfactants

Switching to bio-based surfactants has moved from niche to mainstream as regulators mandate lower carbon footprints and consumers favor products with renewable content. The renewable chemicals sector, encompassing surfactants, will grow 19.11% annually to 2030, reinforcing downstream appetite for fatty methyl ester sulfonates. Multinationals are expanding biomass-balance approaches; BASF added coco-derived betaine grades to its EcoBalanced line to capture the sustainability premium[1]BASF SE, “EcoBalanced Portfolio Expansion,” basf.com. Institutional efforts such as the EU-funded SurfToGreen program, aiming for surfactants with more than 95% bio-content, further institutionalize demand[2]Circular Bio-based Europe, “SurfToGreen Project Overview,” europa.eu. These mutually reinforcing forces underpin enduring upside for the fatty methyl ester sulfonate market.

Rapid Penetration of Premium Compact Powders

Concentrated laundry formats demand surfactants that maintain high foam in low-volume formulations, where fatty methyl ester sulfonates excel. Manufacturers are pairing FMES with novel eco-enzymes to lift stain removal while lowering wash temperature requirements, thereby shrinking energy use. Consumers increasingly accept higher unit prices in exchange for smaller, lighter packs, which cut transport emissions and align with zero-waste goals. The trend, originating in Europe and North America, is spreading across emerging Asia as retailers push compact lines to optimize shelf space. This widespread adoption reinforces volume growth in the fatty methyl ester sulfonate market

Growing Demand from Personal Care Industry

Personal-care formulators view FMES as a naturally sourced, sulfate-free alternative that delivers gentle cleansing and rapid biodegradation. BASF’s launch of Dehyton PK45, derived from Rainforest Alliance-certified coconut oil, illustrates supplier innovation targeting premium skincare. Asia’s expanding middle class fuels premium hair- and skin-care uptake, with China and India leading consumption gains. Premium price points in these categories offset production cost pressures and support margin expansion across the fatty methyl ester sulfonate market.

Increasing Demand for Mild and Non-Irritating Surfactants

Ingredient-sensitive consumers scrutinize product safety and skin-sensory attributes, elevating mild surfactants such as FMES. The EPA’s Safer Choice Program endorses low-toxicity alternatives, accelerating brand reformulation roadmaps in North America[3]United States Environmental Protection Agency, “Safer Choice Program Criteria,” epa.gov. Parallel R&D in glycolipid hydrotropes, including heptyl glucoside, signals a broader industry push toward skin-friendly cleansing bases[4]American Oil Chemists’ Society, “Heptyl Glucoside as Sustainable Hydrotrope,” aocs.org. Collectively, these developments extend FMES's relevance beyond detergents into household and pet-care lines, deepening penetration of the fatty methyl ester sulfonate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility | -1.8% | APAC production hubs, global supply chains | Short term (≤ 2 years) |

| Hydrolysis & viscosity issues in high-water liquid detergents | -0.9% | Global liquid detergent markets, particularly North America & Europe | Medium term (2-4 years) |

| High production costs | -1.4% | Global manufacturing, particularly new entrants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Palm and coconut oil account for nearly two-thirds of total FMES manufacturing cost, so rising prices pressure margins. Indonesia’s B40 biodiesel mandate lifted crude palm oil futures toward MYR 5,000 per tonne in 2025, adding procurement stress for surfactant makers. Coconut oil faces upward pressure as the Philippines warns of tightening global supply while considering export curbs. Climate factors, including El Niño-linked droughts, heighten volatility and complicate long-term feedstock hedging, weighing on the fatty methyl ester sulfonate market.

High Production Costs

FMES plants require specialized sulfonation reactors, corrosion-resistant alloys, and continuous neutralization systems that elevate capital intensity. After multimillion-dollar optimization, Stepan Company reported a 39% EBITDA lift and USD 48 million in annual savings, demonstrating the scale needed to lower unit costs. Smaller entrants often struggle to reach such efficiencies, especially if they must fund compliance upgrades for wastewater, emissions, and worker safety. As a result, new capacity additions remain measured, tempering near-term supply growth in the fatty methyl ester sulfonate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Innovation Expands Liquid Paste Prospects

Powder products accounted for 63.36% of the fatty methyl ester sulfonate market size in 2025, a position secured by stability, shelf life, and ease of bulk transport. Spray-drying lines tailored to FMES allow detergent makers to incorporate enzymes without denaturation, protecting performance at high storage temperatures. Yet R&D breakthroughs in rheology control have propelled liquid paste grades to an 10.86% CAGR, challenging powder dominance. New neutralization methods improve hydrolysis resistance, yielding transparent concentrates that let brands market “cold-wash” liquid detergents.

Granular and flake variants serve commercial laundries that require controlled dissolution in tunnel washers, while gel formats appear in car-wash additives demanding high foam retention. Fermentation-derived rhamnolipids introduced by Evonik illustrate how alternative biosurfactant technologies blur traditional form delineations. As process knowledge spreads, manufacturers will likely fine-tune particle size, moisture, and active-content levels to meet niche application needs, cementing form-based competition within the fatty methyl ester sulfonate market.

By Feedstock Source: Sustainability Reshapes Sourcing Strategies

Palm kernel oil still underpins 81.68% of global FMES output, thanks to robust plantations, reliable fatty-acid profiles, and integrated oleochemical hubs across Malaysia and Indonesia. Mill upgrades under the Malaysian Sustainable Palm Oil 2.0 standard push traceability and greenhouse-gas audits, enabling certified suppliers to capture higher margins. However, coconut oil supply, centered on the Philippines and Indonesia, is expanding at 11.31% annually because brands prize its non-deforestation image and pleasant odor in rinse-off products. Certification programs such as Rainforest Alliance accelerate this shift by rewarding transparent farming practices.

Producers are also trialing soy and tallow methyl esters in regional blends to hedge cost risk and support local agriculture. Unilever’s USD 120 million partnership with Genomatica to develop palm-free surfactant feedstocks exemplifies the strategic push for diversification. In this evolving context, supply-chain resilience and credible certification increasingly determine competitive advantage, anchoring feedstock policy debates in boardrooms linked to the fatty methyl ester sulfonate market.

By End-User Industry: Volume Stability and Margin Upside

Detergents continue to generate the largest revenue block, holding 70.29% of overall demand in 2025. Compact powder detergents remain central within this anchor segment because FMES delivers high foam and easy rinsing even in low-dosage formats. Enzymatic boosters introduced by top brands further enhance wash performance, reinforcing the position of the fatty methyl ester sulfonate market in mass-market laundry products. Institutional cleaning, covering food-service and health-care sites, values FMES for quick biodegradation and safe-handling credentials that help operators comply with sanitary regulations. In contrast, though smaller by volume, personal-care demand posts the fastest 11.02% CAGR as consumers gravitate to sulfate-free shampoos and mild cleansers that command double-digit price premiums versus traditional surfactants.

Personal-care formulators exploit FMES’s balanced hydrophilic-lipophilic profile to design clear shampoos and creamy facial washes with minimal irritation. Premium brands highlight coconut-derived feedstocks on front-of-pack labeling, adding storytelling value that resonates with eco-conscious buyers. The industrial and institutional cleaning sector leverages FMES in concentrated sanitizers, capitalizing on its compatibility with chlorine-based actives. Collectively, these growth pockets diversify revenue streams and help mitigate cyclical swings in detergent volumes, underscoring the resilience of the fatty methyl ester sulfonate market.

Geography Analysis

Asia-Pacific held 57.26% of global revenues in 2025 and is advancing at a 10.82% CAGR through 2031. Abundant palm kernel supplies, an installed base of sulfonation towers, and local demand from China’s detergent majors keep utilization rates high. Malaysia and Indonesia continue to refine oleochemical clusters that bundle feedstock, energy, and logistics advantages. KLK’s decision to expand processing capacity in China underscores the region’s dual role as producer and consumer. That proximity reduces freight costs and shortens order-to-delivery cycles, deepening Asia’s competitive moat within the fatty methyl ester sulfonate market.

North America exhibits slower headline growth yet benefits from regulatory frameworks such as the EPA Safer Choice Program that direct purchasing toward renewable, low-toxicity inputs. Stepan’s new Pasadena, Texas, alkoxylation unit demonstrates a commitment to local capacity as brands seek a secure domestic supply. High consumer willingness to pay for clean-label personal-care products supports added FMES volume despite comparatively higher feedstock costs versus Asia.

Europe’s trajectory is shaped by stringent chemical policy reforms, including updated REACH dossiers and the Detergent Regulation revision that tighten biodegradability and labeling rules. Governments invest in circular-bioeconomy initiatives like SurfToGreen to source surfactants from agricultural side-streams, further embedding FMES in regional supply chains. Eastern Europe offers emerging manufacturing bases for export back into the single market, offsetting Western Europe’s higher labor and energy expenses. Together these patterns add depth to the fatty methyl ester sulfonate market while reinforcing the premium commanded by certified, traceable products.

Competitive Landscape

The fatty methyl ester sulfonate market is moderately concentrated. BASF, Stepan Company, KLK Oleo, Wilmar International, and Lion Corporation collectively hold a significant share by combining integrated feedstock assets with proprietary sulfonation know-how. Strategically, leading players double down on sustainability verification, greenhouse-gas accounting, and traceable sourcing to defend price premiums. Digital monitoring of batch quality and predictive maintenance on sulfonation lines lowers downtime and ensures consistent color and active content, key specifications in premium personal-care grades. R&D races center on greener sulfonation chemistry, improved catalyst recovery, and fully palm-free feedstocks, signaling ongoing innovation cycles within the fatty methyl ester sulfonate market.

Fatty Methyl Ester Sulfonate Industry Leaders

Emery Oleochemicals

KLK Oleo

Lion Corporation

Stepan Company

Wilmar International Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: KLK OLEO, a global oleochemicals producer, has expanded into India with a new representative office in Mumbai—KLK OLEO India (KLKOI). Offering a broad range of basic and specialty products, this move aims to strengthen its presence in the Indian market.

- April 2023: Kuala Lumpur Kepong Bhd (KLK), through its KLK Oleo division, has acquired a controlling stake in Milan-based Temix Oleo SpA for an undisclosed sum. The move strengthens KLK's oleochemicals portfolio and expands its presence in Europe, particularly in specialized products like fatty methyl ester sulfonate.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the fatty methyl ester sulfonate (FMES) market covers all anionic surfactants manufactured by sulfonating fatty-acid methyl esters derived mainly from palm-kernel and coconut oils and sold in powder, flake, or paste form for household detergents, personal-care products, and selected industrial cleaners.

Scope exclusion: Synthetic petroleum-based alkylbenzene sulfonates and non-sulfonated fatty-acid esters are excluded.

Segmentation Overview

- By Form

- Powder

- Granular / Flakes

- Liquid Paste

- By Feedstock Source

- Palm-kernel Oil

- Coconut Oil

- Other Vegetable Oils (e.g., Tallow, Soy)

- By End-User Industry

- Detergents

- Personal Care

- Other End-User Industries (Industrial and Institutional Cleaners, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and email surveys with formulation chemists at detergent makers, oleochemical procurement heads, regional distributors, and regulatory experts across Asia Pacific, Europe, and North America allow us to validate consumption ratios, gauge typical active-matter pricing, and stress-test growth assumptions discussed during desk work.

Desk Research

Our analysts start with public macro data, drawing on sources such as UN Comtrade trade codes for HS 3402, OECD detergent production statistics, FAO oil-seed output, and industry association releases from ACI and APLA to size feedstock and demand pools. Company 10-K filings, customs shipment dashboards, and news streams from Dow Jones Factiva refine price and capacity trends. We supplement these with paid intelligence from D&B Hoovers for producer financials and Questel for patent momentum. The list above is illustrative, not exhaustive; many additional references underpin the dataset vetting.

Market-Sizing & Forecasting

A top-down production-plus-trade rebuild estimates global apparent FMES supply, which is then cross-checked with a selective bottom-up roll-up of major supplier shipments and sampled ASP × volume calculations. Key variables include crude palm-kernel oil output, conversion yields, FMES penetration in powder detergents, regional detergent tonnage, typical active matter concentration, and regulatory bio-based content mandates. A multivariate regression links these drivers to historical market value and feeds an ARIMA overlay for the 2025-2030 outlook, while scenario analysis captures feedstock price swings. Gaps in producer data are bridged through channel checks and averaged import values.

Data Validation & Update Cycle

Outputs face anomaly scans, variance checks versus independent price indices, and a two-step internal peer review before sign-off. Reports refresh yearly, with interim updates if feedstock shocks, capacity additions, or regulatory shifts materially move the baseline. An analyst re-runs the model just before delivery.

Why Mordor's Fatty Methyl Ester Sulfonate Market Baseline Merits High Reliance

Published estimates often diverge because each firm chooses its own product mix, feedstock cost path, and refresh cadence.

Key gap drivers include wider application buckets or aggressive bio-surfactant substitution scenarios elsewhere, currency conversion points that differ from Mordor's mid-year averages, and less frequent updates that miss recent Southeast Asian capacity ramps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.81 B (2025) | Mordor Intelligence | - |

| USD 1.46 B (2024) | Global Consultancy A | Includes broader methyl ester derivatives and applies uniform 22 % CAGR without feedstock constraint checks. |

| USD 0.79 B (2024) | Industry Observatory B | Omits flakes segment and uses 2023 exchange rates, leading to lower converted totals. |

These comparisons show that Mordor's disciplined scope selection, variable-level cross-validation, and annual refresh provide a balanced, transparent baseline that decision-makers can trace back to measurable inputs and repeatable steps.

Key Questions Answered in the Report

What is the current Fatty Methyl Ester Sulfonate Market size?

The fatty methyl ester sulfonate market stands at USD 0.89 billion in 2026 and is projected to reach USD 1.43 billion by 2031.

Which segment generates the largest demand for fatty methyl ester sulfonates?

Detergents dominate, accounting for 70.29% of 2025 revenue due to FMES compatibility with compact powder formulations.

Which region leads growth in the fatty methyl ester sulfonate market?

Asia-Pacific holds 57.26% of global revenue and is expanding at a 10.82% CAGR through 2031 on the back of feedstock availability and booming detergent manufacturing.

What are the main restraints on FMES market growth?

Feedstock price swings and high capital costs for specialized sulfonation equipment weigh on margins and limit rapid capacity expansion.

Page last updated on: