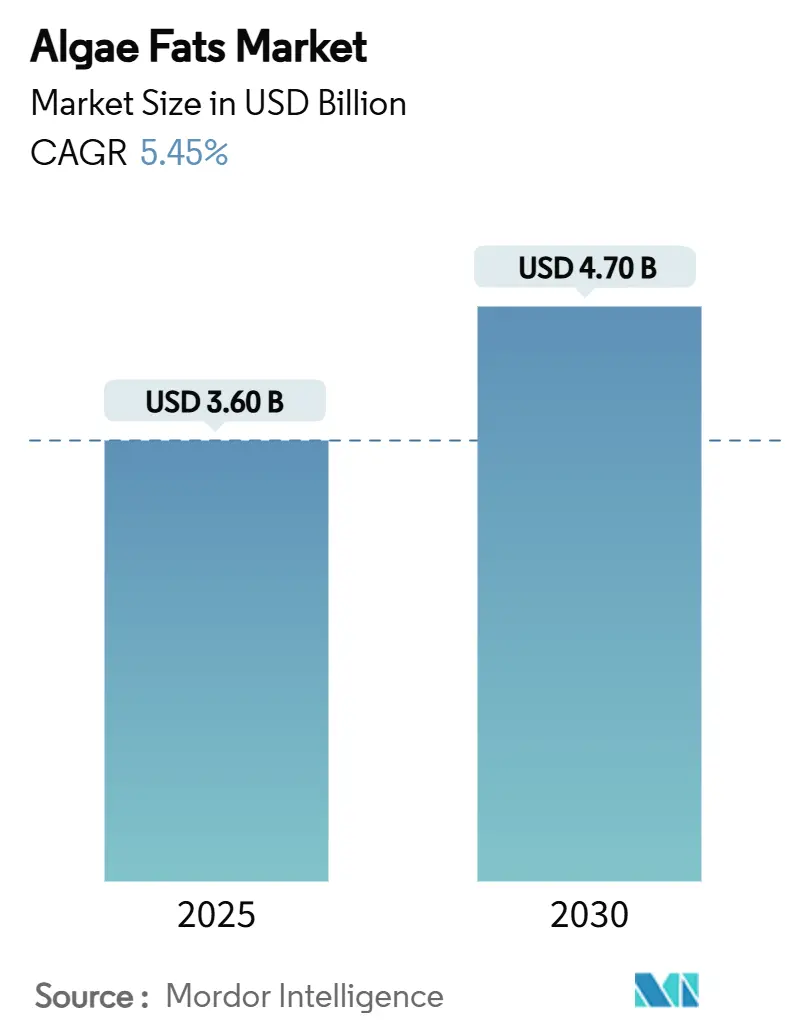

Algae Fats Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 3.60 Billion |

| Market Size (2030) | USD 4.70 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

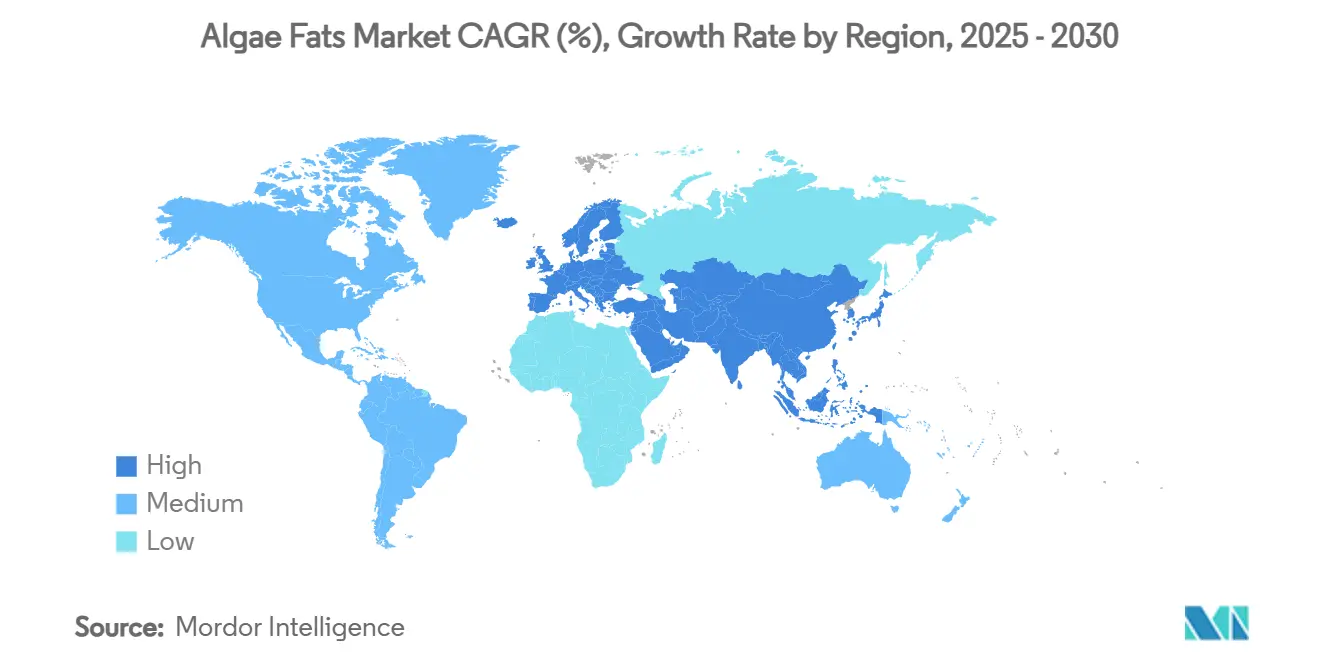

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algae Fats Market Analysis by Mordor Intelligence

The algae fats market size reached USD 3.6 billion in 2025 and is forecast to advance at a 5.45% CAGR, lifting the market value to USD 4.7 billion by 2030. Europe’s leadership drives expansion, the rapid commercialization of heterotrophic fermentation, and a noticeable shift from finite marine ingredients to renewable algal biomass. Asia-Pacific is projected to grow at the fastest rate, driven by China’s dominance in aquafeed production and favorable policy incentives. Microalgae retain a share as the staple raw material, while oil-based formulations capture product forms, underscoring algae’s role in omega-3 replacement. Livestock producers are turning to algae for feed conversion gains and lifecycle greenhouse gas (GHG) labeling advantages. Capacity additions by DSM-Firmenich AG, Corbion N.V., and ADM (Archer Daniels Midland Co.), alongside disruptive startups, demonstrate an industry transitioning from pilot trials to industrial-scale production.

Key Report Takeaways

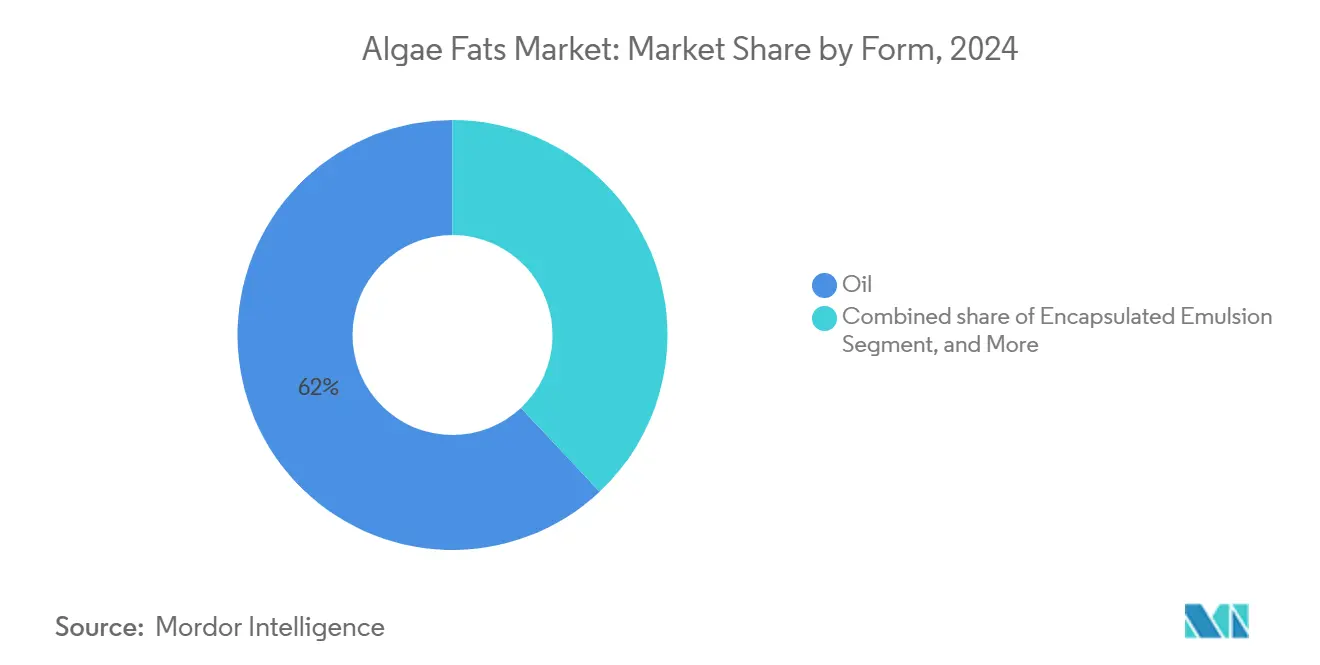

- By form, oil-based products accounted for the largest revenue share of 62% in 2024. Encapsulated emulsions are anticipated to expand at a 22.7% CAGR to 2030.

- By source, microalgae held 72% of the algae fats market share in 2024, while genetically modified strains are projected to grow at a 19.5% CAGR through 2030.

- By application, aquafeed accounted for 46.2% of the algae fats market size in 2024, whereas poultry feed is forecast to climb at an 18.6% CAGR.

- By geography, Europe led with a 36% share in 2024. Asia-Pacific is advancing at a 17% CAGR through 2030.

Global Algae Fats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable omega-3 replacement for fish oil in aquafeed | +2.1% | Global, with early gains in Europe and North America | Medium term (2-4 years) |

| Regulatory pressure to lower fishmeal and fish oil usage | +1.8% | Europe, North America, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Proven feed-conversion-ratio gains in poultry and swine | +1.4% | Global, concentrated in intensive farming regions | Short term (≤ 2 years) |

| Cost declines from large-scale heterotrophic fermentation | +1.2% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Lifecycle-GHG labeling boosts algae-fed meat branding | +0.9% | Europe, North America, premium market segments | Long term (≥ 4 years) |

| Insect-algae co-feed models for circular agriculture | +0.6% | Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainable Omega-3 Replacement for Fish Oil in Aquafeed

Commercial salmon diets can now rely entirely on algal oils without performance losses, as DSM-Firmenich’s Life’s OMEGA O3020 and the Veramaris Nebraska plant bring industrial volumes equivalent to 1.2 million metric tons of fish to market. Food and Drug Administration (FDA) rulings on Schizochytrium sp. confirm regulatory confidence and signal broader livestock adoption [1]Source: U.S. Food and Drug Administration, “GRAS Notice Inventory,” fda.gov. As premium seafood brands highlight carbon-reduced omega-3 sourcing on pack, price insensitivity in high-end retail channels accelerates uptake.

Regulatory Pressure to Lower Fishmeal and Fish Oil Usage

The EU added more than 20 algae species to its Novel Food catalogue in 2024, saving producers EUR 10 million (USD 11 million) in filings and streamlining the path to market [2]Source: European Commission, “Novel Food Catalogue Update,” commission.europa.eu. Similar reforms in India, such as customs-duty relief on shrimp-feed inputs, improve cost competitiveness and spur exports. Food and Drug Administration (FDA) status for Euglena gracilis and other strains provides a transferable template for novel feed approvals. Collectively, these actions reduce legal uncertainty and amplify investor confidence, underpinning the algae fat market’s capacity additions.

Proven Feed-Conversion-Ratio Gains in Poultry and Swine

Broiler studies show that 5% inclusion of Aurantiochytrium limacinum elevates omega-3 levels in meat without raising mortality. In Nile tilapia, Spirulina can substitute up to 30% of fishmeal protein with no growth penalty. Ruminant trials are extending this evidence base, and swine integrators are piloting DHA-rich blends to improve reproductive metrics. As performance data accumulate, nutritionists now treat algae as a strategic ingredient rather than a niche additive, cementing demand in intensive systems.

Cost Declines from Large-Scale Heterotrophic Fermentation

Algenie’s thin-layer photobioreactor targets sub-USD 1/kg biomass costs, a step-change from current ranges. Arborea’s biosolar leaf promises 10-fold lower capital intensity, while AI-guided fermentation raises lipid yields as much as 43%. Waste-stream utilization exemplified by MiAlgae’s whisky-byproduct model turns disposal liabilities into feedstocks. Together, these advances narrow the cost gap with soybean oil and accelerate bankability for greenfield projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus soybean and canola oils | -1.9% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Pellet durability and handling issues at high inclusion rates | -1.2% | Global, affecting feed mill operations | Medium term (2-4 years) |

| Batch-to-batch Eicosapentaenoic Acid/Docosahexaenoic Acid variability | -0.8% | Global, quality-critical applications | Medium term (2-4 years) |

| Supply-security skepticism among integrated feed mills | -0.7% | Global, conservative procurement strategies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Premium Versus Soybean and Canola Oils

Microalgae costs currently outstrip conventional oils, reaching USD 2.8–315/kg. That price delta restricts adoption to premium channels where performance or branding gains offset higher input spend. Energy-intensive cultivation and downstream dewatering remain the key cost drivers, though modular thin-layer reactors and waste-stream feedstocks are bringing break-even costs within range of mainstream commodities.

Batch-To-Batch Eicosapentaenoic Acid/Docosahexaenoic Acid Variability

Variability in eicosapentaenoic acid/docosahexaenoic acid profiles complicates formulation, as late stationary growth phases increase eicosapentaenoic acid while docosahexaenoic acid plateaus. Laboratory methods lack standardization, resulting in inconsistent readings for protein and lipid levels. Feed mills demand predictable specifications, so producers are investing in inline analytics and ISO-compliant quality controls to reduce rejection rates and reassure formulators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Encapsulated Emulsions Address Handling Challenges

Oil-based products captured a 62% share in 2024. Liquid forms enable direct omega-3 dosing and seamless inclusion, yet susceptibility to oxidation and pellet durability issues limit high-rate usage in pelleted diets. Encapsulated emulsions, forecasted to grow at a 22.7% CAGR, address both hurdles by protecting lipids and enhancing flowability. Studies confirm that improved pellet hardness and reduced fat leakage occur when microalgae are microencapsulated. Powdered formats maintain relevance in premixes where moisture control is pivotal.

The shift toward encapsulated forms reflects the industry's maturation from laboratory-scale applications to industrial feed manufacturing, where processing requirements and quality consistency take precedence over raw material costs. Advanced encapsulation technologies using phospholipids enhance bioavailability while providing protection against environmental degradation, creating premium product segments that justify higher pricing.

By Source: Genetically Modified Strains Drive Innovation

Microalgae commanded 72% of the algae fats market size in 2024. Adoption rests on mature cultivation chains for Spirulina and Chlorella. Genetically modified microalgae, although nascent, are projected to post a 19.5% CAGR, fueled by engineered nutrient profiles, faster growth, and policy support in China’s bio-economy. The regulatory landscape for GM microalgae is evolving favorably, with synthetic biology advances reducing safety concerns and improving economic viability, particularly in China, where the microalgae biofuel industry shows strong government support

In parallel, traditional microalgae continue to scale through fermentation infrastructure now repurposed from bio-ethanol and pharmaceutical lines. The segment’s durability stems from supply reliability and universal feed regulatory acceptance, making it a baseline ingredient, even as engineered strains penetrate premium niches. Wild-type strains maintain advantages in regulatory approval timelines and consumer acceptance, particularly in organic and natural product segments where genetic modification restrictions are in place.

By Application: Poultry Feed Adoption Accelerates

Aquafeed held a 46.2% market share of the algae fats market in 2024, aligning with salmon, shrimp, and trout producers' mandates to reduce fish-oil dependency. Complete fish-oil replacement trials with Veramaris oil underline performance parity and sustainability messaging that resonates in export-oriented seafood chains. Poultry feed, meanwhile, is set to grow at an 18.6% CAGR as integrators target omega-3-enriched chicken and eggs. Clinical work on Aurantiochytrium limacinum demonstrates the safe inclusion of up to 5%, enhancing DHA levels without performance degradation.

Specialty feed additives and premixes represent emerging high-value applications where algae's bioactive compounds provide functional benefits beyond basic nutrition. Pet nutrition applications show strong growth potential, with companies like PhytoSmart and Cellana merging to target the USD 10 billion global pet and human supplement market. Ruminant feed applications face challenges from the complex digestive systems of these animals, which may limit the efficiency of algae utilization. However, research continues on processing methods to enhance bioavailability in cattle and sheep diets.

Geography Analysis

Europe maintained a 36% share of the algae feed market in 2024, driven by stringent sustainability mandates, a mature salmon sector, and consumer preference for eco-labels. Norway’s feed majors, BioMar and Skretting, anchor demand, while EU Novel Food reforms are projected to drive algae demand across value chains by 2030. Financial instruments such as Horizon Europe grants de-risk R&D, and retailers consistently reward lower-carbon seafood provenance at the checkout.

The Asia-Pacific region delivers the highest 17% regional CAGR, as China, the world’s largest aquafeed manufacturer, commissions facilities like Calysseo’s 20,000 metric tons plant in Chongqing. Government-backed demonstration farms showcase algae-fed shrimp for premium export markets. India’s tariff relief on shrimp-feed inputs and Vietnam’s low-cost biomass cultivation ecosystems further stack the regional growth trajectory, bringing new entrants into the algae feed industry.

North America is progressing steadily in capital deployment and regulatory certainty. Veramaris’ USD 200 million Nebraska plant underpins regional supply and captures 15% of global salmon omega-3 demand. The FDA’s Generally Recognized as Safe (GRAS) affirmations lower legal barriers, and a robust venture capital network funds next-generation photobioreactor startups. Cross-border with Canadian aquaculture clusters foster technology transfer and bolster continental self-sufficiency.

Competitive Landscape

Competitive intensity is moderate, with multinationals and biotech start-ups coexisting. DSM-Firmenich AG anchors the front line, pairing its life’s OMEGA portfolio with Veramaris’ Nebraska output that alone can replace 1.2 million metric tons of fish. Corbion N.V.'s AlgaPrime DHA fermentation is projected to achieve significant sales growth by 2028 and diversify into the pet nutrition market [3]Source: Corbion Investor Relations, “Strategy Update 2024,” corbion.com. ADM (Archer Daniels Midland Co.) and Cargill Inc. integrate algae into bundled feed solutions, utilizing their distribution networks for market penetration.

Disruptive newcomers focus on cost and flexibility. Algenie’s thin-layer reactor promises lower capex, while Arborea’s biosolar leaf leverages sunlight over artificial LEDs to cut power bills. MiAlgae’s circular model monetizes whisky industry effluents, demonstrating alternative economics for feedstock. Strategic moves include joint ventures (Adisseo-Calysta), capacity expansions, and mergers and acquisitions (M&A), such as JRS’s acquisition of Algaia to integrate seaweed inputs into animal nutrition.

Success differentiators now center on achieving cost parity with plant oils, ensuring supply reliability, and verifying sustainability metrics. Players achieving sub-USD 1/kg costs with stable omega-3 profiles are poised to gain share as mainstream buyers shift volume from fish oil to algal alternatives. Investors gravitate toward platforms that couple low energy demand with modular scalability, anticipating that price parity with soybean oil will unlock mass-market adoption. Mergers such as the 2024 union of PhytoSmart and Cellana show early consolidation aimed at assembling broader strain libraries and downstream application reach.

Algae Fats Industry Leaders

DSM-Firmenich AG

ADM (Archer Daniels Midland Co.)

BASF SE

Corbion N.V.

Cargill Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Algiecel secured EUR 6.5 million in equity funding to scale microalgae production for feed and food industries, supporting transition from pilot operations to full-size demonstration plant as part of the CAPCO2 project targeting CO2-emitting industries.

- October 2024: PhytoSmart Inc. and Cellana Inc. signed a merger agreement to enhance omega-3 algae strain production capabilities, with the combined company targeting both pet and human supplement markets exceeding USD 10 billion globally using Cellana's ALDUO technology.

- April 2024: Edonia secured EUR 2 million investment for microalgae-based protein development, focusing on spirulina and chlorella with proprietary 'edonization' process creating meat-like texture while avoiding EU Novel Food classification requirements.

Global Algae Fats Market Report Scope

| Oil |

| Powder |

| Encapsulated Emulsion |

| Microalgae |

| Genetically Modified Microalgae |

| Aquafeed |

| Poultry Feed |

| Swine Feed |

| Ruminant Feed |

| Pet Nutrition |

| Specialty Feed Additives & Premixes |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Norway |

| United Kingdom | |

| Germany | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Form | Oil | |

| Powder | ||

| Encapsulated Emulsion | ||

| By Source | Microalgae | |

| Genetically Modified Microalgae | ||

| By Application | Aquafeed | |

| Poultry Feed | ||

| Swine Feed | ||

| Ruminant Feed | ||

| Pet Nutrition | ||

| Specialty Feed Additives & Premixes | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | Norway | |

| United Kingdom | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the algae feed market?

The algae feed market size stood at USD 3.6 billion in 2025 and is projected to reach USD 4.7 billion by 2030.

Which region leads the algae feed market?

Europe leads with a 36% share, propelled by strict sustainability rules and mature aquaculture sectors.

Why are algal oils important in aquafeed?

Algal oils replace fish oil as a sustainable eicosapentaenoic acid/docosahexaenoic acid source, enabling salmon diets that meet omega-3 needs without depleting wild fish stocks.

Which application will grow fastest through 2030?

Poultry feed is forecast to expand at an 18.6% CAGR due to proven feed-conversion gains and consumer demand for omega-3-enriched meat.

How are costs declining for algae feed?

Next-generation thin-layer photobioreactors, AI-optimized fermentation, and waste-stream substrates are pushing production costs toward USD 1/kg.

What is the main barrier to algae feed adoption?

A price premium over conventional oils remains the key hurdle, though scaling technologies are narrowing the gap.

Page last updated on: