Bioherbicides Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

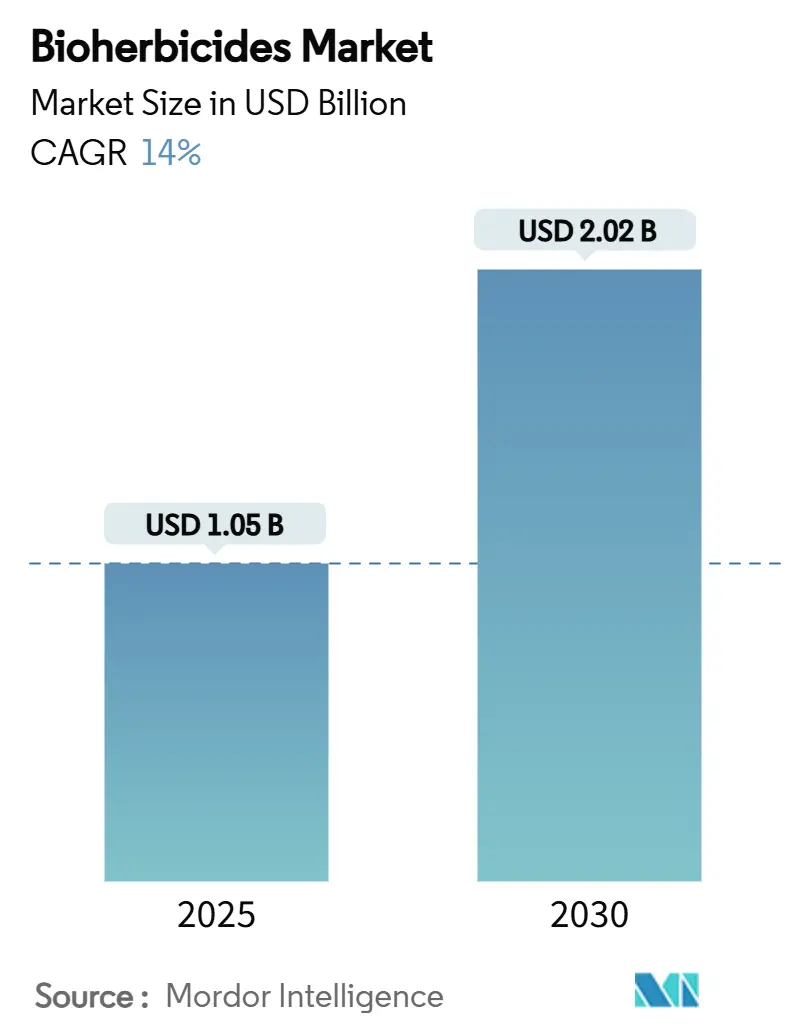

| Market Size (2025) | USD 1.05 Billion |

| Market Size (2030) | USD 2.02 Billion |

| Growth Rate (2025 - 2030) | 14.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

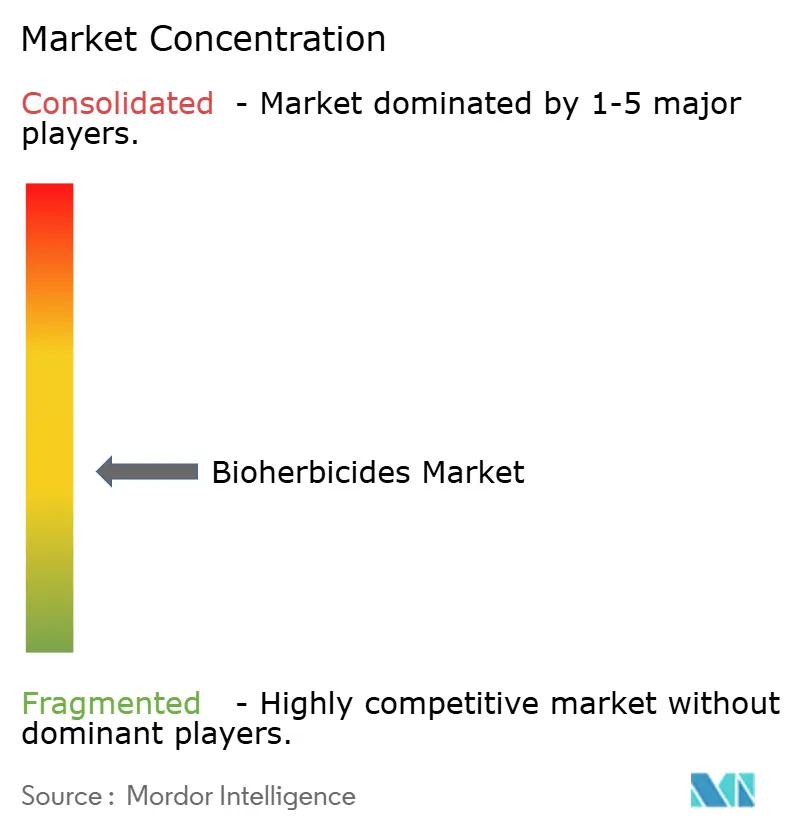

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioherbicides Market Analysis by Mordor Intelligence

The bioherbicides market size reached USD 1.05 billion in 2025 and is forecast to attain USD 2.02 billion in 2030, advancing at a 14.0% CAGR during 2025-2030. Rising regulatory phase-outs of synthetic herbicides, the spread of herbicide-resistant weeds, and breakthroughs in RNA-interference and peptide technologies are accelerating global demand. Intensifying pressure from glyphosate-resistant species across major row-crop regions is steering growers toward biological solutions that protect yields while satisfying residue limits set by premium food retailers. Public and private investment is expanding as multinational agrochemical firms earmark billion-dollar biological revenue targets, and carbon-credit schemes reward low-residue inputs, strengthening the growth outlook for the bioherbicides market. North America leads adoption owing to streamlined EPA approvals, while Asia-Pacific registers the fastest gains on the back of rapid scale-up in China and India. Competitive dynamics favor innovators that combine microbial know-how with next-generation RNA-based delivery platforms, creating room for both start-ups and incumbents to capture untapped acreage.

Key Report Takeaways

- By source, microbial solutions held 47% of the bioherbicides market share in 2024, whereas biochemicals (plant extracts, allelochemicals) are forecast to post a 21.5% CAGR to 2030, the fastest among all sources.

- By formulation, liquid suspensions led with 52.3% revenue in 2024, yet encapsulated or micro-encapsulated formulations are projected to expand at a 19.3% CAGR through 2030.

- By mode of application, foliar sprays dominated sales in 2024, accounting for 40% of the revenue, while seed treatments represented the highest growth trajectory, with a 18.9% CAGR during the forecast period.

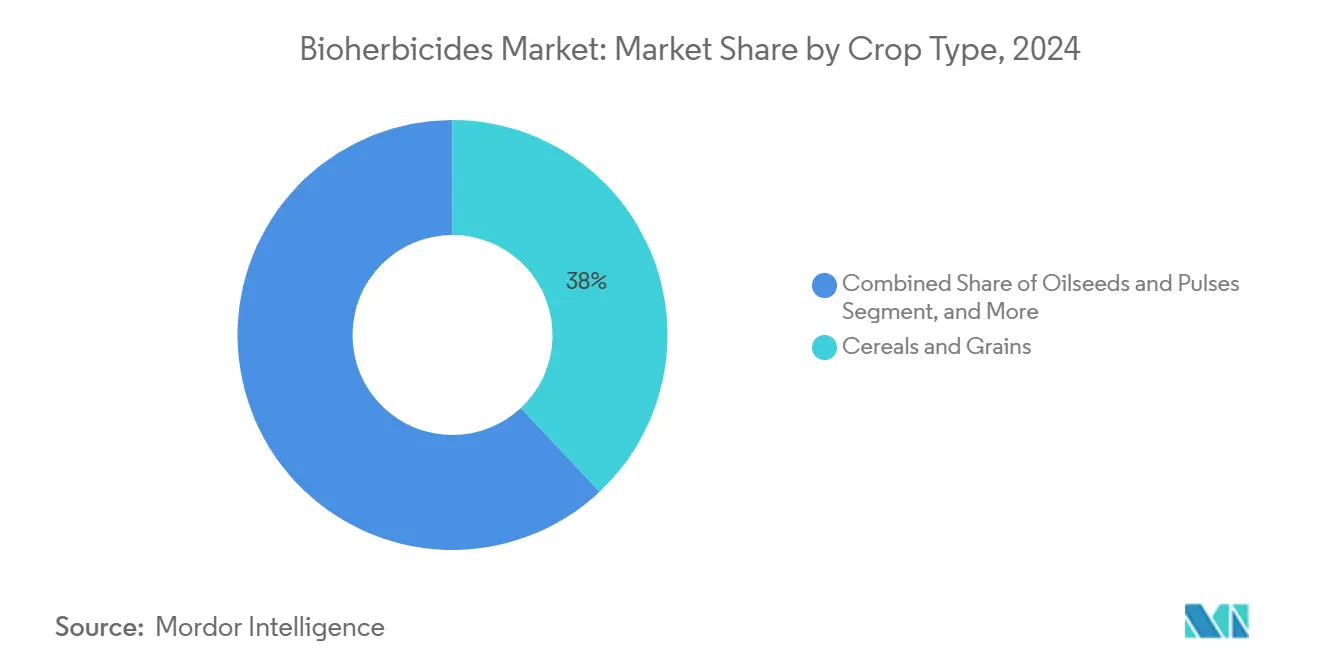

- By crop type, cereals and grains captured the largest share of the bioherbicides market size in 2024, and oilseeds and pulses are anticipated to grow at a 20.2% CAGR due to the mounting resistance to glyphosate in soybean and canola fields.

- By geography, North America contributed roughly 44% of 2024 revenues, and the Asia-Pacific region is forecast to accelerate at a 19.8% CAGR to 2030, driven by the adoption of biological solutions in China and India.

- The top five suppliers hold a significant share confirming a moderately fragmented structure that rewards differentiation.

Global Bioherbicides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to organic farming systems | +2.30% | Global, especially North America and Europe | Medium term (2-4 years) |

| Regulatory phase-outs of synthetic herbicides | +2.80% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Escalating herbicide-resistant weed pressure | +3.10% | Global, acute in North America and Brazil | Short term (≤ 2 years) |

| Advances in encapsulation and shelf-life technologies | +1.90% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Carbon-credit programs rewarding low-residue inputs | +1.40% | North America and EU, pilots in Asia-Pacific | Long term (≥ 4 years) |

| RNA-interference and peptide bioherbicide pipeline | +2.70% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Organic Farming Systems

Rising consumer preferences for chemical-free produce have pushed certified organic acreage past 75 million ha in 2024, widening the addressable bioherbicides market [1]Source: Food and Agriculture Organization, “World Organic Agriculture Statistics 2024,” fao.org. Retailers now seek traceable, low-residue supply chains that mainstream growers can satisfy through biological weed control, especially in fruits and vegetables where premium pricing offsets higher input costs. The European Union’s Farm to Fork strategy requires a 50% cut in synthetic pesticide use by 2030, driving immediate substitution demand. Brazil’s bio-input sales climbed to BRL 5 billion (USD 1 billion) in 2024, and soybeans alone account for over half of domestic biological herbicide volumes. Specialized bioherbicide blends that target crop-specific weed spectra are proliferating, enabling growers to maintain export certifications and avoid maximum residue violations.

RNA-Interference and Peptide Bioherbicide Pipeline

Next-generation products deliver double-stranded RNA that induces gene silencing in weeds, achieving high specificity while sparing crops and beneficial organisms. Polymer nanocarriers protect dsRNA from UV degradation, thereby extending the field persistence and enabling foliar or seed-coat delivery. The United States Patent and Trademark Office (USPTO) lists 268 RNAi pest-control patent families, illustrating robust pipeline activity. Peptide herbicides targeting photosystem II provide complementary mechanisms, bolstering the long-term growth of the bioherbicides market.

Escalating Herbicide-Resistant Weed Pressure

More than 250 weed species now resist at least one mode of action of herbicides, resulting in growers incurring USD 43 billion per year in lost yield and additional inputs. Recent confirmation of glyphosate-resistant goosegrass in Japan, driven by EPSPS (5-enolpyruvylshikimate-3-phosphate synthase) mutations, underscores the rapid spread of resistance genes. Bioherbicides provide alternative biochemical pathways and living antagonists that suppress resistant biotypes. Harpe Bioherbicide Solutions reported efficacy on 30+ resistant species during 1,000 greenhouse and field trials completed in 2024. Integrated programs that combine biological sprays with reduced-rate synthetic products delay the evolution of resistance and enhance crop yields.

Carbon-Credit Programs Rewarding Low-Residue Inputs

Carbon registries across North America and Europe now issue credits for regenerative practices, including reduced synthetic herbicide loads that lower nitrous oxide emissions. Growers adopting biological weed control gain new revenue streams, partially offsetting higher application costs. Early participation in pilot schemes boosts return on investment and encourages broader acreage enrollment, supporting sustained uptake of bioherbicide technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short field persistence needing repeat applications | -2.10% | Global, especially arid zones | Short term (≤ 2 years) |

| High unit cost versus generic synthetics in broad-acre crops | -1.80% | Global, most acute in price-sensitive markets | Medium term (2-4 years) |

| Inconsistent performance under extreme climates | -1.50% | Tropical and arid regions, intensifying with climate change | Medium term (2-4 years) |

| Fragmented global approval paths for live microbials | -1.20% | Global, varying complexity by country | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short Field Persistence Needing Repeat Applications

Most microbial bioherbicides remain active only 7-14 days, forcing multiple passes that raise labor costs. Research shows Fusarium oxysporum chlamydospore formulations outperform microconidia, yet all lose efficacy after prolonged field exposure. Reapplication economics become prohibitive in corn and soybean operations exceeding 4,000 ha. Encapsulated formulations extend activity windows, but inherent biological decay still limits season-long control relative to single-shot synthetics.

High Unit Cost Versus Generic Synthetics in Broad-Acre Crops

Glyphosate pricing fell 13% in 2024, widening the premium commanded by bioherbicides in commodity crops. Fermentation and cold-chain requirements inflate the cost of goods. Economic modeling suggests biologicals must deliver at least a 20% yield or soil-health benefit to neutralize the price gap. Premium fruit and organic segments absorb the differential, but price-sensitive growers delay adoption until proven cost-effectiveness improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Dominance Faces RNA-Based Disruption

Microbial agents held the largest share of the market at 47% in 2024, reflecting mature production systems and well-established regulatory frameworks that underpin the bioherbicides market. The bioherbicides market size for microbial solutions is projected to grow at a comparatively moderate rate as alternative technologies gain ground. Growth persists because growers value proven field results and cost profiles that improve when fermentation capacity scales up.

Biochemicals (plant extracts, allelochemicals) products are the breakout segment, forecasted to expand at a 21.5% CAGR and capture an 18% share by 2030. These naturally derived compounds offer selective weed control with low environmental persistence, aligning with tightening residue regulations and pollinator protection standards. Backed by increasing venture interest and evolving regulatory support for botanical actives, this segment is rapidly advancing from niche to mainstream.

By Formulation: Liquid Suspensions Lead Despite Encapsulation Surge

Liquid suspensions commanded 52.3% of 2024 revenue, reflecting seamless integration with farm sprayers and tank-mix flexibility. Farmers appreciate the ability to co-apply nutritional and crop-protection inputs, which lowers operational passes and protects margins. The segment’s projected to growing stems from incremental enhancements in surfactant systems and microbial stabilizers that extend shelf-life without refrigeration.

Encapsulated or Microencapsulated formulations are advancing at a faster rate of 19.3% CAGR, as nanocellulose and lipid-based carriers shield actives from UV degradation. Encapsulation enables once-per-season programs in orchards and vineyards, reducing labor. With leading firms converting liquid products into encapsulated formats, the bioherbicides market for encapsulated or microencapsulated solutions is poised for significant growth by 2030, reshaping the competitive landscape.

By Mode of Application: Foliar Spray Dominance Challenged by Soil Innovation

Foliar sprays generated 40% of the bioherbicides market revenue in 2024 due to immediate plant-contact efficacy and easily observable results. Growers trust foliar delivery for post-emergence rescue treatments, especially when resistance breakthroughs threaten yields. The segment continues to record double-digit expansion as application equipment becomes more precise and drone-enabled.

Soil treatments and seed coatings are scaling quickly on the back of innovations that allow bioherbicide microbes to colonize the rhizosphere and suppress germinating weed seeds. Myrothecium verrucaria shows 95% hemp sesbania control when applied pre-emergence, matching synthetic benchmarks at lower environmental risk. As seed companies bundle biological coatings with elite genetics, seed-treatment revenue is poised to rise 18.9% annually through 2030, narrowing the gap with foliar dominance.

By Crop Type: Cereals Lead While Specialty Crops Drive Innovation

Cereals and grains accounted for the largest revenue contribution of 45% in 2024, thanks to their vast acreage in corn, wheat, and rice. The bioherbicides market share for cereals stood at significant, driven by escalating resistance to ALS- and EPSPS (5-enolpyruvylshikimate-3-phosphate synthase)-inhibiting synthetic herbicides. Public-sector extension programs in the United States and Brazil are validating biological mixes that sustain yields even under heavy weed pressure, solidifying demand.

Oilseeds and pulses form the fastest-growing crop group with a 20.2% CAGR as soybean growers confront widespread glyphosate failure. Specialty crops such as fruits, vegetables, and ornamentals foster high-margin pilots of RNA-interference sprays that promise residue-free labels. These high-value segments incubate technology refinements that later migrate to broad-acre markets, acting as a proving ground for efficacy and economics.

Geography Analysis

North America retained its leadership position with 44% revenue in 2024, driven by clear EPA guidelines and extensive extension support that accelerates grower confidence. Registrations for 24 microbial actives since 1972, along with a steady pipeline of RNA-based dossiers, keep product launches flowing. Near-term growth remains robust as carbon markets in the United States reward lower synthetic herbicide footprints, and Canada’s Pest Management Regulatory Agency (PMRA) expedites the approval of biological product labels.

Asia-Pacific emerges as the fastest area of expansion, posting a 19.8% CAGR during 2025-2030. China’s biopesticide consumption is projected to surge by 2025, reflecting a strong shift toward sustainable crop protection, while India’s bio-agriculture sector is anticipated to nearly double in value, signaling growing mainstream adoption across emerging markets. Government grants, startup incubators, and state procurement of bio-inputs spur rapid commercial scale. Japan’s clarified rules for genome-edited organisms reduce uncertainty for developers of topical RNA silencing sprays, inviting cross-border collaborations.

Europe maintains a significant share, anchored by the Farm to Fork mandate to reduce chemical pesticide use by 50% by 2030. Public sentiment strongly favors residue-free produce, prompting supermarket chains to secure long-term biological supply contracts. South America is a growing market, with Brazil’s BRL 5 billion (USD 1 billion) bio-input sector serving soybean and corn growers eager to curb resistance spirals. The Middle East and Africa markets, respectively, benefit from government subsidies that lower upfront costs for biological inputs and compensate for water scarcity challenges.

Competitive Landscape

The top five suppliers hold roughly 39.5% of combined global sales, confirming a moderately fragmented structure that rewards differentiation. Pro Farm (Marrone Bio Innovations), Certis Biologicals, and Valagro (Syngenta Biologicals) leverage legacy discovery pipelines plus distribution muscle to maintain scale. Emerging players like Harpe Bioherbicide Solutions are gaining traction with next-generation, non-GMO formulations, while Emery Oleochemicals brings expertise in sustainable oleochemical-based actives to the space.

Start-ups, including Harpe Bioherbicide Solutions, raised USD 10.5 million in 2024 to commercialize mint-derived chemistries lethal to resistant Amaranthus species. Platform players are converging microbial agents with synthetic enhancers that broaden temperature and pH operating ranges. Syngenta’s tie-ups with Intrinsyx Bio for endophyte nutrient enhancers and with Provivi for pheromone integration illustrate the growing role of partnerships in capturing multipoint farm budgets.

Patent activity is brisk, nearly 268 RNA-interference pest-control patent families exist, providing defensive moats around delivery methods and target genes. As licensing gains importance, intellectual property competence becomes a deciding factor for sustained leadership. Suppliers that marry robust patent portfolios with manufacturing scale will shape the next phase of bioherbicides market consolidation.

Bioherbicides Industry Leaders

Certis USA L.L.C.

Harpe BioHerbicide Solutions, Inc

Pro Farm Group Inc.

Valagro(Synegnta Biologicals)

Emery Oleochemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bayer unveiled Vyconic soybeans featuring tolerance to five herbicide classes, enabling reduced synthetic load and greater fit for biological programs, including bioherbicides.

- May 2024: Harpe Bioherbicide Solutions completed over 1,000 trials on 30 resistant weed species, advancing EPA registration filings.

- April 2024: Seipasa developed a new bioherbicide in collaboration with the Polytechnic University of Valencia to address the decreasing availability of synthetic herbicides in the European Union.

Global Bioherbicides Market Report Scope

| Microbial |

| Biochemical |

| Others |

| Liquid Suspension |

| Dry Granules and Wettable Powders |

| Encapsulated or Micro-encapsulated |

| Foliar Spray |

| Soil Treatment |

| Seed Treatment |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Turf and Ornamentals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Kenya | |

| Nigeria | |

| Rest of Africa |

| By Source | Microbial | |

| Biochemical | ||

| Others | ||

| By Formulation | Liquid Suspension | |

| Dry Granules and Wettable Powders | ||

| Encapsulated or Micro-encapsulated | ||

| By Mode of Application | Foliar Spray | |

| Soil Treatment | ||

| Seed Treatment | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected CAGR of the bioherbicides market from 2025 to 2030?

The market is expected to grow at a 14.0% CAGR during 2025-2030

Which region will expand the fastest through 2030?

Asia-Pacific is forecast to post the fastest growth at a 19.8% CAGR, propelled by adoption in China and India .

Which source category currently dominates the bioherbicides market?

Microbial agents hold the largest share at 47%, owing to mature fermentation processes and established regulatory pathways .

How do encapsulated formulations benefit growers?

Encapsulation lengthens shelf-life, shields actives from UV degradation, and can cut application frequency, making biological weed control more cost-effective .

Why are RNA-interference bioherbicides considered a breakthrough?

They silence specific weed genes without harming crops or non-target organisms, delivering precision control and supporting residue compliance .

Page last updated on: